When people needto secure funds for some purpose, one of

the ways they usually resort to is borrowing. On the other

hand, the person or institution that lend the money would

also wish to get something in return for use of money.

Debtor or Maker. The person who borrows money for any

purpose.

Lender or Creditor. The person or institution that loans the

money.

A. Simple Interest

3.

Interest is thepayment for the use of borrowed money.

Principal is the sum of money invested.

Interest rate. The fractional part of the principal that is

paid on the loan and is usually expressed as percent.

Time or term. The length of time for which the money

is borrowed.

Maturity Value or Final Amount. The sum of the

principal and the interest which is accumulated at a

certain time.

4.

Kinds Of SimpleInterest

1. Ordinary – a simple interest that uses 360 days in a

year

2. Exact – a simple interest that uses the exact number of

days in a year which is 365 (or 366 for leap year)

*These two kinds of simple interest are only applicable if

the unit of time used is in days.

5.

Example:

On May 30,2022, the businessman loans 15,000 in the bank for

the expansion of his restaurant. It was agreed that he would pay the

amount with a 6% interest rate on August 10, 2022. Find the

simple interest.

Given:

Principal =15,000.

Rate = 6% or 0.06

Counting the number of days from May 30 to August 10;

May 31=1

June 1-30 =30

July 1-31=31

August 1-10 =10

Total: 72 days

Note: Since May 30 is the beginning date, it is not included in the counting.

6.

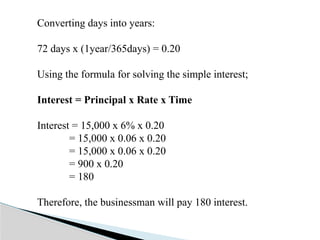

Converting days intoyears:

72 days x (1year/365days) = 0.20

Using the formula for solving the simple interest;

Interest = Principal x Rate x Time

Interest = 15,000 x 6% x 0.20

= 15,000 x 0.06 x 0.20

= 15,000 x 0.06 x 0.20

= 900 x 0.20

= 180

Therefore, the businessman will pay 180 interest.

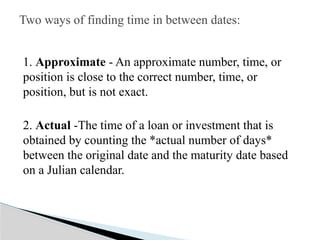

7.

1. Approximate -An approximate number, time, or

position is close to the correct number, time, or

position, but is not exact.

2. Actual -The time of a loan or investment that is

obtained by counting the *actual number of days*

between the original date and the maturity date based

on a Julian calendar.

Two ways of finding time in between dates:

8.

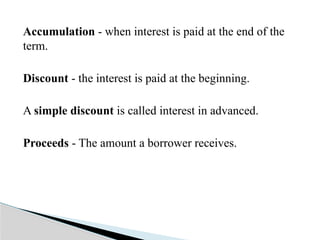

Accumulation - wheninterest is paid at the end of the

term.

Discount - the interest is paid at the beginning.

A simple discount is called interest in advanced.

Proceeds - The amount a borrower receives.

9.

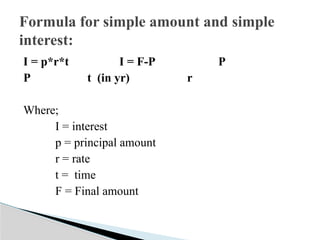

I = p*r*tI = F-P P

P t (in yr) r

Where;

I = interest

p = principal amount

r = rate

t = time

F = Final amount

Formula for simple amount and simple

interest:

10.

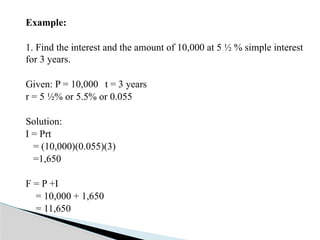

Example:

1. Find theinterest and the amount of 10,000 at 5 ½ % simple interest

for 3 years.

Given: P = 10,000 t = 3 years

r = 5 ½% or 5.5% or 0.055

Solution:

I = Prt

= (10,000)(0.055)(3)

=1,650

F = P +I

= 10,000 + 1,650

= 11,650

11.

