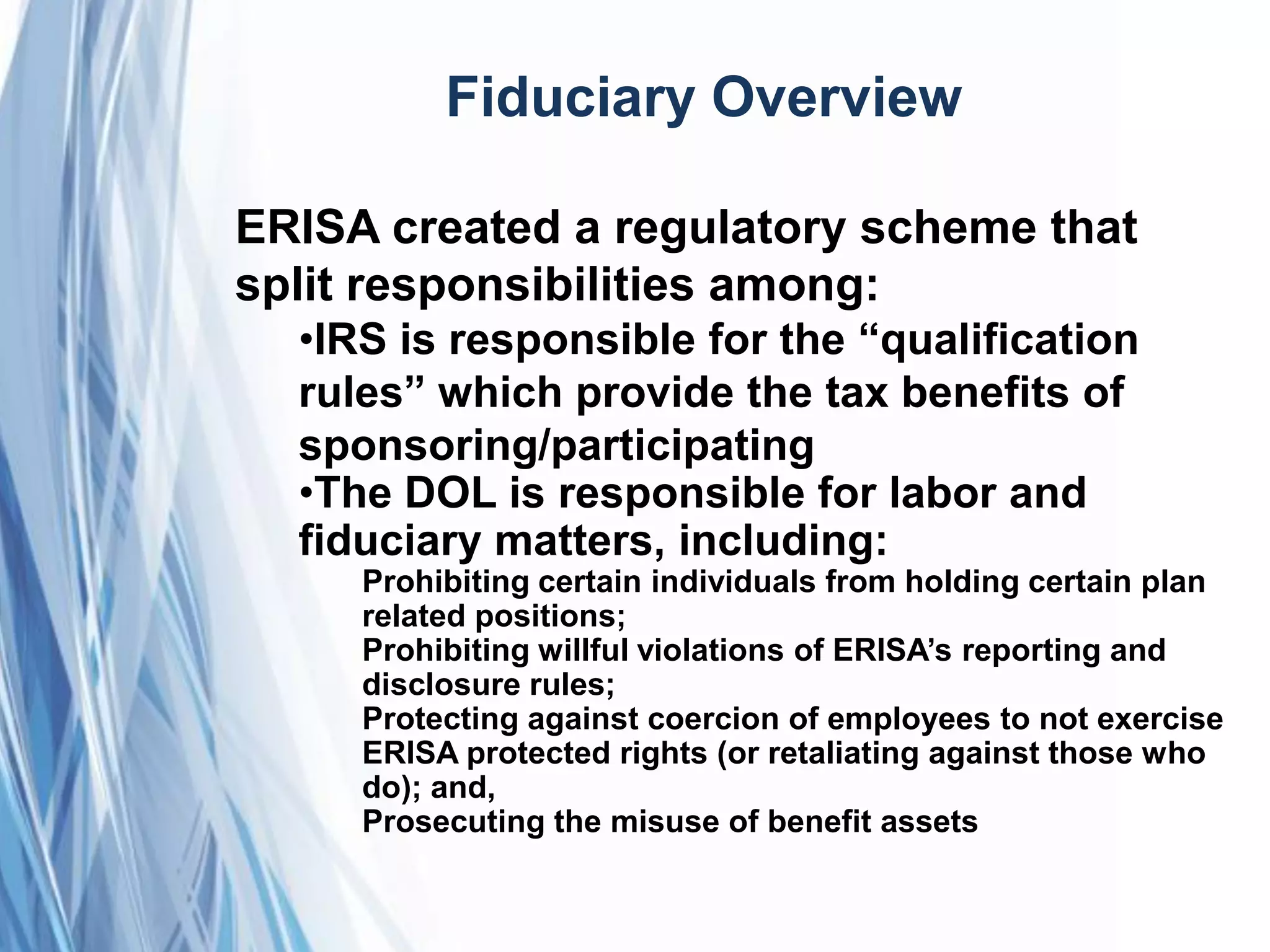

