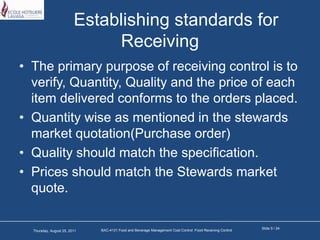

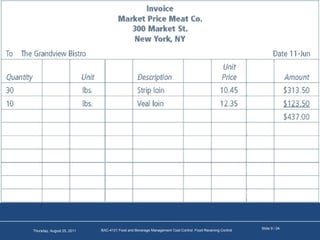

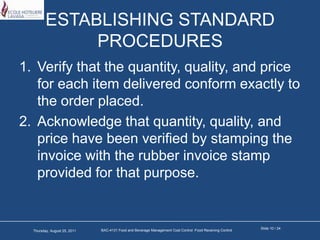

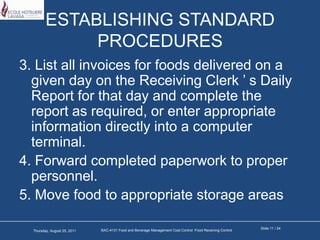

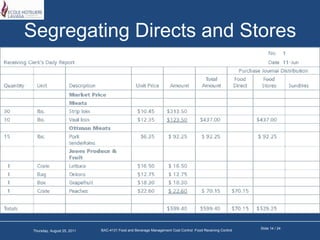

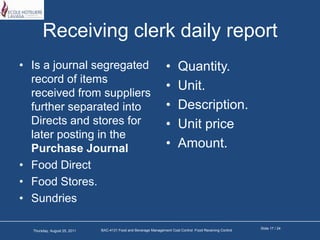

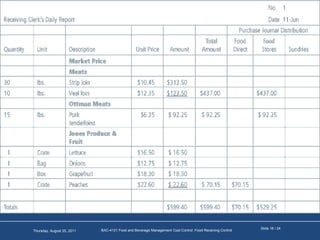

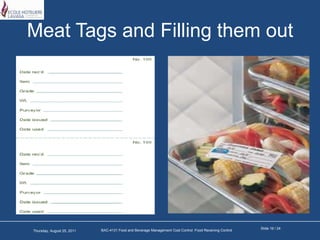

The document discusses food receiving control procedures. It outlines establishing standards for receiving, including verifying quantity, quality, and price against purchase orders. It also describes segregating foods into directs and stores, completing a receiving clerk's daily report, and properly tagging and storing received foods. Common oversights in receiving like accepting incorrect quantities or faulty expiration checks are also noted.

![Facilities design, décor and cleaning [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/facilitiesdesigndcorandcleaningcompatibilitymode-131126044615-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![Menu the foundation for control [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/menuthefoundationforcontrolcompatibilitymode-130708052052-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![Security and the lodging industry [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/securityandthelodgingindustrycompatibilitymode-130119023537-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![The challenge of f&b operations [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/thechallengeoffboperationscompatibilitymode-130116220357-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)