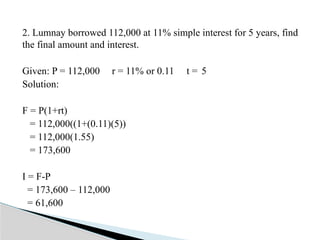

2. Lumnay borrowed112,000 at 11% simple interest for 5 years, find

the final amount and interest.

Given: P = 112,000 r = 11% or 0.11 t = 5

Solution:

F = P(1+rt)

= 112,000((1+(0.11)(5))

= 112,000(1.55)

= 173,600

I = F-P

= 173,600 – 112,000

= 61,600

12.

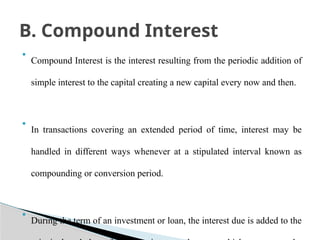

• Compound Interestis the interest resulting from the periodic addition of

simple interest to the capital creating a new capital every now and then.

• In transactions covering an extended period of time, interest may be

handled in different ways whenever at a stipulated interval known as

compounding or conversion period.

• During the term of an investment or loan, the interest due is added to the

B. Compound Interest

13.

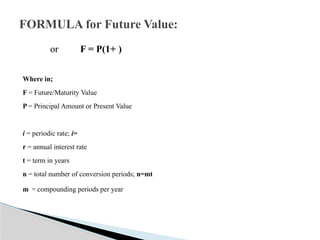

or F =P(1+ )

Where in;

F = Future/Maturity Value

P = Principal Amount or Present Value

i = periodic rate; i=

r = annual interest rate

t = term in years

n = total number of conversion periods; n=mt

m = compounding periods per year

FORMULA for Future Value:

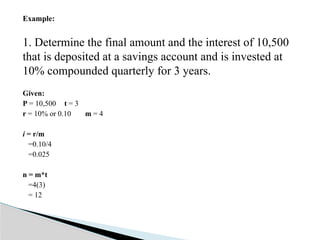

Example:

1. Determine thefinal amount and the interest of 10,500

that is deposited at a savings account and is invested at

10% compounded quarterly for 3 years.

Given:

P = 10,500 t = 3

r = 10% or 0.10 m = 4

i = r/m

=0.10/4

=0.025

n = m*t

=4(3)

= 12

16.

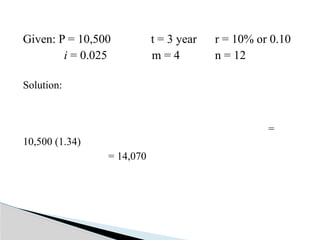

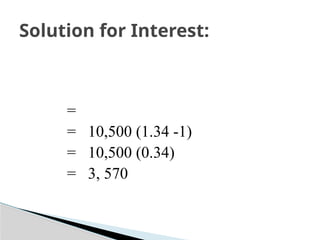

Given: P =10,500 t = 3 year r = 10% or 0.10

i = 0.025 m = 4 n = 12

Solution:

=

10,500 (1.34)

= 14,070

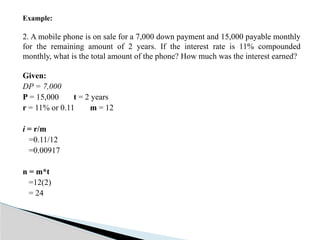

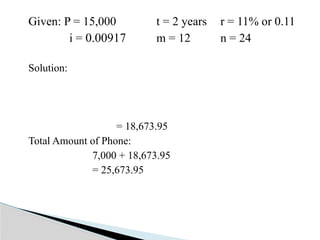

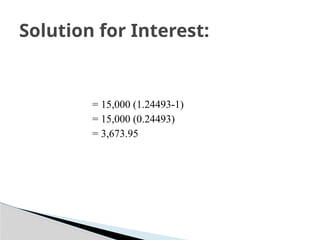

Example:

2. A mobilephone is on sale for a 7,000 down payment and 15,000 payable monthly

for the remaining amount of 2 years. If the interest rate is 11% compounded

monthly, what is the total amount of the phone? How much was the interest earned?