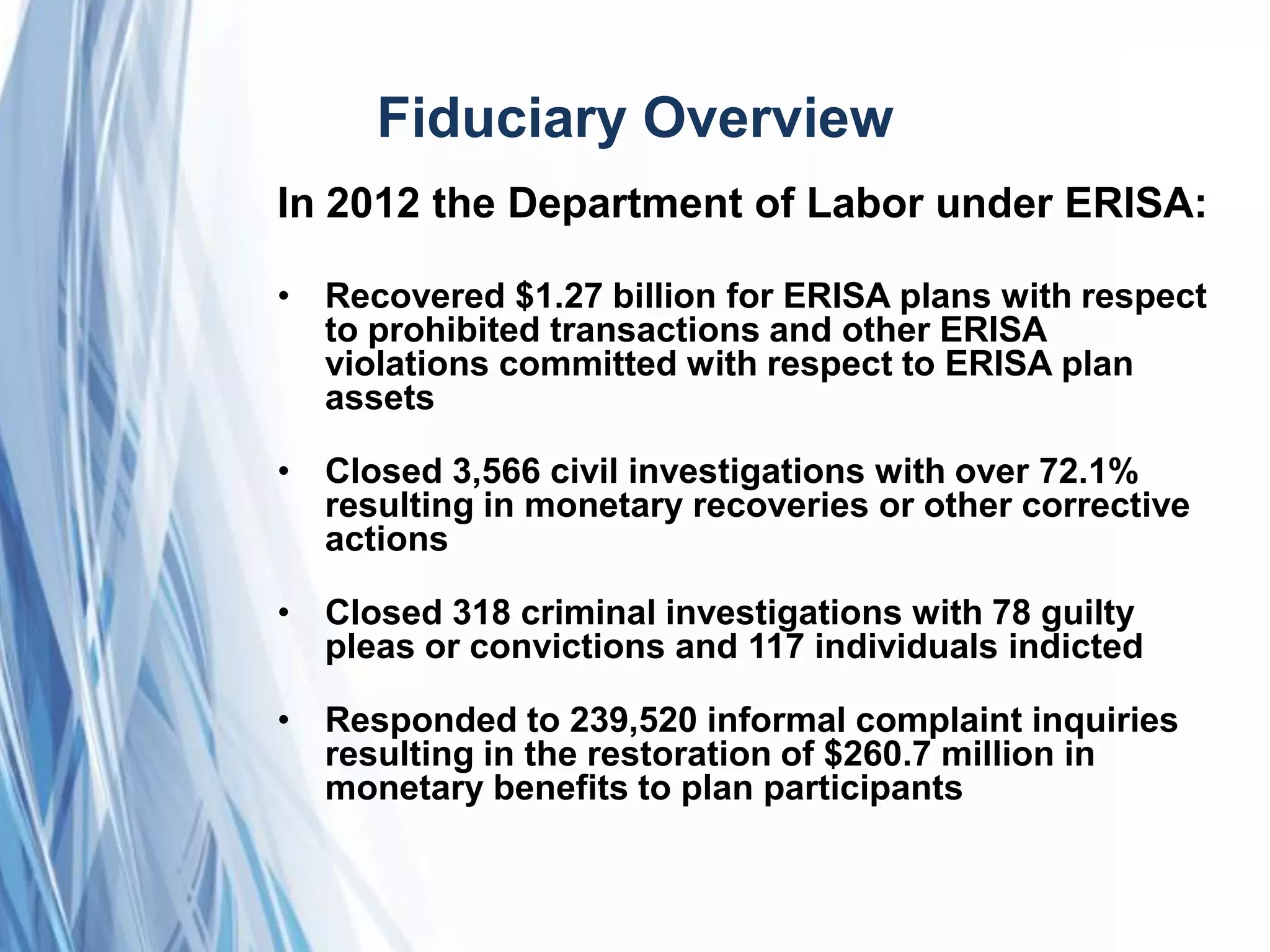

