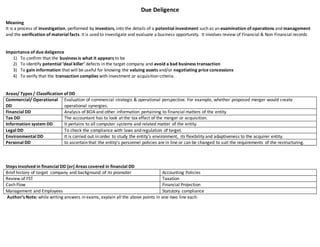

1. Due Deligence

Meaning

It is a process of investigation, performed by investors, into the details of a potential investment such as an examination of operations and management

and the verification of material facts. It is used to investigate and evaluate a business opportunity. It involves review of Financial & Non Financial records

Importance of due deligence

1) To confirm that the business is what it appears to be

2) To identify potential ‘deal killer’ defects in the target company and avoid a bad business transaction

3) To gain information that will be useful for knowing the valuing assets and/or negotiating price concessions

4) To verify that the transaction complies with investment or acquisition criteria.

Areas/ Types / Classification of DD

Commercial/ Operational

DD

Evaluation of commercial strategic & operational perspective. For example, whether proposed merger would create

operational synergies.

Financial DD Analysis of BOA and other information pertaining to financial matters of the entity

Tax DD The accountant has to look at the tax effect of the merger or acquisition.

Information system DD It pertains to all computer systems and related matter of the entity.

Legal DD To check the compliance with laws and regulation of target.

Environmental DD It is carried out in order to study the entity’s environment, its flexibility and adaptiveness to the acquirer entity.

Personal DD to ascertain that the entity’s personnel policies are in line or can be changed to suit the requirements of the restructuring.

Steps involved in financial DD (or) Areas covered in financial DD

Brief history of target company and background of its promoter Accounting Policies

Review of FST Taxation

Cash Flow Financial Projection

Management and Employees Statutory compliance

Author’s Note: while writing answers in exams, explain all the above points in one-two line each.

2. Hidden liabilities Overvalued assets

Show cause notice not matured into demand. Maybe material & imp.

Letters of comfort to Banks & Financial Institutions.

Tax liabilities Under direct & indirect tax

Long pending sales tax assess.

Pending final assess. of customduty

Agreement to buyback shares at stated price

Future lease liabilities

Unresolved labour litigations

Uncollected/uncollectable receivables.

Obsolete, slow non-moving inventories or inventories valued above NRV

Underused or obsolete Plant and Machinery and their spares asset

values which have been impaired due to sudden fall in market value etc.

Intangible assets of no value

Litigated assets and property.

Investments carried at cost though realizable value is much lower.

Investments carrying a very low rate of income / return.

Infructuous project expenditure/deferred revenue expenditure etc.

Work Approachto DD

Reviewing & reporting on the financials submitted by the target company

Accessing the business first hand by a site visit (if applicable)

Working through the due diligence process with the acquisitioning company (or) investor by defining the key areas

Helping prepare an offer based on completion of due diligence

How to conduct DD?

Start with open mind. Identify trouble spots & ask for explanation

Get best team of people. You may hire DD experts.

Get help in all areas to get 360-degree view of Co.

Talk to customers, suppliers, business partners, and employees are great resources.

Take a risk management approach.

Prepare comprehensive report detailing compliances & substantive risks/issues

Contents of DD Report

Executive summary

Introduction

Background of Company

Objective of DD

Terms of reference & scope of verification

Brief history of Company

Assessment of Financial Liabilities

Assessment of valuation of assets

Assessment of Net Worth

Assessment of Operating results

3. INVESTIGATION

Issues in Investigations

a) Whether an investigator is required to undertake 100% verification approach or selective verification approach.

b) Investigation out of disputes & conflicting claims.

c) Basis of opinion of an investor

d) Whether he can make futuristic statements

e) Whether to retain working papers or not.

f) Whether he can rely on the already audited FS

g) Whether he necessarily requires assistance of expert.

Types of Investigation

Investigation under Companies Act, 2013 Voluntary Investigation

Investigation into the affairs Investigation of Ownership

of the company u/s 210,212 & 213 u/s 216

For Incoming Partner

By Bank for Providing Loan

For Valuation of Shares

For buying Business

Investigation of Fraud

4. Investigation under Companies Act, 2013

Investigation vs Audit

Nature of Difference Investigation Audit

Objective It is inquiry in to facts Expressing opinion of Facts

Period No time fixed Quarterly, Half Yearly, Yearly

Inherent Limitations No Limitation Engagement suffers from Limitation

Evidence Conclusive Persuasive

Nature It involves detailed examination It involve sampling, Judgements

Reporting Authority initiating investigation Owners / Shareholders

Investigation in affairs of company u/s 210,212 & 213

Part-A Part-B

a) Who can initiate investigation: CG (u/s 210,213)

b) When

Suo Moto On the receipt of

(for Public Interest)

Report Intimation of SR Order of

from ROC by Company Court/NCLT

c) Who will conduct investigation - The CG may order, assign the

investigation into affairs of Company to SFIO. He shall follow the

manners and procedure as provided.

a) Who can initiate investigation: Tribunal

b) When: - on receipt of application from any person, if it is satisfied

then and is instances

Like:

-Defrauding creditors

-Company incorporated for useful purpose

-Not supplying information

c) If fraud is proven then :- Every officer of the company (or) mgmt shall

be punished for fraud (as per Sec 447)

Common point of part A and B

What powers the inspector posses:

Investigation may extend to company, it holding, its subsidiary or any other subsidiary of such holding company

Other body corporate having same management

Other body corporate accustomed to act as per director of co under investigation

Any person who was or is at any relevant time MD/ Manager/ Employee.

