BNPL also knownas Buy Now Pay Later is a payment

option where you can make a purchase without

having to pay the full amount at the time of purchase.

Typically, you sign up with a company providing this

facility who makes the payment when you make the

purchase. However, once the lender pays on your

behalf, you will have to repay the amount within a

specified time period. When compared to a personal

loan, generally no interest is levied under the BNPL

scheme. You can either pay it as a lumpsum amount,

or you can pay it via no cost Equated Monthly

Instalments (EMIs). If you fail to pay the amount

within the given repayment tenure, then the lender

will be liable to charge you interest on your amount.

Further delay could impact your credit score.

3.

Here's how BNPLusually works:

1. Customer make a purchase at a participating

retailer.

2. Opts for the ‘Buy now, pay later’ option.

3. Makes a small down payment of the overall

purchase amount and completes the

transaction.

4. The remaining amount shall be deducted in a

series of interest-free EMIs.

5. The payment of EMIs is made via bank transfer,

cheques, credit card, debit card or directly from

the bank account.

4.

Increases affordability

Instant access to credit

Safe and secure transaction

Can choose repayment tenure

No cost EMI

Simple process

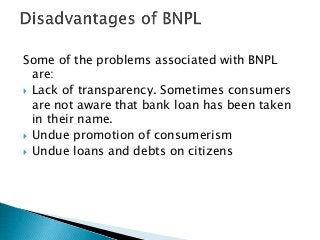

5.

Some of theproblems associated with BNPL

are:

Lack of transparency. Sometimes consumers

are not aware that bank loan has been taken

in their name.

Undue promotion of consumerism

Undue loans and debts on citizens

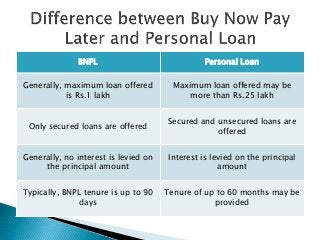

6.

BNPL Personal Loan

Generally,maximum loan offered

is Rs.1 lakh

Maximum loan offered may be

more than Rs.25 lakh

Only secured loans are offered

Secured and unsecured loans are

offered

Generally, no interest is levied on

the principal amount

Interest is levied on the principal

amount

Typically, BNPL tenure is up to 90

days

Tenure of up to 60 months may be

provided

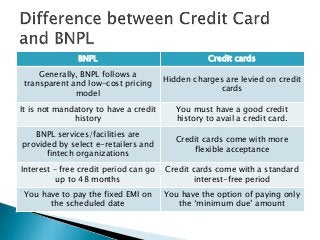

7.

BNPL Credit cards

Generally,BNPL follows a

transparent and low-cost pricing

model

Hidden charges are levied on credit

cards

It is not mandatory to have a credit

history

You must have a good credit

history to avail a credit card.

BNPL services/facilities are

provided by select e-retailers and

fintech organizations

Credit cards come with more

flexible acceptance

Interest – free credit period can go

up to 48 months

Credit cards come with a standard

interest-free period

You have to pay the fixed EMI on

the scheduled date

You have the option of paying only

the ‘minimum due’ amount

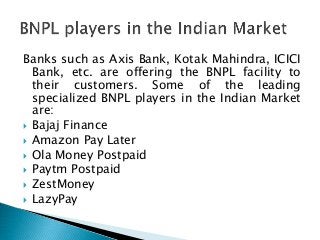

8.

Banks such asAxis Bank, Kotak Mahindra, ICICI

Bank, etc. are offering the BNPL facility to

their customers. Some of the leading

specialized BNPL players in the Indian Market

are:

Bajaj Finance

Amazon Pay Later

Ola Money Postpaid

Paytm Postpaid

ZestMoney

LazyPay

9.

BNPL makes moneyfrom both sellers and

consumers. In case of sellers, they pay BNPL a

fee ranging between 2% and 8% of the

purchasing amount if the customer uses the

BNPL facility. BNPL players also make money

from customers by charging an interest on

delays ranging between 10% and 30% based

on their credit score, repayment tenure, etc.

10.

Many fintechfirms have stopped the buy now pay later

(BNPL) services after a recent Reserve Bank of India

notification. The new guidelines, issued by the RBI last

month, stopped non-bank prepaid payment instruments

(PPIs) from being loaded with credit lines. The central

bank's move comes amid rising concerns over card-based

credit services and PPIs being loaded through credit lines.

According to the RBI, the new credit instruments could

result in systemic risk. The new-age fintech firms are

using lines of credit from banks and non-banking financial

companies (NBFCs) to load customer wallets. The bank

regulator is apprehensive about a lack of due diligence

while loading the PPIs through credit lines.

11.

The newRBI guidelines, issued on June 20, have

sent the fintech companies into a tizzy and many

have temporarily stopped prepaid instruments.

According to the new directive, non-banking

companies cannot offer credit cards or other PPIs

without the prior approval of RBI. However, the

customers can load their pre-paid wallets with

cash or use credit and debit cards issued by their

banks for the same.

Fintech firms have requested a clarification from

the RBI as the new guidelines have caused a

disruption in the industry, especially adversely

affecting small players.

12.

Fintech startup PayUIndia's lending platform,

LazyPay, has temporarily discontinued its buy

now pay later product LazyPlus UPI. Online

credit service platforms Jupiter, EarlySalary

and KreditBee have temporarily halted all

transactions through their prepaid

cards. Slice and Uni also have restricted

issuances of new credit cards after the RBI

directive, the ET report mentioned quoting

sources.