Downloaded 101 times

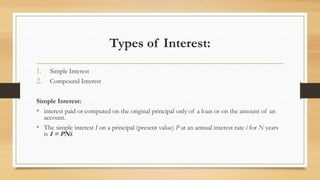

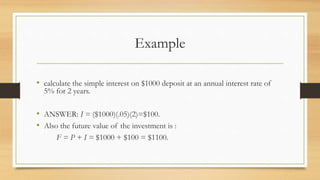

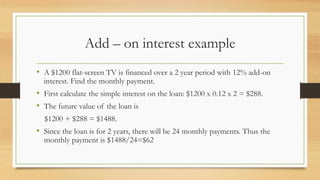

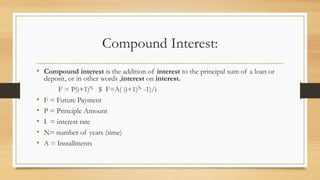

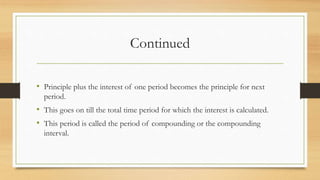

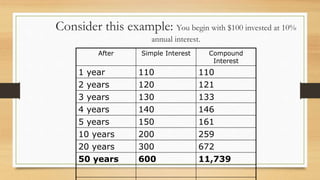

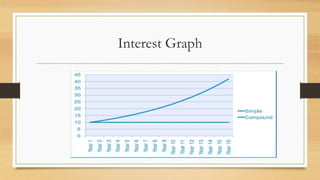

The document discusses different types of interest. It defines interest as a payment made by a borrower to a lender for the use of borrowed money. There are two main types of interest - simple interest, which is calculated only on the original principal amount, and compound interest, which calculates interest on both the principal and previously accumulated interest. The document provides examples to illustrate how to calculate simple interest and compound interest over time. It explains that compound interest results in higher total interest paid compared to simple interest due to interest being added to the principal each compounding period.