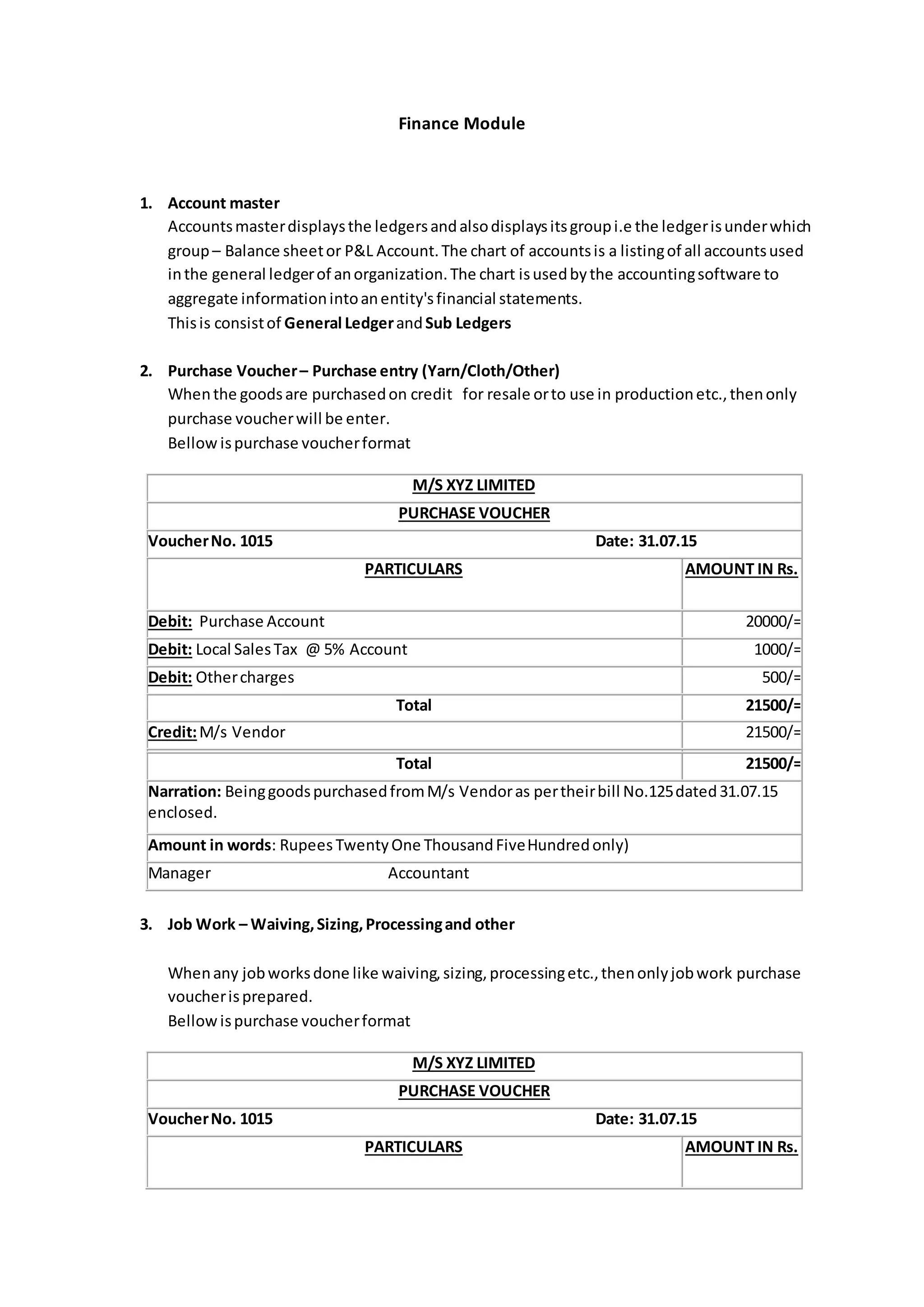

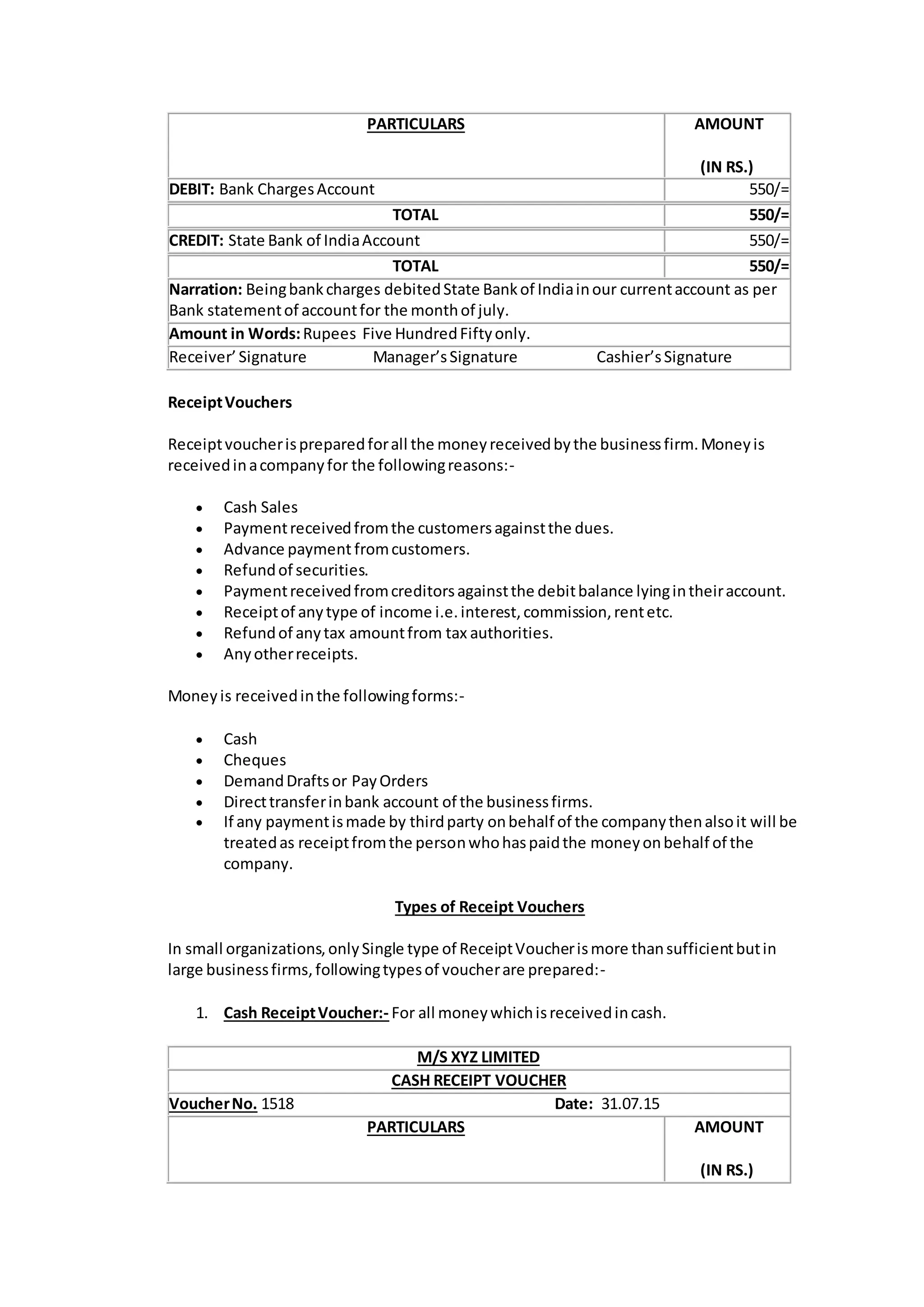

The document outlines the various accounting modules used to record financial transactions, including accounts payable and receivable, purchase and sales entries, payroll processing, payment and receipt vouchers, journal entries, and reports such as trial balances, balance sheets, registers and notes. Standard formats are provided for vouchers, journals, and reports to record and track the financial activities and position of a business in a systematic manner according to accounting principles. The modules help automate and streamline the accounting process for organizations.