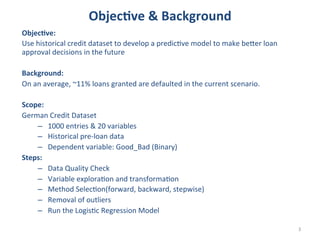

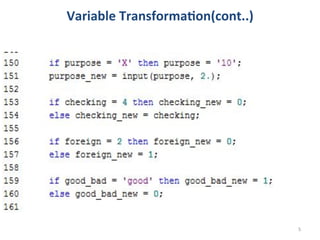

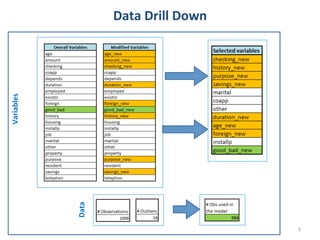

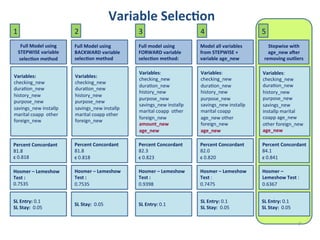

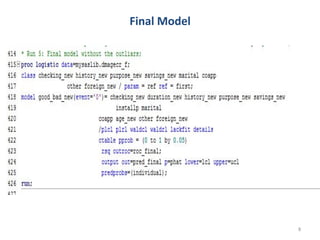

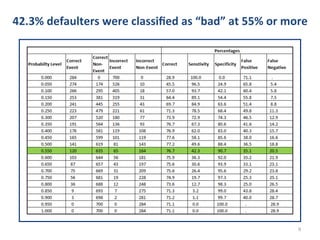

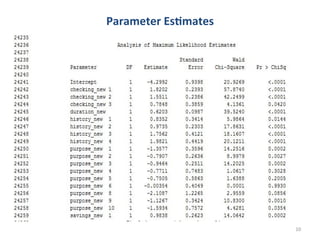

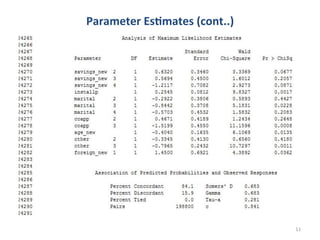

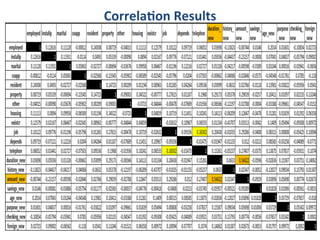

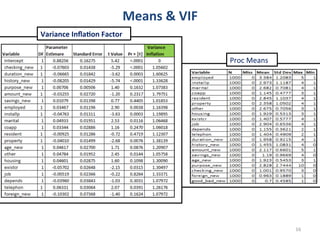

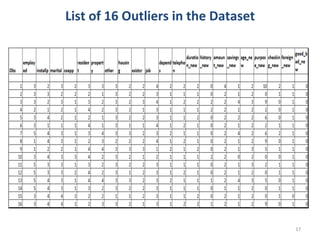

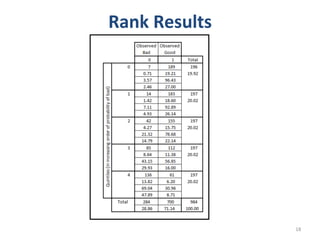

The document outlines a predictive model developed using a historical credit dataset to improve loan approval decisions, noting that approximately 11% of loans currently granted default. It details the methodology, including data quality checks, variable selection using different methods, and the final model's performance metrics, revealing that a significant percentage of defaulters can be classified. Additionally, it provides characteristics to avoid targeting in loan approvals, based on the model's estimates.

![[rokonz.com] Glossary of Semantic SEO Part-1.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/rokonz-260123200456-440e4060-thumbnail.jpg?width=640&height=640&fit=bounds)

![[EN].CleverGroup Vietnam Profile 20251202](https://cdn.slidesharecdn.com/ss_thumbnails/en-260120091417-fe6f88ec-thumbnail.jpg?width=640&height=640&fit=bounds)