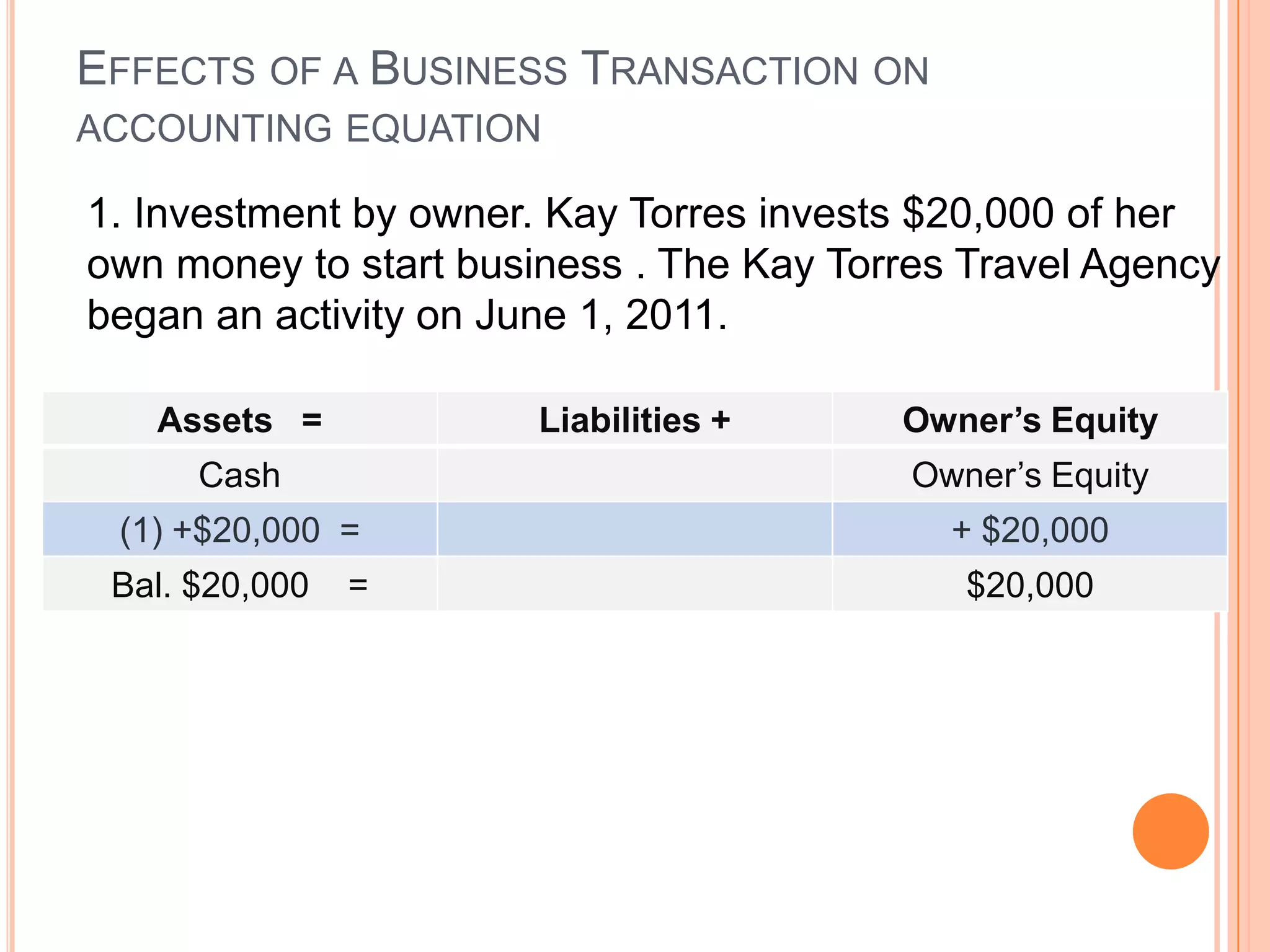

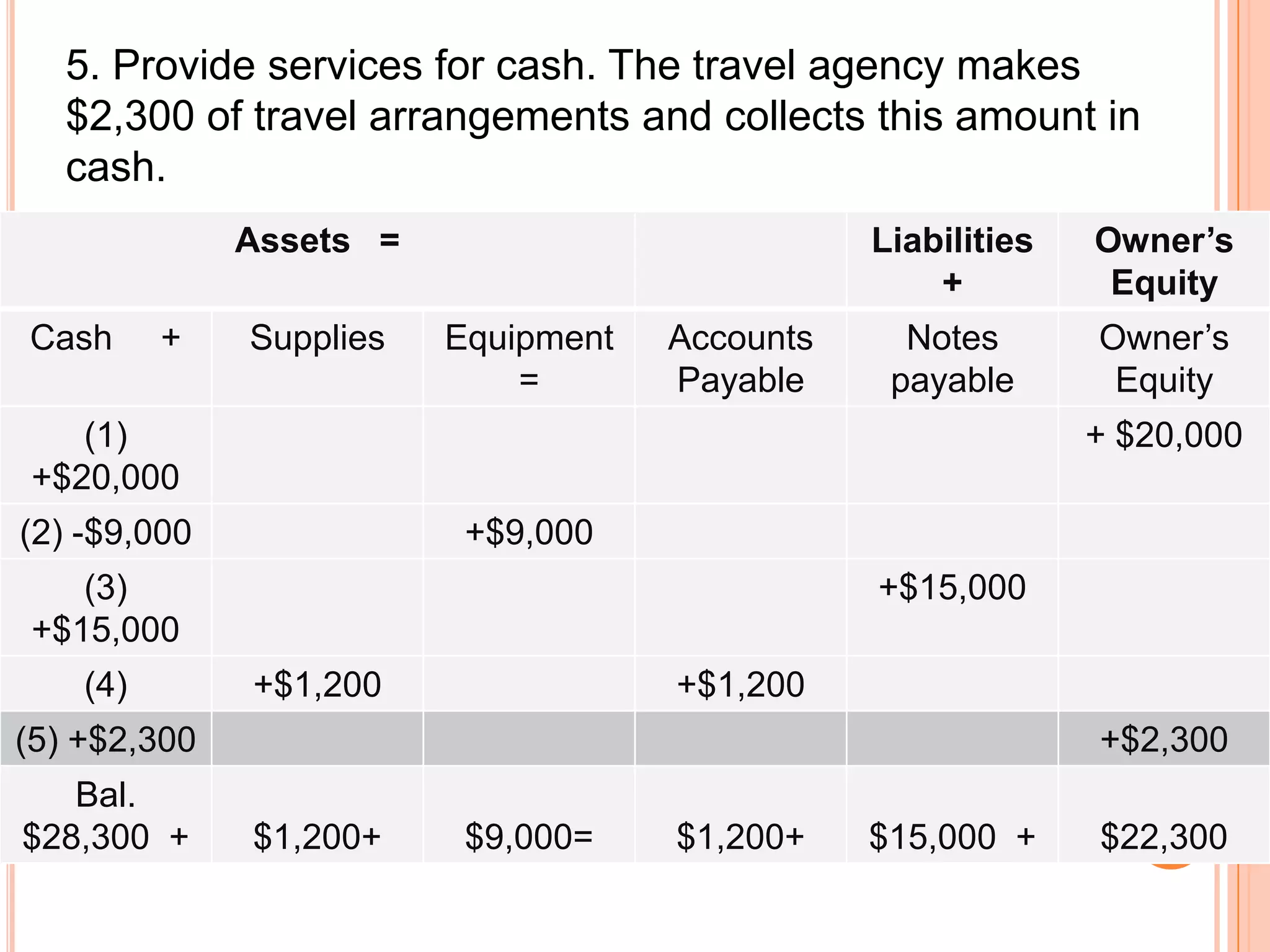

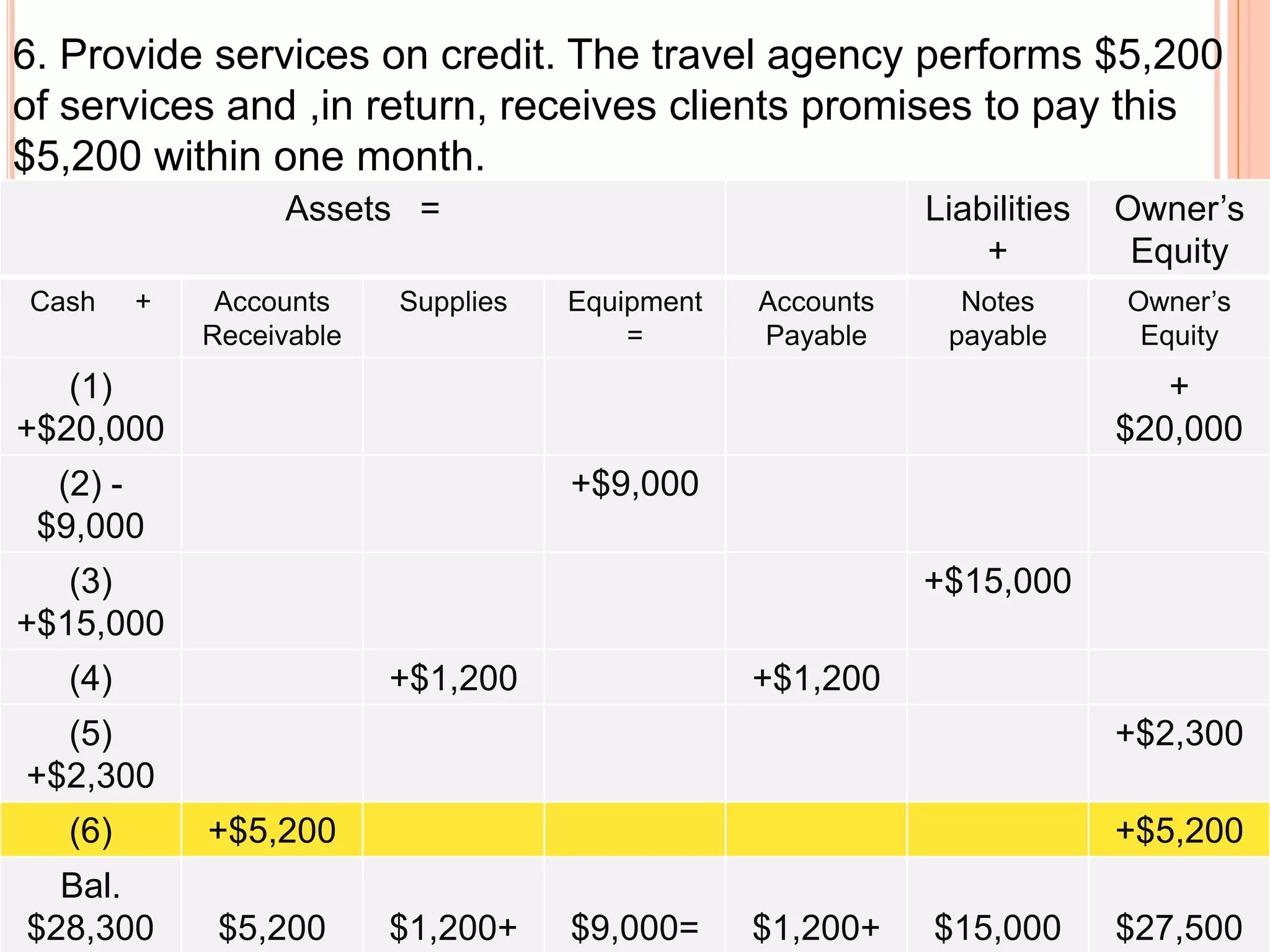

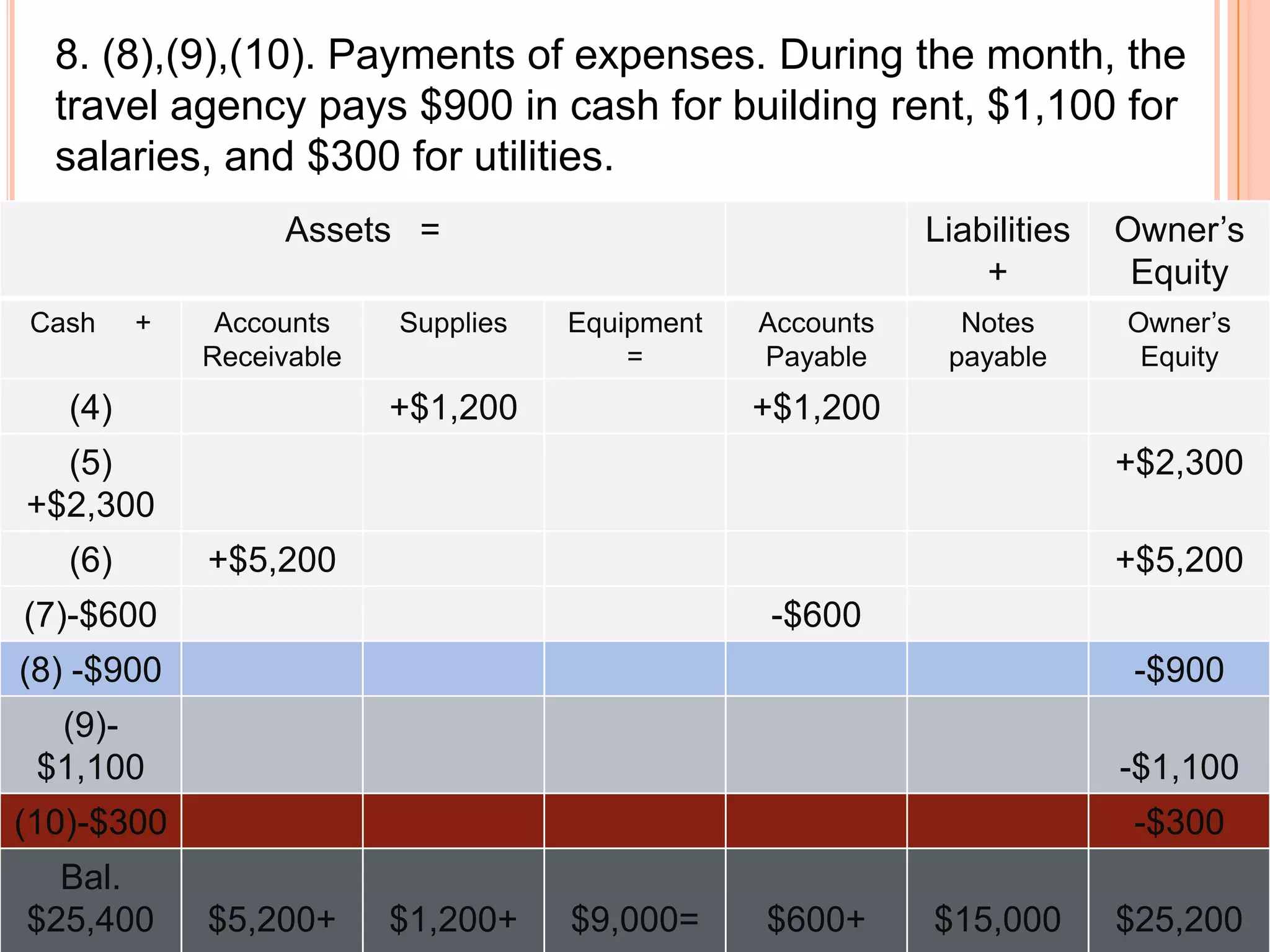

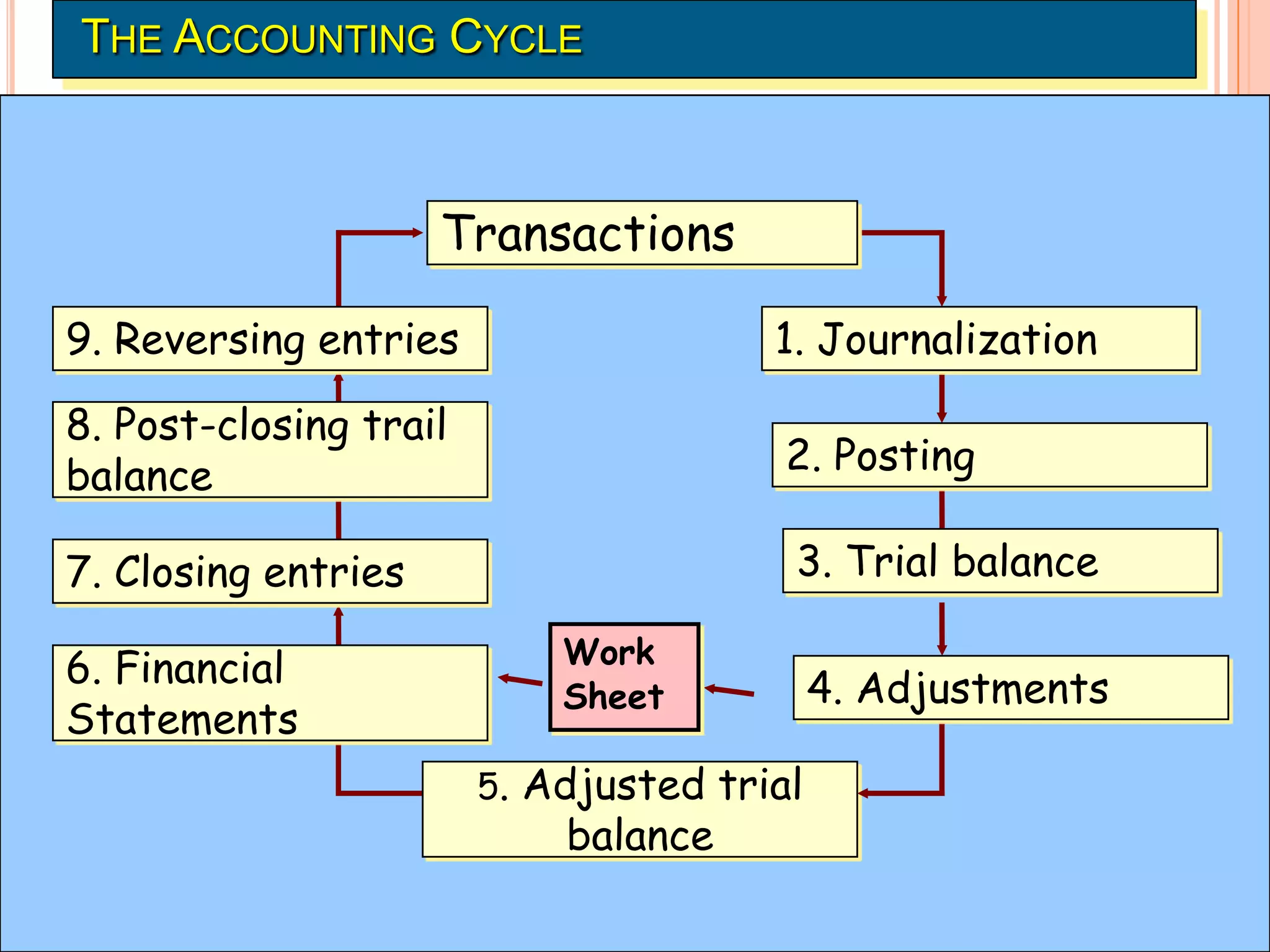

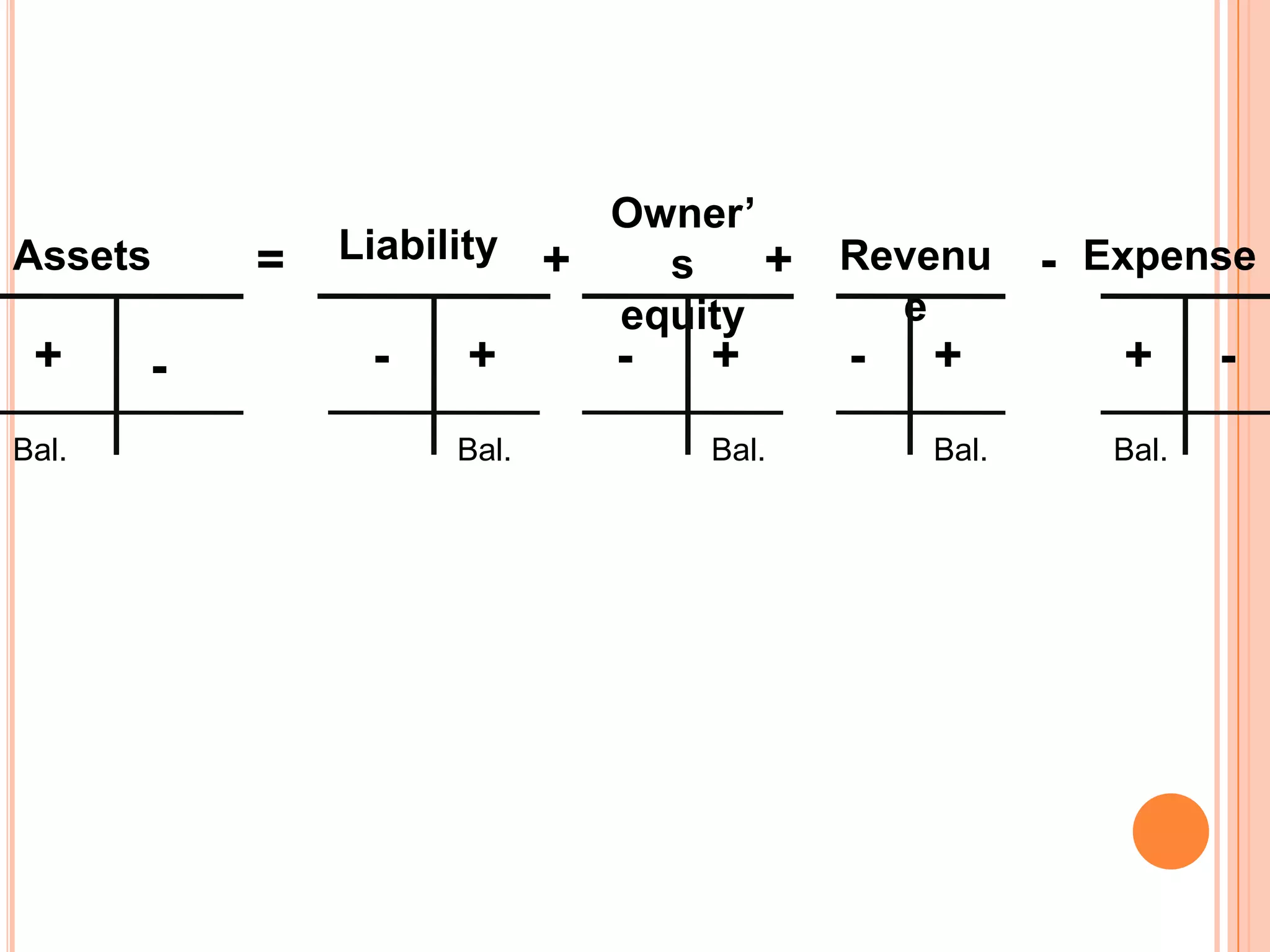

