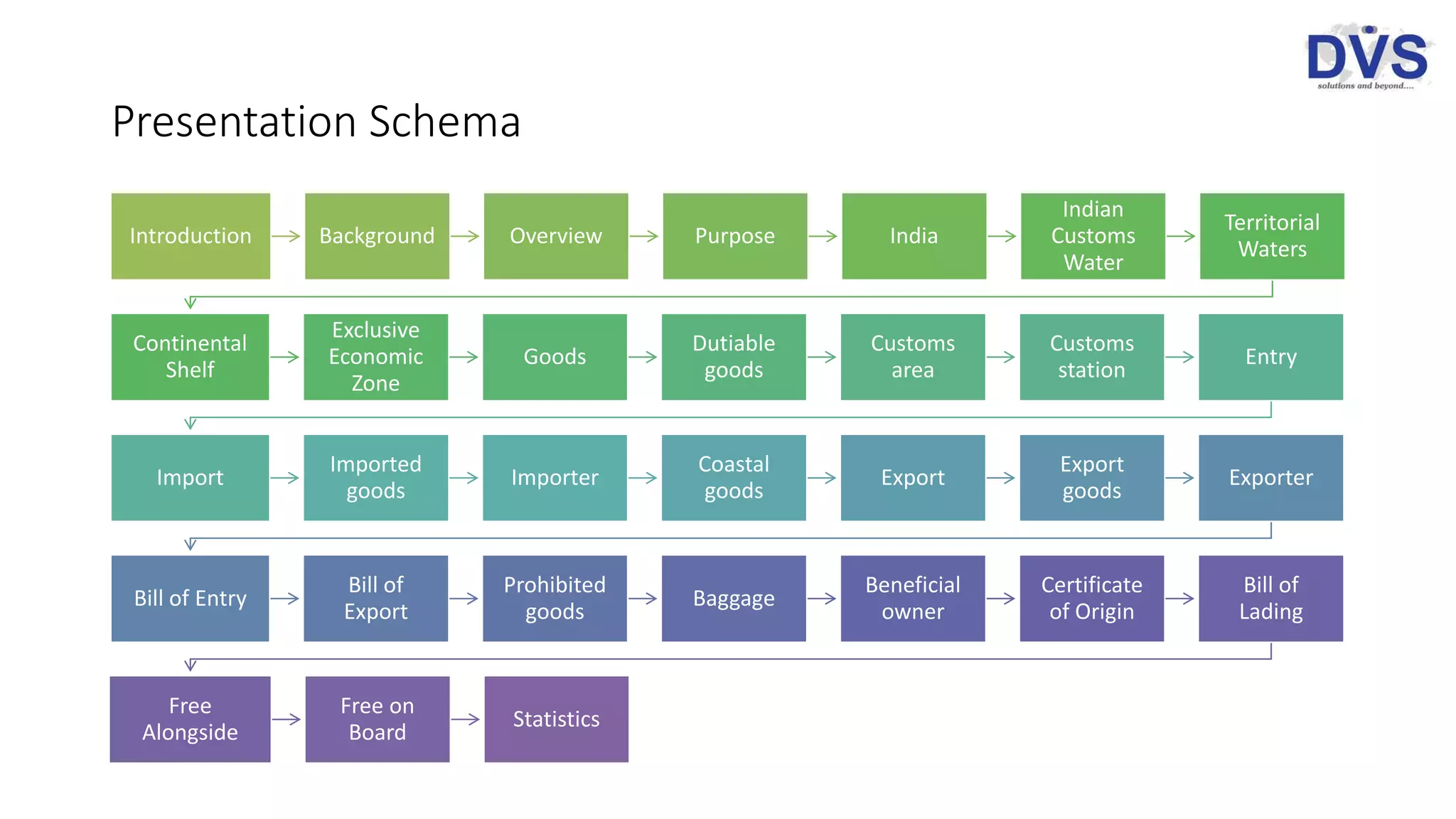

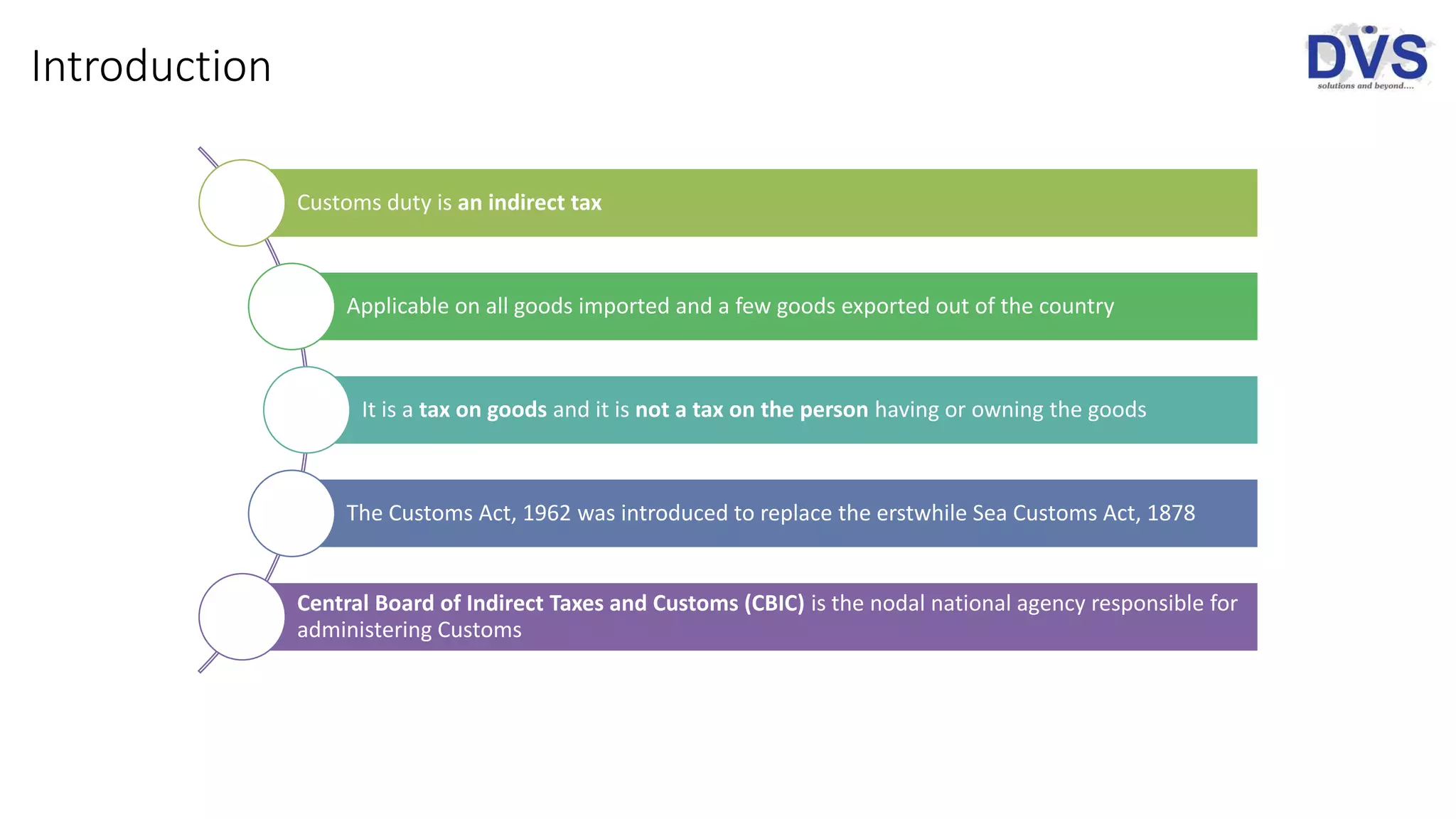

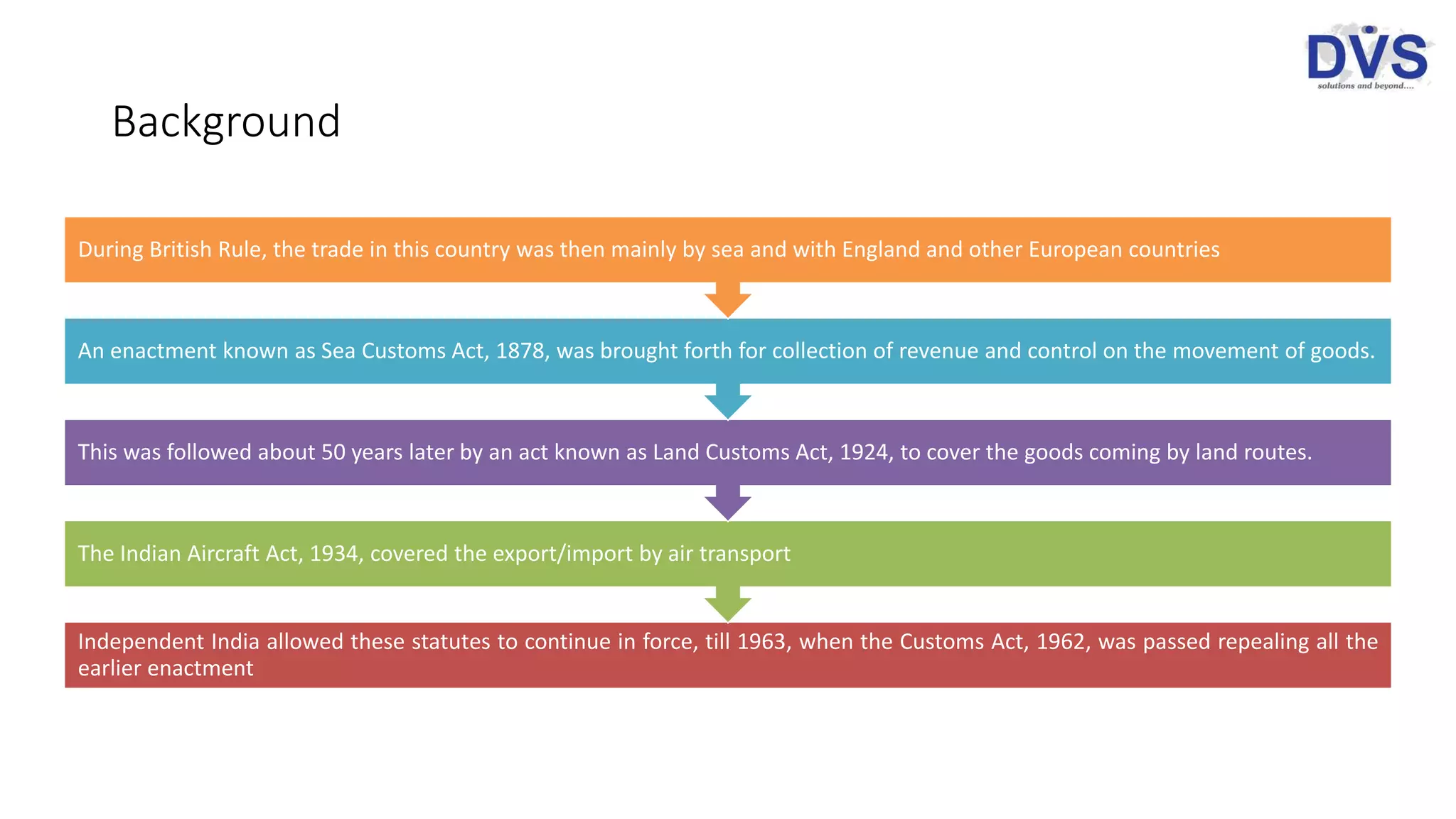

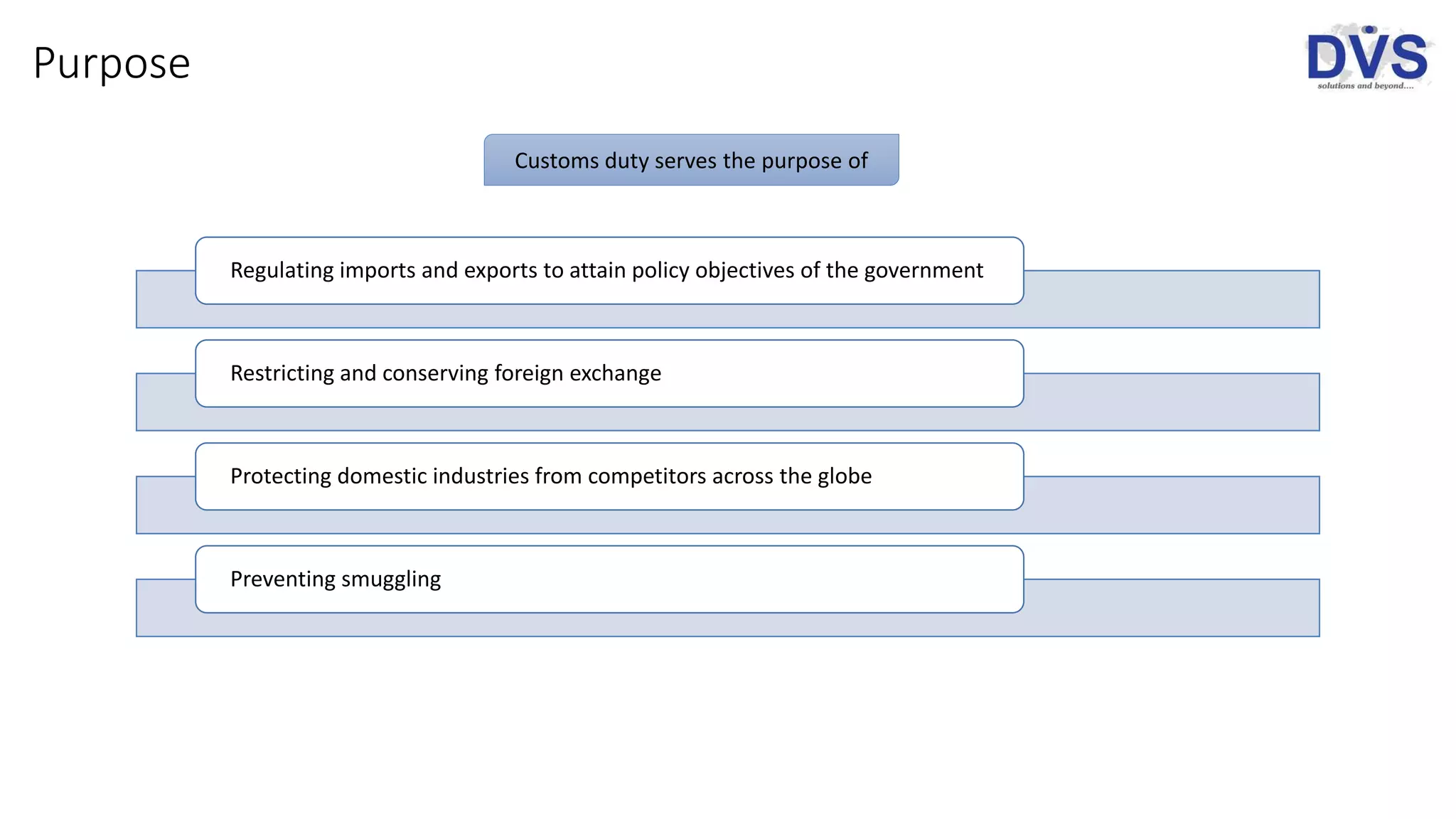

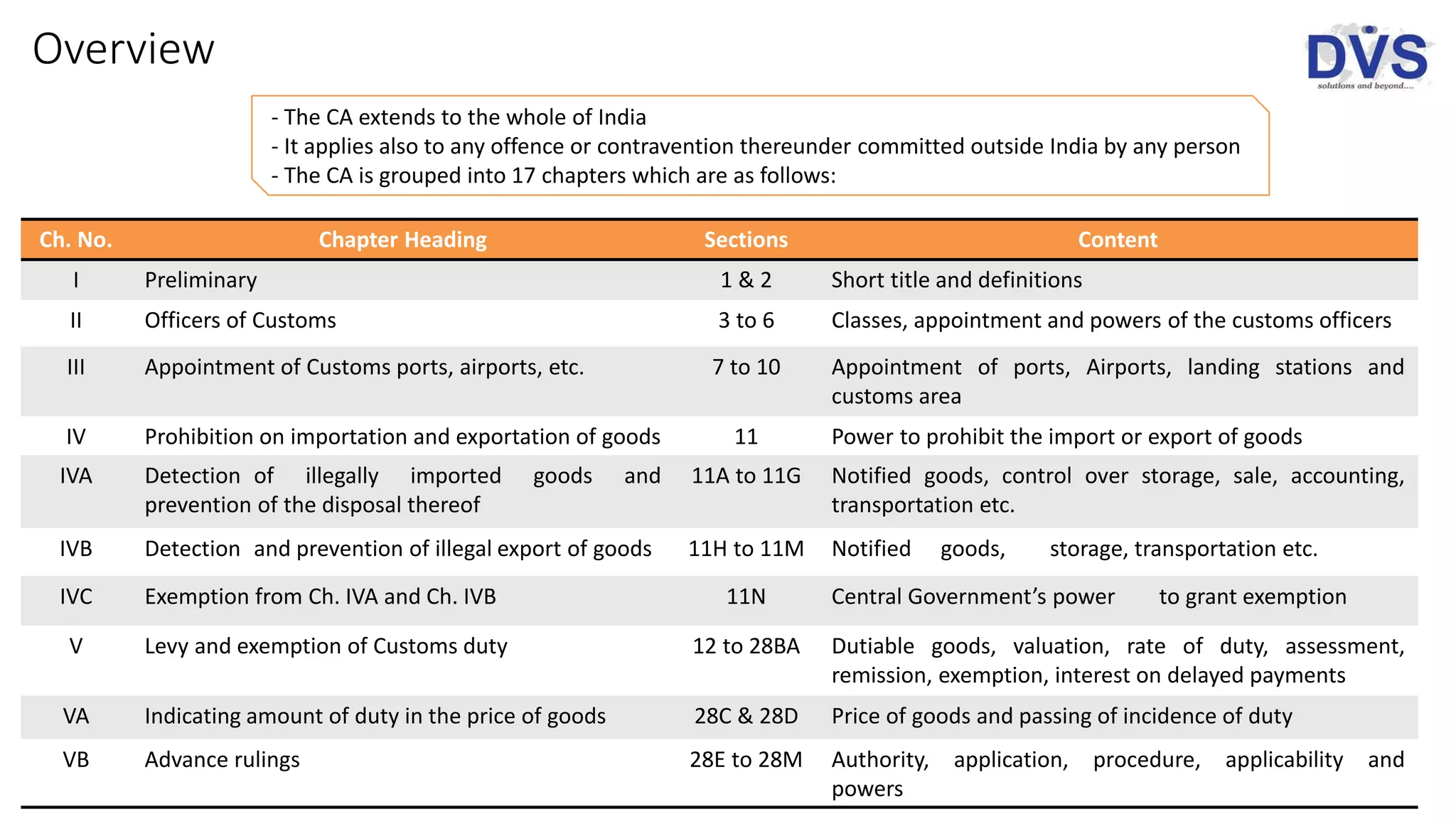

