Downloaded 126 times

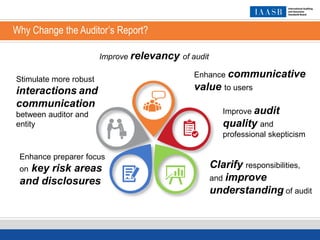

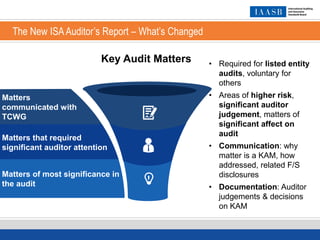

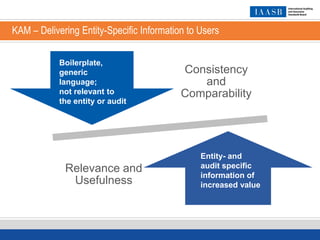

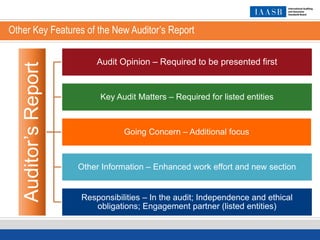

The document outlines the changes to the auditor's report aimed at improving communication between auditors and entities, enhancing focus on key risk areas, and clarifying responsibilities. Key Audit Matters (KAM) are introduced to provide entity-specific information, which is particularly mandatory for listed entities. The overall goal is to enhance audit quality, professional skepticism, and the relevance of the audit report to users.