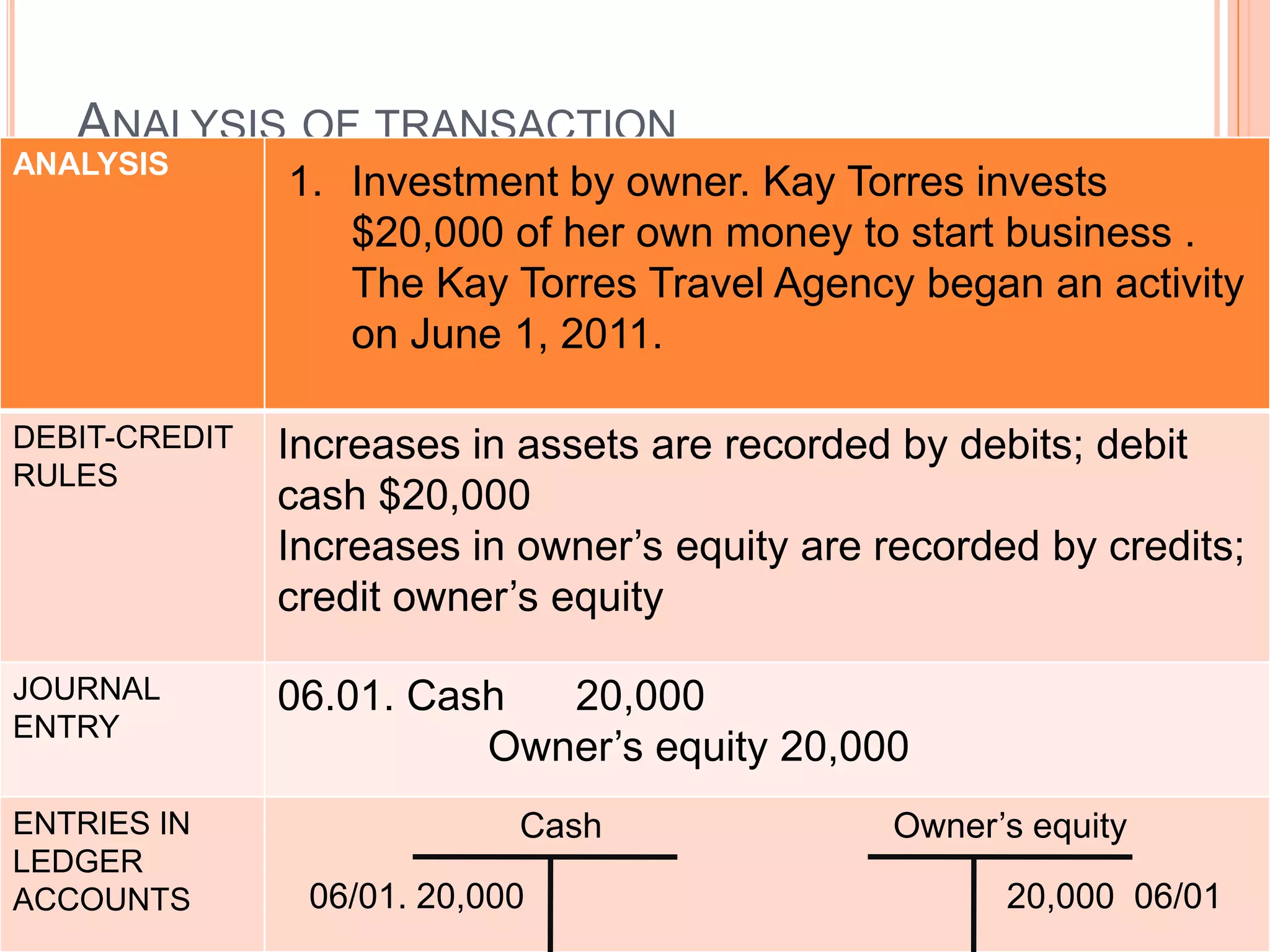

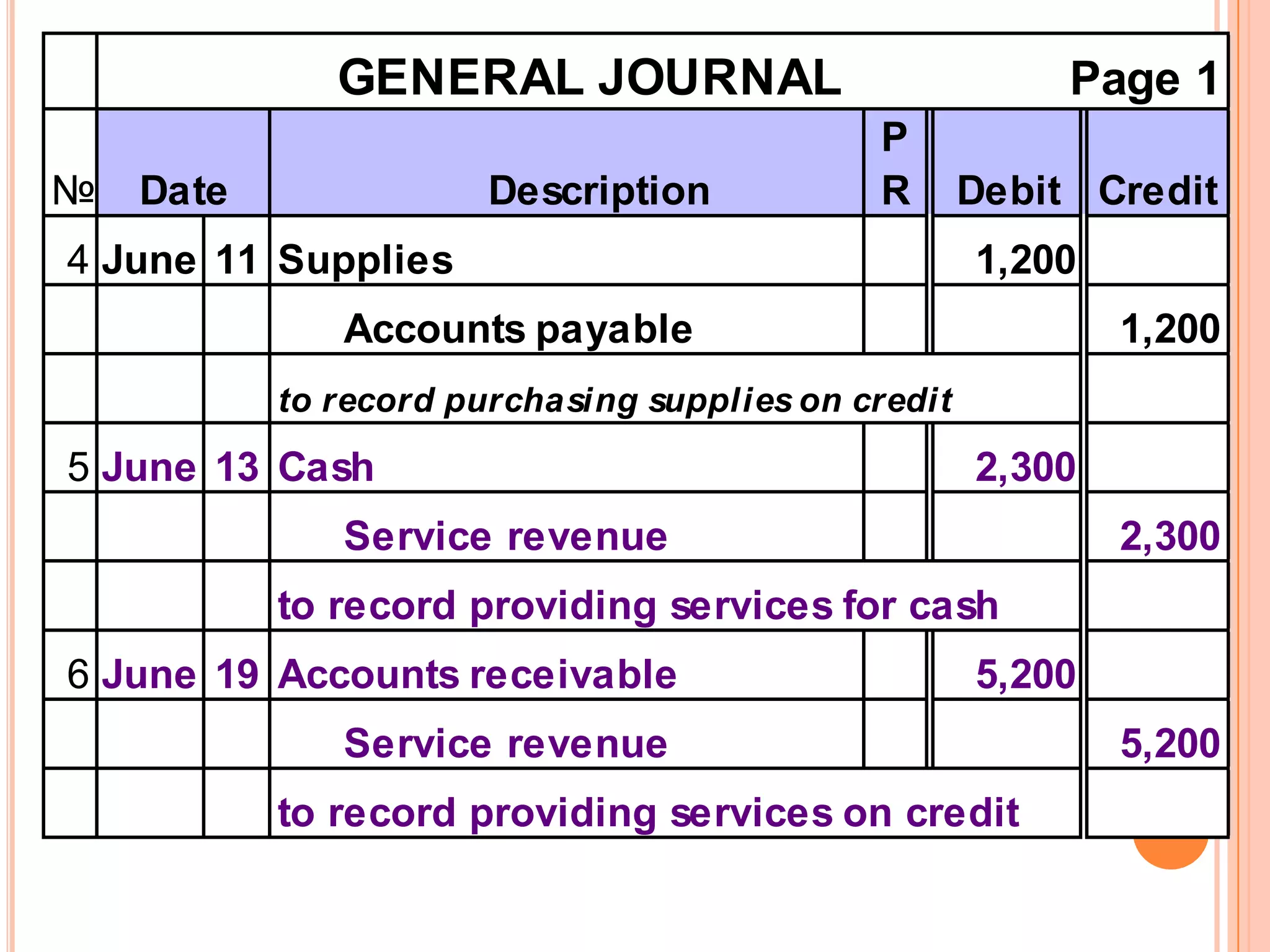

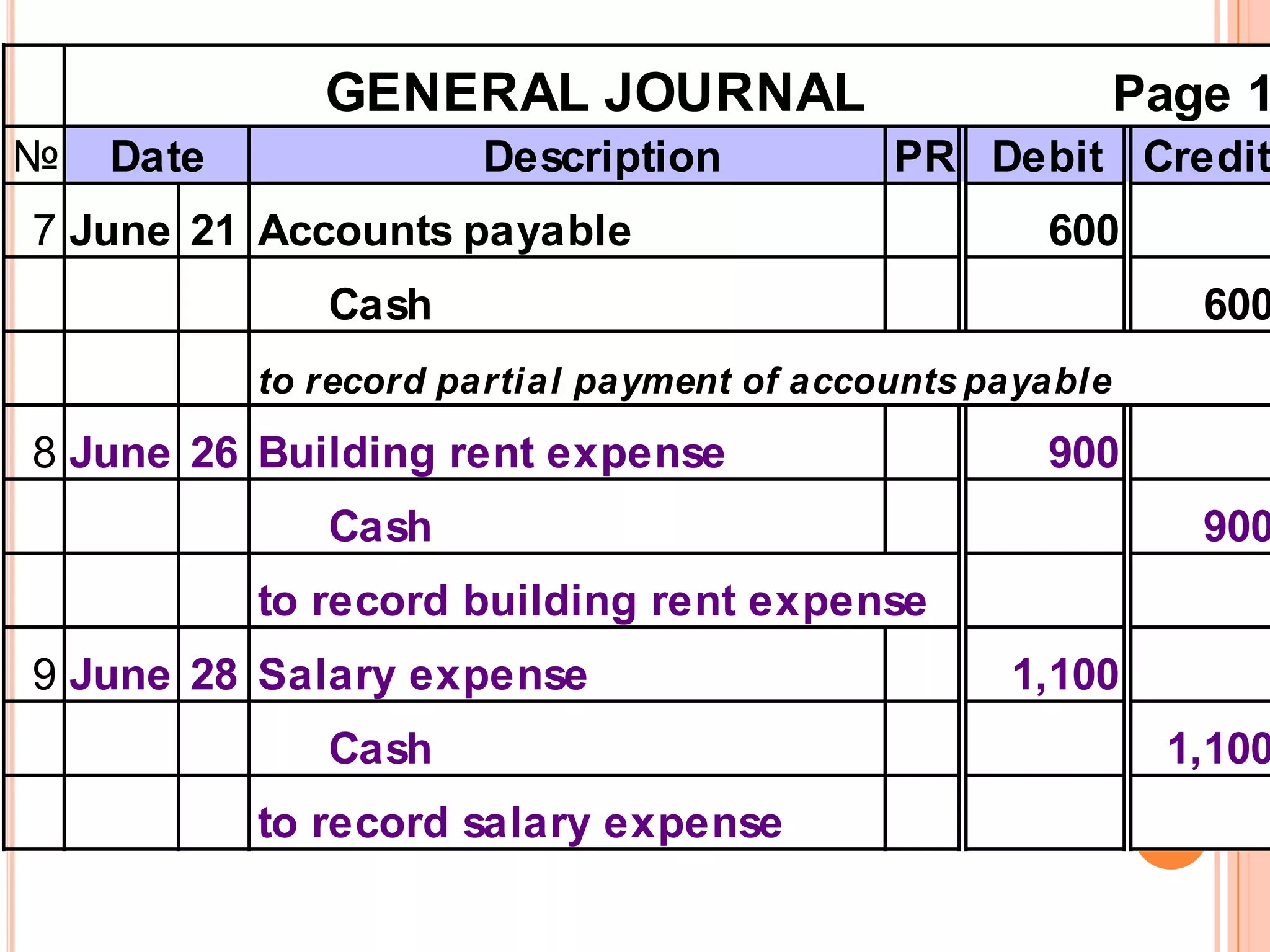

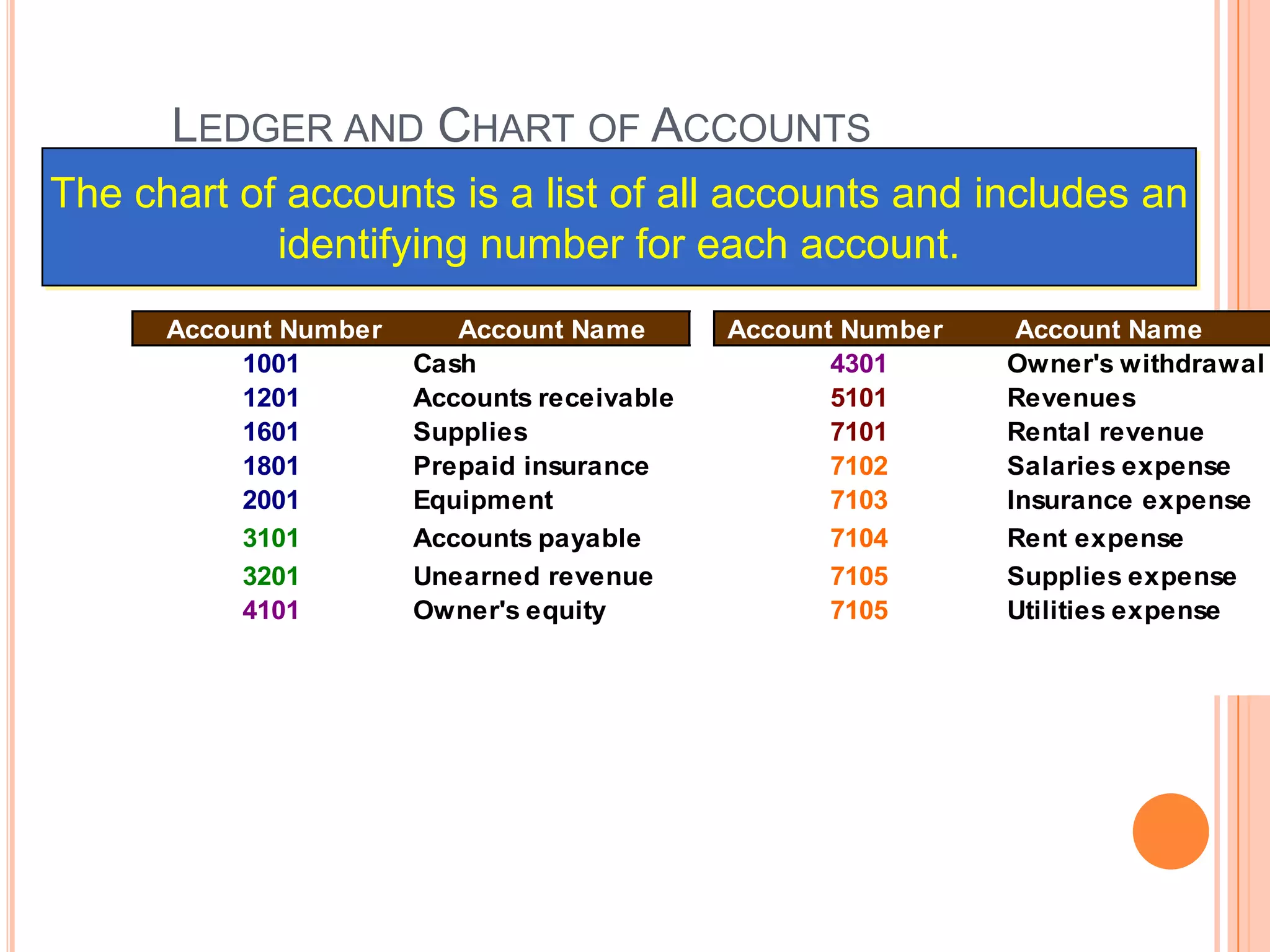

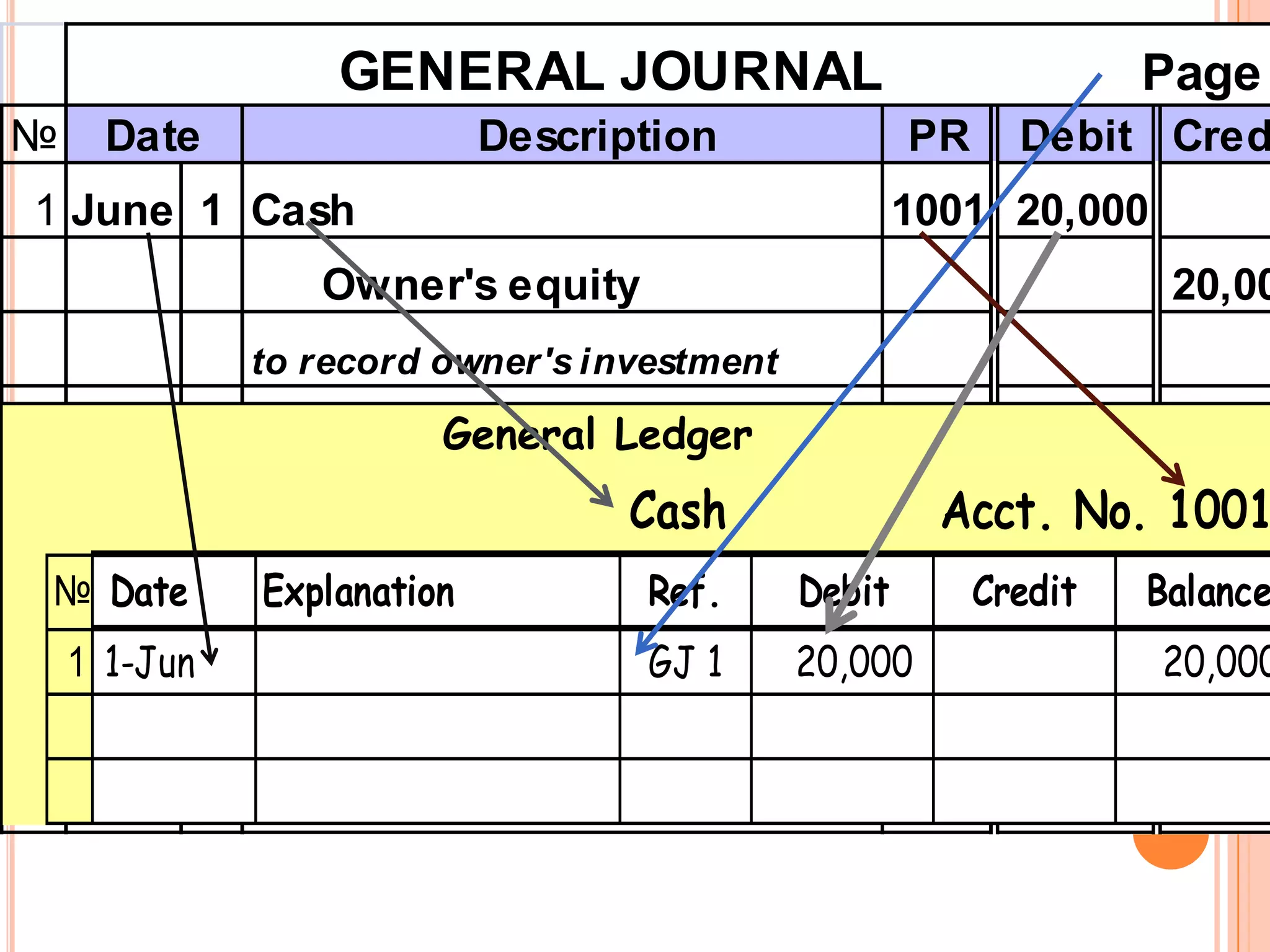

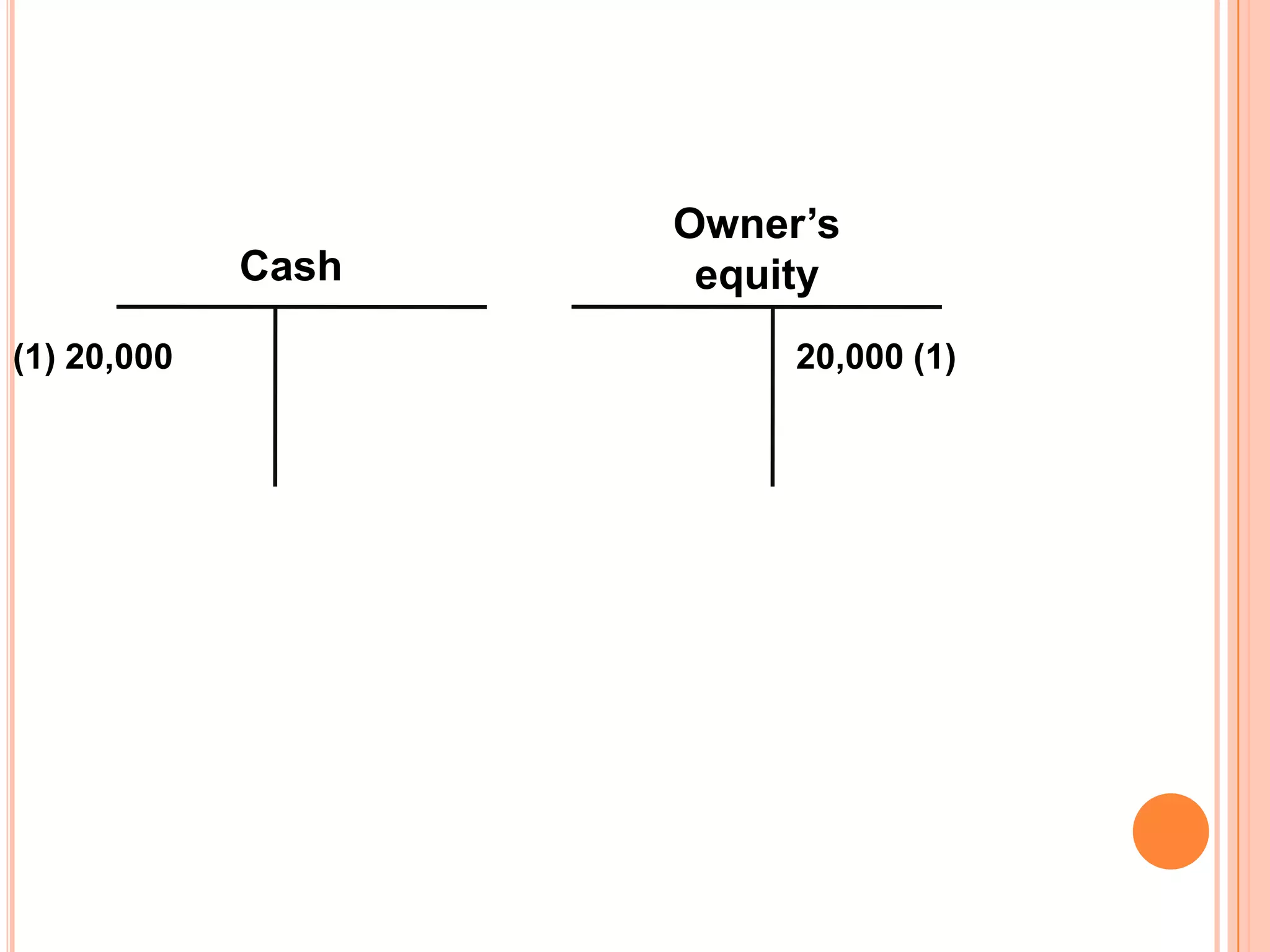