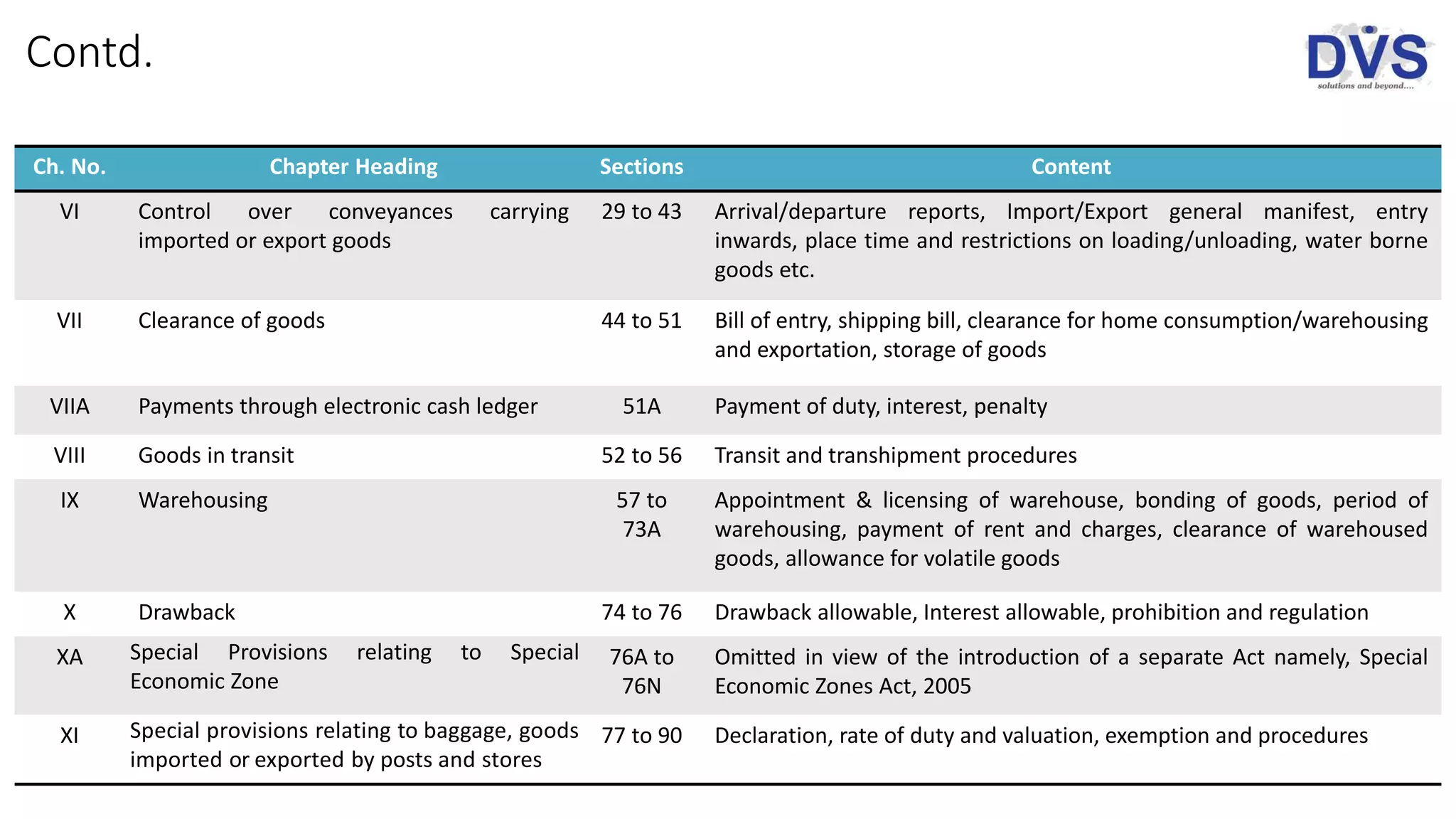

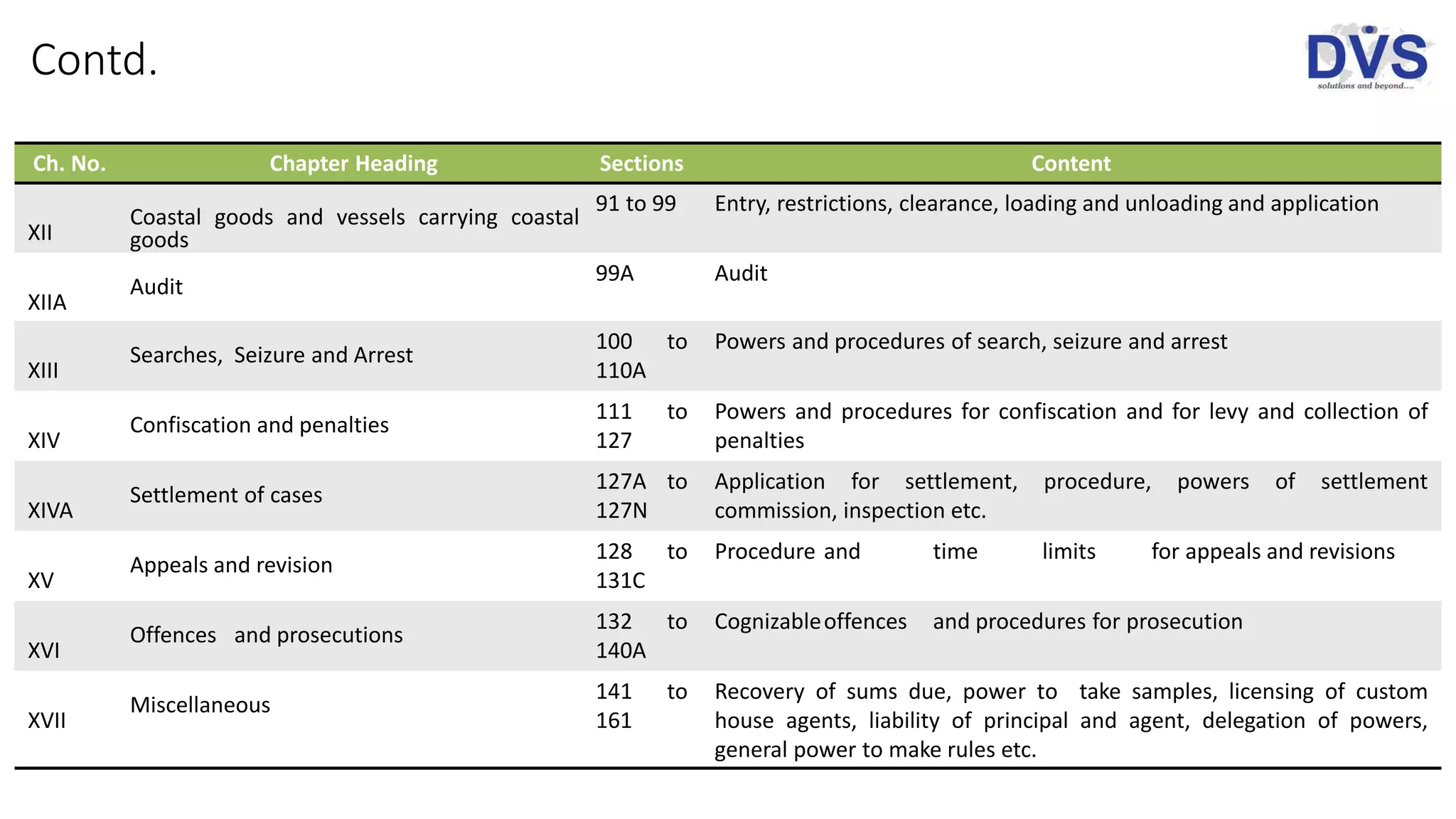

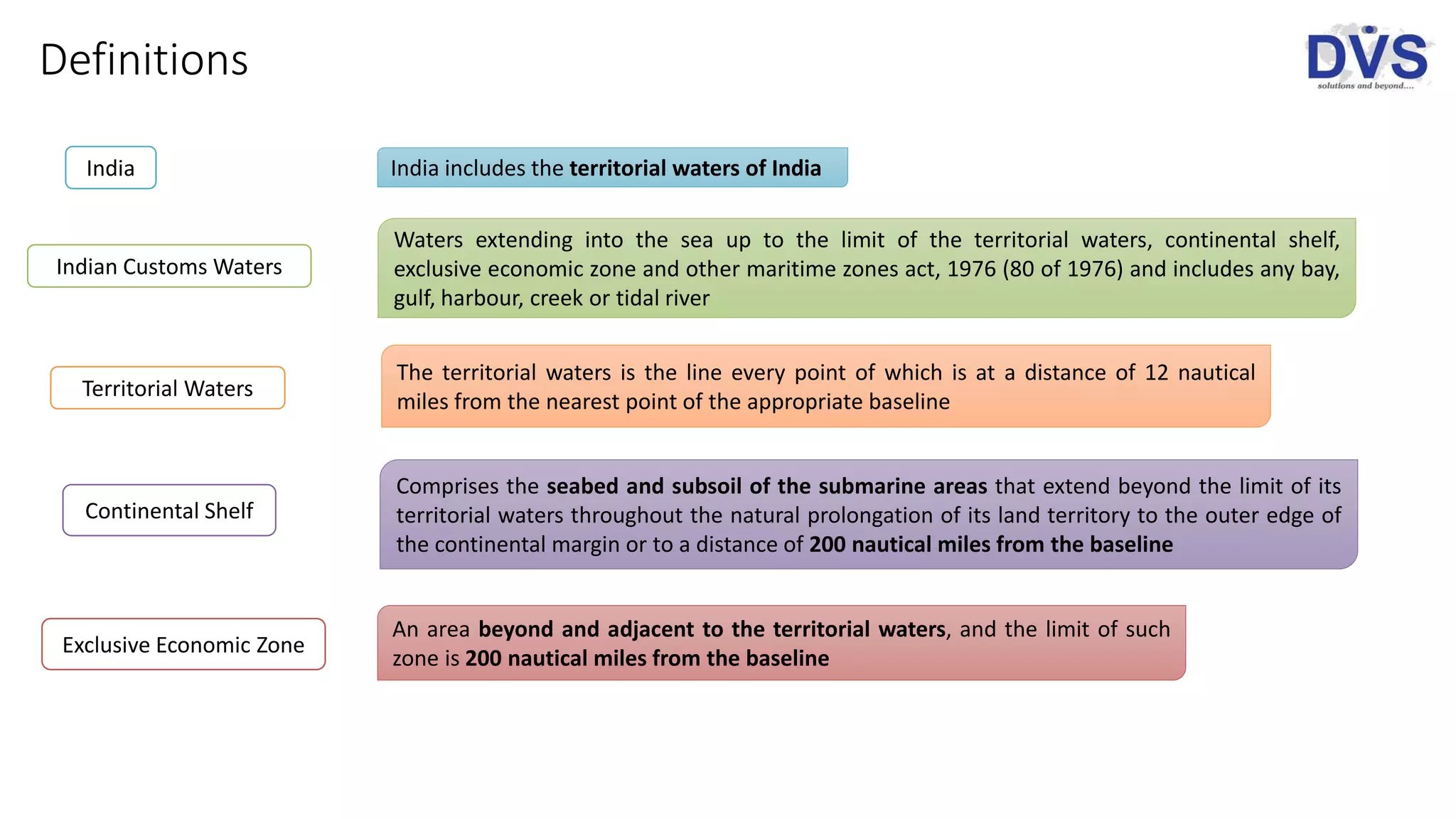

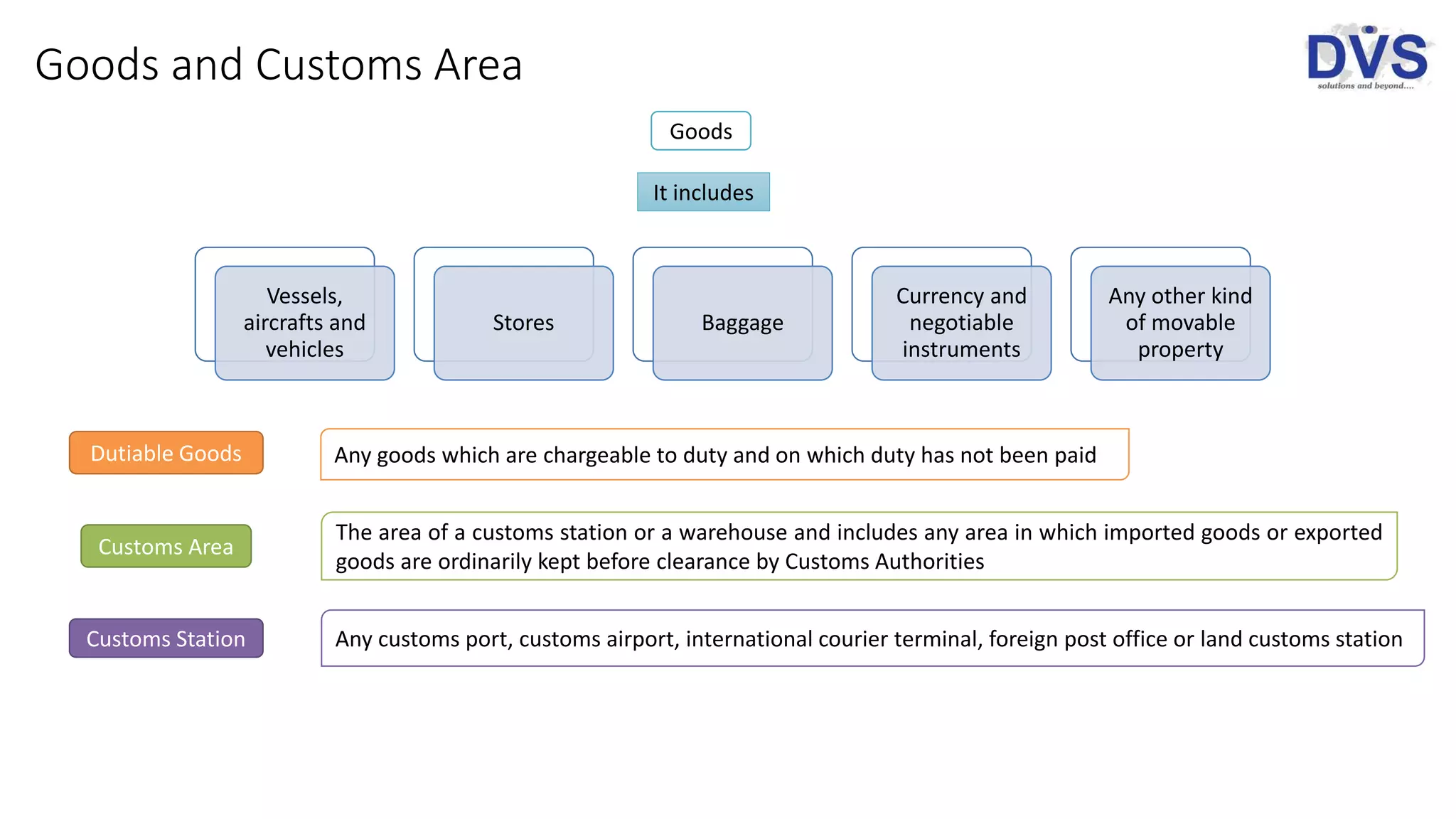

