Downloaded 304 times

![What attracts you towards a service provider? [Network Coverage of my service

provider was a decisive factor that influenced my purchase]

CUIM

Page 39](https://image.slidesharecdn.com/indiantelecomserviceproviders-111027002842-phpapp01/85/Indian-telecom-service-providers-39-320.jpg)

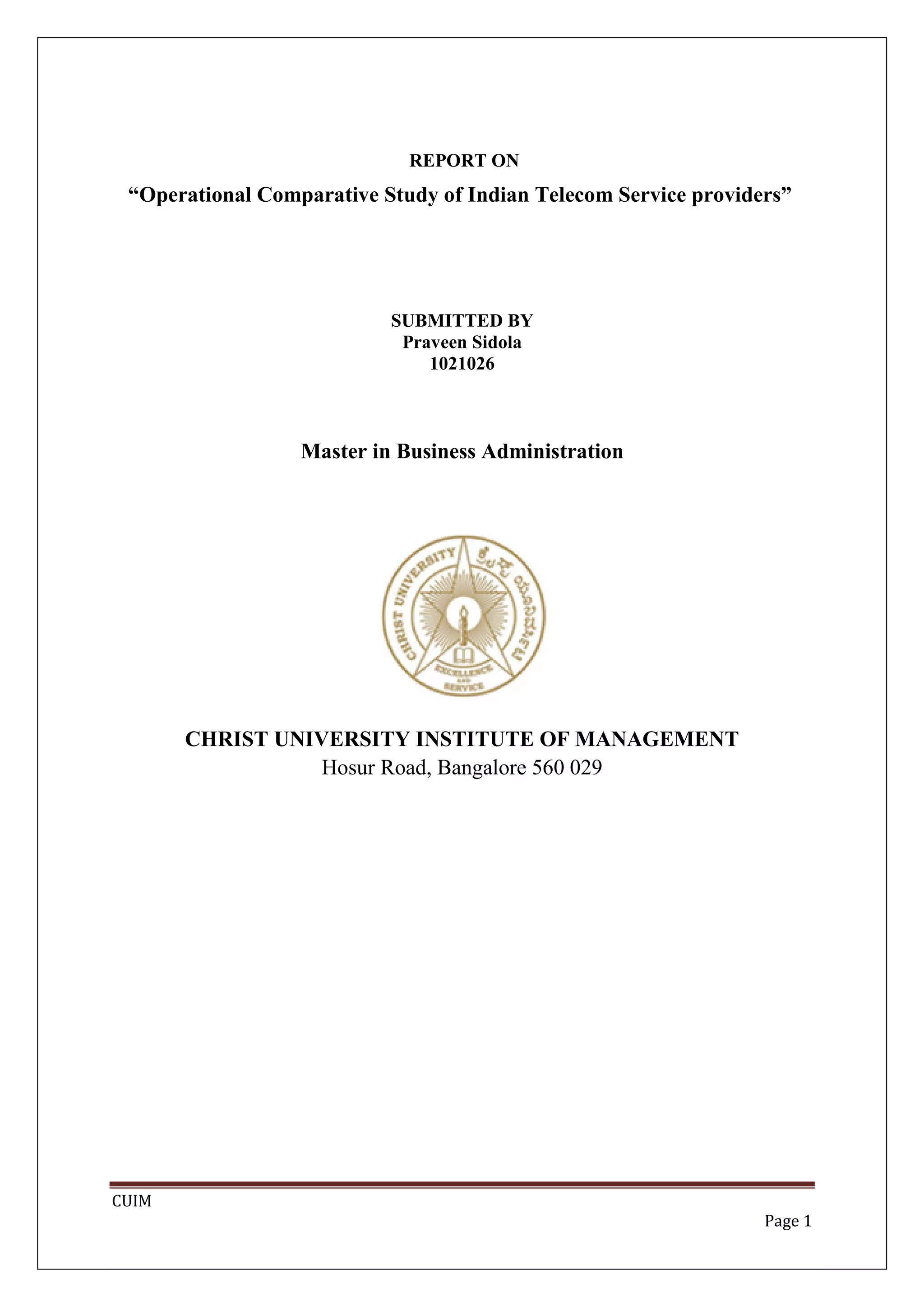

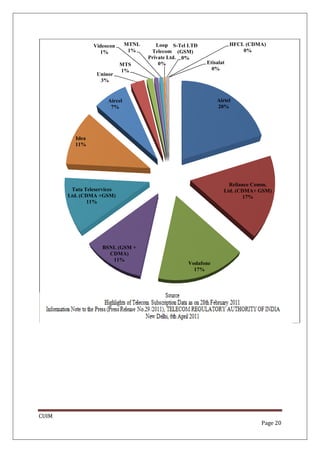

![How would you rate your mobile service provider in terms of [Network

coverage]

ANOVA

How would you rate your mobile service provider in terms of [Network coverage]

Sum of Squares df Mean Square F Sig.

Between Groups 21.299 5 4.260 4.320 .001

Within Groups 100.580 102 .986

Total 121.880 107

CUIM

Page 41](https://image.slidesharecdn.com/indiantelecomserviceproviders-111027002842-phpapp01/85/Indian-telecom-service-providers-41-320.jpg)

![Post hoc tests are not performed for What attracts you towards a service provider?

[Advertisements played a major role in my decision to choose my service provider]

because at least one group has fewer than two cases.

CUIM

Page 51](https://image.slidesharecdn.com/indiantelecomserviceproviders-111027002842-phpapp01/85/Indian-telecom-service-providers-51-320.jpg)

![Post hoc tests are not performed for What attracts you towards a service provider?

[Network Coverage of my service provider was a decisive factor that influenced my

purchase] because at least one group has fewer than two cases.

CUIM

Page 52](https://image.slidesharecdn.com/indiantelecomserviceproviders-111027002842-phpapp01/85/Indian-telecom-service-providers-52-320.jpg)

![Post hoc tests are not performed for How would you rate your mobile service provider in

terms of [Network coverage] because at least one group has fewer than two cases.

CUIM

Page 53](https://image.slidesharecdn.com/indiantelecomserviceproviders-111027002842-phpapp01/85/Indian-telecom-service-providers-53-320.jpg)

![Post hoc tests are not performed for What attracts you towards a service provider? [Value

added services are a major factor that attracts me to a service provider] because at least

one group has fewer than two cases.

CUIM

Page 54](https://image.slidesharecdn.com/indiantelecomserviceproviders-111027002842-phpapp01/85/Indian-telecom-service-providers-54-320.jpg)

This document provides a 3-page report on operational comparisons of Indian telecom service providers. It includes an index listing the various sections, an executive summary highlighting key facts about India's telecom sector growth and subscriber numbers, and an introduction covering the global telecom industry trends, Asia's leadership in growth, and an overview of India's telecom market characteristics including services, operators, and circles.