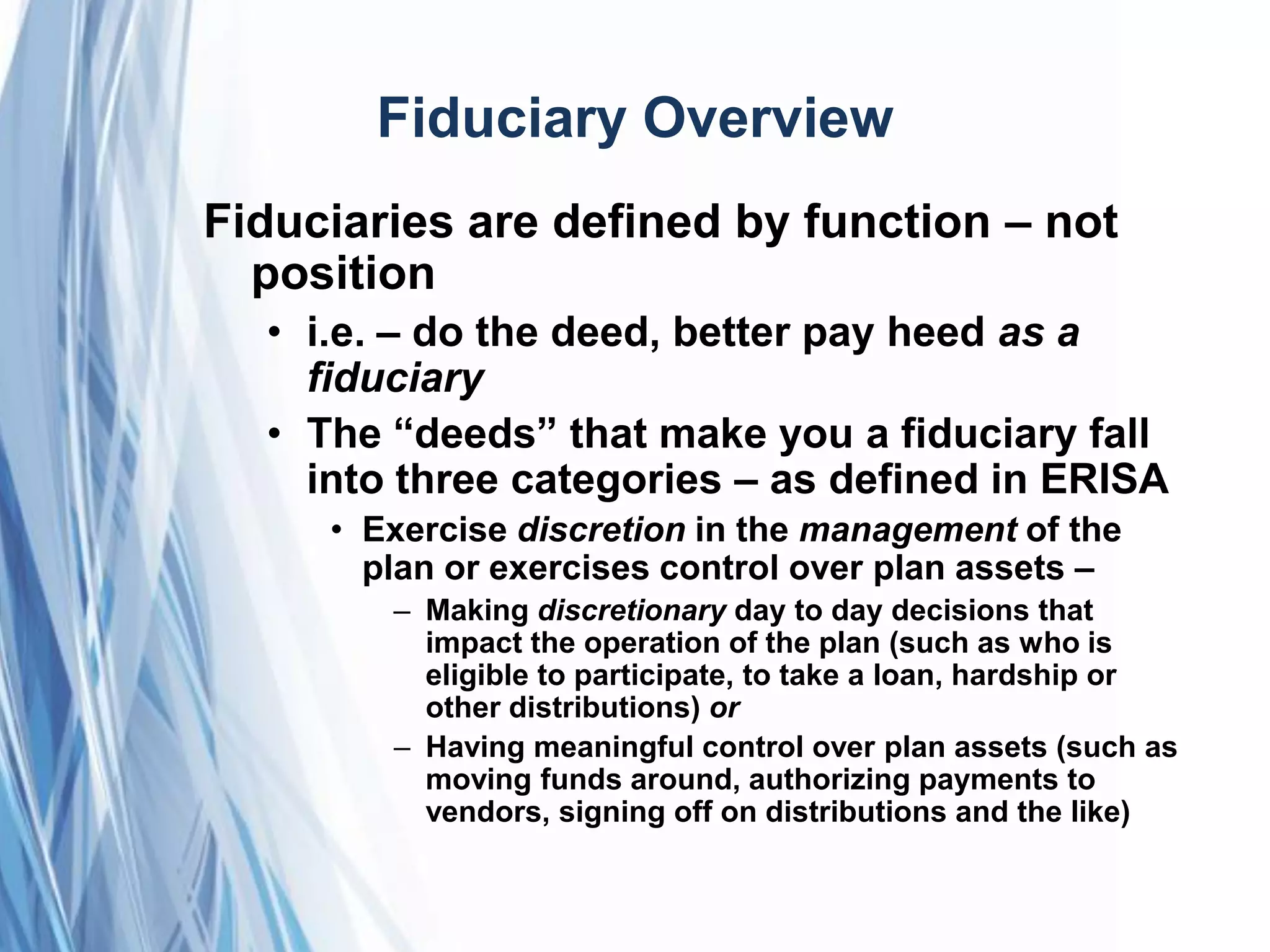

