Download to read offline

![12

TTVV A

A

A

T

A εσ

σ

µ +

−+=

2

lnln

2

(2.4)

where

ε is a standard normal random variable.

Eq. (2.4) involves estimation of the drift rate of the firm’s asset value which usually

involves significant error. KMV uses a constant drift rate for all firms in the same

market, which is the expected growth rate of the market as a whole. Based on the

same rational, the drift rate can be replaced by the risk free rate, which can be

estimated more accurately. We can then go on to calculate the upper bound of the

default probability assuming that the drift rate is always greater than the risk free rate.

The probability of default is the probability that the market value of the firm’s assets

will be less than the default point by the time the debt mature at time T. That is

[ ]

[ ]

−+

−=

≥

−+

−=

≤+

−+=

≤=

≤=

T

Tr

X

V

N

T

Tr

X

V

P

XTTrVP

XVP

XVPEDF

A

AA

A

AA

A

A

A

T

A

T

A

σ

σ

ε

σ

σ

εσ

σ

2

ln

2

ln

ln

2

ln

lnln

2

2

2

(2.5)](https://image.slidesharecdn.com/ifrs9ntu-mfe2000-ews-credit-deterioration-170707153133/85/Ifrs9-ntu-mfe2000-ews-credit-deterioration-15-320.jpg)

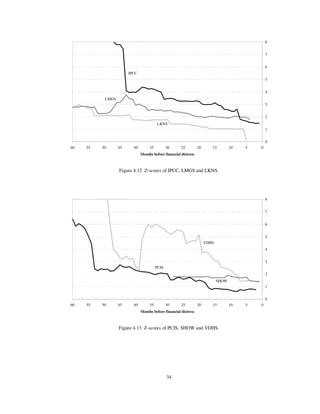

This dissertation examines the likelihood of default among local companies listed on the Singapore Exchange using the KMV default prediction framework, which models equity as a call option on a firm's assets. The study finds that expected default frequencies generated by this approach can predict financial distress approximately six months in advance, highlighting the importance of equity price and volatility in assessing credit risk. Comparisons with the Altman's Z-score model indicate both methodologies yielded consistent results in predicting financial distress.

![Lgd Model Jacobs 10 10 V2[1]](https://cdn.slidesharecdn.com/ss_thumbnails/lgdmodeljacobs1010v21-12872530142448-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)