Given:

DP = 7,000

P = 15,000 t = 2 years

r = 11% or 0.11 m = 12

i = r/m

=0.11/12

=0.00917

n = m*t

=12(2)

= 24

19.

Given: P =15,000 t = 2 years r = 11% or 0.11

i = 0.00917 m = 12 n = 24

Solution:

= 18,673.95

Total Amount of Phone:

7,000 + 18,673.95

= 25,673.95

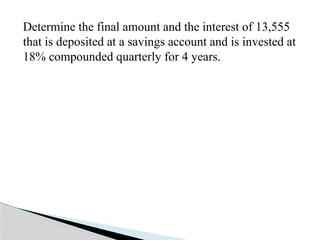

Determine the finalamount and the interest of 13,555

that is deposited at a savings account and is invested at

18% compounded quarterly for 4 years.

22.

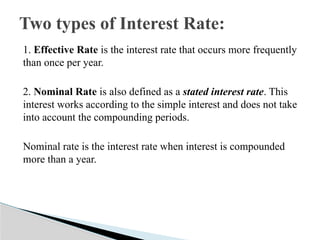

1. Effective Rateis the interest rate that occurs more frequently

than once per year.

2. Nominal Rate is also defined as a stated interest rate. This

interest works according to the simple interest and does not take

into account the compounding periods.

Nominal rate is the interest rate when interest is compounded

more than a year.

Two types of Interest Rate:

23.

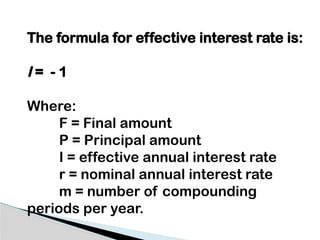

The formula foreffective interest rate is:

I = - 1

Where:

F = Final amount

P = Principal amount

I = effective annual interest rate

r = nominal annual interest rate

m = number of compounding

periods per year.

24.

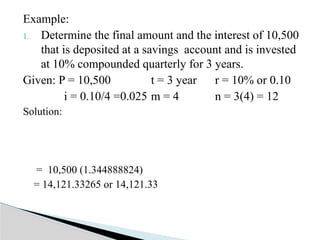

Example:

1. Determine thefinal amount and the interest of 10,500

that is deposited at a savings account and is invested

at 10% compounded quarterly for 3 years.

Given: P = 10,500 t = 3 year r = 10% or 0.10

i = 0.10/4 =0.025 m = 4 n = 3(4) = 12

Solution:

= 10,500 (1.344888824)

= 14,121.33265 or 14,121.33

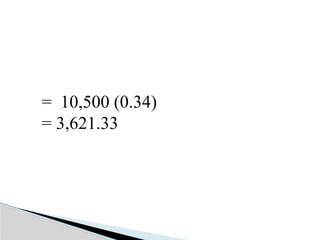

Example:

A credit cardcompany lend 25,500 with charges of 21%

compounded monthly in a year . Determined the interest

amount and final amount?

Given:

P = 25,500 t = 1 r = 21% or 0.21 m = 12 months

Solution

I = 25,500 [ (1 + (0.21 / 12)^12 – 1]

= 25,500 [(1 + 0.0175)^12 – 1]

= 25,500 (1.0175)^12 – 1

= 25,500 [1.231439315 – 1]

= 25,500 (0.231439315)

= 5,901.702533

Accumulation is theprocess of determining

the amount F of a given principal P due at a

specified time t. to accumulate a principal P

for t years means to solve for the final

amount by applying the formula.

Simple interest: F = P(1+rt)

Compound Interest:

Lesson 2: Accumulating and Discounting

29.

Discounting is theprocess of determining the present

value (P) of any amount due in the future. To discount

the amount F for t years, means to solve P by applying

the formula.

Simple interest:

Compound interest: or

30.

A discount isa deduction from the final amount(F) or

maturity value (MV) of a loan or obligation. A simple

discount is often called Bank discount or Interest in

Advance (Ia). The amount of money that the borrower

receives is called proceed.

Simple interest: Proceeds =

Compound interest: Proceeds or

31.

