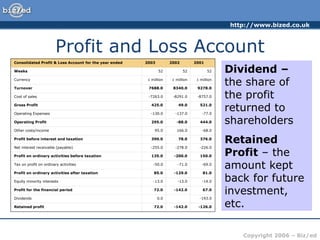

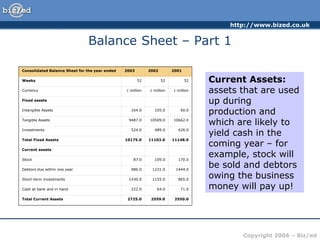

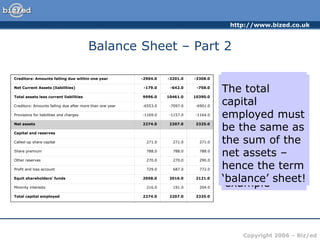

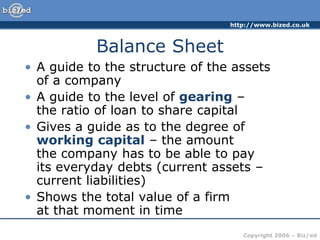

The document provides information about accounting concepts such as costs, revenue, profit, break even analysis, the profit and loss account, and the balance sheet. It defines different types of costs as fixed, variable, and semi-fixed costs. It explains how to calculate total costs, average costs, marginal costs, total revenue, and profit. It describes the purpose of financial accounts and what a profit and loss account and balance sheet show. The profit and loss account shows the flow of sales and costs over a period to determine profit or loss. The balance sheet provides a snapshot of a company's assets, liabilities, and capital at a point in time.