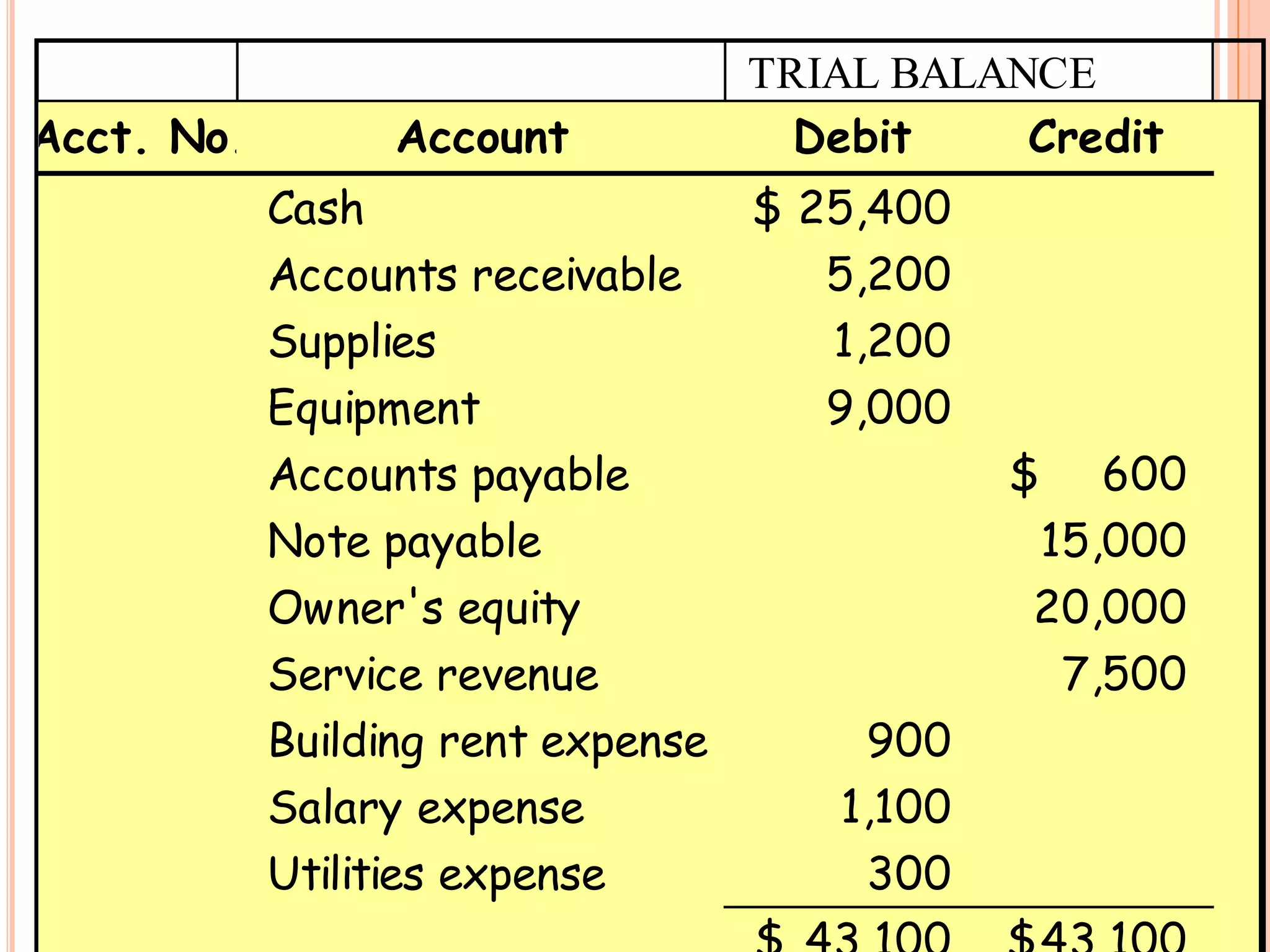

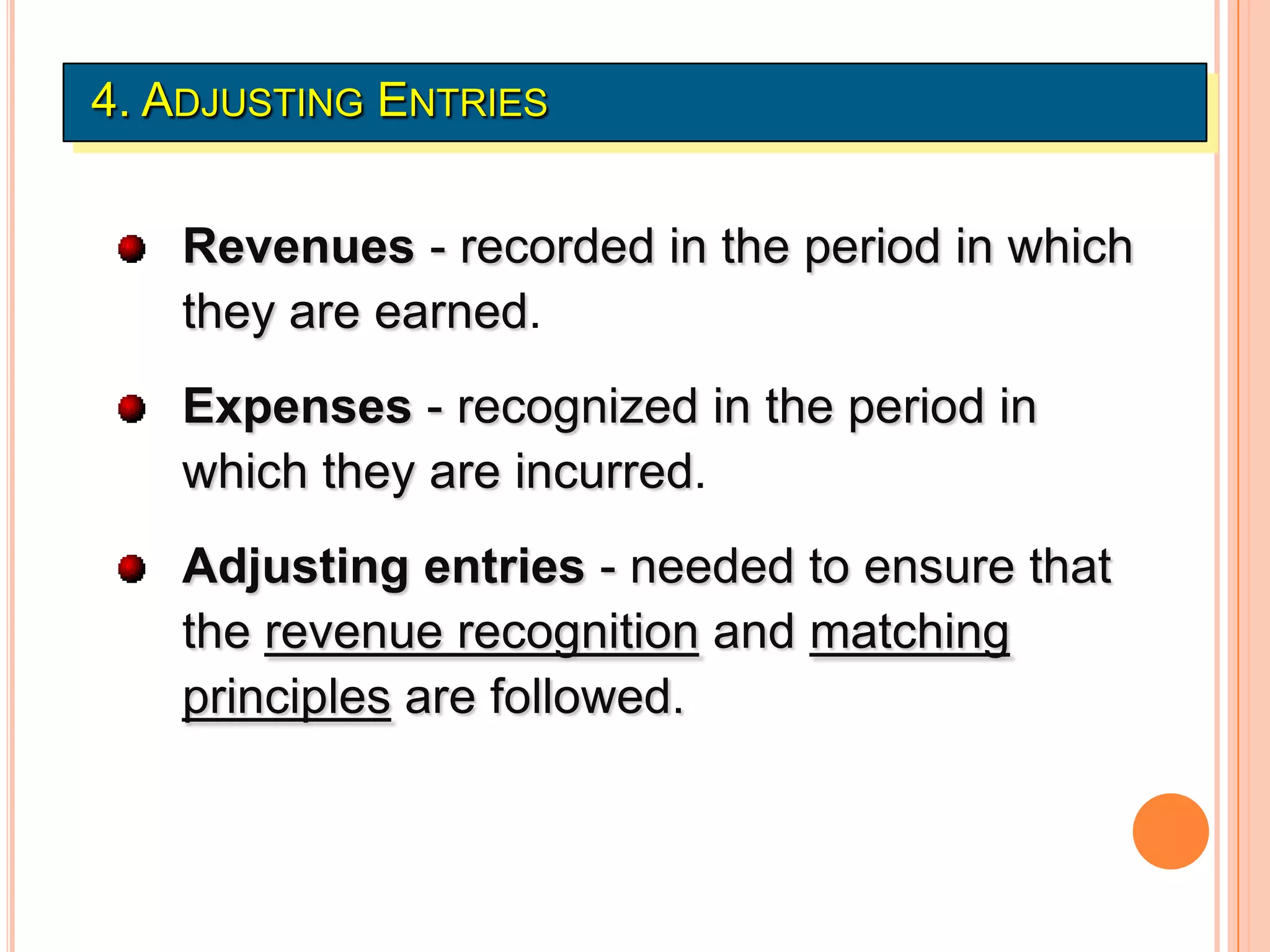

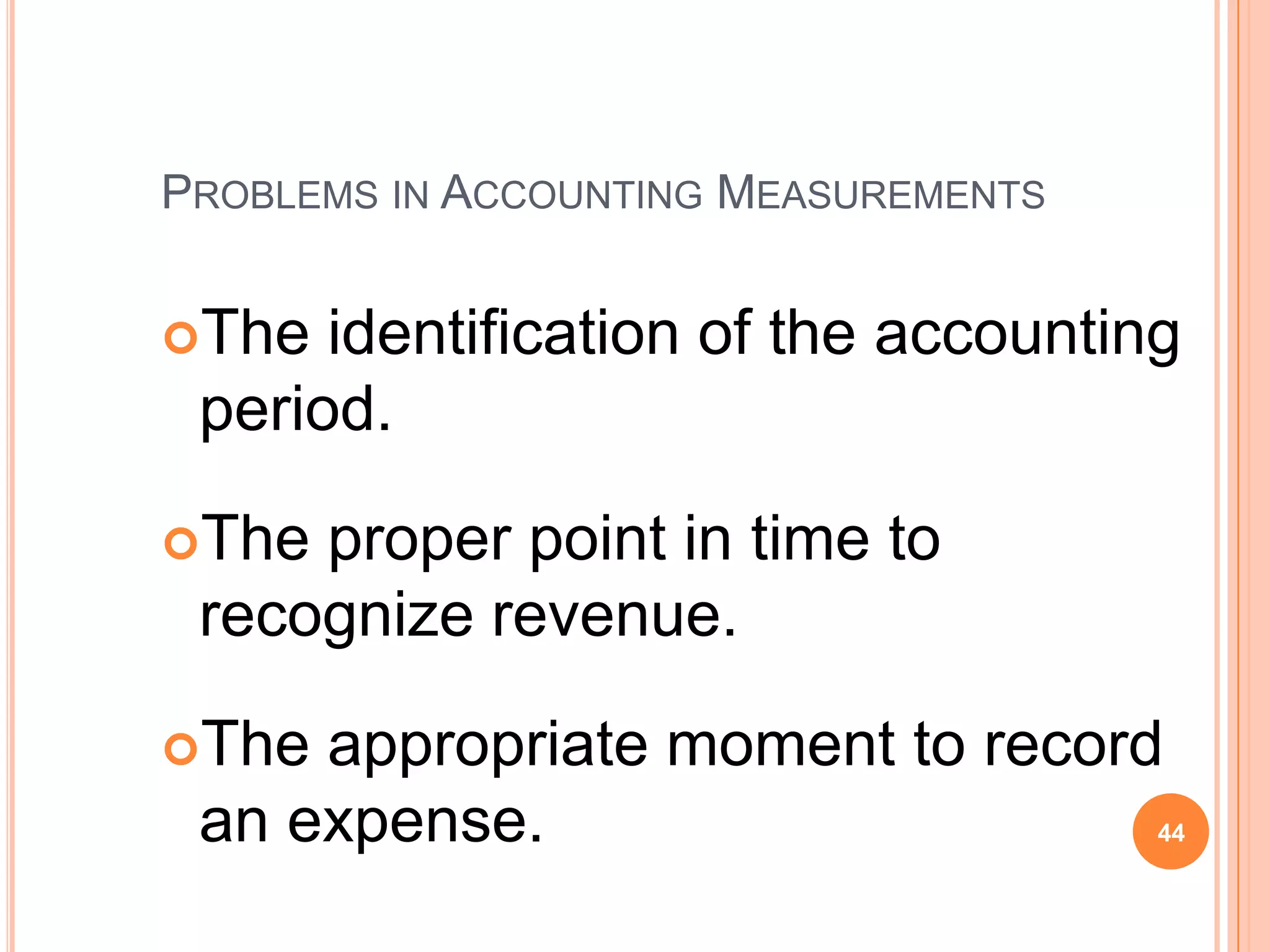

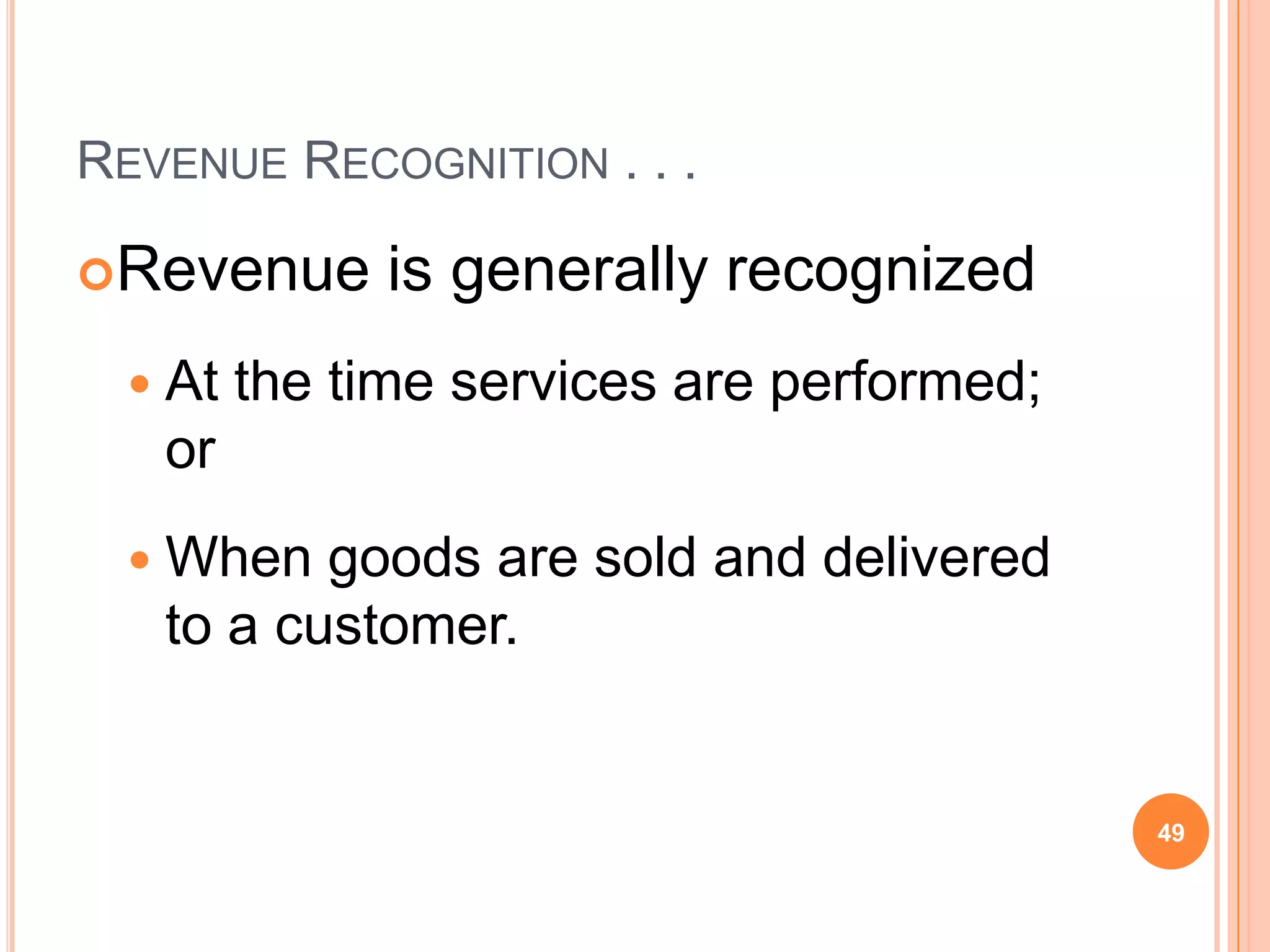

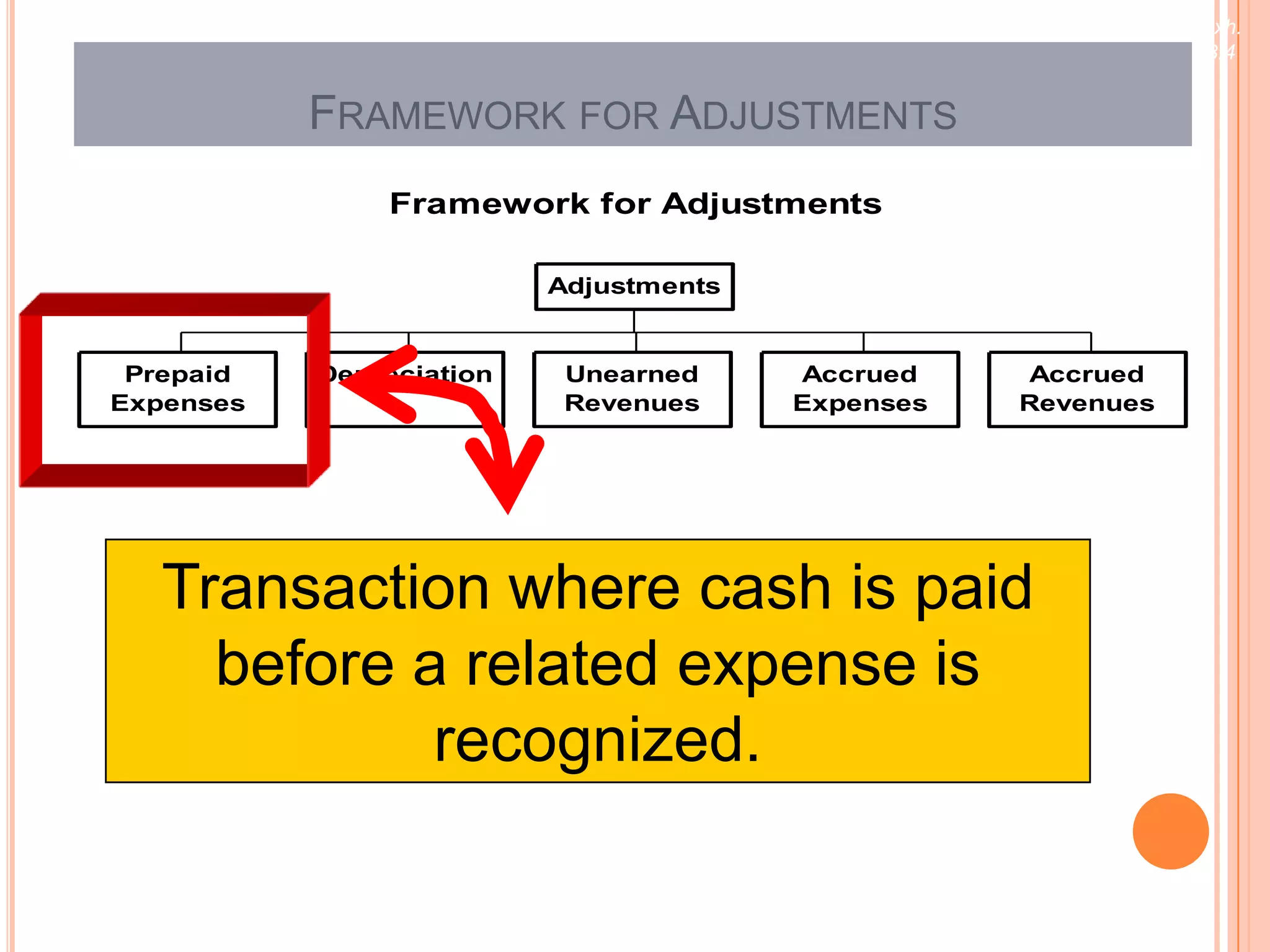

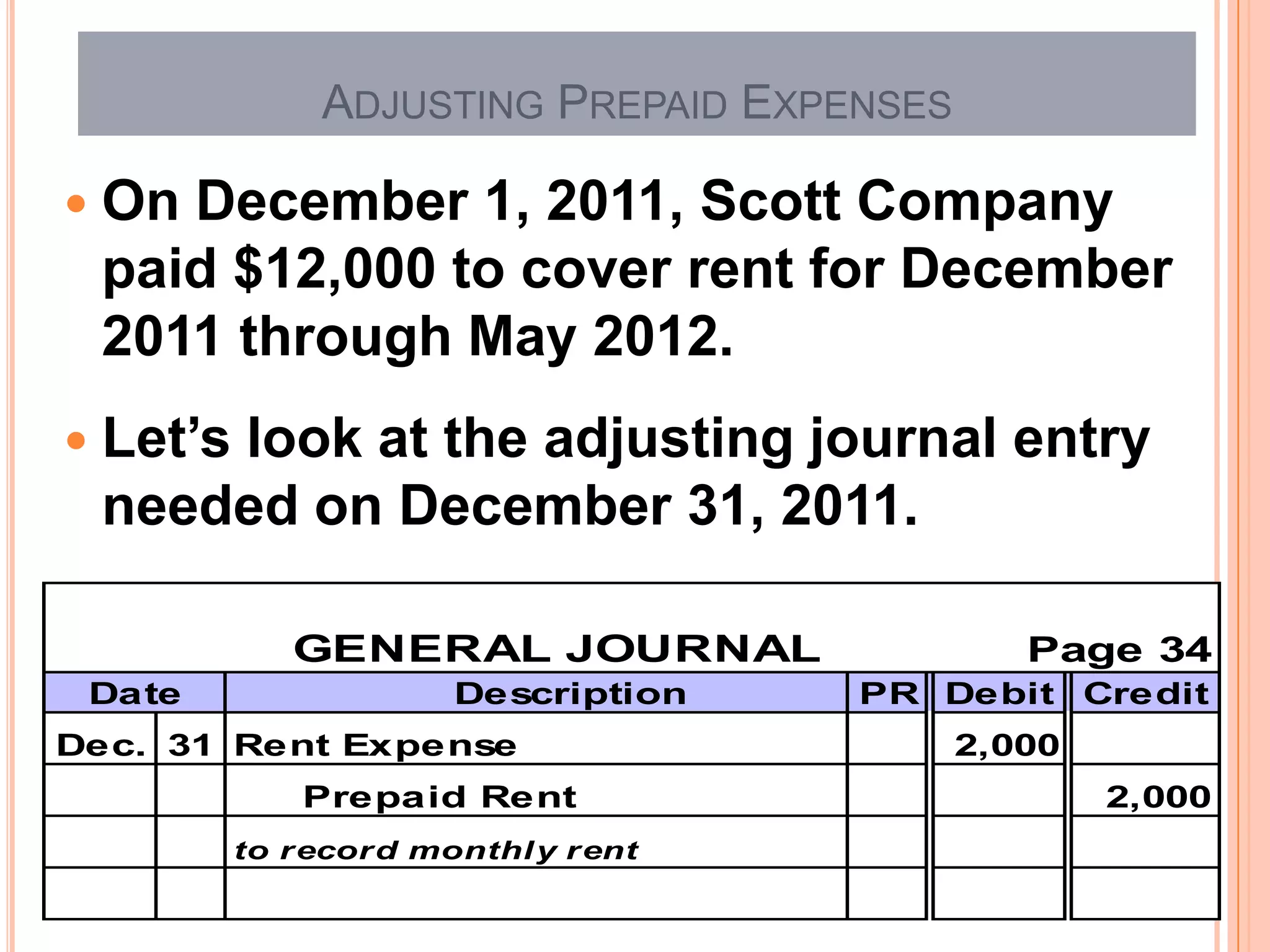

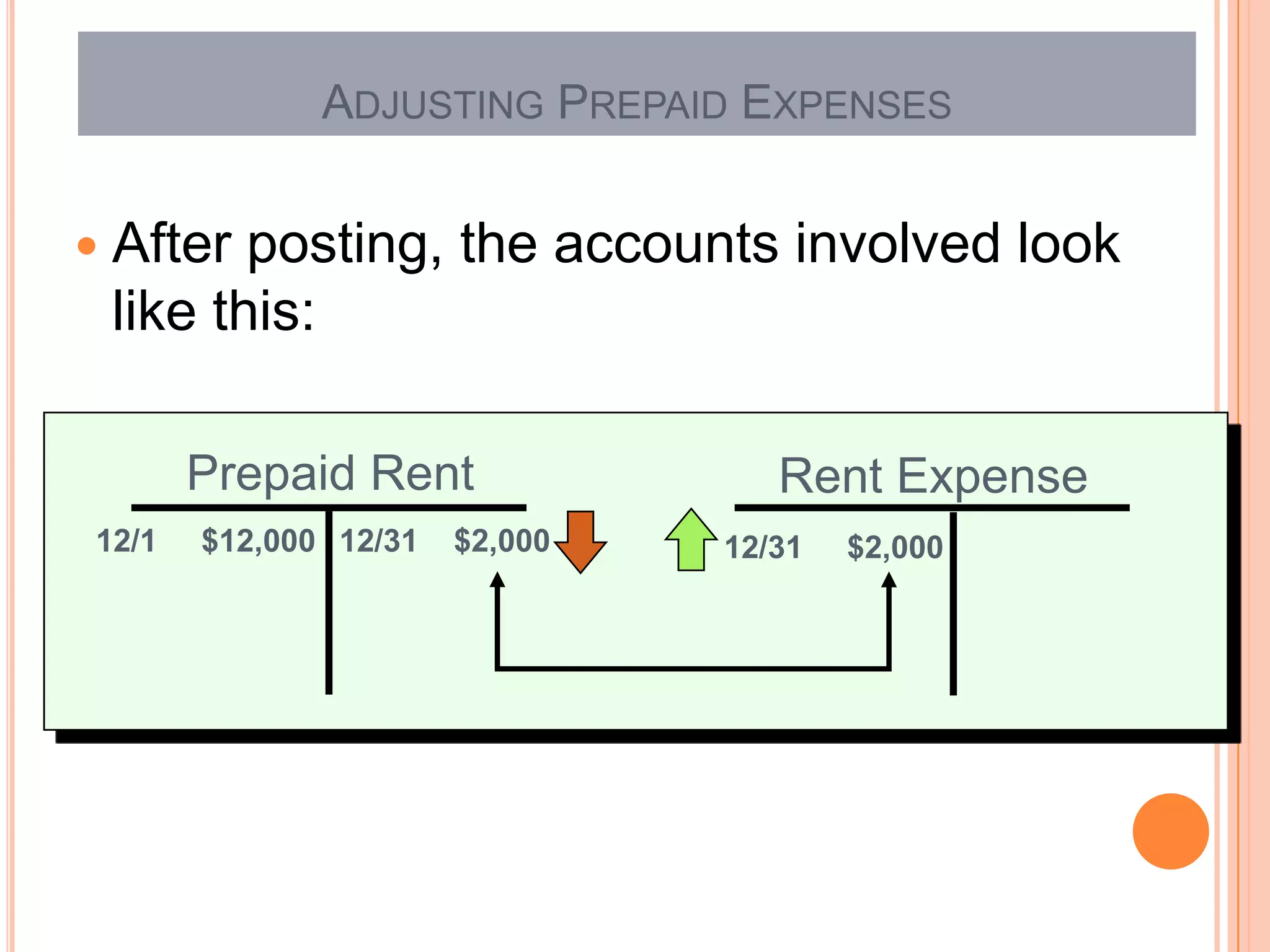