To elucidate theabove concept, let us consider the case

of Mr. Takoda, who wants to borrow 15,500 for six

months from a lender that charges 13 ¾ % simple

discount. The lender will deduct 12% at 15,500 or 1,860,

which is called amount of discount or interest in advance,

and Mr. Takoda will receive 13,640, which is called the

proceeds. Thus, the computation of bank discount is

based on the final amount or maturity value rather than

the present value.

32.

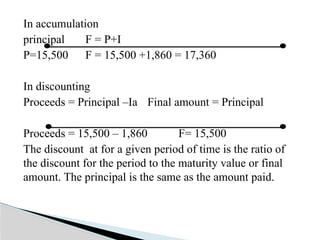

In accumulation

principal F= P+I

P=15,500 F = 15,500 +1,860 = 17,360

In discounting

Proceeds = Principal –Ia Final amount = Principal

Proceeds = 15,500 – 1,860 F= 15,500

The discount at for a given period of time is the ratio of

the discount for the period to the maturity value or final

amount. The principal is the same as the amount paid.

33.

Since principal isthe same as the final amount paid,

discount or interest in advance can be computed by

means of the formula:

Ia = Fdt

Where:

Ia = amount of discount or interest in advance

F = final amount

d = discount rate

t = time or term of discount

34.

Other formulas thatcan derived from the foregoing:

d = t = F =

Present Value or Proceed Formula:

Proceeds = F – Ia or Proceeds = F(1-dt)

Final amount formula: F =

35.

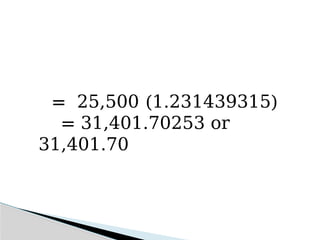

Example:

1. A fruitvendor at the market borrows 9,000 for 6

months at 10 ¼ % simple interest. What amount must

he repay?

Given: P = 9,000 r = 10 ¼ % or 0.1025

t = 6 months or ½ year

Solution:

F = P (1+rt)

= 9,000 [1+(0.1025x0.5)]

= 9,000 (1.05125)

= 9,461.25

36.

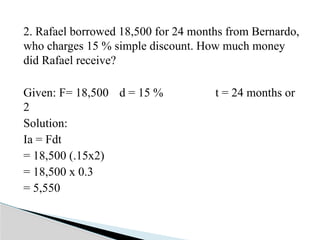

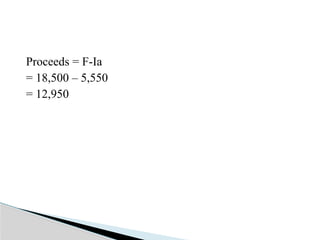

2. Rafael borrowed18,500 for 24 months from Bernardo,

who charges 15 % simple discount. How much money

did Rafael receive?

Given: F= 18,500 d = 15 % t = 24 months or

2

Solution:

Ia = Fdt

= 18,500 (.15x2)

= 18,500 x 0.3

= 5,550

![Example:

A credit card company lend 25,500 with charges of 21%

compounded monthly in a year . Determined the interest

amount and final amount?

Given:

P = 25,500 t = 1 r = 21% or 0.21 m = 12 months

Solution

I = 25,500 [ (1 + (0.21 / 12)^12 – 1]

= 25,500 [(1 + 0.0175)^12 – 1]

= 25,500 (1.0175)^12 – 1

= 25,500 [1.231439315 – 1]

= 25,500 (0.231439315)

= 5,901.702533](https://image.slidesharecdn.com/chapter-4-consumer-mathematics-250224033927-c1aa2677/85/Chapter-4-Consumer-Mathematics-pptxbbbbj-26-320.jpg)

![Example:

1. A fruit vendor at the market borrows 9,000 for 6

months at 10 ¼ % simple interest. What amount must

he repay?

Given: P = 9,000 r = 10 ¼ % or 0.1025

t = 6 months or ½ year

Solution:

F = P (1+rt)

= 9,000 [1+(0.1025x0.5)]

= 9,000 (1.05125)

= 9,461.25](https://image.slidesharecdn.com/chapter-4-consumer-mathematics-250224033927-c1aa2677/85/Chapter-4-Consumer-Mathematics-pptxbbbbj-35-320.jpg)