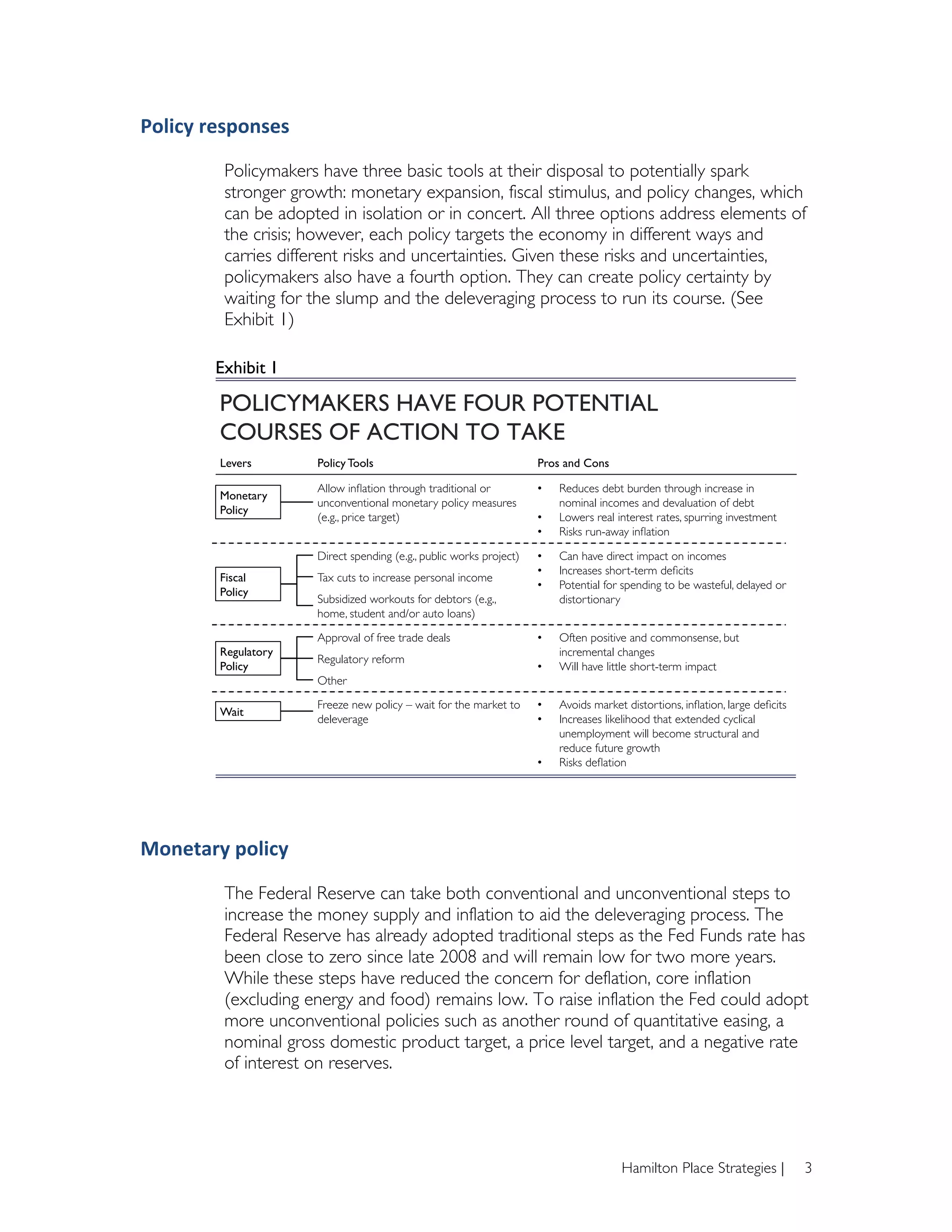

The document discusses four potential policy options to address the ongoing economic challenges: monetary policy, fiscal policy, regulatory policy changes, and waiting for the deleveraging process to run its course. Monetary policy could increase inflation to reduce debt burdens, but also carries risks of runaway inflation. Fiscal stimulus through spending and tax cuts could boost incomes, but impact may be delayed and increase deficits. Targeted debt relief programs could directly reduce household debt levels with less deficit impact compared to broad stimulus. Regulatory reforms may have limited short-term effect. Simply waiting risks prolonged high unemployment and possible deflation.