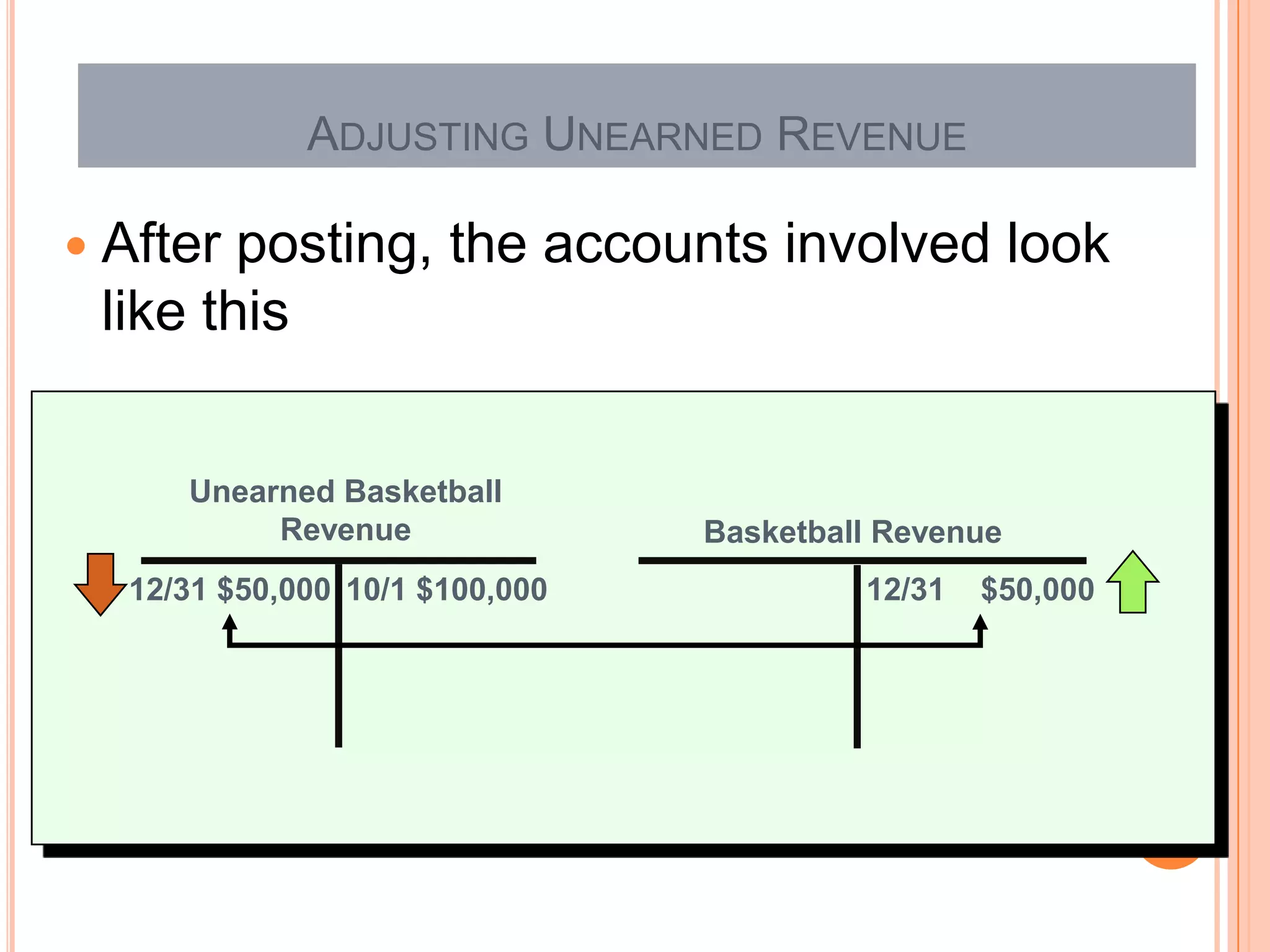

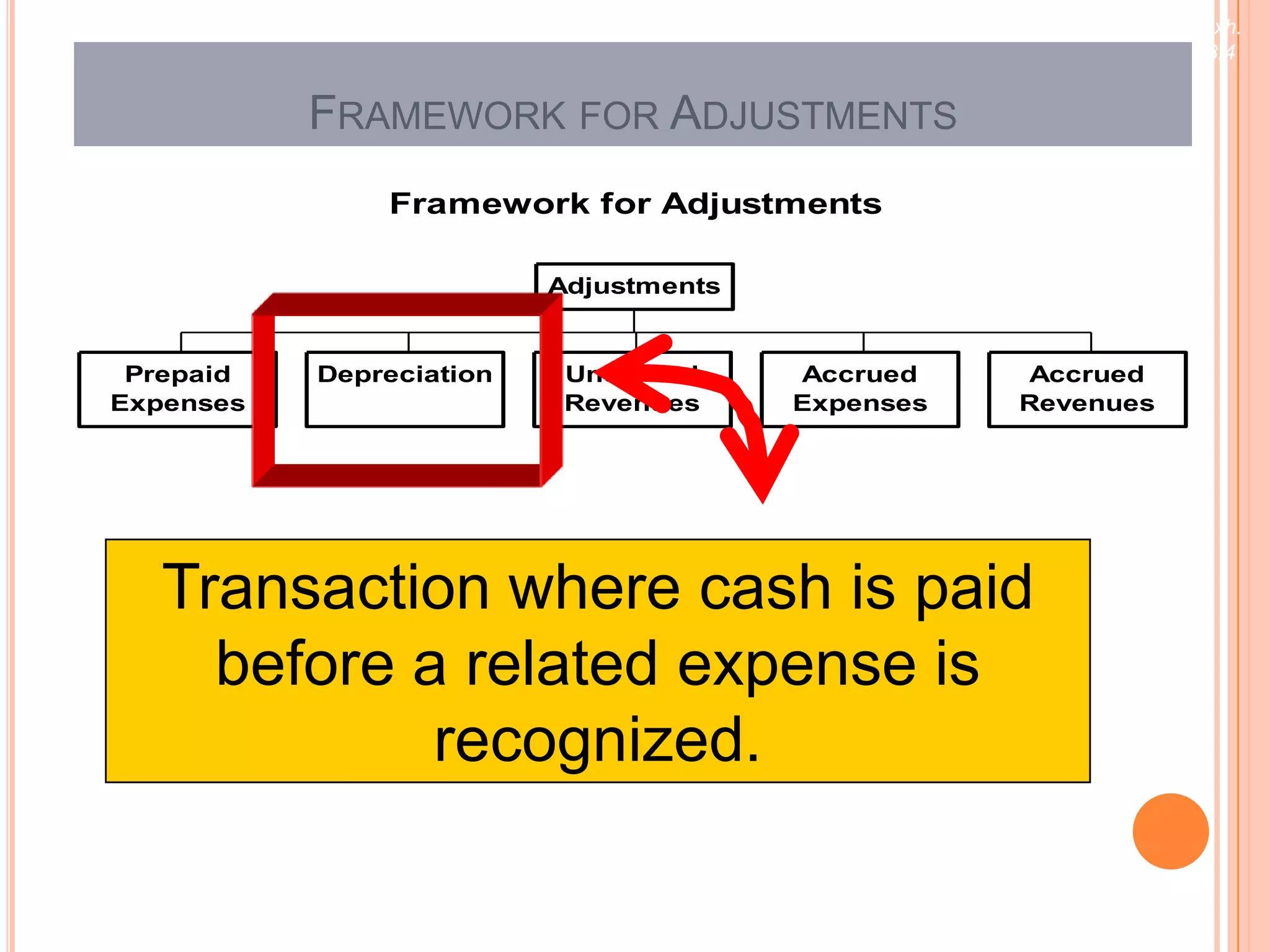

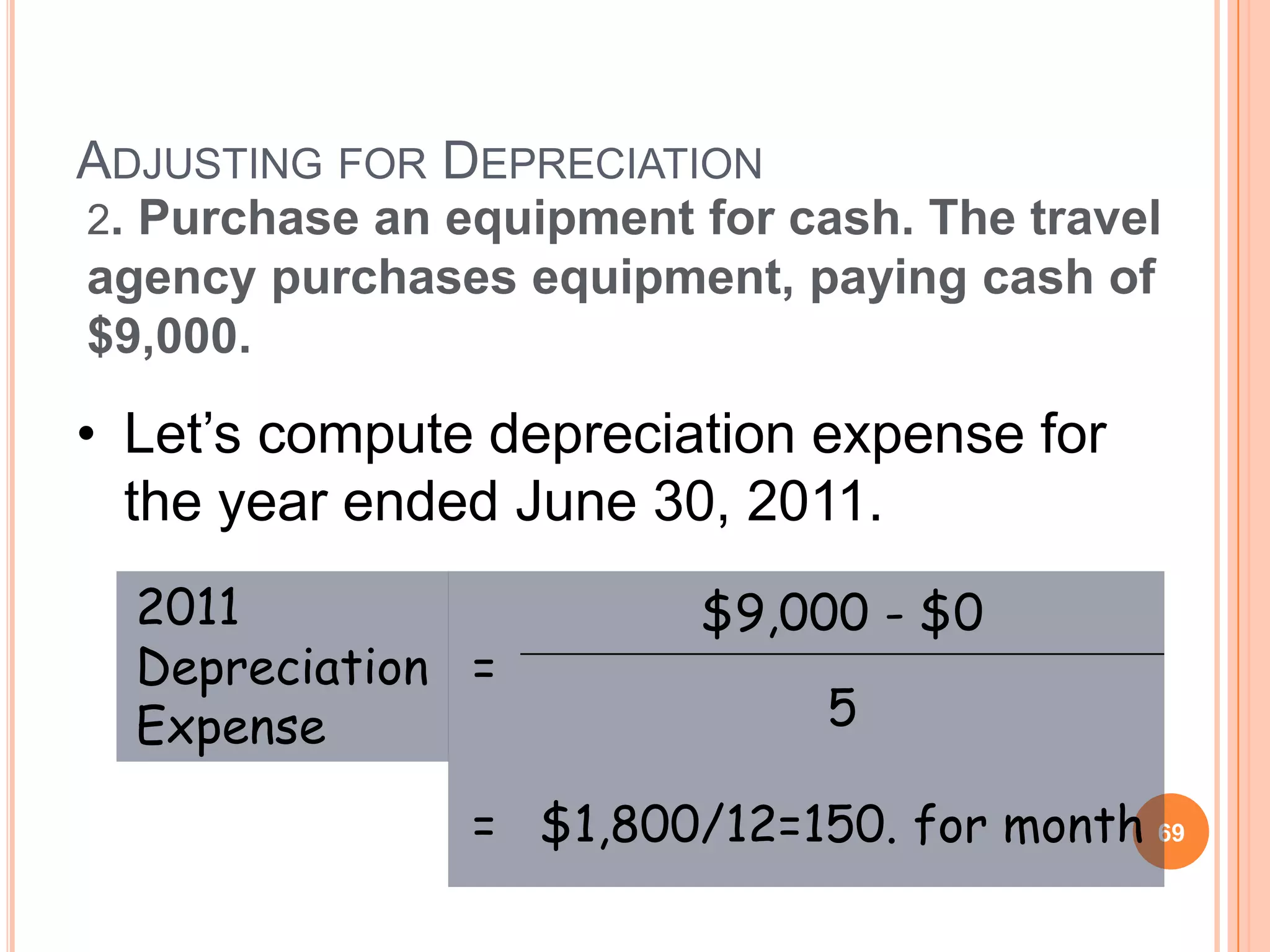

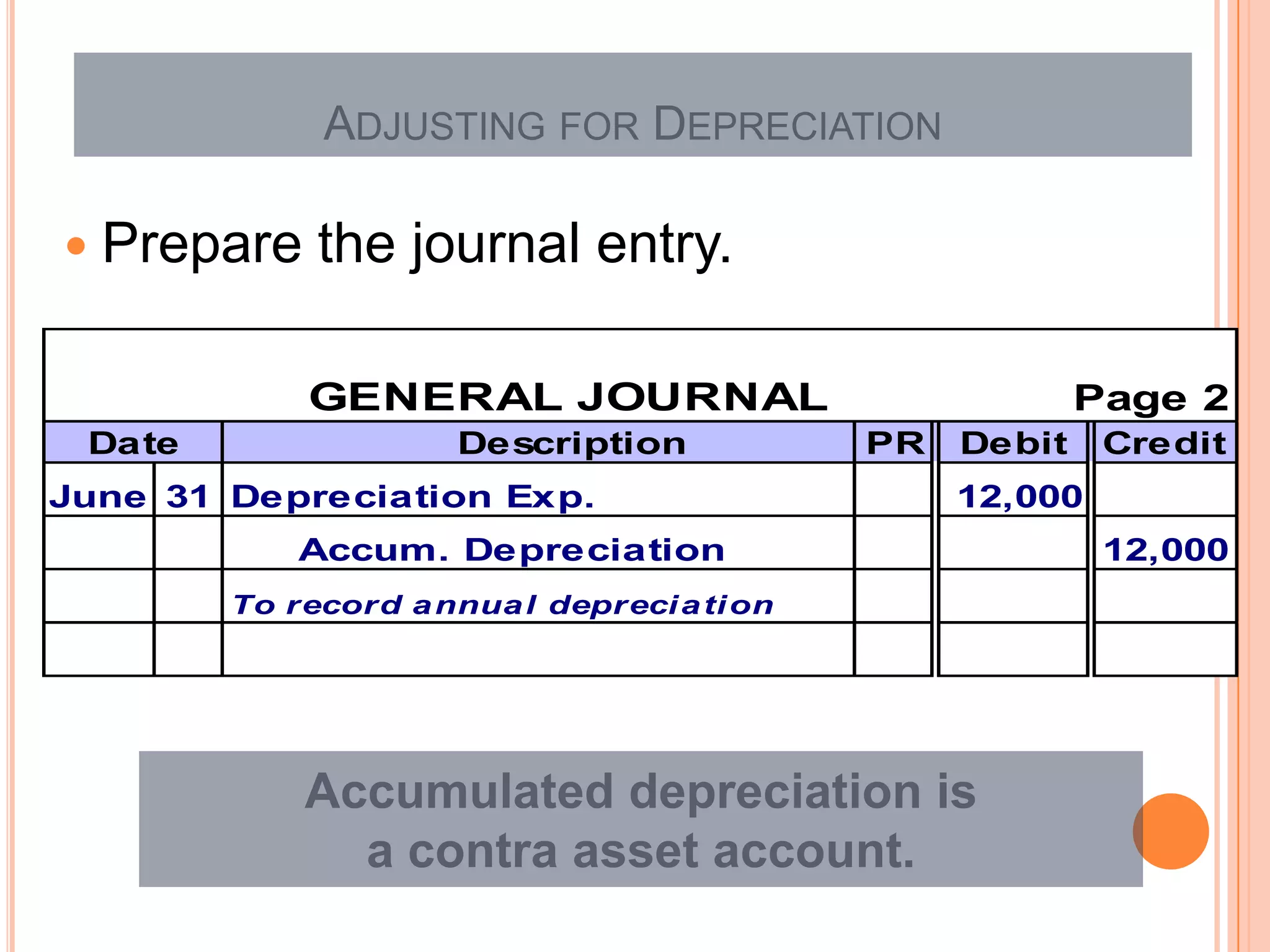

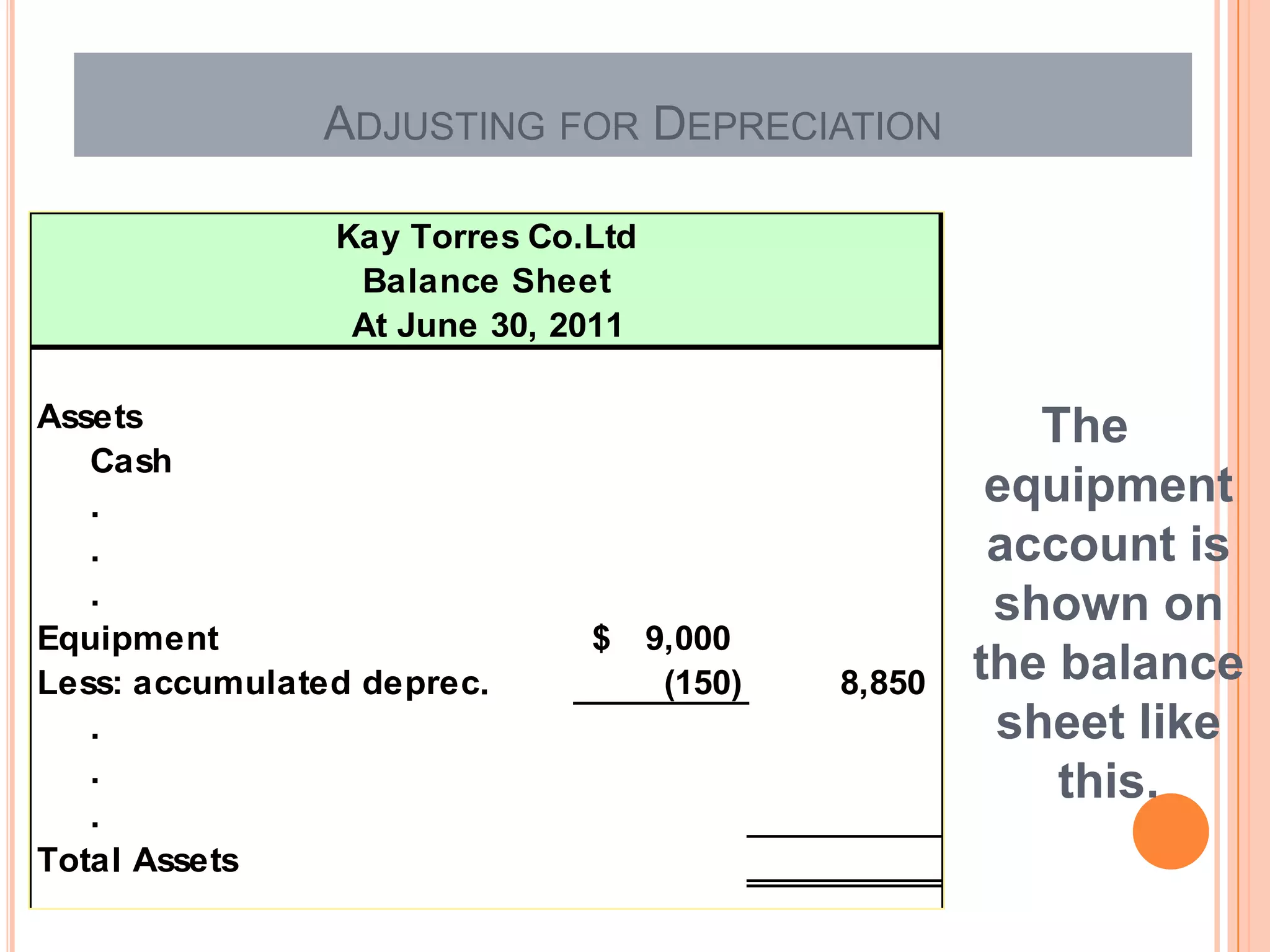

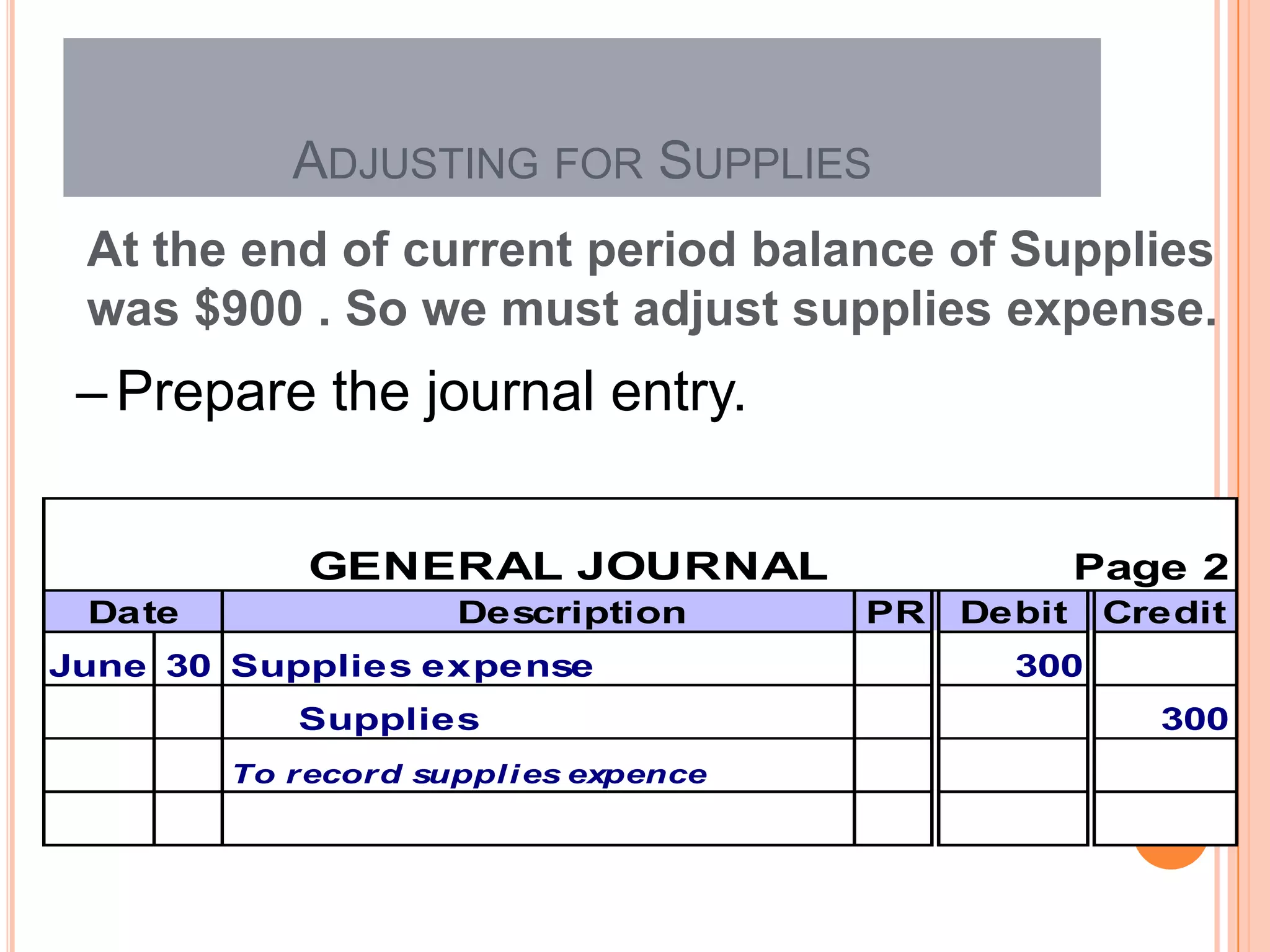