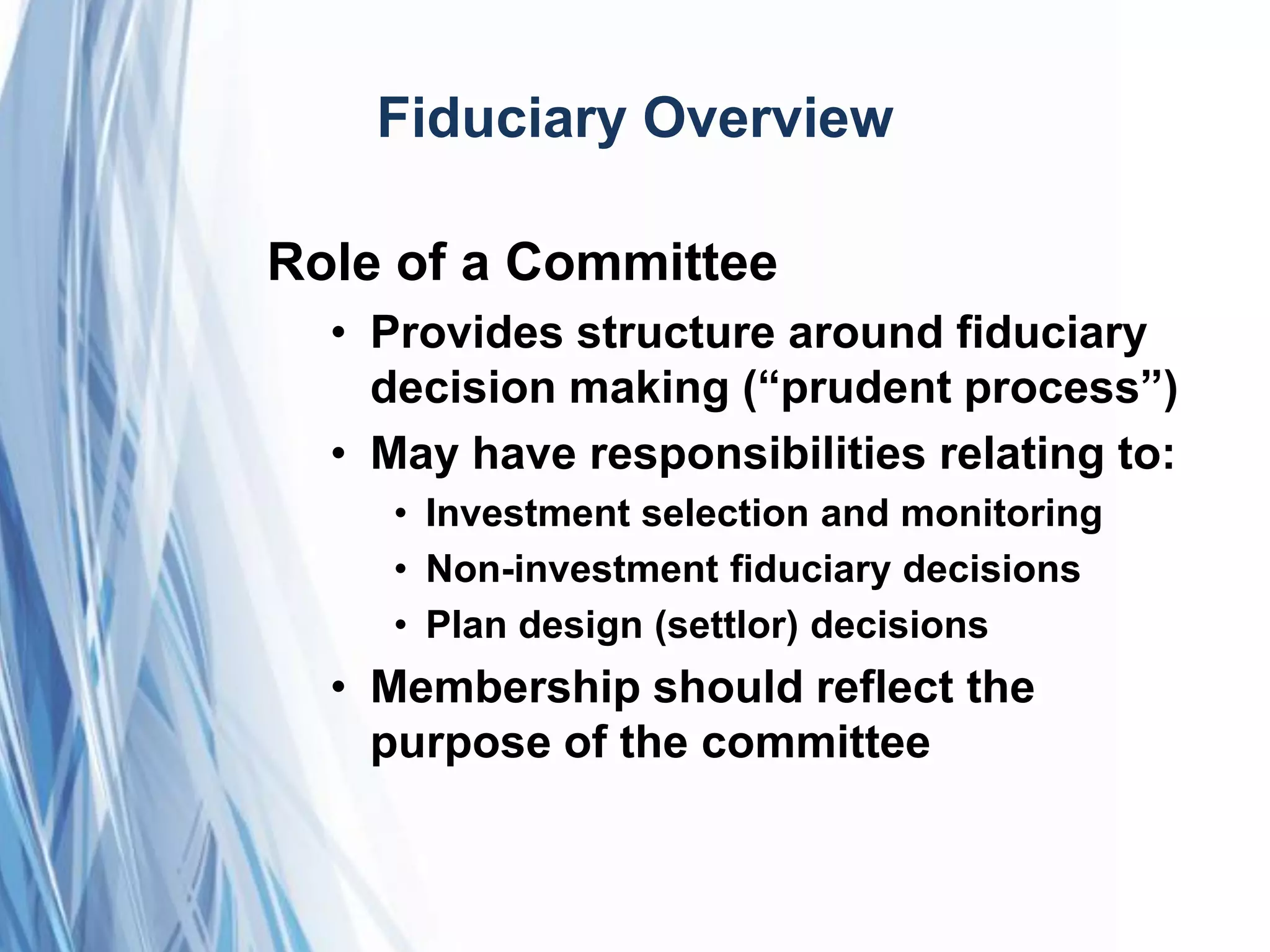

