Downloaded 577 times

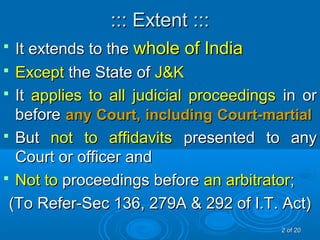

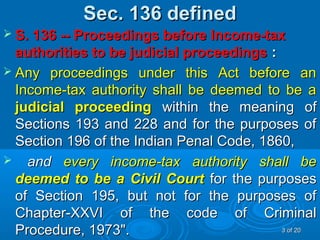

The document provides an overview of the Indian Evidence Act of 1872. Some key points: - It extends to all of India except Jammu and Kashmir. It applies to all judicial proceedings in any court, including court-martial, but not to affidavits or arbitrator proceedings. - Proceedings before the Income Tax Authority are deemed judicial proceedings. Every income tax authority is deemed a civil court for some purposes. - It defines terms like court, fact, evidence, and document. A court includes all judges and magistrates legally authorized to take evidence. Evidence includes oral statements and documents. - Oral evidence must be from an eyewitness or earwitness. Documentary evidence can be primary like