Ias 37 provision

This document summarizes accounting guidance on provisions according to IAS 37. It defines a provision as a present obligation from a past event that will likely require a future outflow of resources and can be reliably estimated. Provisions should be recognized if the criteria are met. Measurement of provisions involves estimating the required expenditure to settle the obligation, using the most likely amount or probability-weighted expected value and discounted if material. Checks are recommended to validate the appropriateness and completeness of provisions for items like damaged stock, slow moving inventory, and doubtful debts. Disclosures for provisions should include accounting policies, movements during the period, and separate reporting not with other payables.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Ias 37 provision

Similar to Ias 37 provision (20)

Recently uploaded

Recently uploaded (20)

Ias 37 provision

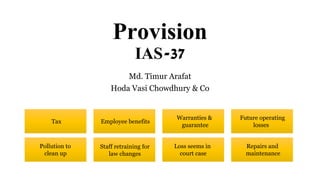

- 1. Provision IAS-37 Md. Timur Arafat Hoda Vasi Chowdhury & Co Tax Employee benefits Warranties & guarantee Future operating losses Pollution to clean up Staff retraining for law changes Loss seems in court case Repairs and maintenance

- 2. Definition Present obligation as a result of a past event, whereby- Settlement of the obligation - require future outflow of resources Uncertain amount or timing Reliable estimate is feasible

- 3. Recognizing a provision Start Present obligation as a result of an obligating event Provision Do nothing Disclose contingent liability Possible obligation ? Reliable estimate ? Probable outflow ? Remote? No No No (rare) No No Yes Yes Yes Yes Yes

- 4. Measurement of provisions Best estimate of expenditure to settle the present obligation at balance sheet date - Most likely amount - Probability-weighted expected value - Discounted PV using a pre-tax discount rate and the risks specific to the liability Adjust to reflect the current best estimate. No longer probable? Then reverse.

- 5. - Obtain details of the basis and ensure adequacy, correctness and consistency What required to check ? - Check appropriateness considering the nature of business - Review the stock sheets (damaged, slow moving or obsolete items correctly written?) - Review WIP (ensure that provision has been made against any ‘old’ jobs) Assessing the need for any further provision: (consider following) - Production levels are falling ? - Stock levels are high in comparison to orders received and anticipated demand ? - Any fluctuations in cost or selling price ? and - Likely change in technology or market demands ? - Ensure adequate provision for all bad and doubtful trade debts. - Subsequent position check – (was the estimation reasonable ?)

- 6. Ensure its completeness by reviewing: (a) the previous year’s provisions (b) items recorded on the bank certificate; (c) minutes of meetings; (d) major contracts (e) Correspondence and (f) Ageing What required to check ? - Sampling of stock and WIP items - compare costs to (selling price - expenditure for realization) - Losses on one line cannot be set off against profits on another, so check such instances, and - Provision is made on a finished product? YES ? ensure provision against WIP and materials in the process. excessive provisions deliberate overstatement

- 7. – Accounting policies for each major type of provision (for example, warranties) – Movements in provisions during the period – Confirm in the letter of representation – Report separately. (Not with trade and other payables) Disclosures