Obtain information and expiation.

Examine or both

He shall possess allpowers of civil court.

Apply to competent court to obtain evidence outside India.

5. Can keep the record in custody of 180 days which can be extended further 180 days

Approach/ steps for pursuingthe investigation

Ensure terms of engagement are not ambiguous

Inspector should evaluate history of the company and design scope of investigation

Plan period of investigation

Frame, programme of other expert Examine various records interpret result.

Consider assistance of other experts.

Complete finding and make final report on. the conclusive evidence or reporting should be as per provision of companies Act, 2013.

Authors Notes: - Student may use above content as General steps for conducting Investigation

Investigation of ownership of a company(Section 216)

a) Who can initiate: CG

b) Why: to determine the true person/s

Who have been financial interested in success/failure of Co. Who have been able to control materially influence of Investigation

c) What is scope and extent of investigation u/s 216

Clearly understand the scope of investigation

Determine the areas of accounts which require investigation and extent to which enquiry in to be made

In case of group companies, example intention of transfer securities all sales and purchases of goods from director and their associated

owners.

Investigate breach of duty or abdication of responsibility if it has resulted into loss.

Any negligence in the discharge of duty of a director (or) any other manager must be constructed very broadly, as they are trustees of its

property.

Conclusion can be drawn after understanding necessary leqal assistance and by evaluation all conclusive evidence

6. Voluntary Investigation

Investigation on behalf of an Incomingpartner

Reasons: To check whether terms offered to him are reasonable to check whether his contribution would be safe and applied usefully

Areas examined:

History of Firm Position of Assets & Liabilities Profitability

Capital Employed Goodwill of Firm Areas of Specification

Partnership Deed Range of Customer Term Loans

Reason of Admission Reputation of Partners Contractual Obligation

Investigation on behalf of bank proposing to advance loanto a company

Reasons: to evaluate credit worthiness of entity approaching for loan.

Areas examined:

Purpose of Loan Project Growth Integrity of Management

Value of Securities Condensed Income Statement Past records & Growth

Government Policies Various Ratios

Valuation of Shares

Methods

Net worth Approach Yeilds Approach

Value of Shares= Total Assets – Total Liabilities Value of Shares= Present Value of FMP

No. of Shares No. of Shares

Investigation on behalf of an Individual (or) a Firm proposingto buya business

7. Reasons: To collect information which would enable the purchases to decide whether it is worthwhile to buy the business, if so for what amount:

Areas Examined:

For Proprietary Audit For Company

Reason for sale of business Other than Points mentioned beside check

Length of Property Lease, if any Capital Structure

Unexpired period of patent Class and price of shares

Managerial Staff Dividends

Customer Base Mortgages, if any

Goodwill

Investigation of Frauds:-

Fraud is intentional act, executed to gain unjust/illegal advantage. It includes misappropriation of money (or) goods, manipulation of accounts, etc

(i) Frauds at different Level

Fraud for Personal Gain Corporate Frauds / Irregulation Fraud at Operational Level

Bribery Advance Billing Tampering of cheques/ drafts/

online payment/ Receipts

Shell/Dummy Company Schemes

Money Laundering Activities Off Book Frauds

Cash Misappropriation

Teeming and lading

Fraudulent disbursement

Expense disbursement Schemes

Payroll Fraud

Commission Schemes

(ii) Verification of Fraud in

Fraud for Personal Gain Corporate Frauds / Irregulation Fraud at Operational Level

Different sources of Income Internal Controls Goods inwards Book

Completeness of Income accounted Acknowledgment Credit for goods received

Negligible source of income Bearer Cheques Rebates

Copies of Receipts Petty Cash Related Parties

Cash Discounts Unusual Payments Balance Confirmation

Serially numbered Dummy Workmen

Cancelled Receipts Alternations in payments

8. Cash Deposited & Withdrawal Related Parties

Cash Sales

(iii) Areas to be examined if in spite of increase in sales turnover there is decline in profits

Unfavourable sales mix Competitive Price

Negative impact of Financial Leverage Additions to Fixed Assets (depreciation)

Cost included in Sales Lost Price Relationship

High Admin Cost

(iv) Factors considered in assessing the future maintainable turnover

Trend Marketability

Political / Economic Condition Competition

(v)