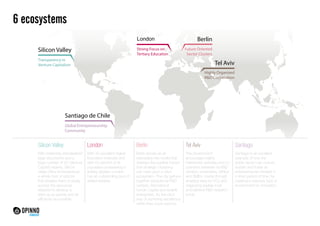

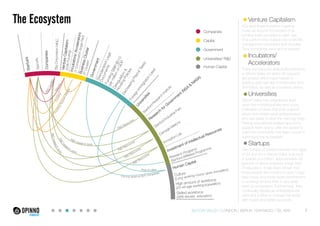

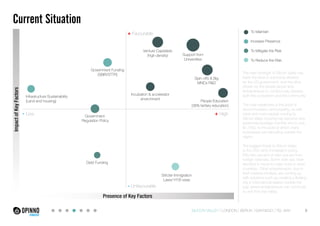

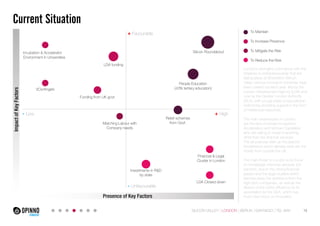

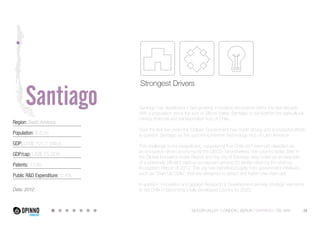

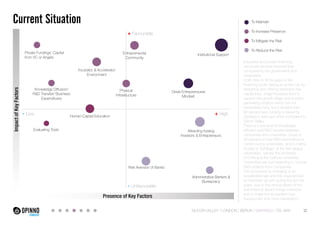

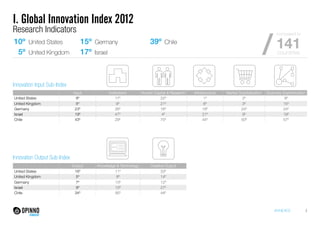

Silicon Valley has established itself as the leading global innovation ecosystem due to key factors such as transparency in venture capitalism funding, support from top universities, and a skilled workforce culture. However, strict immigration laws and high housing costs present challenges. While venture capital and university partnerships remain strengths, addressing foreign talent restrictions and infrastructure sustainability will help Silicon Valley maintain its edge in the face of global competition.