Downloaded 15 times

![There are tow Parts :

1. Interest payable by the Assessee,

2. Interest payable to the Assessee.

Interest Payable by the Assessee by the assessee in the following cases :

Intt. Payable by the Assessee

A. Interest for dafaults in furnishing of the return of income u/s 234 A,

B. Interest for defaults in payment of Advance tax u/s 234 B ,

C. Interest for deferment of payment of Advance Tax u/s 234 C,

D. Interest for granting of Excess refund. …u/s 234 D.

Interest When the assessee is deemed to be in default….. u/s 220(2).

Interest for failure to deduct and Pay TDS….. u/s 201.

Some case laws :

140 A paid before Due date ; Return Submitted after due date :

--- Intt. u/s 234 A is not payable .

( Dr. Pranoy Roy V CIT [2002] 121 Taxman 314 ( Del) ]

Intt. Must be charged in the asstt. Order.

“Charge Intt. As per law ” will not suffice.

[CIT V. Inchcape India (P) Ltd [2002] 124 Taxman 744( Del) ]

Books of a/c with IT authority.

[ Intt u/s 234 A is not chargeable for delayed return ]

Issue of notice u/s 142 (1) does not give the AO jurisdiction to levy intt. u/s 234 A.

[ CIT V Ranchi Club Ltd.[(2001) 114 Taxman 414 ( SC) ]

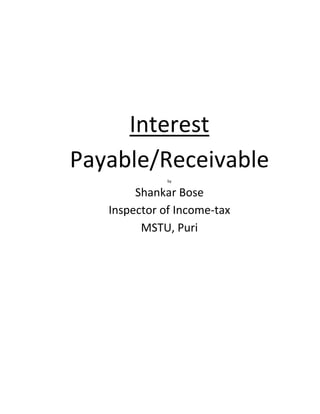

When Intt is payable Amt. On which intt. Is payable Rate of Int Period for

which intt. Is

payable

‘A’ failed to pay

Adv. Tax

Assessed Tax @ 1% for every month or part

of a month

From 1

st

April

of AY to dt of

143(1) or dt

of Regular

asstt.

Adv tax < 90 % of

Assessed Tax

Assessed Tax minus Adv Tax @ 1% for every month or part

of a month

From 1

st

April

of AY to dt of

143(1) or dt

of Regular

asstt.](https://image.slidesharecdn.com/interestpayablereceivable-bose-130514031044-phpapp01/85/Interest-payable-receivable-bose-2-320.jpg)

![ Cash seized during search should be treated as Advance Tax for the Purpose of computation of

Intt u/s 220(2) & sections 234 A,B,C.

[ Vipul D. Doshi V CIT (2001) 118 Taxman 30 ( Mum) ]

Interest Payable to the Assessee :

1. On delayed refund ……… u/s 244A.

Interest Payable to the Assessee :

2. 132B(4) ::

( Interest in respect of seized or requisitioned assets)

234 A

Default in Furnishing of Return of Income before due date :

Rate of Interest : @ 1 % p.m. or part of a month.

Period : From Due date to date of Furnishing of the Return.

When actually no Return has been furnished :

From Due date to Completion of assessment u/s 144

Interest to be calculated on :

Amount of tax determined u/s 143 (1)

Or

when Regular Asstt. Has been made

Tax assessed

[ Minus ]

(1) Advance Tax ,

(2) TDS/TCS ,

(3) Relief/Deduction of tax allowed u/s 90,90A,91 or any Tax Credit allowed to be Set Off u./s 115 JAA ,

115JD

234 B

Intt for default for payment of Advance tax

Assessed Tax : =

Tax on T.I. [u/s 143 (1)] / Regular assessment

MINUS

(1) TDS/TCS ,

(2) From AY 2007-08 any Relief/Deduction of tax allowed u/s 90,90A,91 or any Tax Credit allowed to be

Set Off u./s 115 JAA , 115JD

234 C

Intt for Deferment of Advance tax::::

If ‘A’ Under estimated installments of advance Tax:

----Intt to be calculated as below :

In case of non-corporate assessee](https://image.slidesharecdn.com/interestpayablereceivable-bose-130514031044-phpapp01/85/Interest-payable-receivable-bose-3-320.jpg)

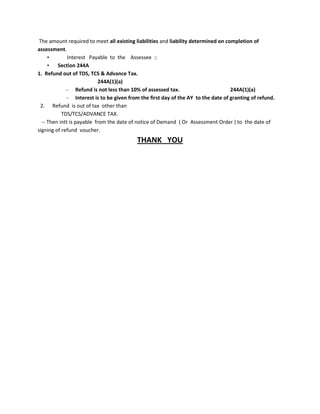

![ a. : Tax returned by “a”.

b. : TDS / TCS , etc.

c. : Adv. Tax Before June 15.

d. : Adv. Tax Before September 15

e. : Adv. Tax Before December 15

f. : Adv. Tax Before March 15

Interest on Excess Refund

234D : Interest on Excess Refund

Section 234 D( applicable from June 01, 2003).

Interest u/s 234 D is attracted in any of the Two cases :

1] Where Refund is granted u/s 143 (1) but no refund is due on regular assessment.

2] Where Refund is granted u/s 143 (1) But the refund so granted exceeds the amount

refundable on regular assessment

Computation of Interest u/s 234D:

Rate of Interest :: 0.5 % p.m. or part of a Month.

Period for which intt. Payable :: From the date of grant of refund to the date of Regular

assessment

Amount on which Intt. Is payable::

[Case1] : on Whole of amount.

[Case 2] : On the Excess amount refunded u/s 143(1) over the amount refundable on regular

assessment.

201(1A), 220(2)

TDS Default

Default to 156 notice

Interest Payable to the

Assessee ::

132B(4)-Interest Payable to the Assessee ::

1. 132B (4) :

Who shall pay : Central Government.

Rate of Interest : 0.5 % per month or part of a month.

132 B ( 4) :Interest Payable to the Assessee ::contd.

Period Involved : Calculated from the date immediately following the expiry of the period of

120 days from the date on which the last Authorization for Search u/s 132 or Requisition u/s

132A was Executed … To… the date of completion of assessment u/s 153 A or Chapter XIV-B(

Special Procedure for assessment of search cases.

132 B (4)Interest Payable to

the Assessee ::contd.

Amount on which interest to be paid :

Excess amount i.e. Amount seized or requisitioned

[ MINUS ]

Amount already Released [ MINUS ]](https://image.slidesharecdn.com/interestpayablereceivable-bose-130514031044-phpapp01/85/Interest-payable-receivable-bose-5-320.jpg)

This document discusses interest payable by and to taxpayers in various situations under the Indian Income Tax Act. It covers interest charged for late filing of returns, late payment or underpayment of advance tax, excess refunds granted, and interest paid on amounts seized during a search that are eventually refunded. The key points covered include calculation methods for different types of interest, applicable rates, and time periods over which interest applies. Case laws are also referenced related to issues like what date should be used to determine interest and whether interest can be charged without being specified in the assessment order.