Downloaded 22 times

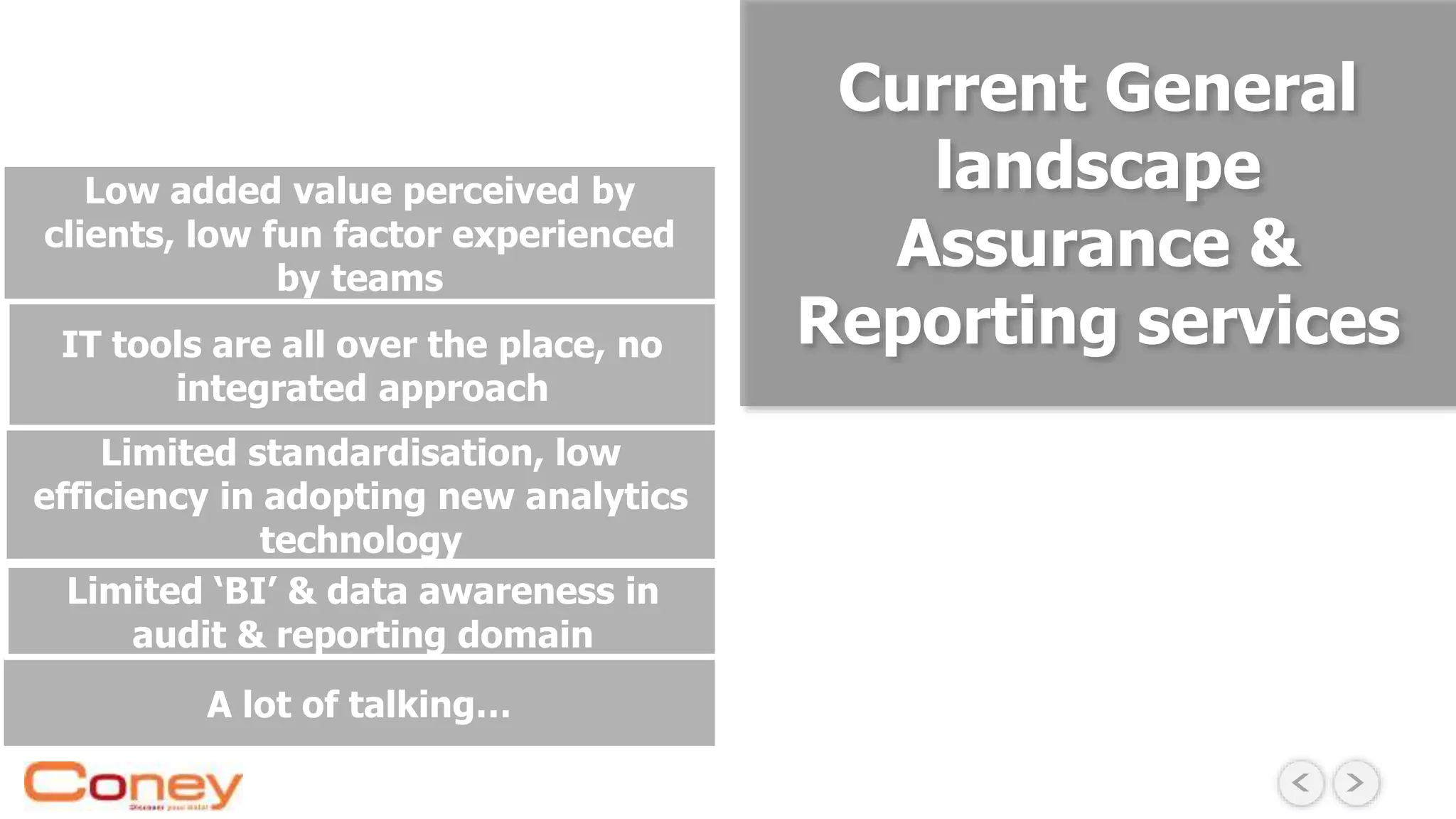

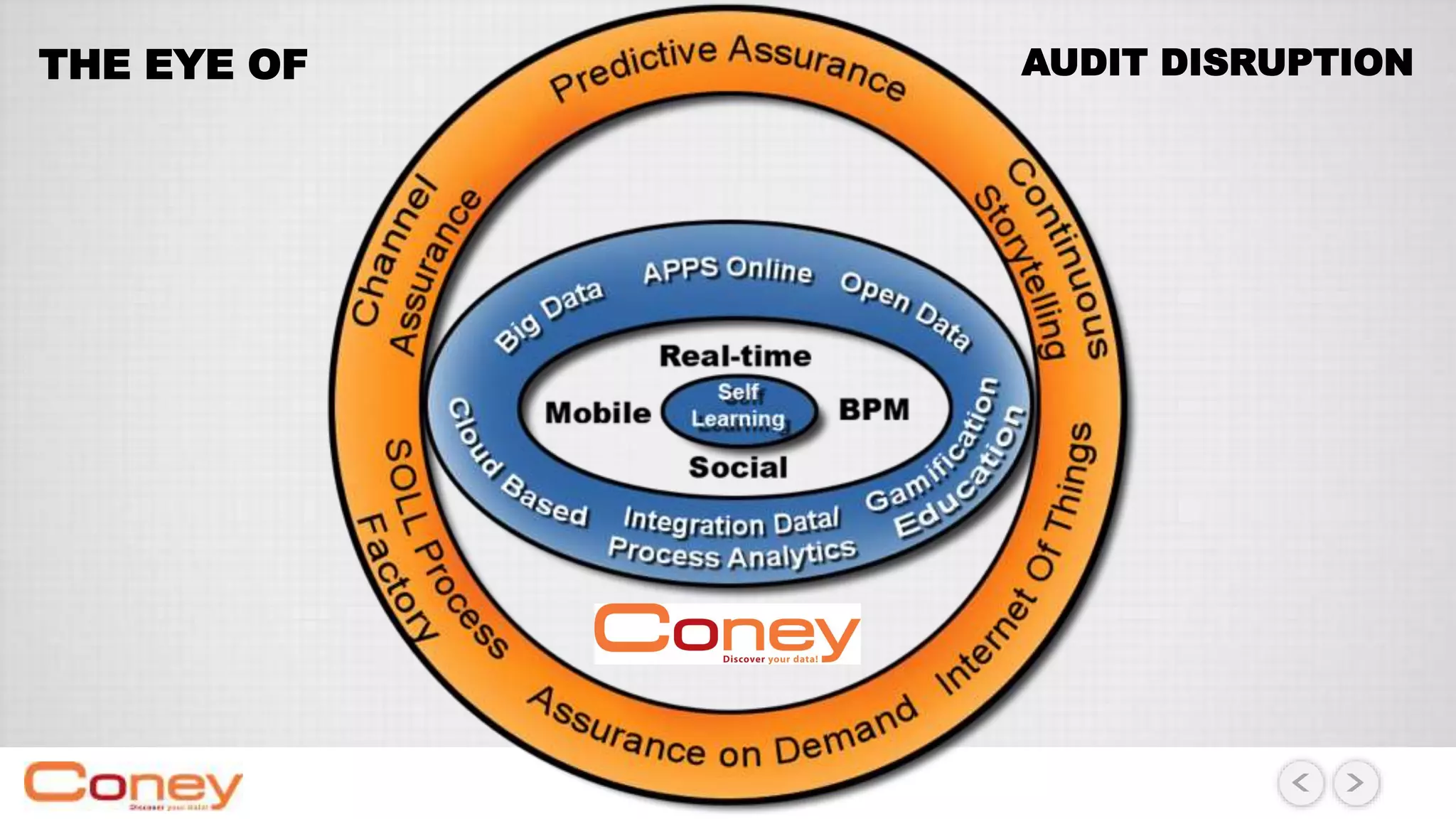

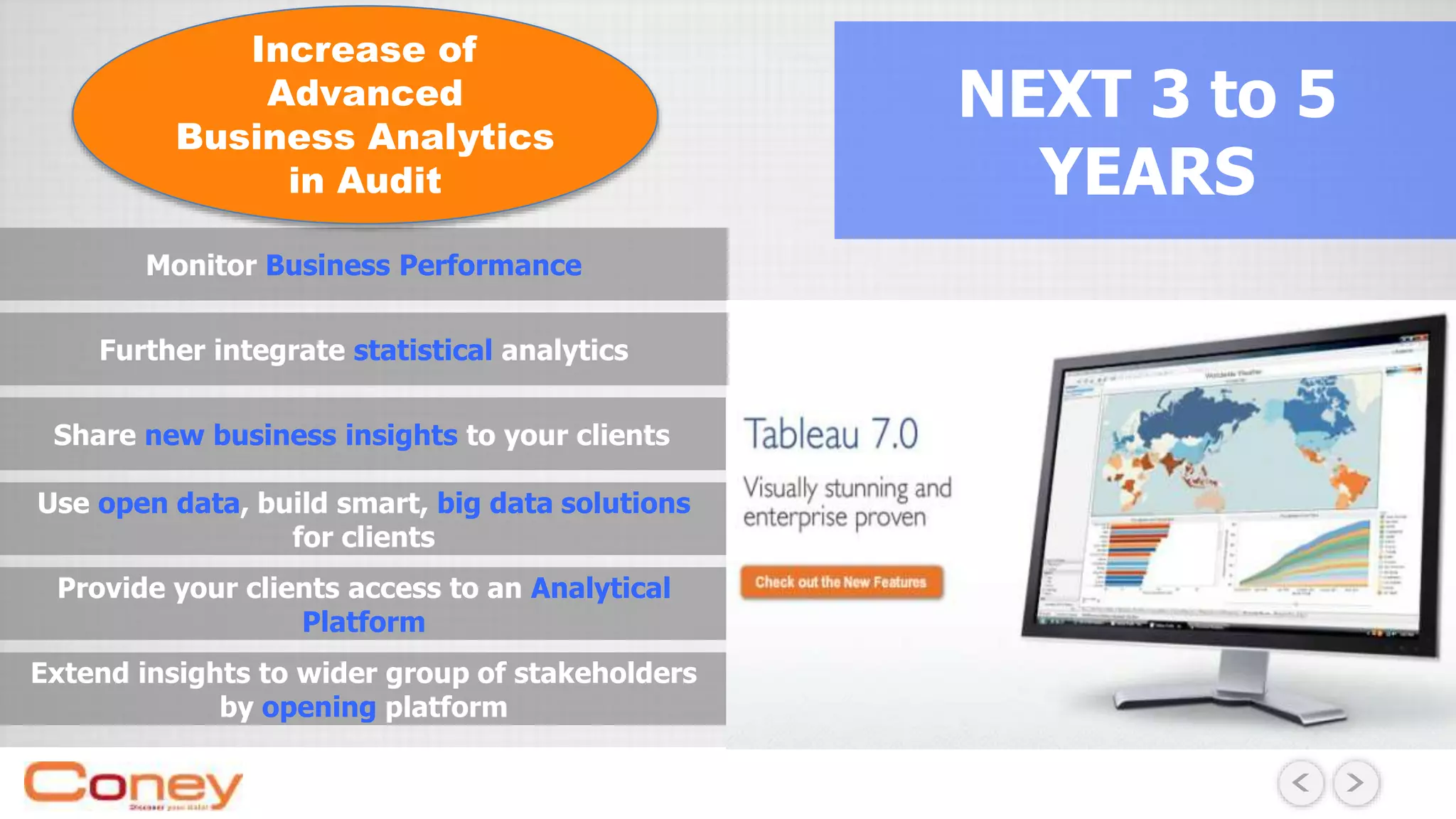

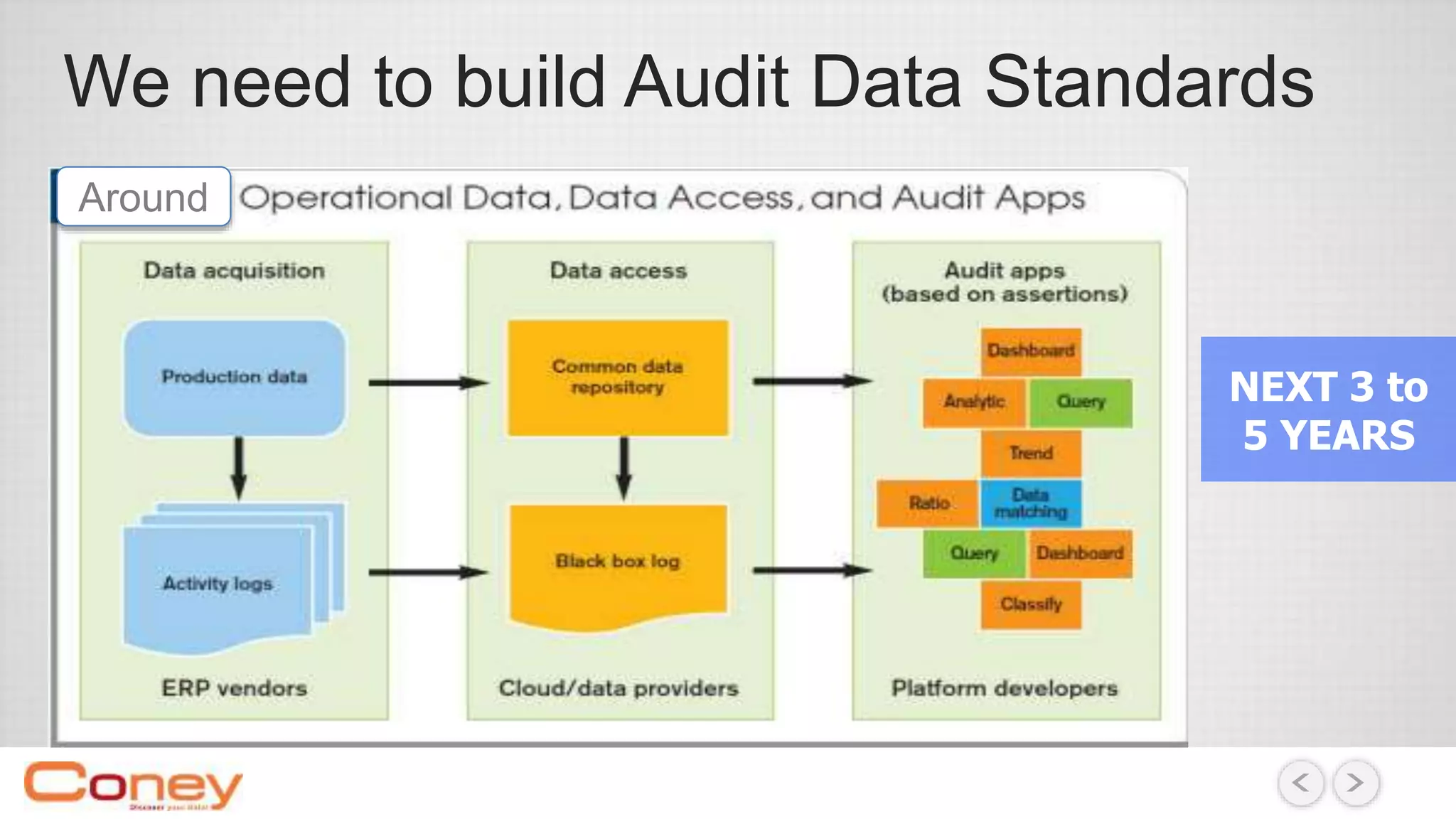

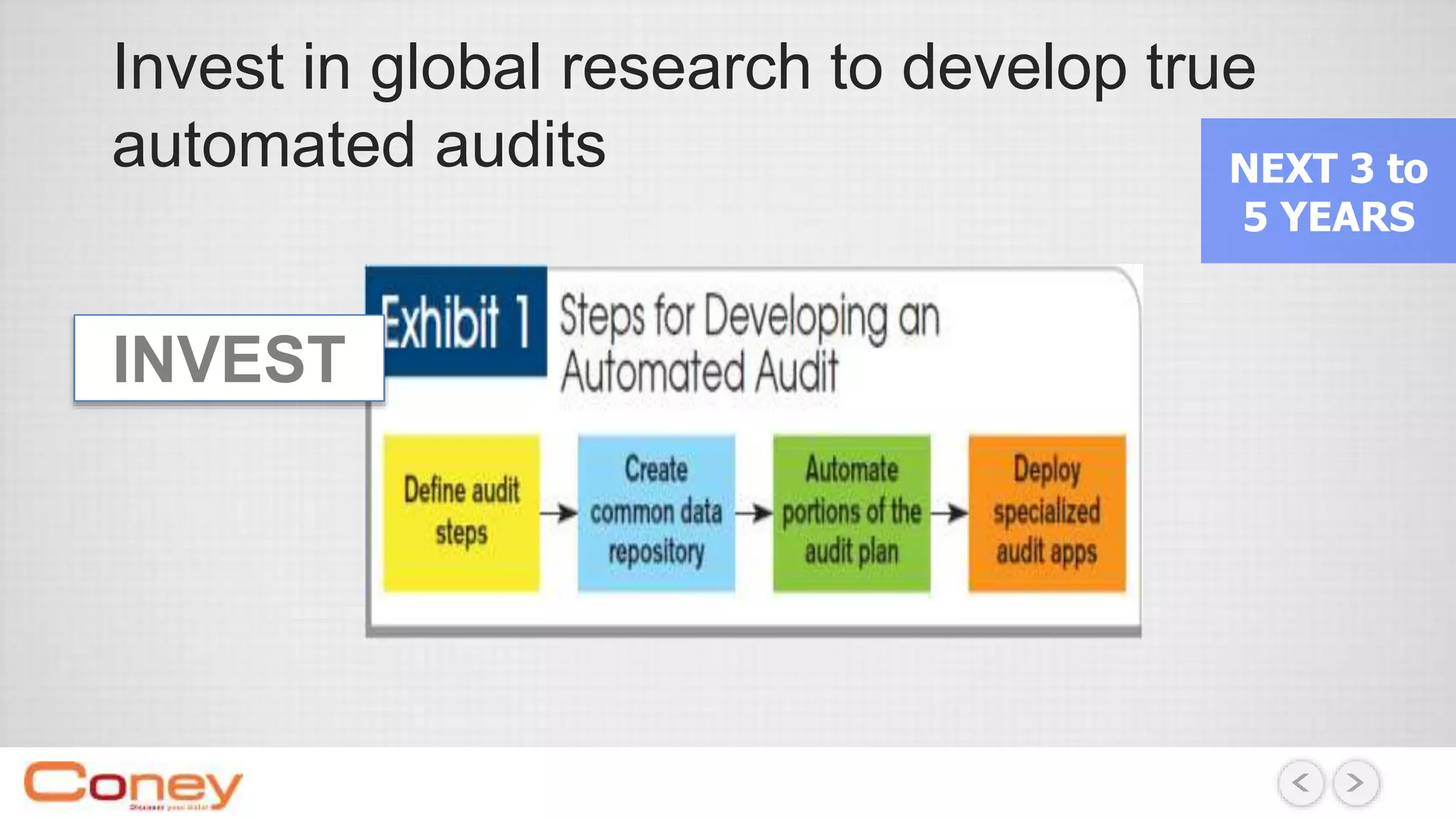

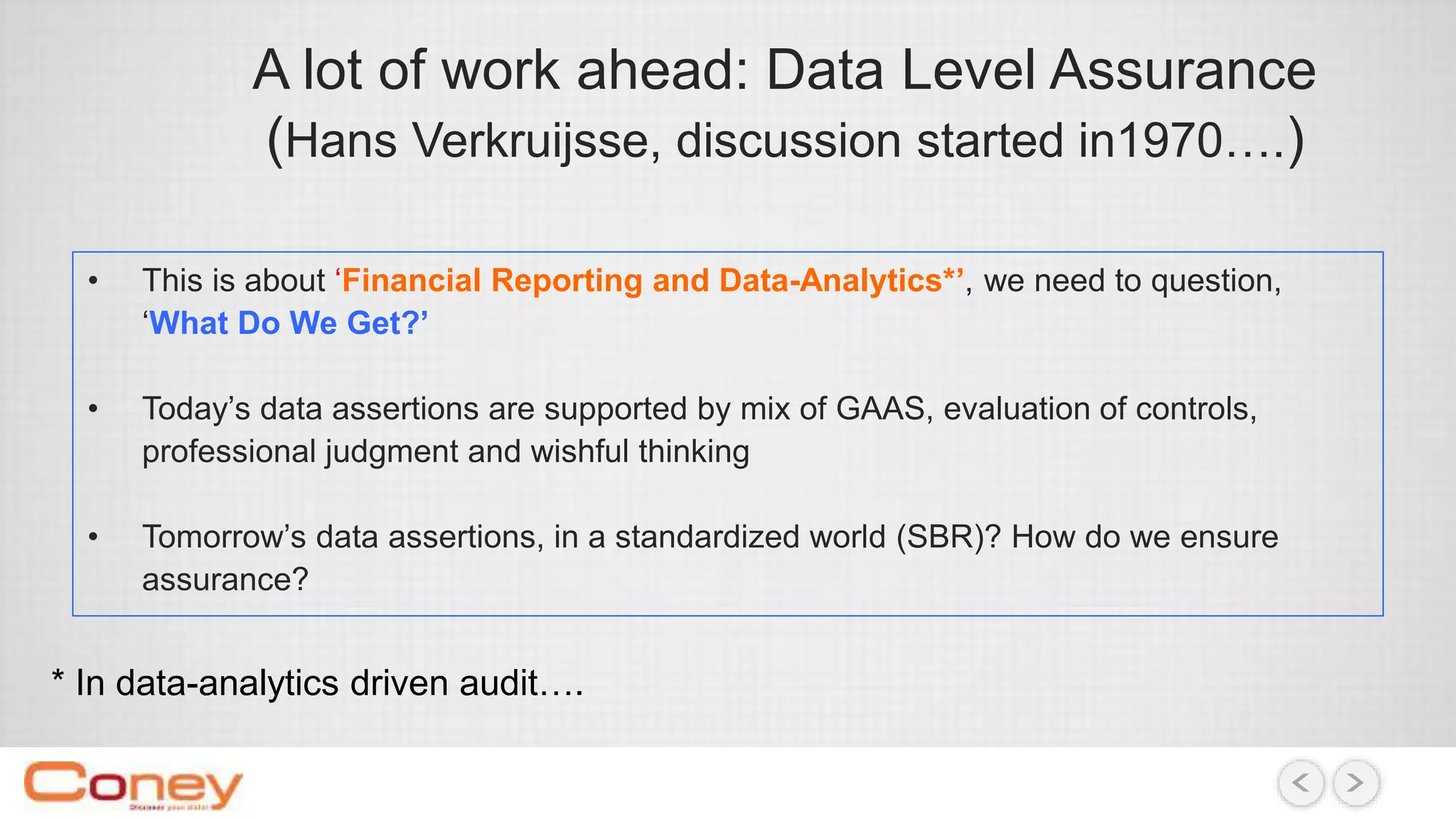

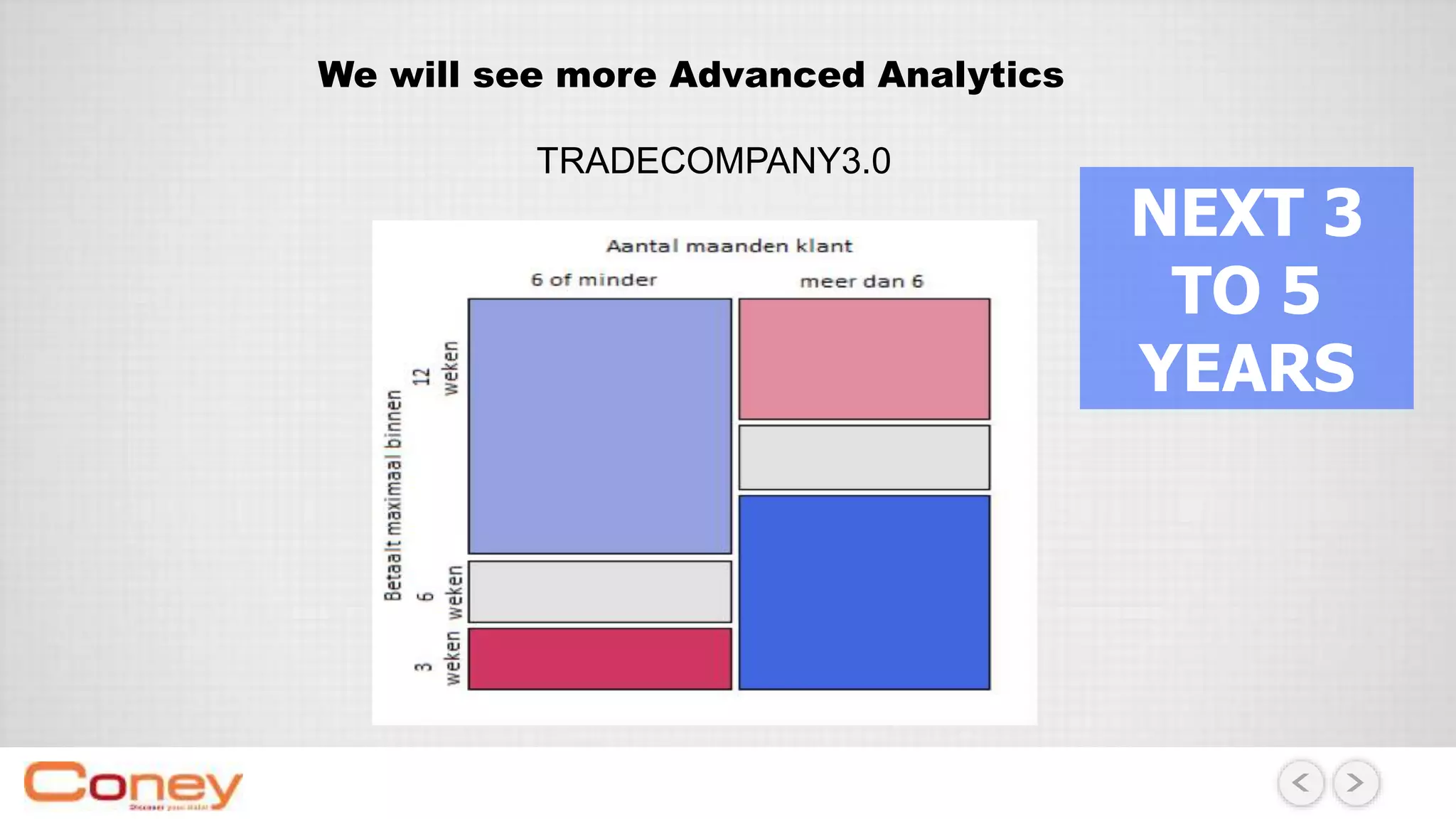

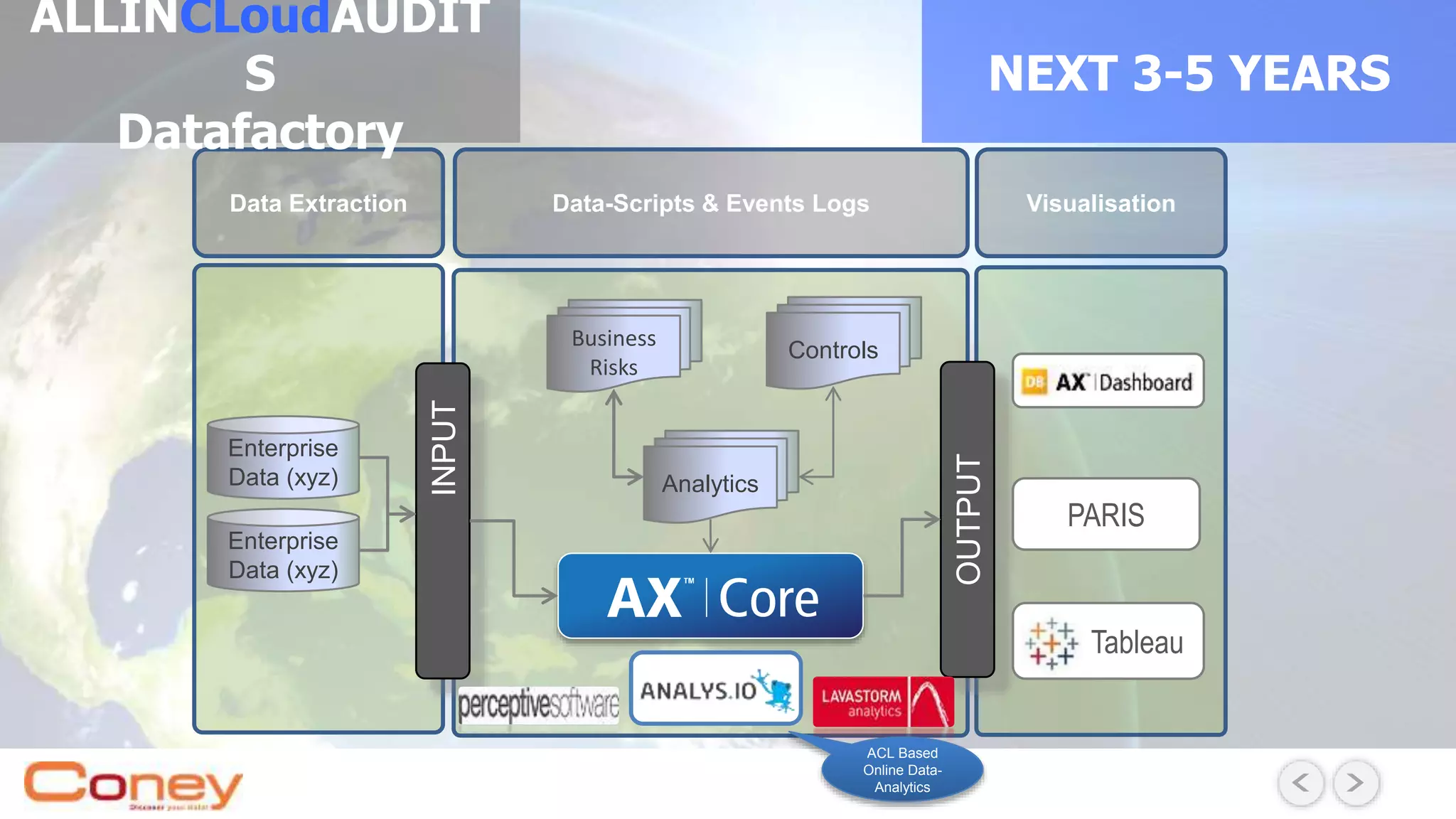

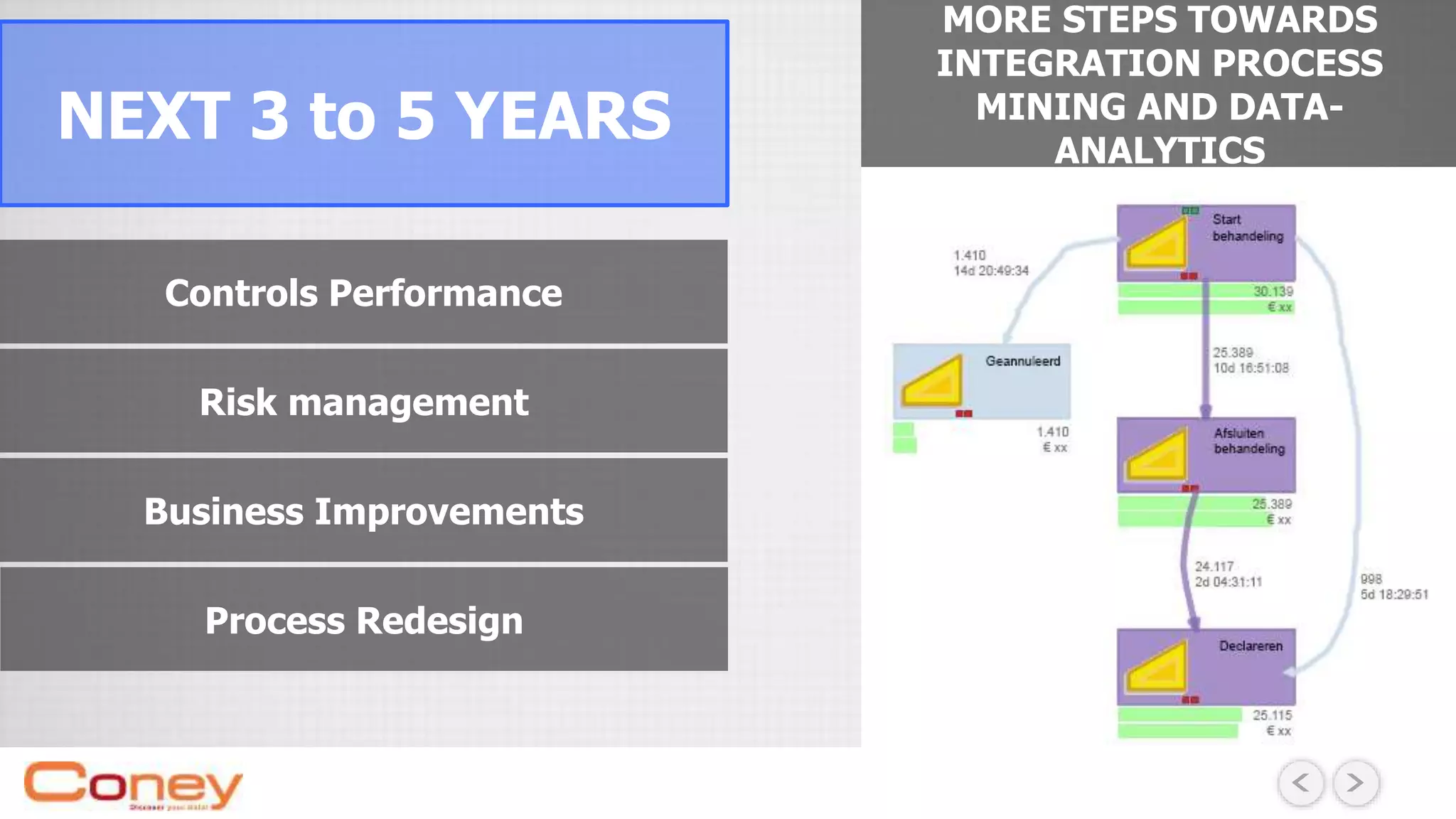

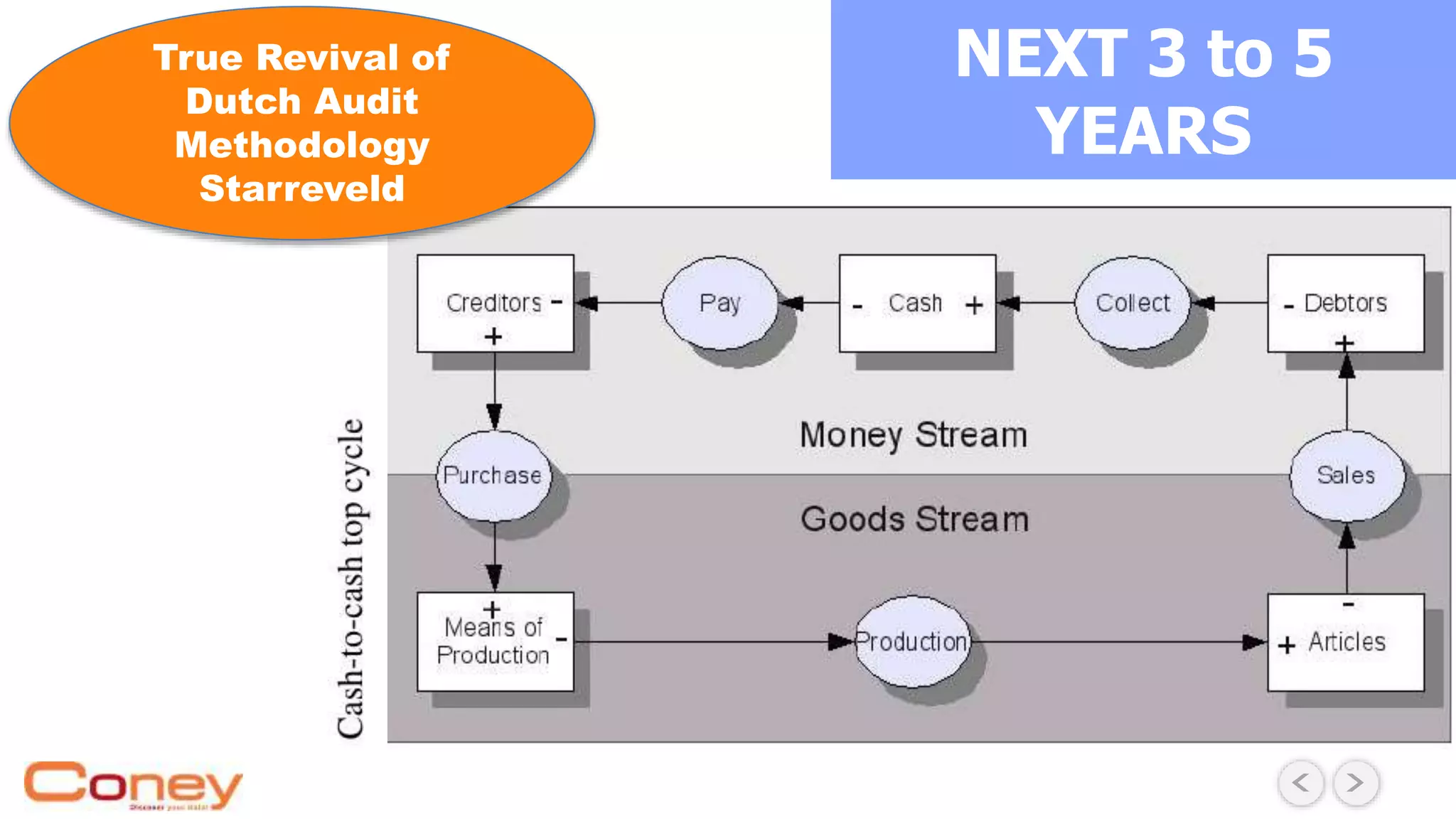

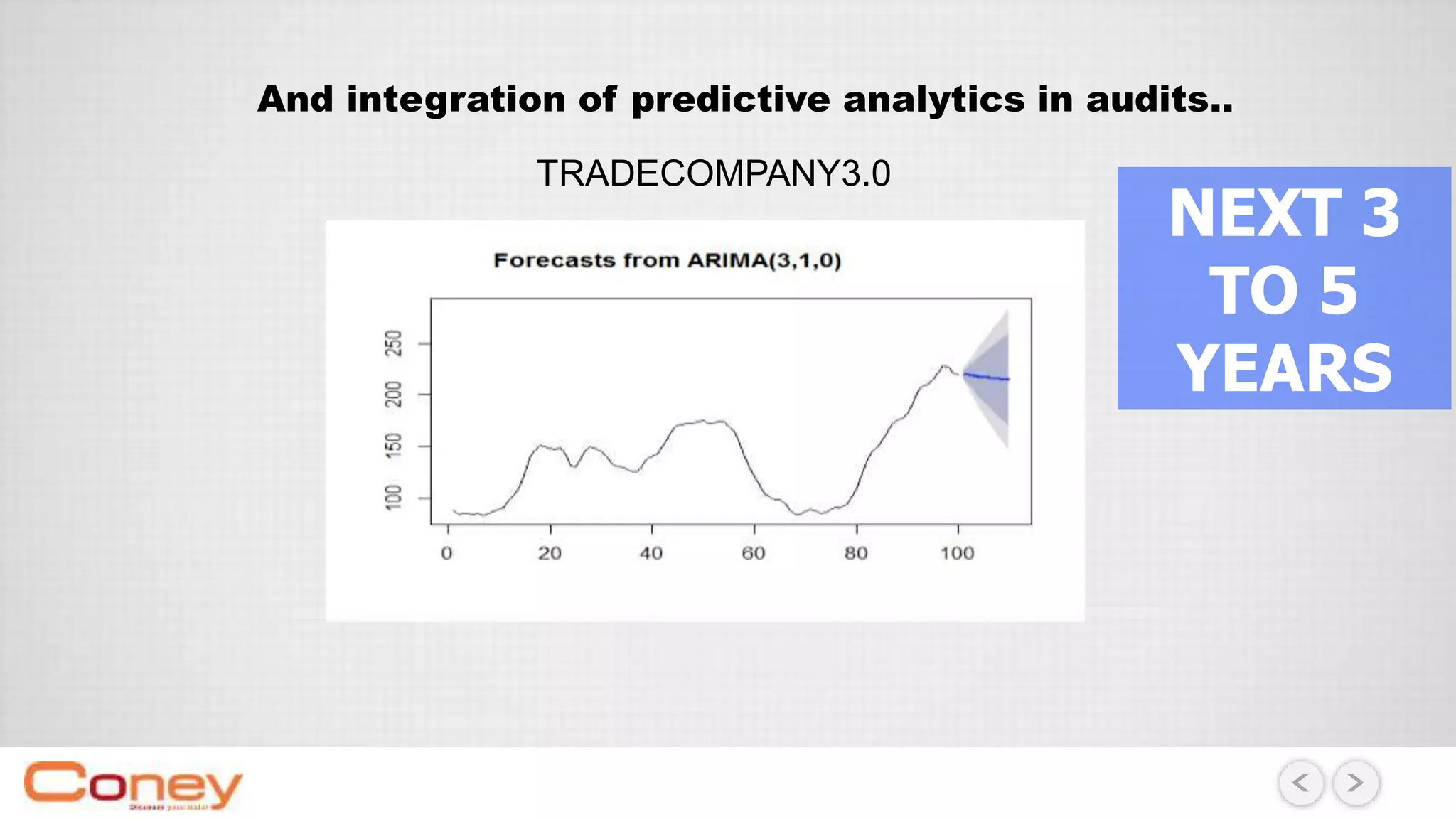