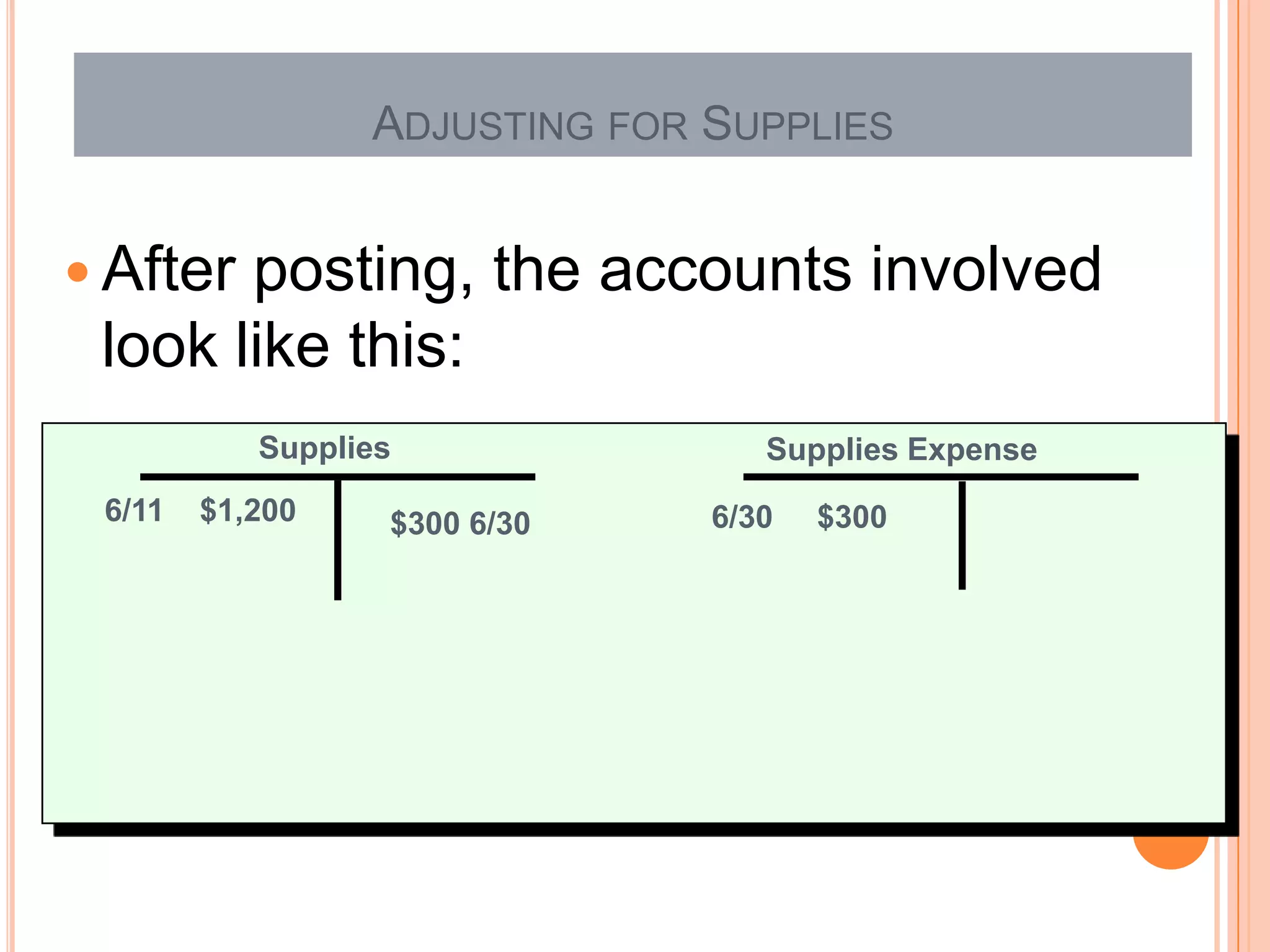

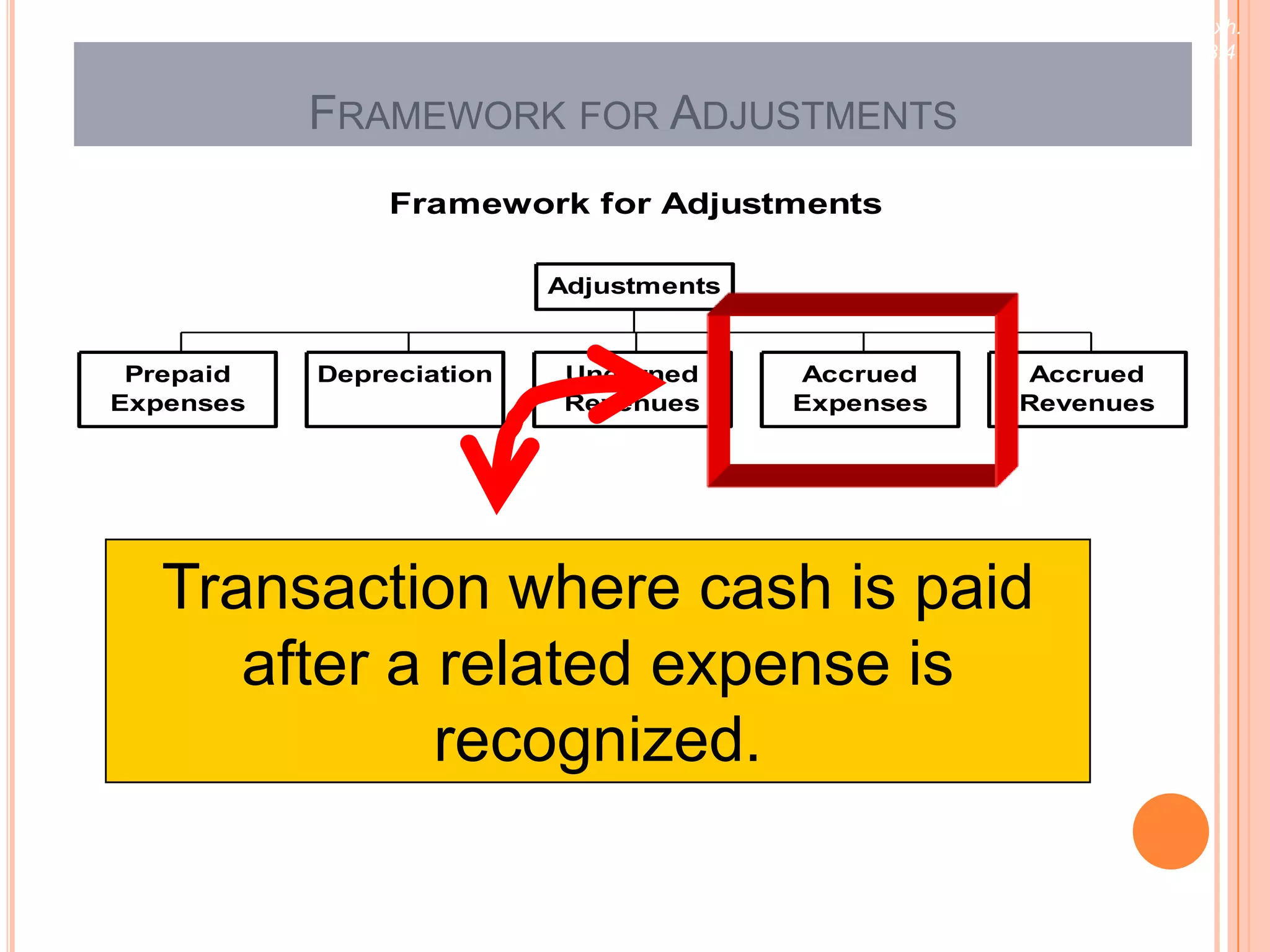

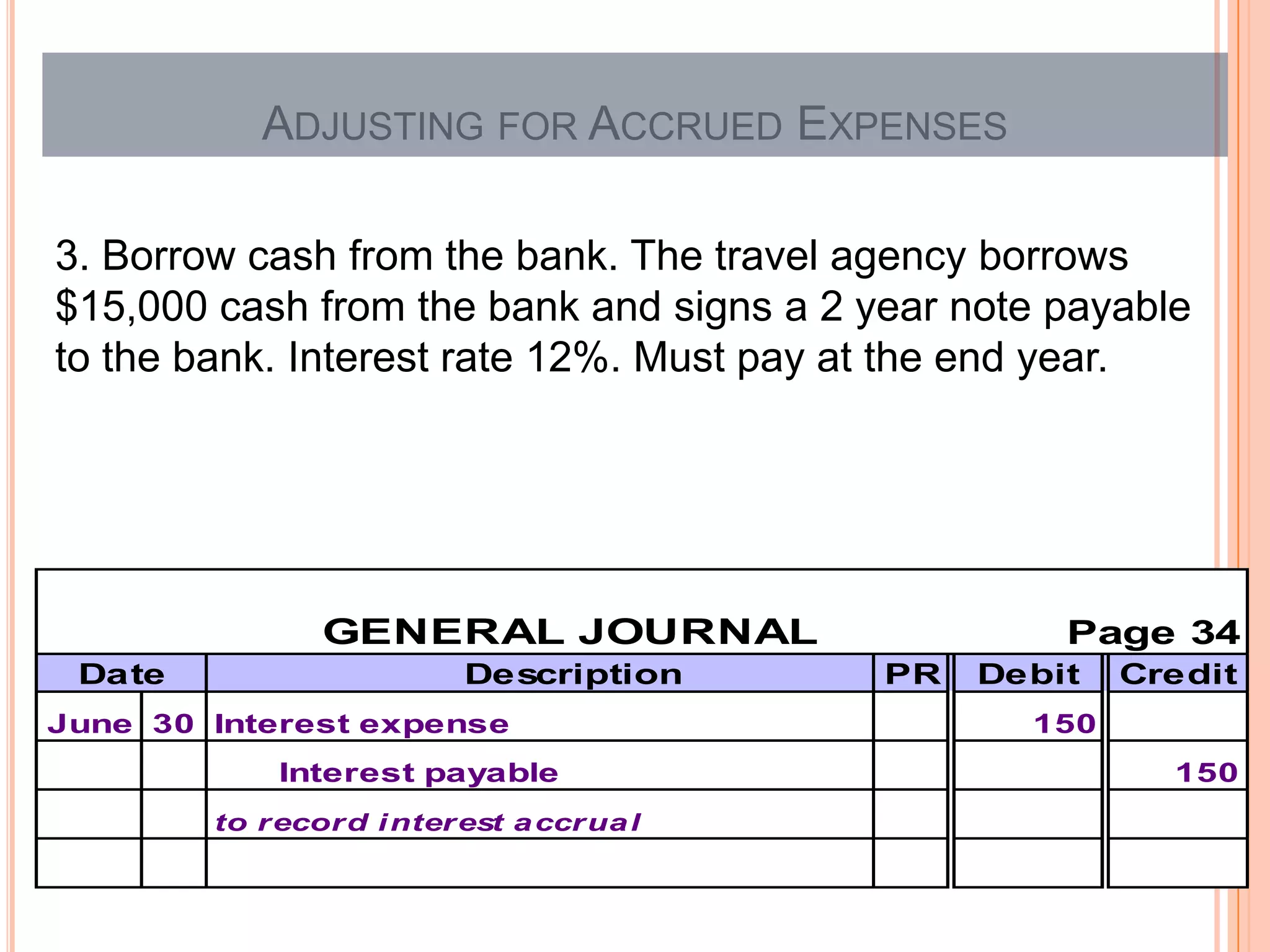

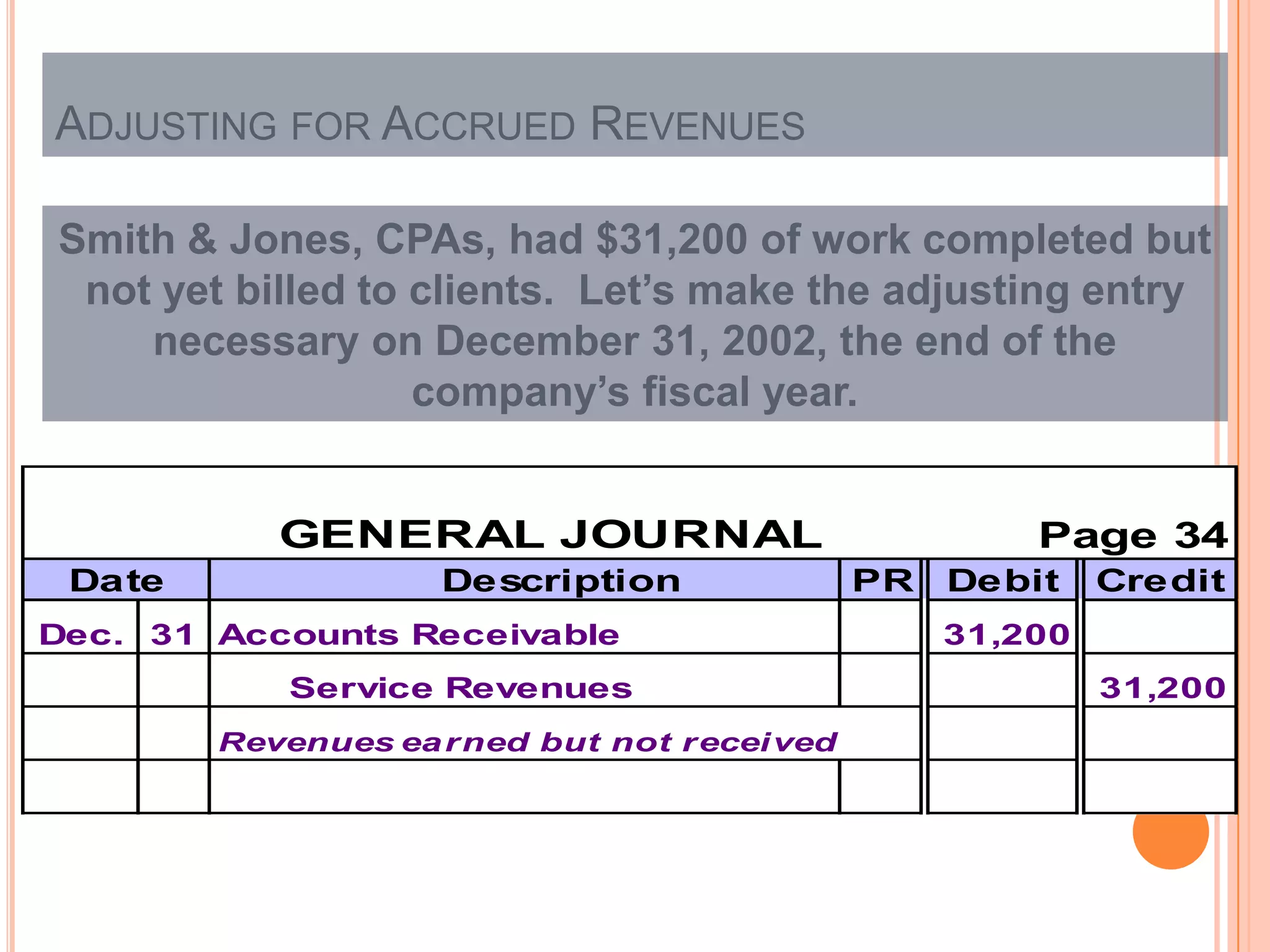

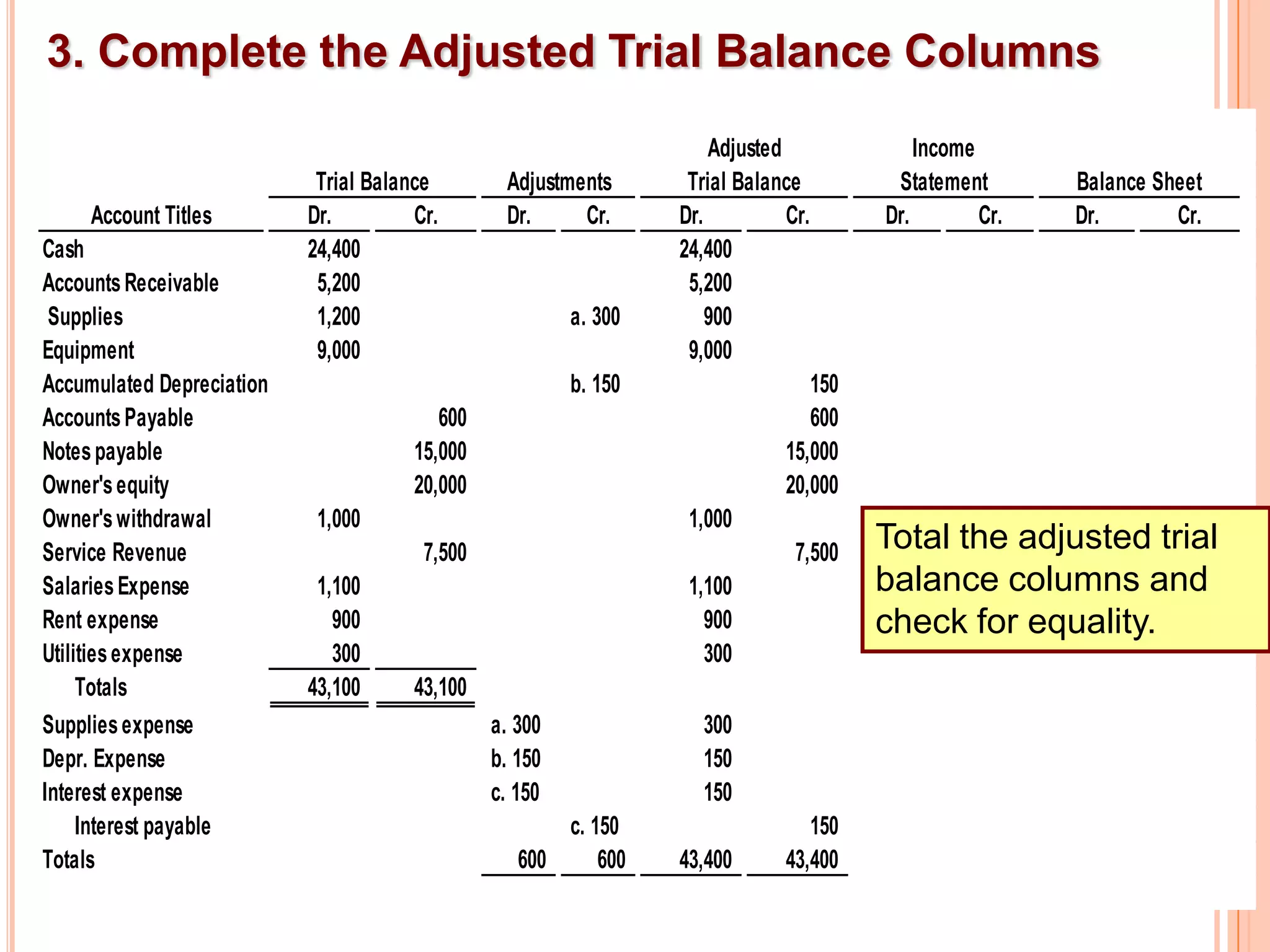

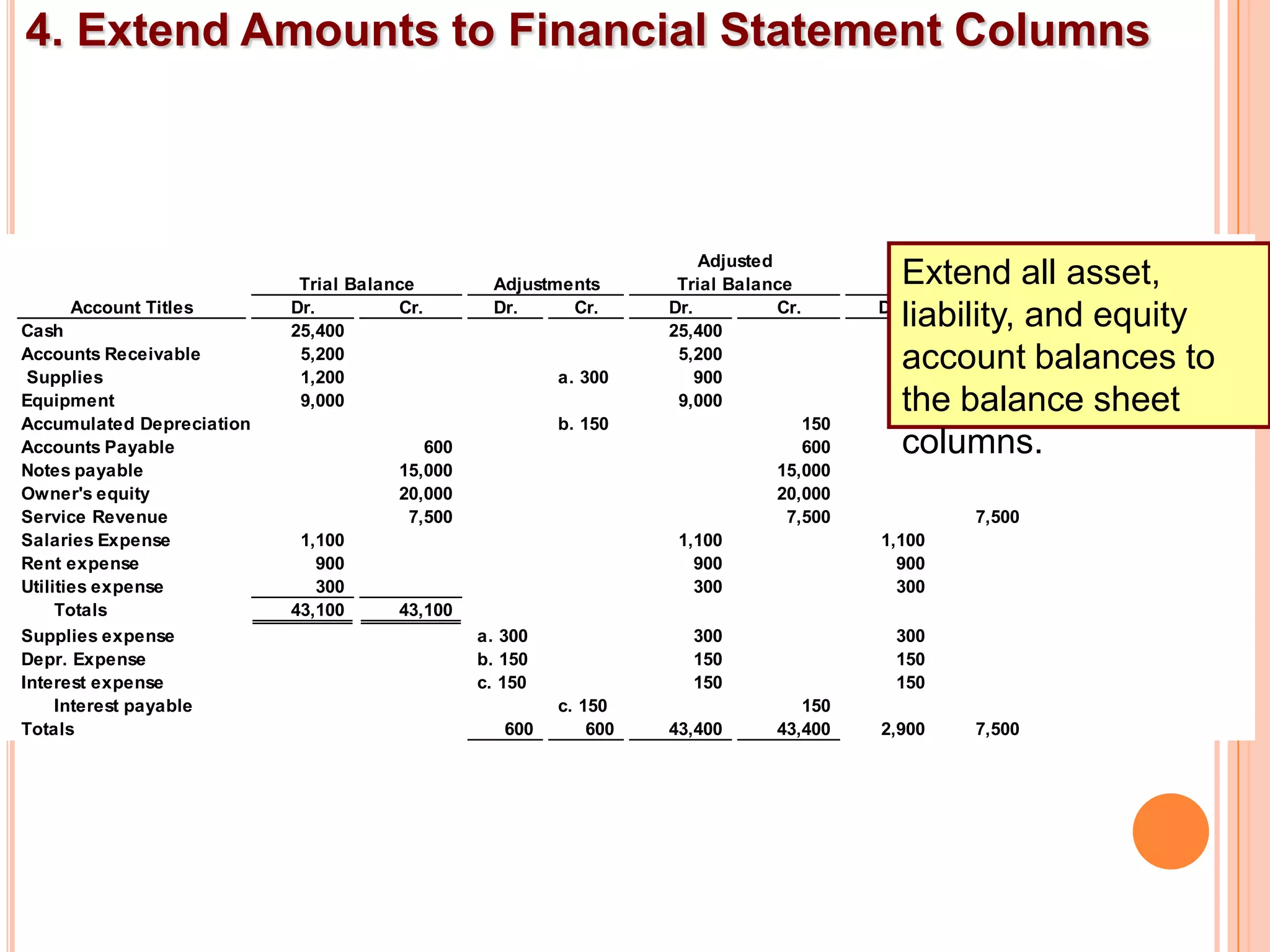