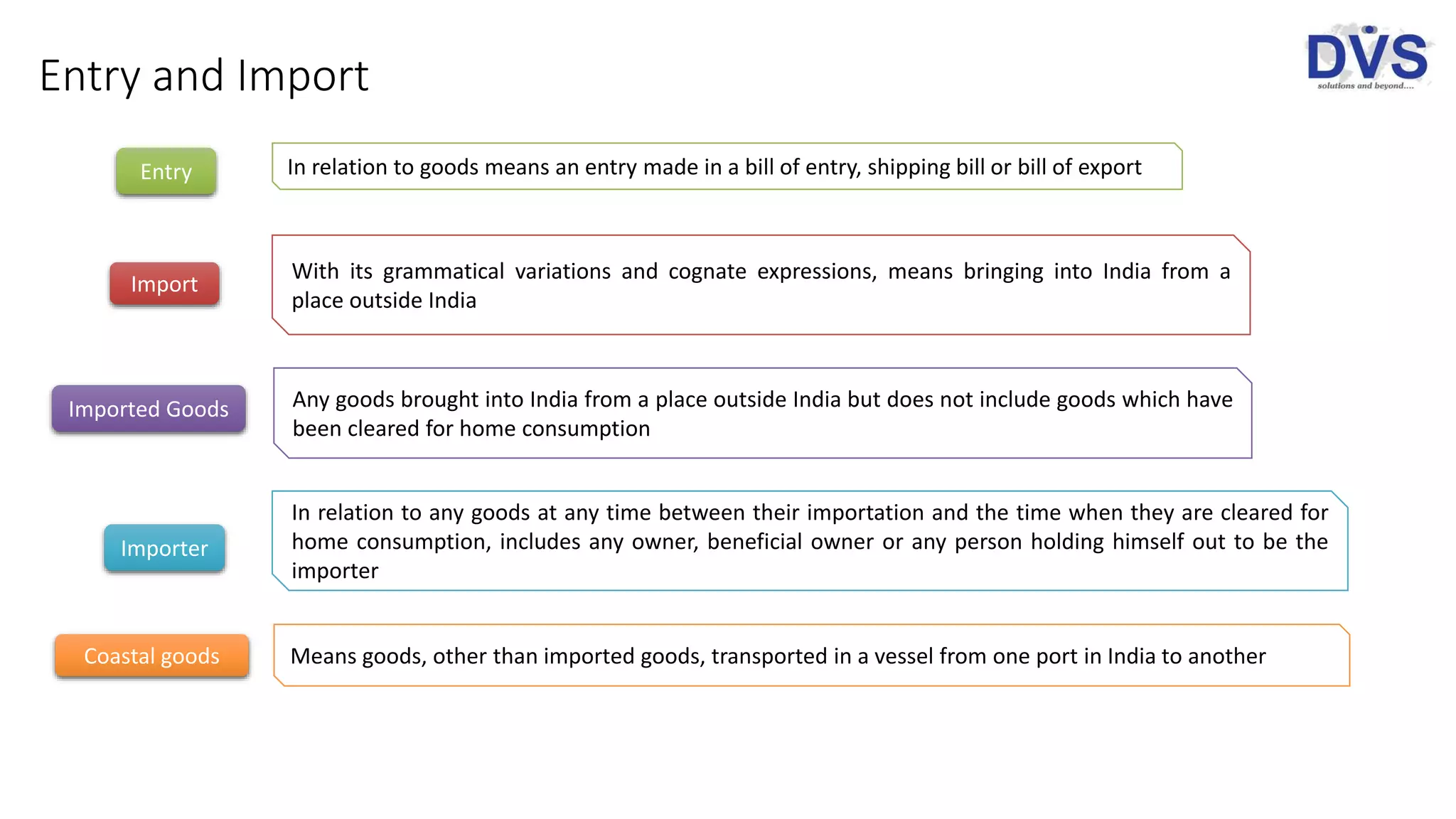

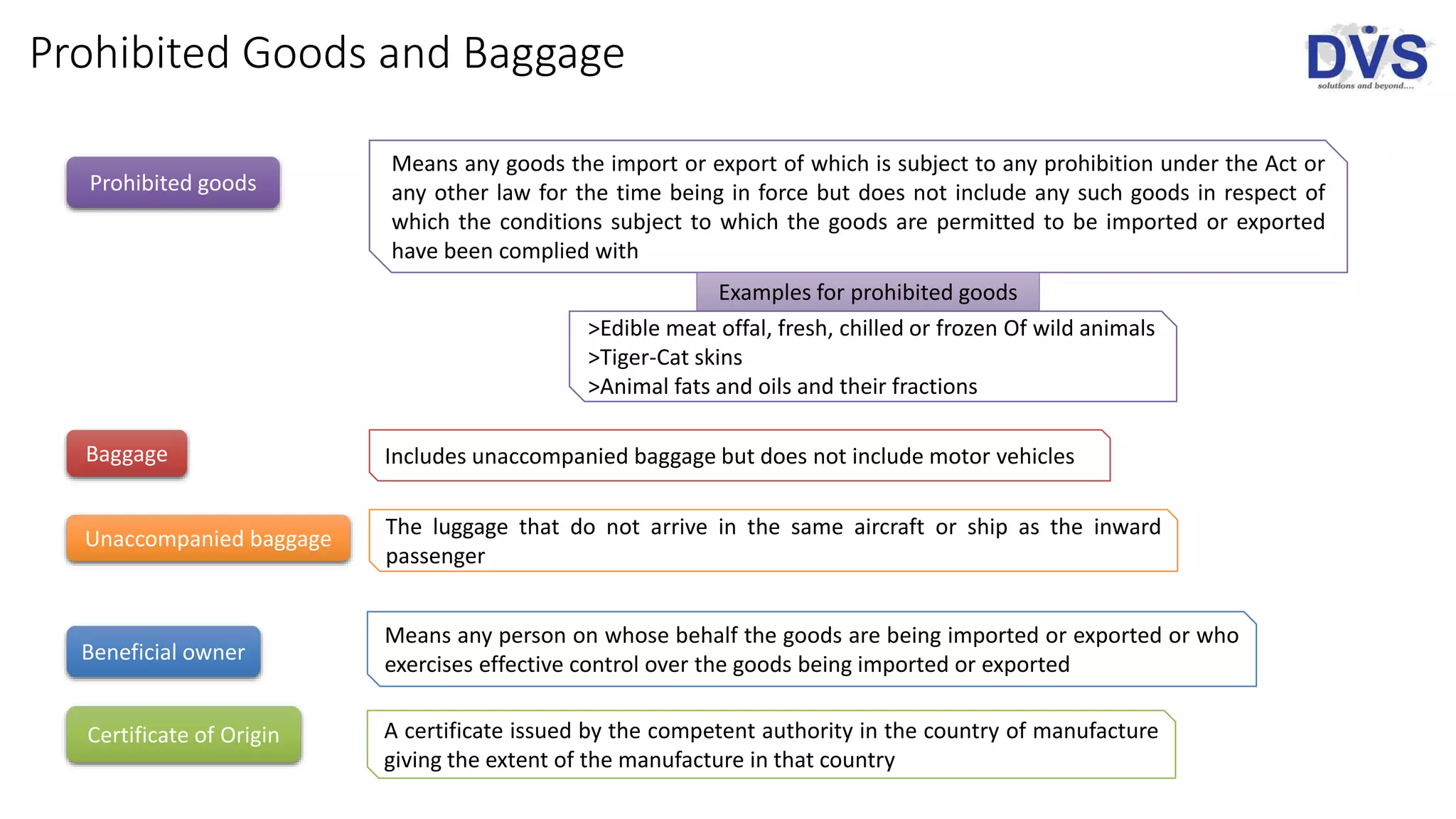

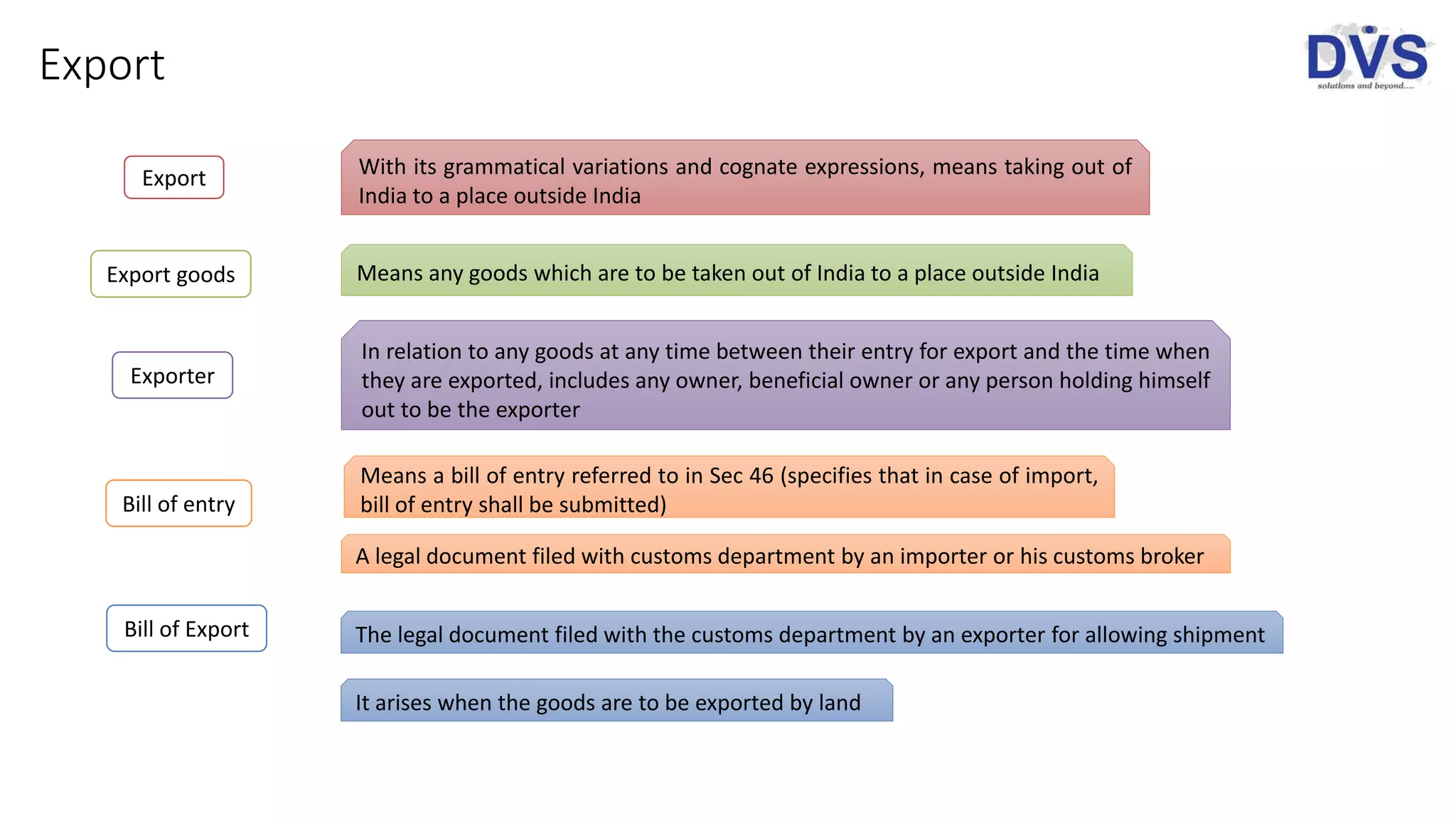

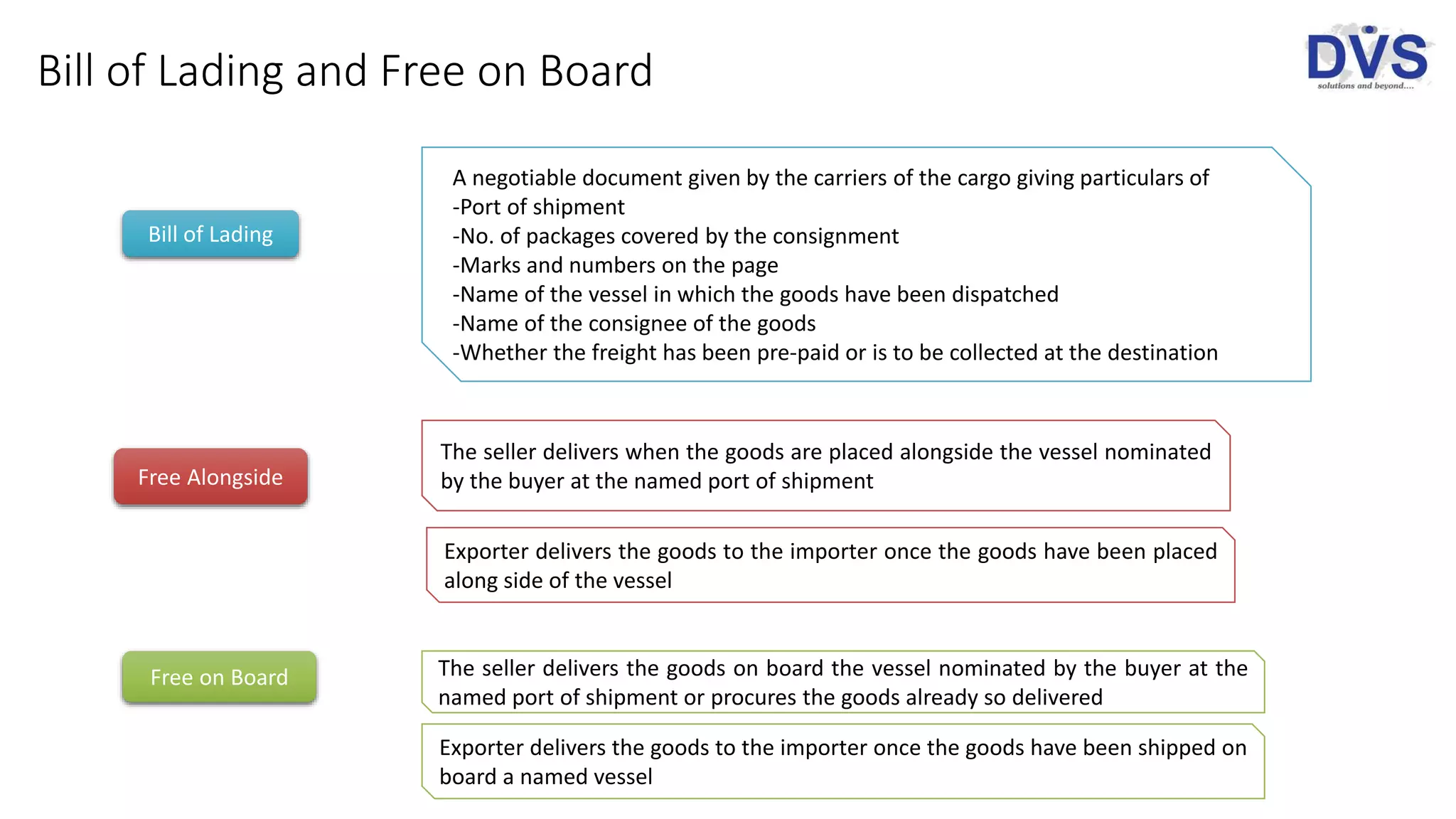

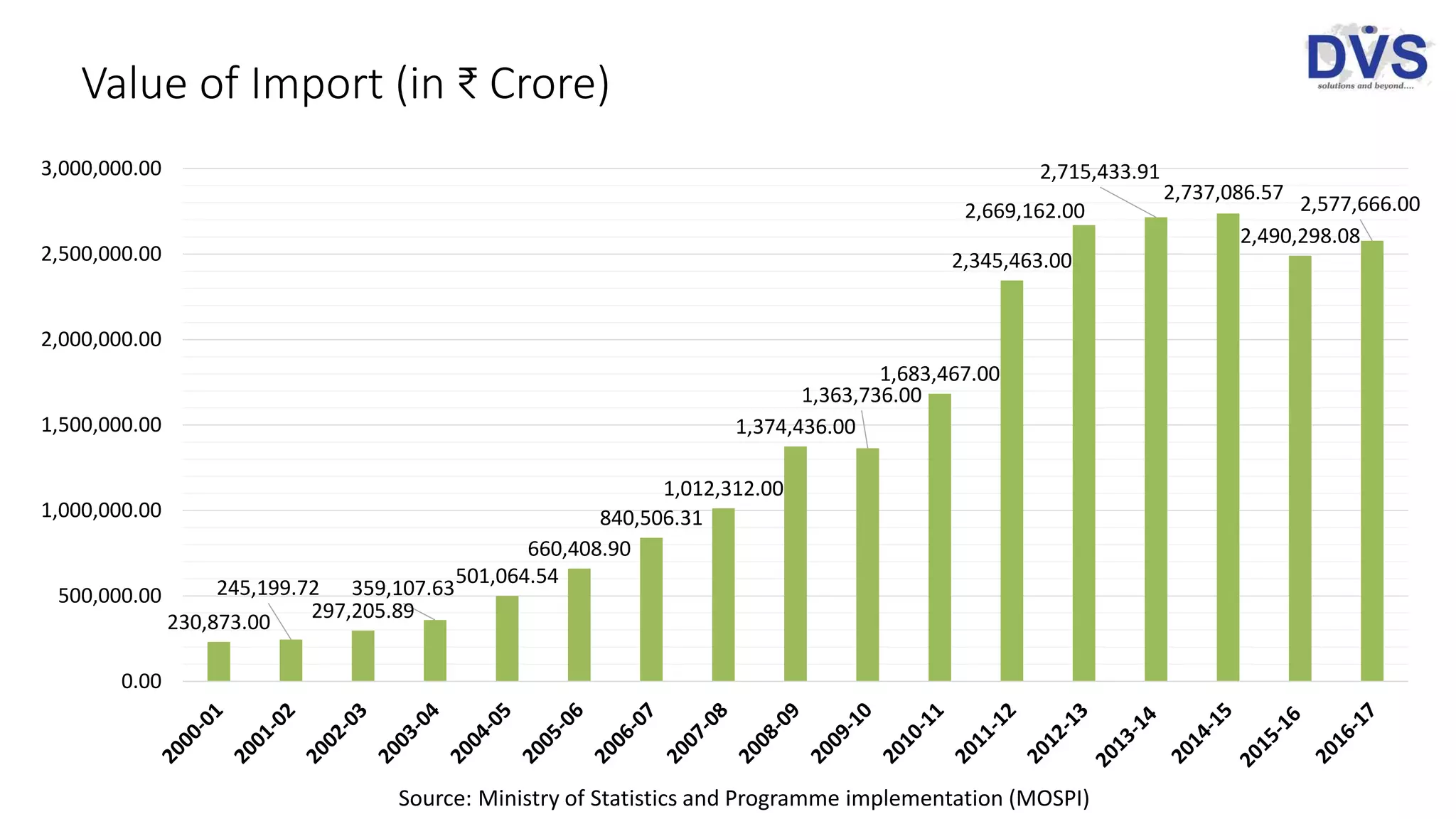