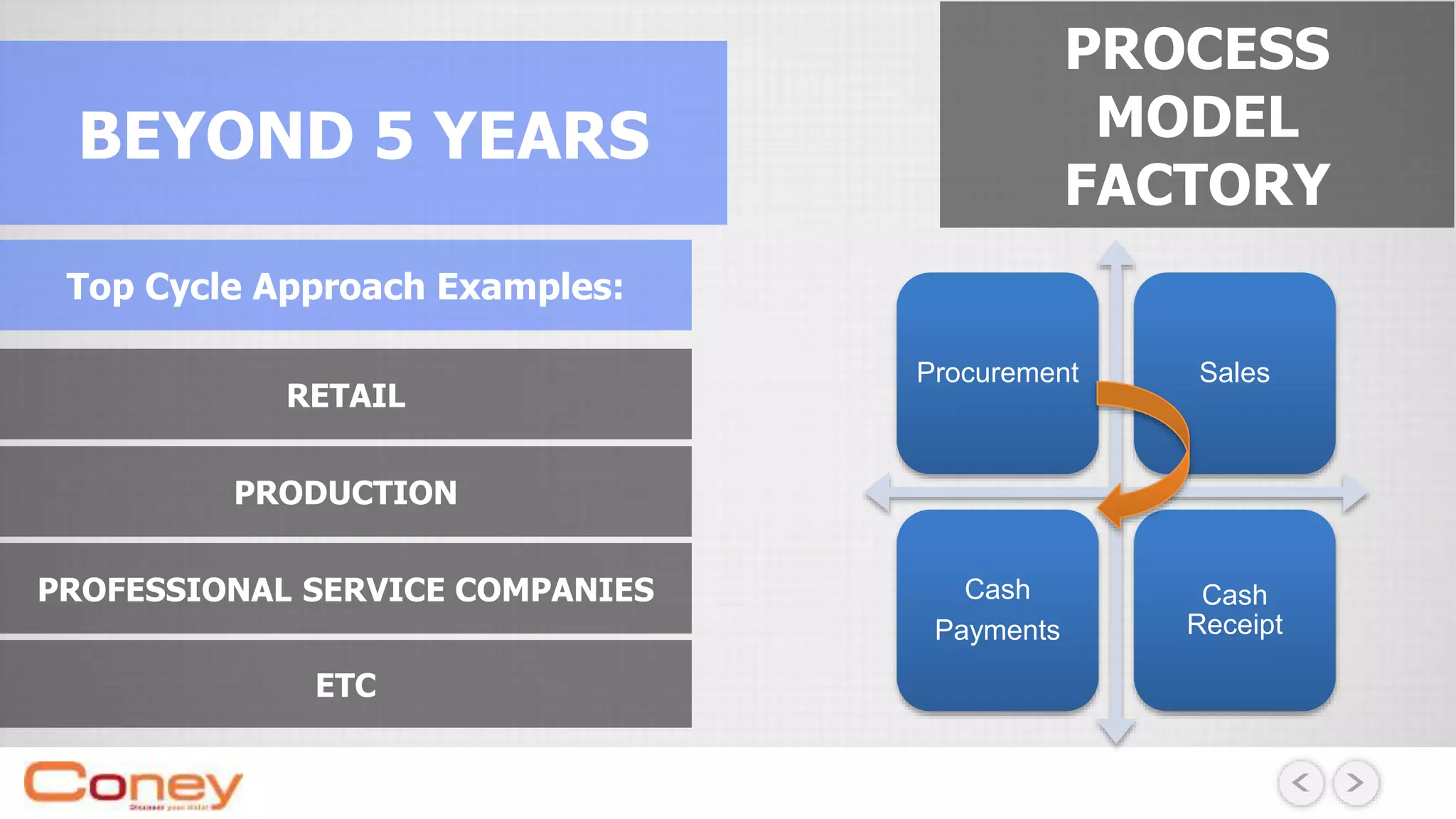

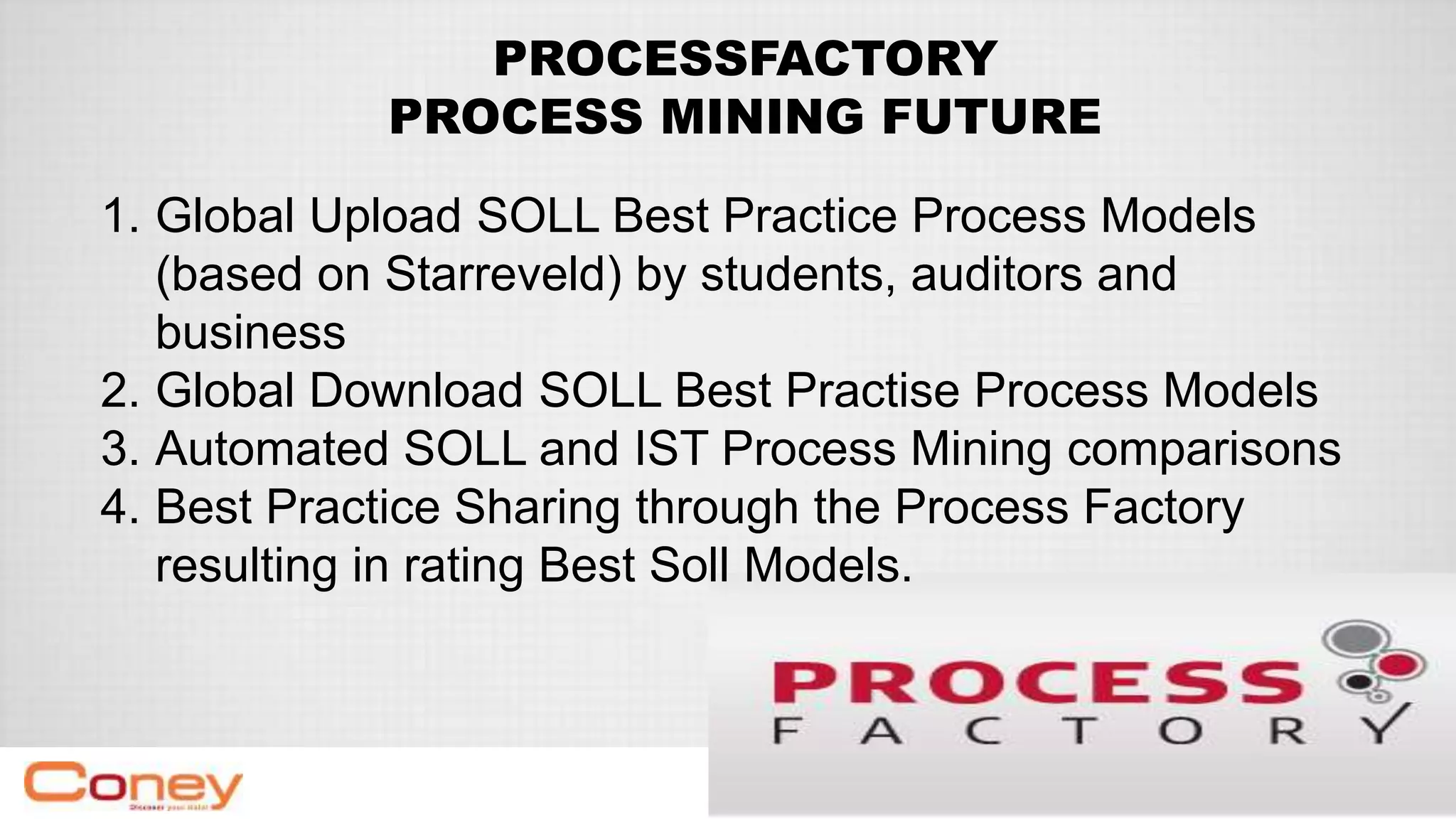

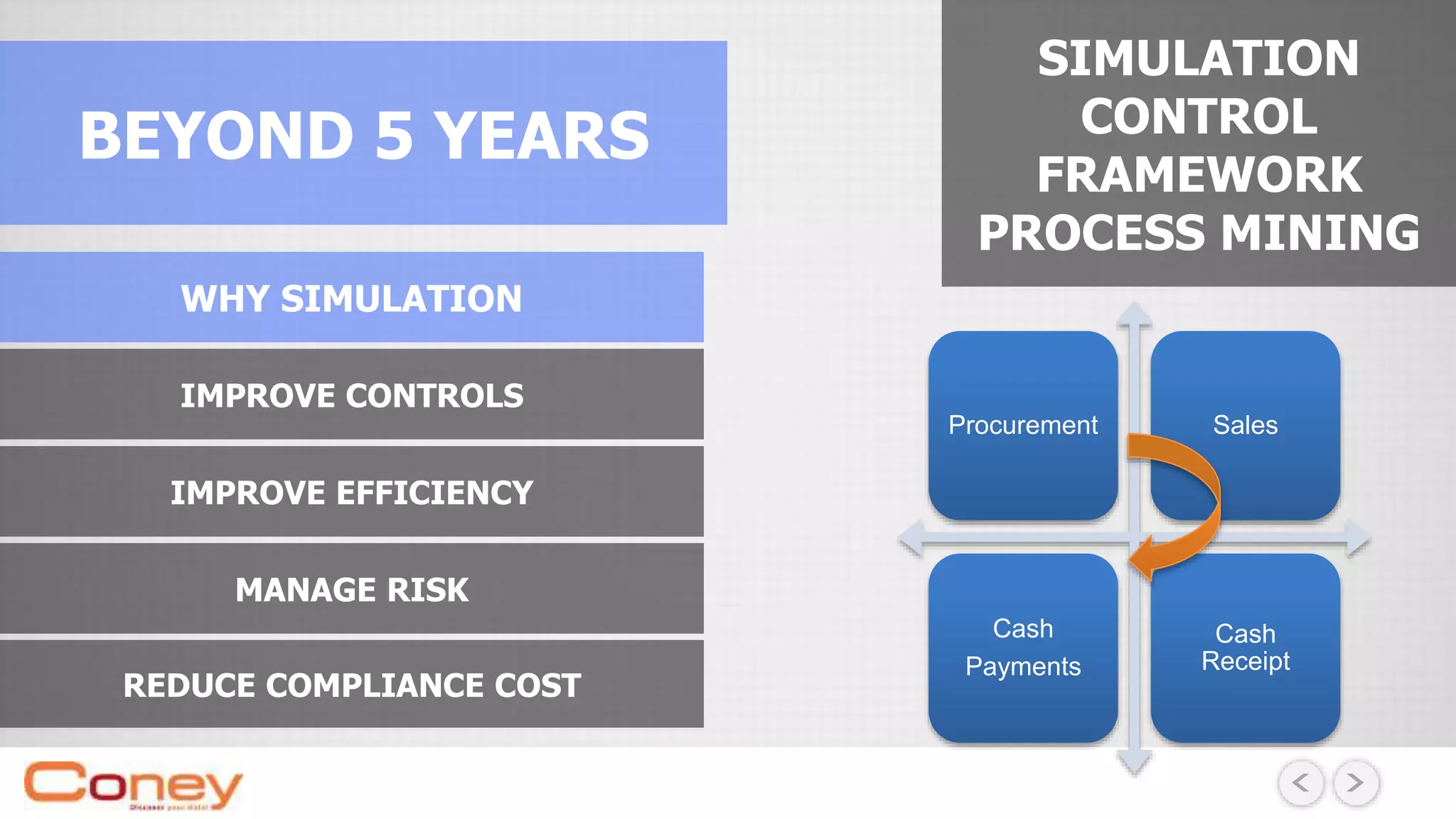

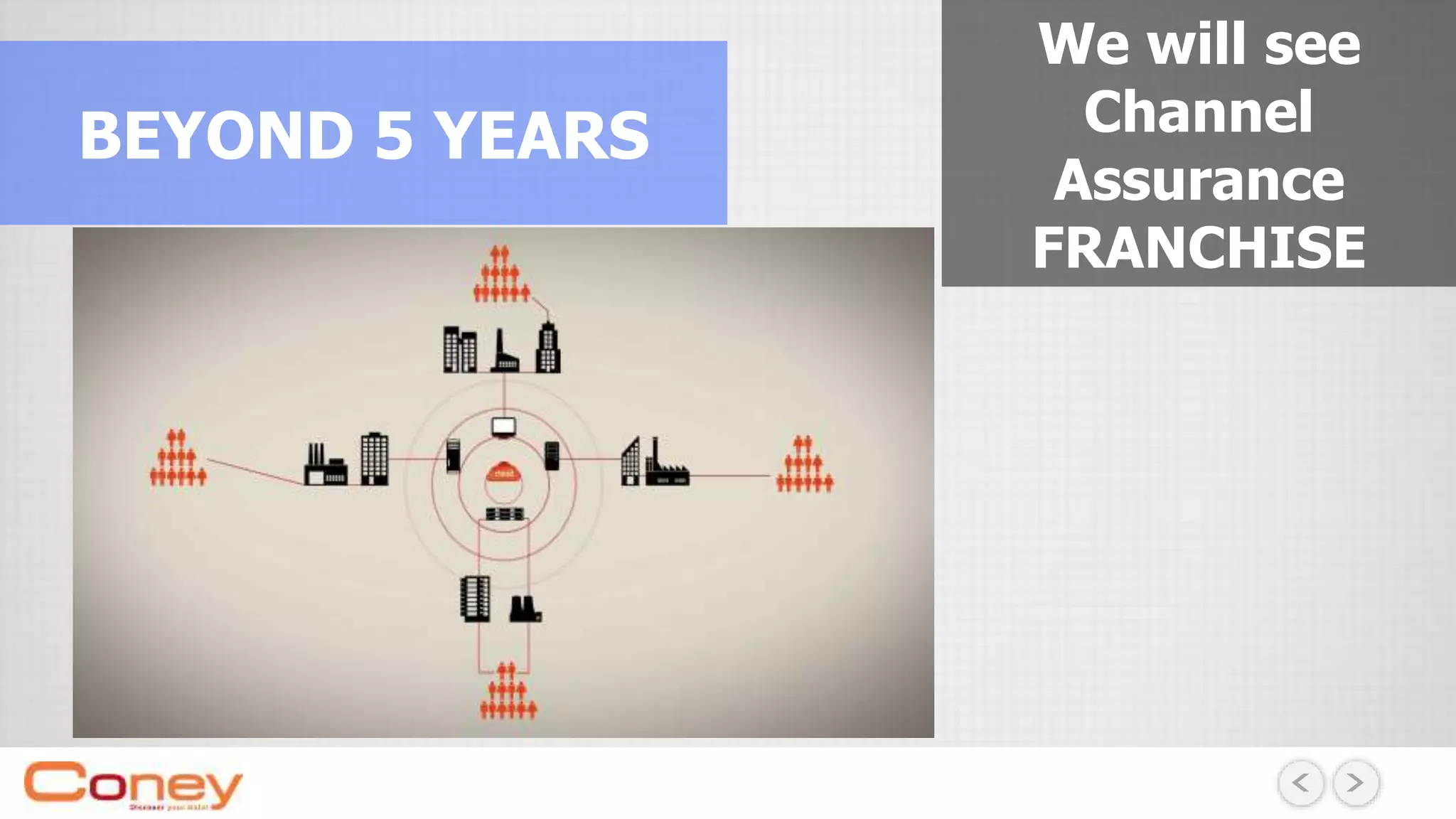

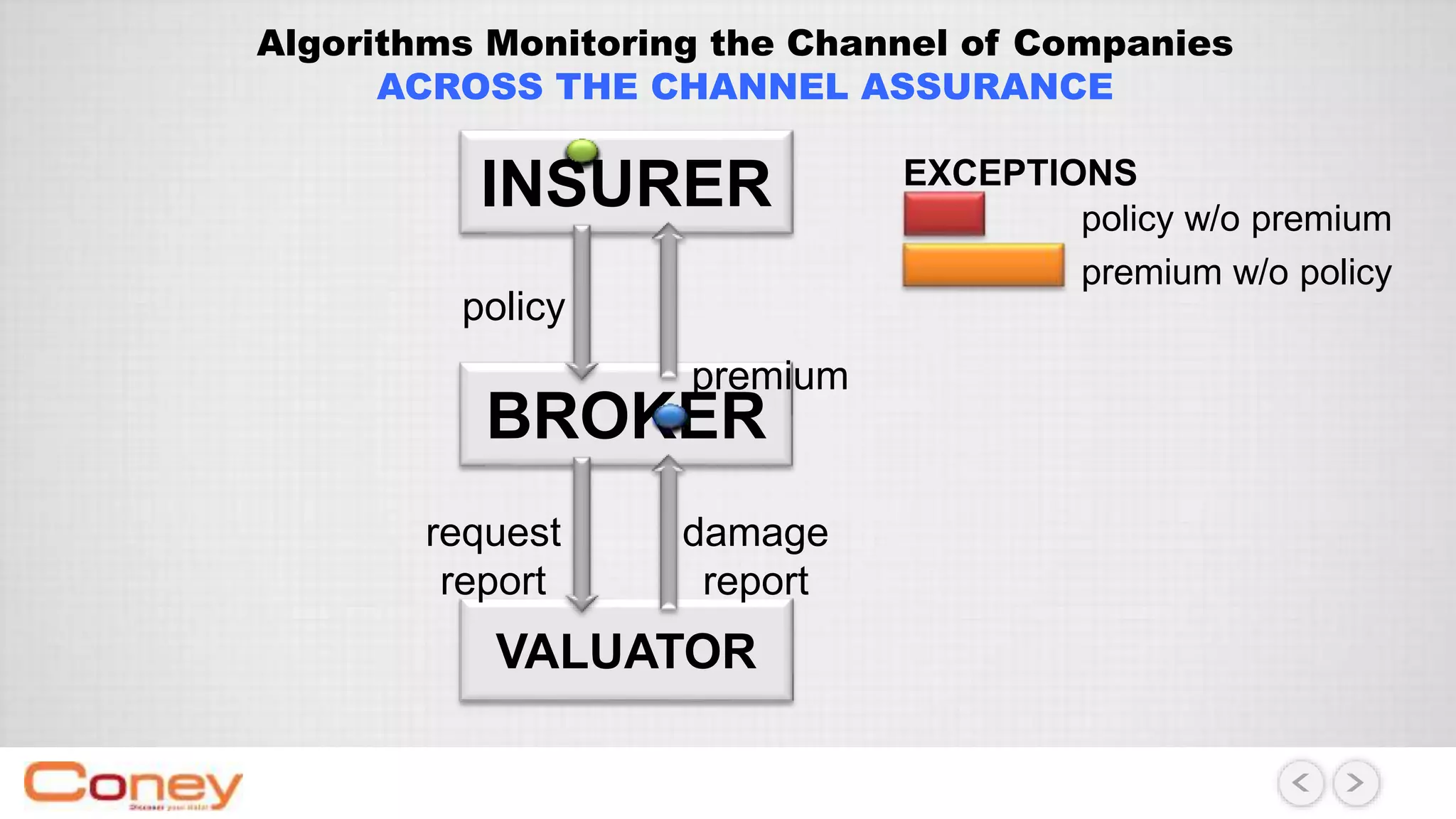

The document discusses the future of auditing, emphasizing the need for integration of advanced data analytics and process mining to improve efficiency and client value. It outlines key objectives for enhancing assurance services over