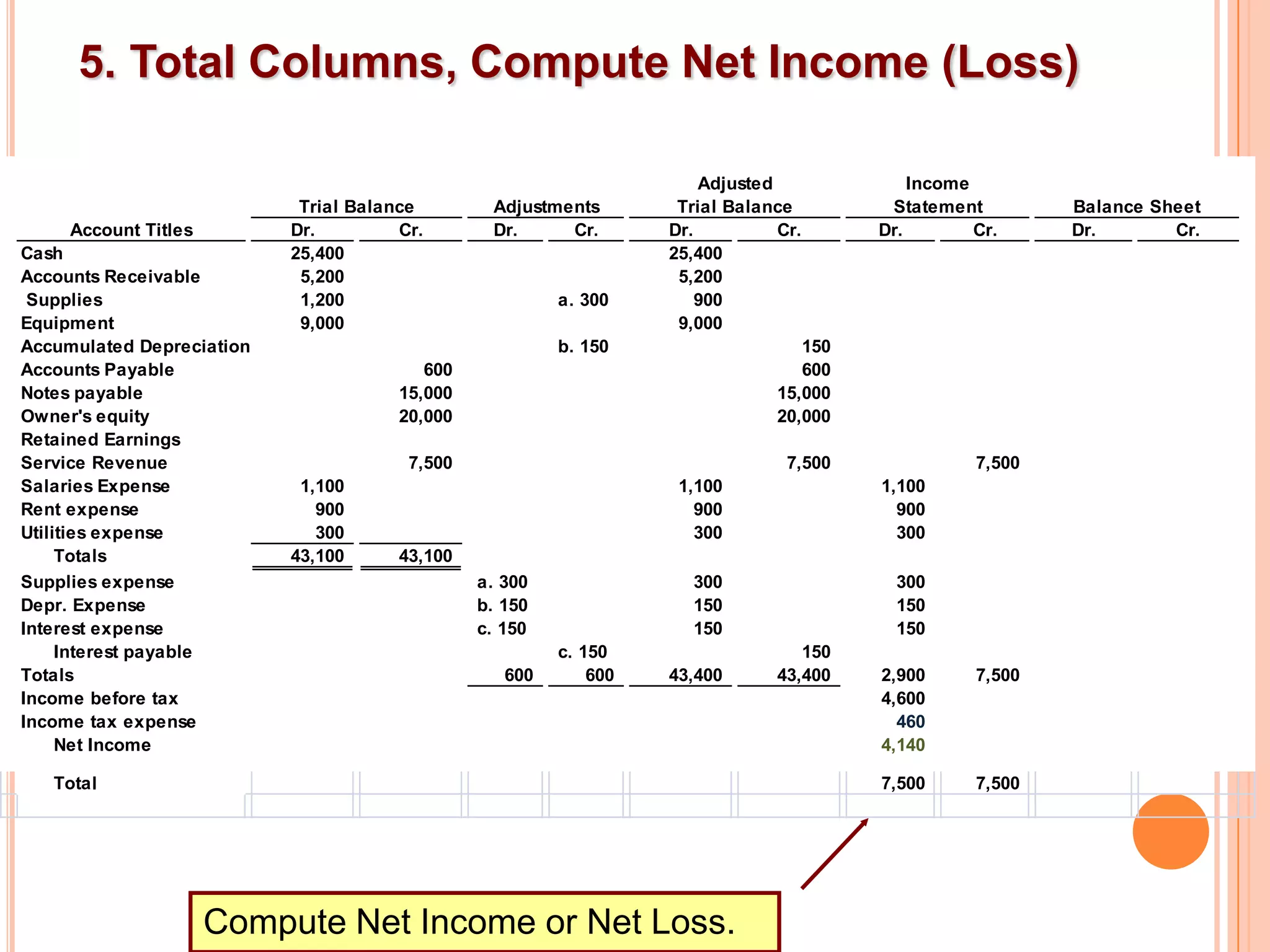

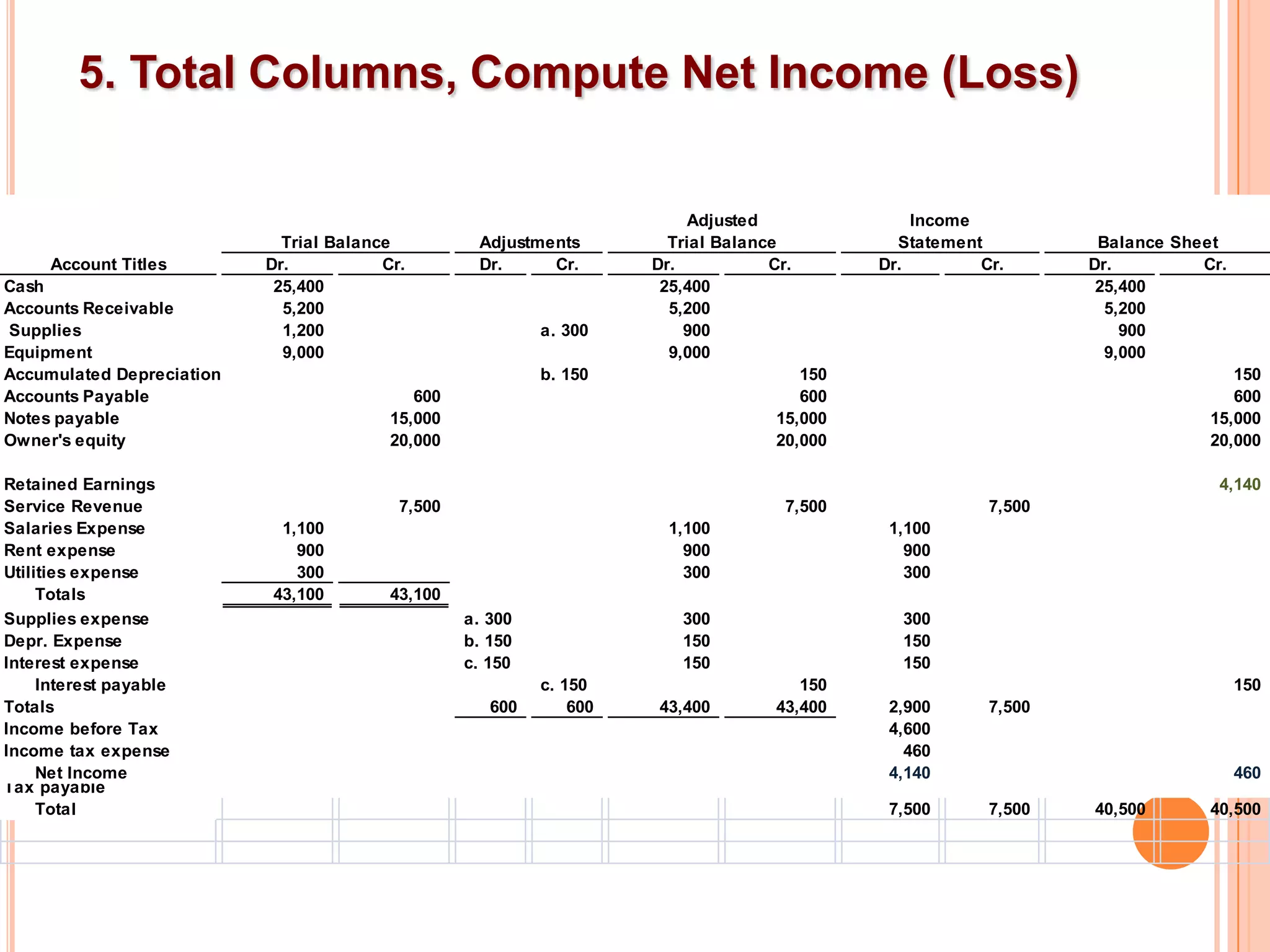

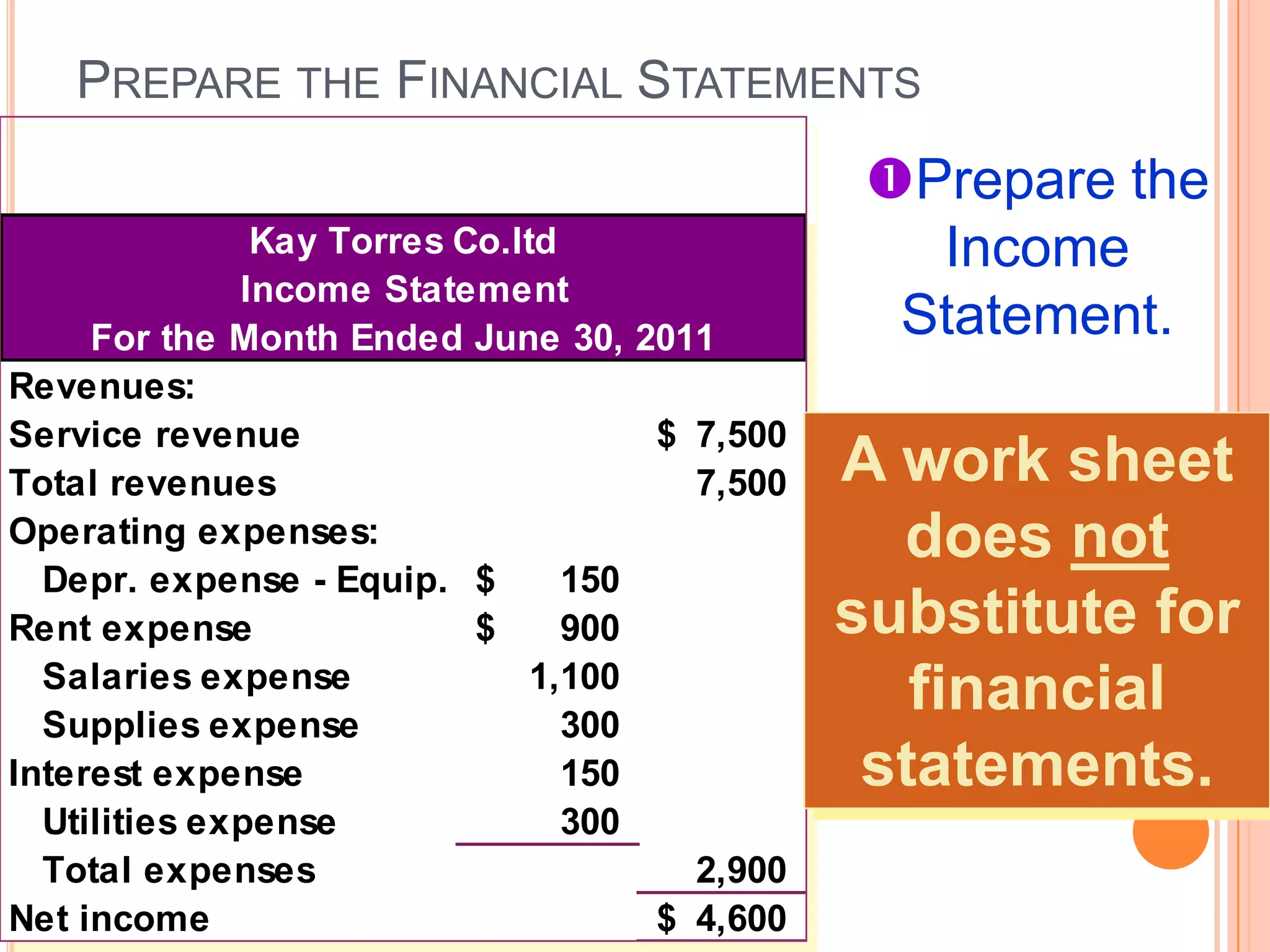

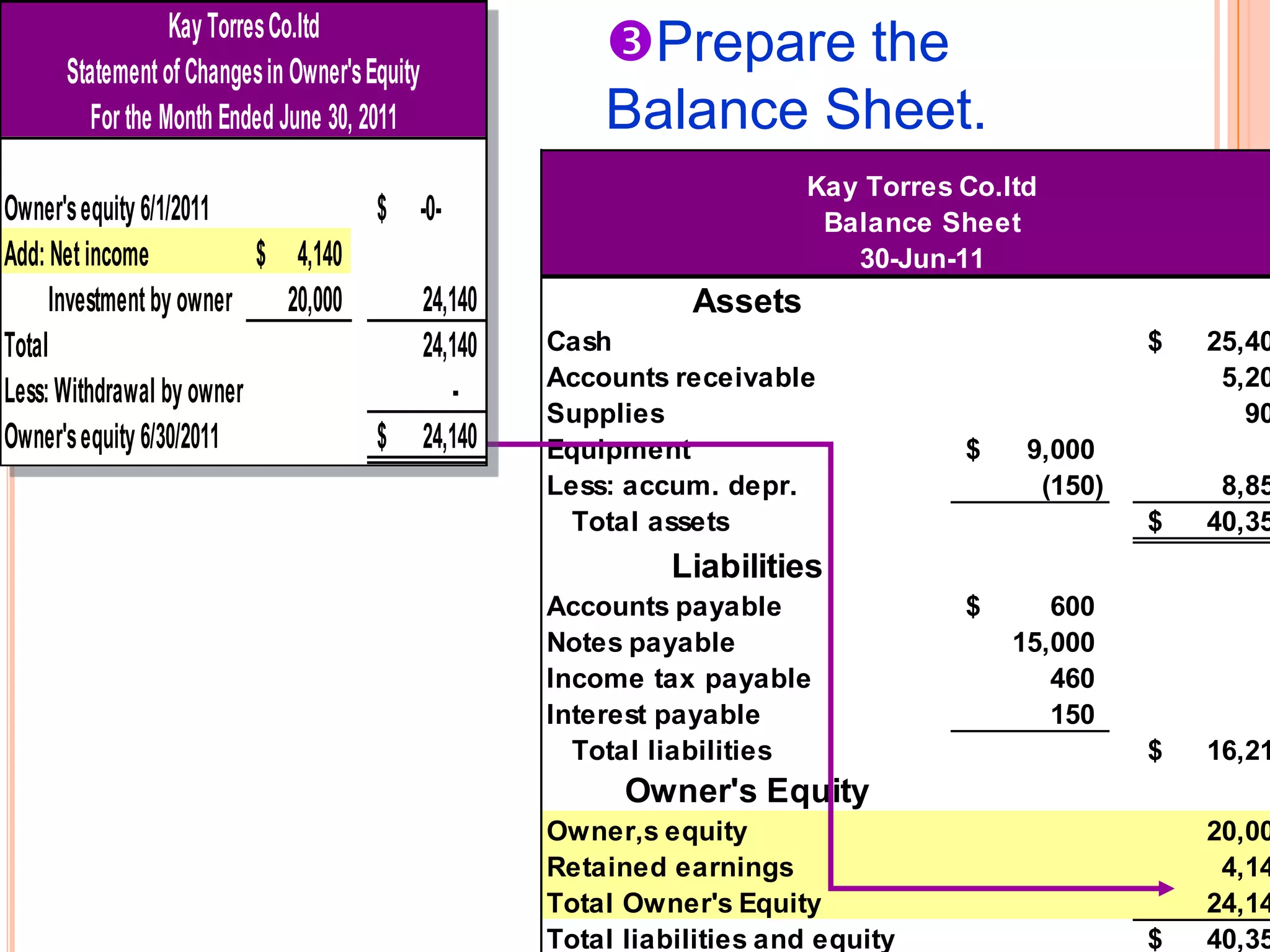

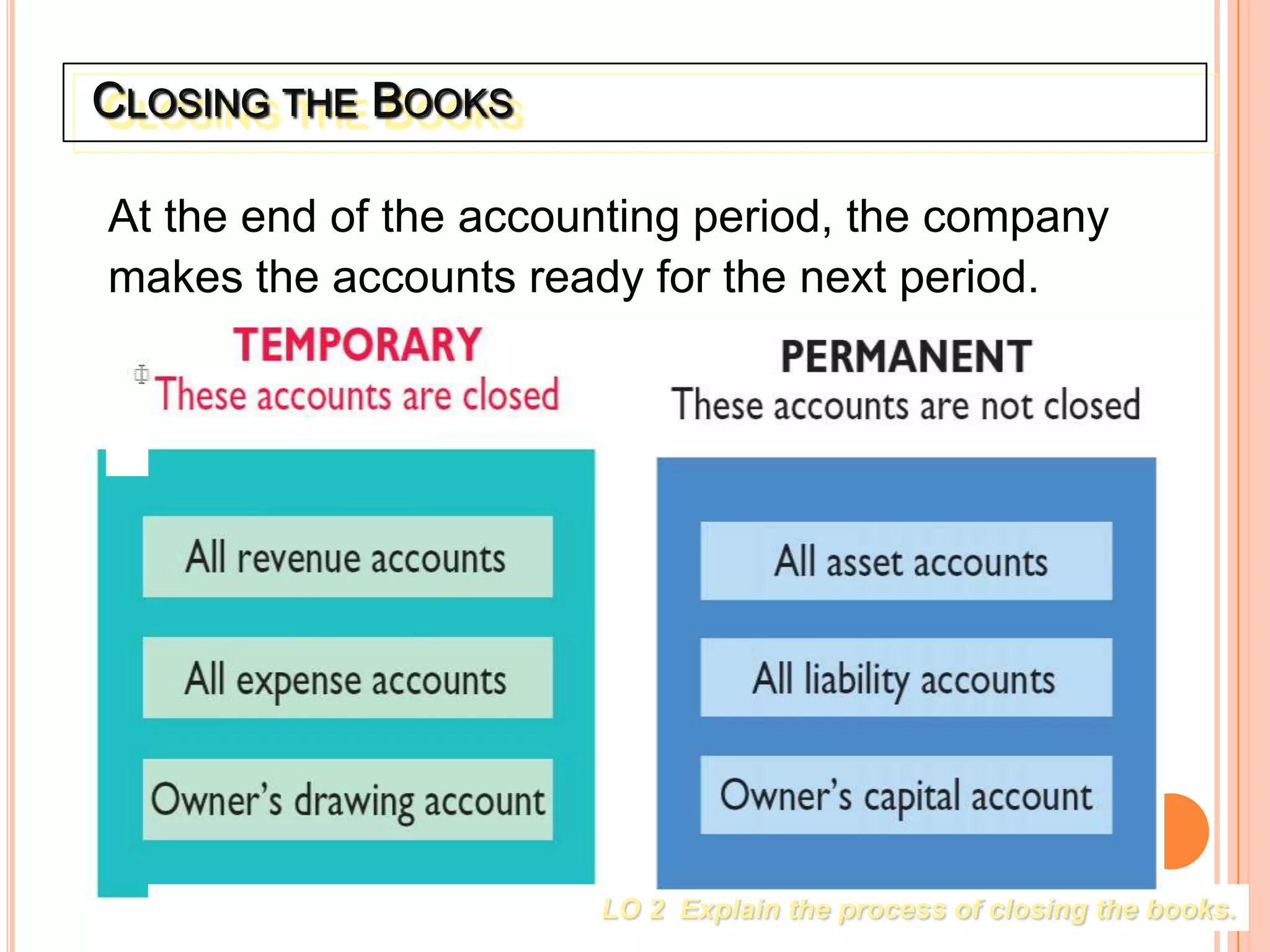

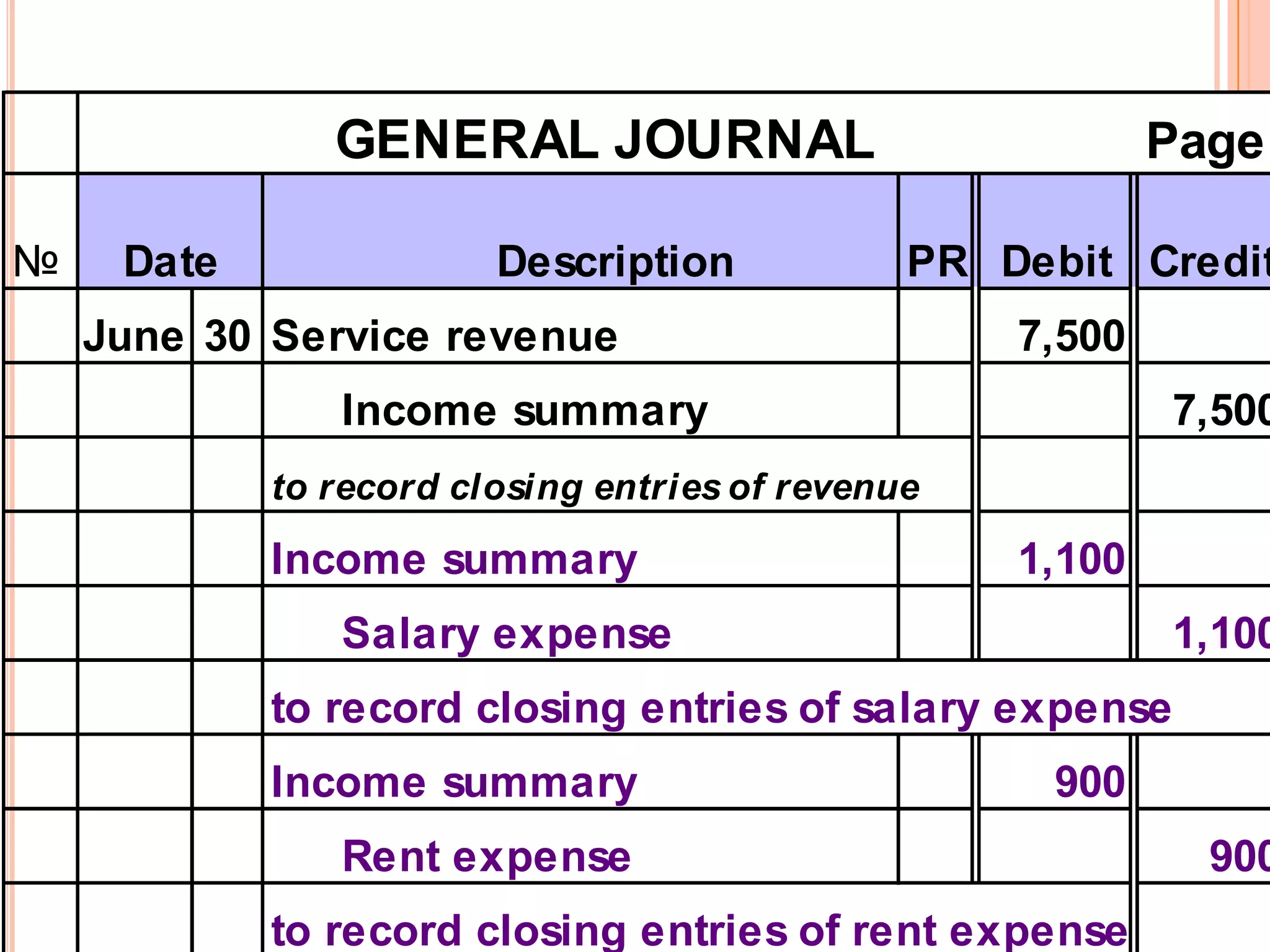