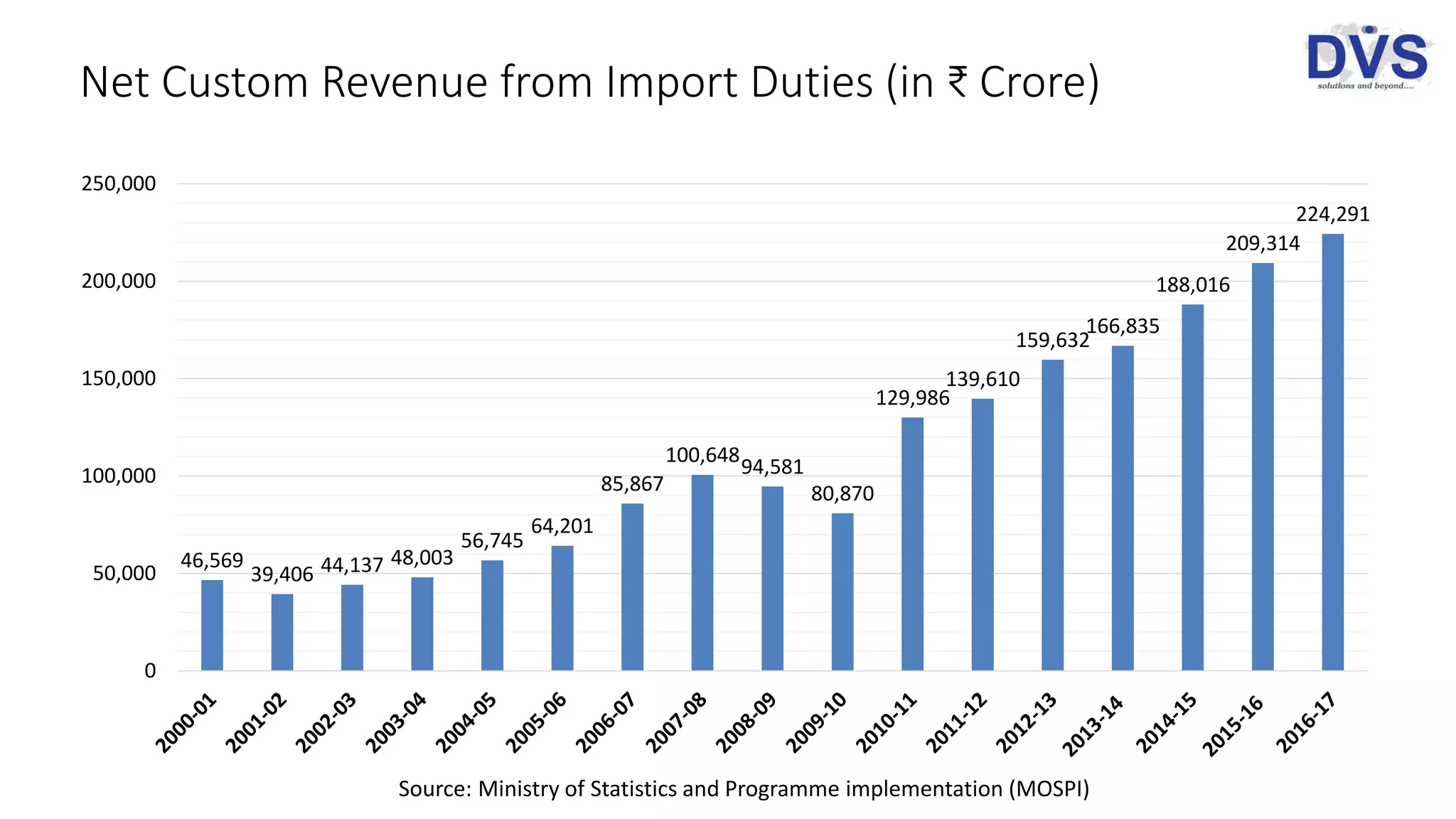

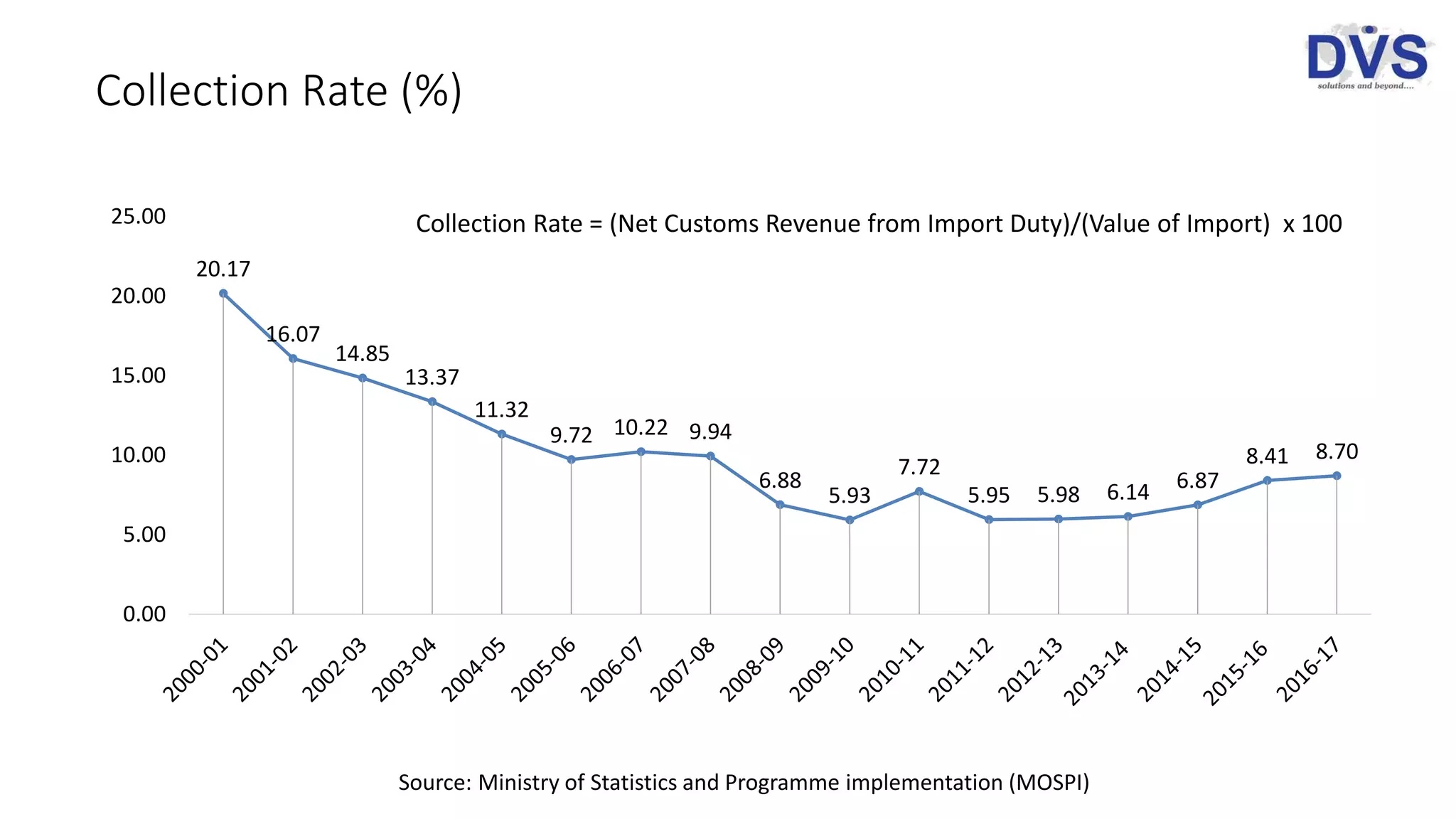

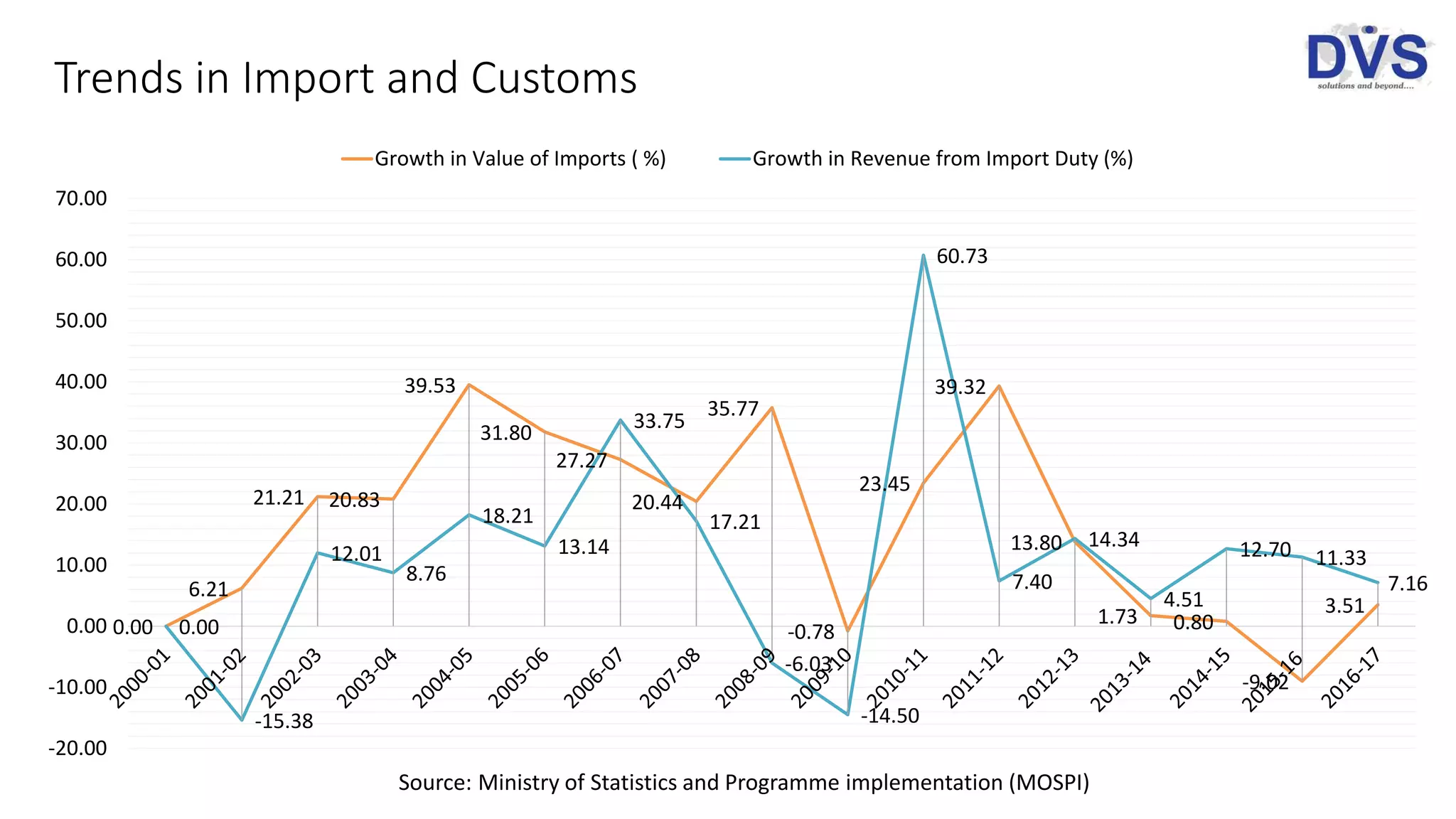

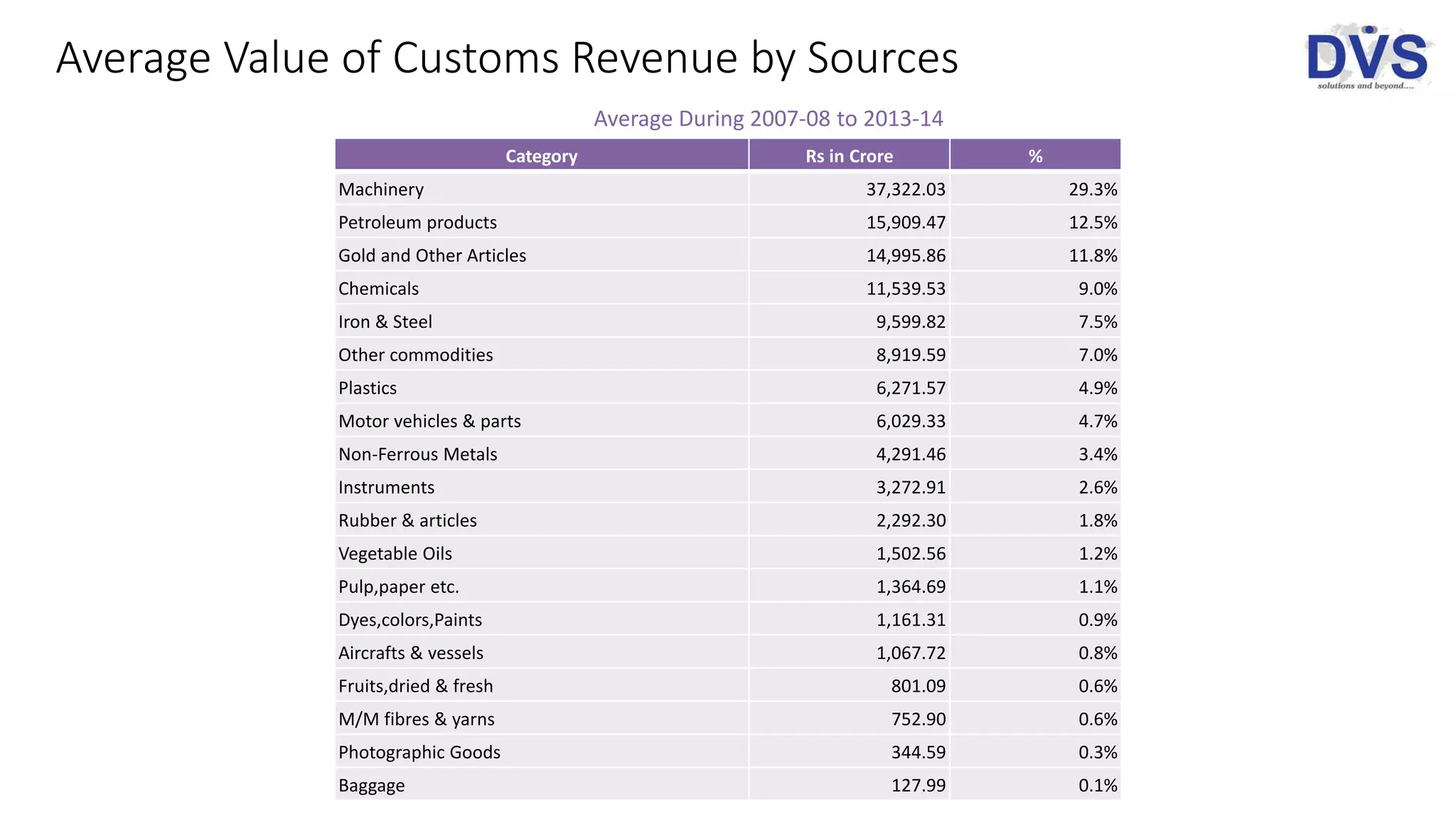

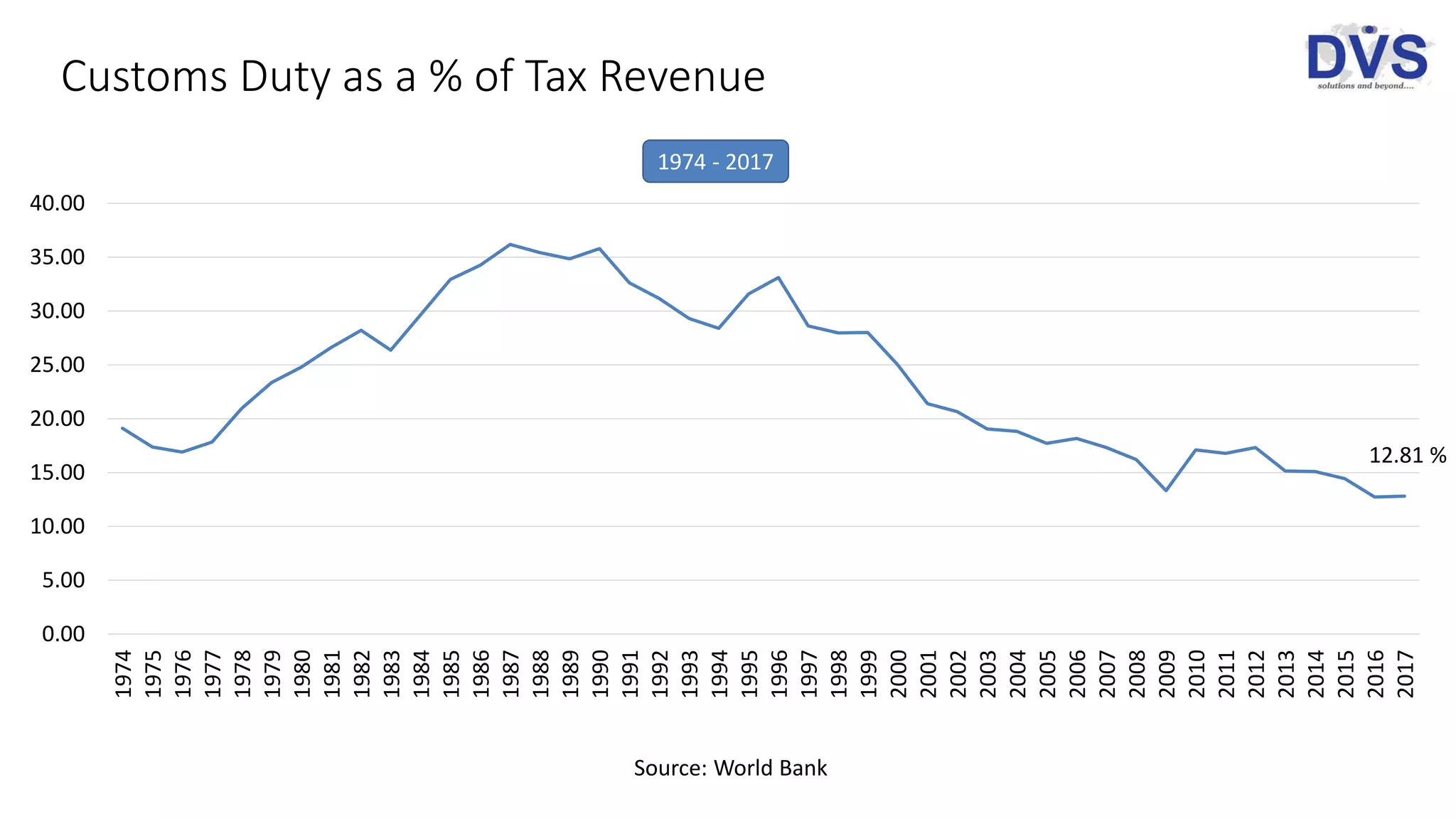