the next 3 to 5 years, including the development of standardized audit data, automation of audit processes, and the use of predictive analytics. Furthermore, it anticipates a shift towards 'assurance on demand', utilizing new technologies and media for a more responsive and engaging auditing approach.

![[DSC Europe 25] Tatevik Maytesyan - How to actually use AI in marketing: gett...](https://cdn.slidesharecdn.com/ss_thumbnails/tjo626lsqdgfntbgl2mw-4-251216103155-e36cd239-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Jean Del Rosario - How to Reduce GenAI Costs up to 73.45%.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/zjehcwqsiwjisav1znml-5-251217093201-eae4440a-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Miodrag Pesovic & Vladislav Radonjic - Federated Data Archite...](https://cdn.slidesharecdn.com/ss_thumbnails/gsbe3y5it5uhndi4e08e-1-251212103249-f1008e0c-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Ivan Petrovic - Is it really that expensive to build an AI sy...](https://cdn.slidesharecdn.com/ss_thumbnails/ybqhdwvusbg7jms3doxh-9-251216105605-7aab5a10-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Francisco Prado Moreno - Model Validation in the Age of AI: T...](https://cdn.slidesharecdn.com/ss_thumbnails/2igqvkir1yd2yzlhoylg-3-251215095918-6676c4e6-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Velibor Ilic - Autonomous Driving - How AI Shapes Technical ...](https://cdn.slidesharecdn.com/ss_thumbnails/gwu9aqths9ovngsrhidc-3-velibor-ilic-autonomous-driving-how-ai-shapes-technical-challenges-251219150035-7436923a-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Djordje Hirs - Revolutionizing Telco Customer Experience with...](https://cdn.slidesharecdn.com/ss_thumbnails/zif75aur3qscnckv6tnc-djordje-hirs-cc-dsc2025-1-251219145617-679178aa-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Dobrica Cosic - From Electrons to Innovation: How Granular Da...](https://cdn.slidesharecdn.com/ss_thumbnails/h4qk69zereaumbceubgr-dobrica-cosic-from-electrons-to-innovation-how-granular-data-and-analytics-are--251218085301-b982fb14-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Mathias Halkjær Petersen - The AI workforce revolution.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/3xviexv7q5gojhdsyvat-the-ai-workforce-revolution-251218084820-f3c286ed-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Maria Kokiasmenos - AI Governance US Perspective.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/eszqnbzlsqa2vch6dmci-6-251215095918-6fcdf45f-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Katherine Forrest - AI NOW: Understanding the Velocity of Cha...](https://cdn.slidesharecdn.com/ss_thumbnails/wvvbruqfrci0sfq9xwgb-4-251212104007-e5ad1987-thumbnail.jpg?width=640&height=640&fit=bounds)