Downloaded 57 times

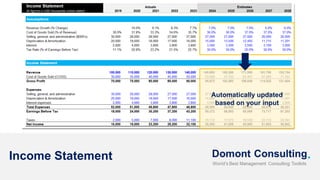

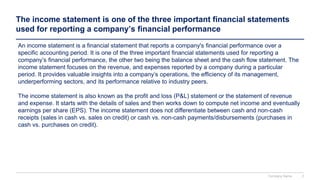

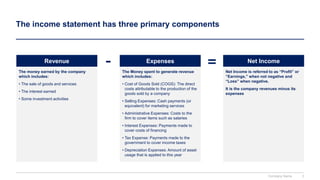

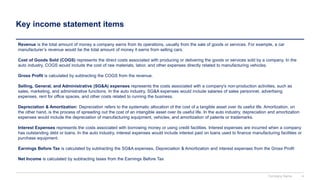

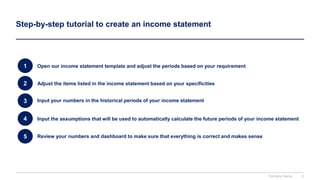

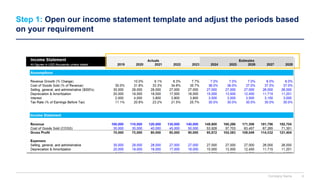

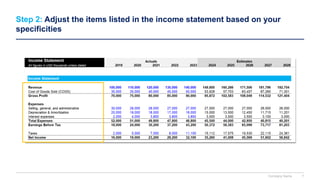

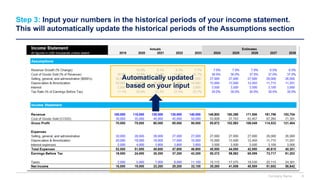

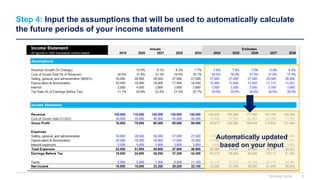

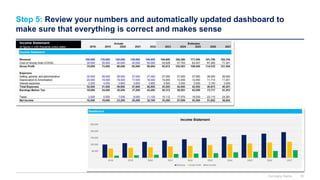

The income statement is a key financial document that reports a company's performance over a specific period, detailing revenue, expenses, and net income. It includes components like revenue earned from sales, cost of goods sold, and various expenses, along with insights into company operations and management efficiency. A step-by-step tutorial is provided for creating an income statement using a template, including adjusting periods, inputting numbers, and reviewing calculations.