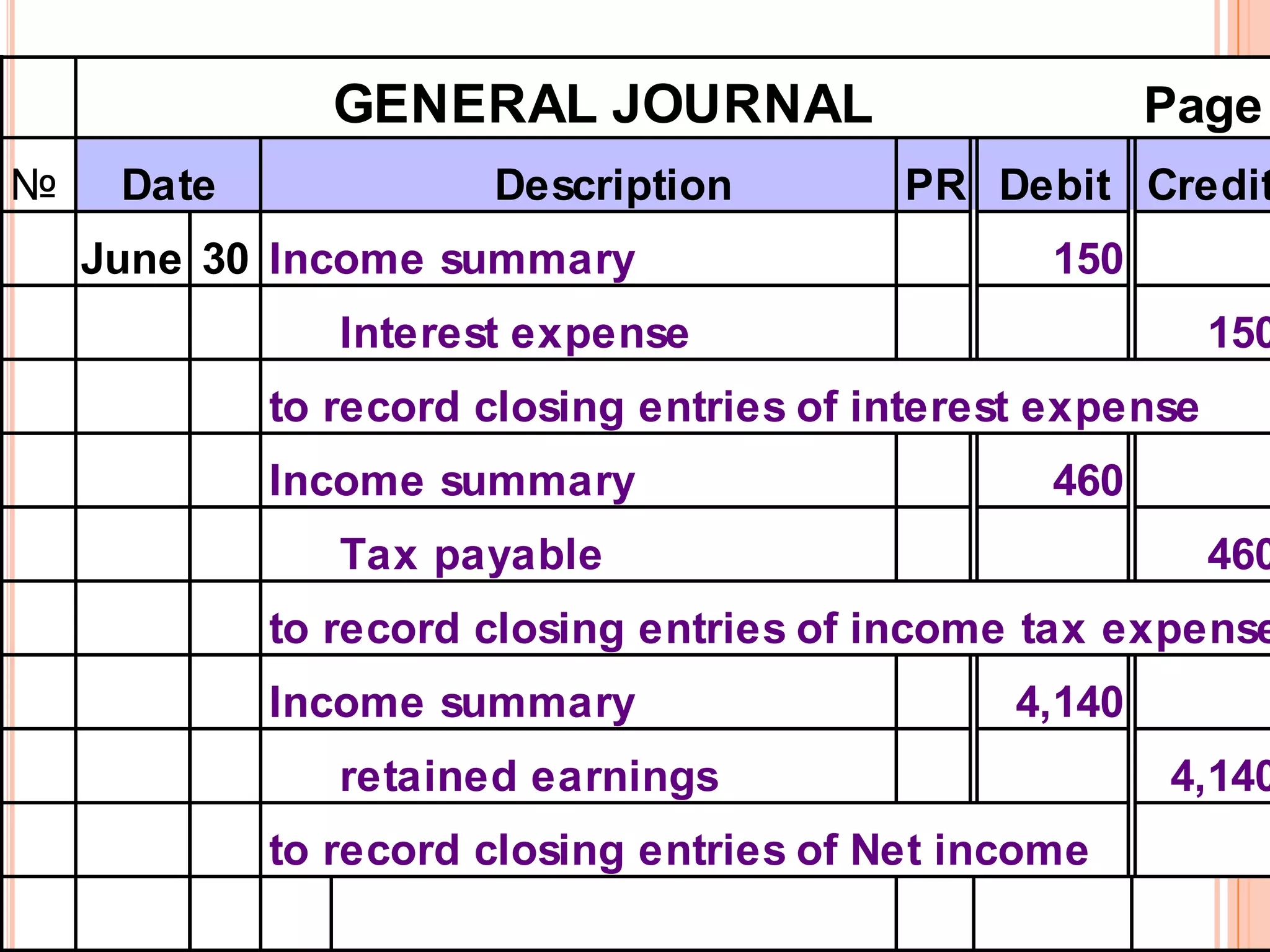

This document discusses key accounting concepts including the accounting cycle, journal entries, the general ledger, and trial balance. It provides examples of business transactions and their impact on the accounting equation. The accounting cycle involves recording transactions, preparing journal entries, posting to ledger accounts, creating an adjusted trial balance, and producing financial statements. Double-entry accounting and the rules for debit and credit entries are also explained.