Income Statement:

Management Accounting

Thispresentation explores the income statement. We'll examine it from

a management accounting view. Join us as we decode financial

performance. Learn strategic decision-making insights.

by Dr.Rajamani G

Assistant Professor of BCOM-A&F

SRCAS

2.

Core Components: Revenue,Cost of Goods Sold,

and Gross Profit Explained

Revenue

Revenue is the income earned from

business activities. This includes

selling goods or services.

Cost of Goods Sold (COGS)

COGS are the costs directly tied to

producing goods. This includes

materials and labor.

Gross Profit

Gross profit is revenue less the cost of

goods sold. It shows profit before

operating expenses.

3.

Diving Deeper: Operating

Expensesand Income

Operating Expenses

These are costs to run the

business day-to-day. This

includes salaries, rent, and

marketing.

Operating Income

Operating income is gross

profit minus operating

expenses. It reflects profit

from core operations.

EBIT

Earnings Before Interest and Taxes, a metric often used instead of

Operating Income.

4.

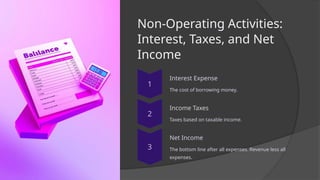

Non-Operating Activities:

Interest, Taxes,and Net

Income

Interest Expense

The cost of borrowing money.

Income Taxes

Taxes based on taxable income.

Net Income

The bottom line after all expenses. Revenue less all

expenses.

5.

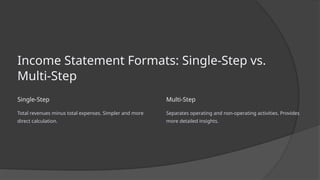

Income Statement Formats:Single-Step vs.

Multi-Step

Single-Step

Total revenues minus total expenses. Simpler and more

direct calculation.

Multi-Step

Separates operating and non-operating activities. Provides

more detailed insights.

6.

Importance of theIncome

Statement: Key

Performance Indicators

(KPIs) for Management

Profit Margins

How much profit is

generated per dollar

of revenue.

Revenue Growth

The rate at which

revenue is increasing

over time.

Expense Ratio

How much of revenue

is consumed by

expenses.

7.

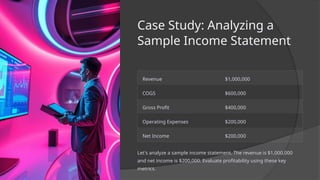

Case Study: Analyzinga

Sample Income Statement

Revenue $1,000,000

COGS $600,000

Gross Profit $400,000

Operating Expenses $200,000

Net Income $200,000

Let's analyze a sample income statement. The revenue is $1,000,000

and net income is $200,000. Evaluate profitability using these key

metrics.

8.

Conclusion: Using the

IncomeStatement for

Strategic Decision-Making

1 Performance

Evaluation

Assess company financial

health and profitability.

2 Trend Analysis

Identify patterns and

growth opportunities.

3 Resource Allocation

Make informed decisions about investments.