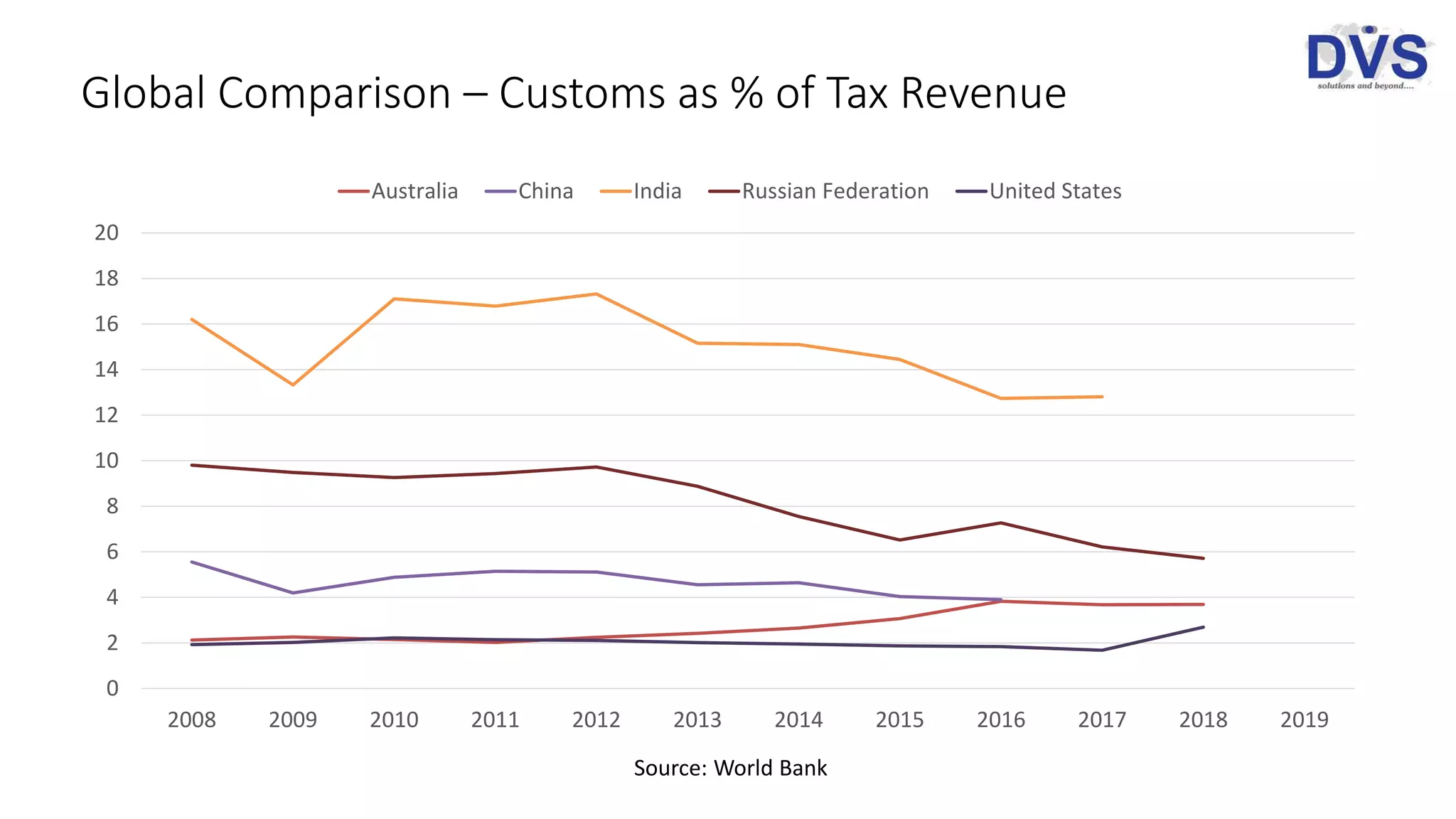

The document provides a comprehensive overview of customs law in India, highlighting significant definitions, the structure of the Customs Act of 1962, and the responsibilities of the Central Board of Indirect Taxes and Customs (CBIC). It outlines the purpose of customs duties, the categorization of goods, and statutory provisions concerning imports and exports. The content also includes statistical data on customs revenue, trends in imports, and an analysis of the customs duty's impact on tax revenue over the years.

![AUTOMATIC VACATION OF STAY GRANTED BY TRIBUNALDCIT v. PEPSI FOODS LTD. [2021]...](https://cdn.slidesharecdn.com/ss_thumbnails/depcitvpepsifoodsco-210717130643-thumbnail.jpg?width=640&height=640&fit=bounds)