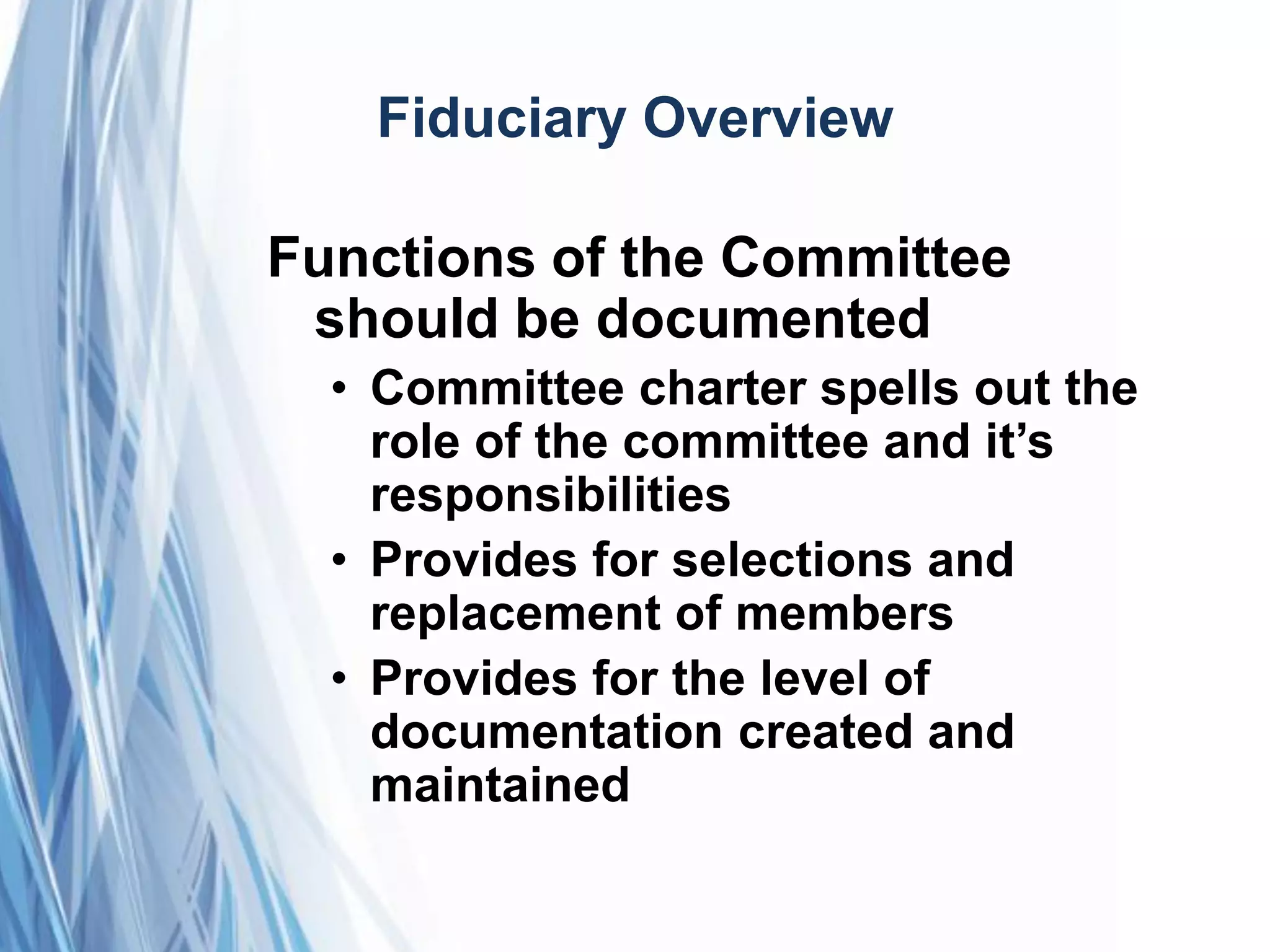

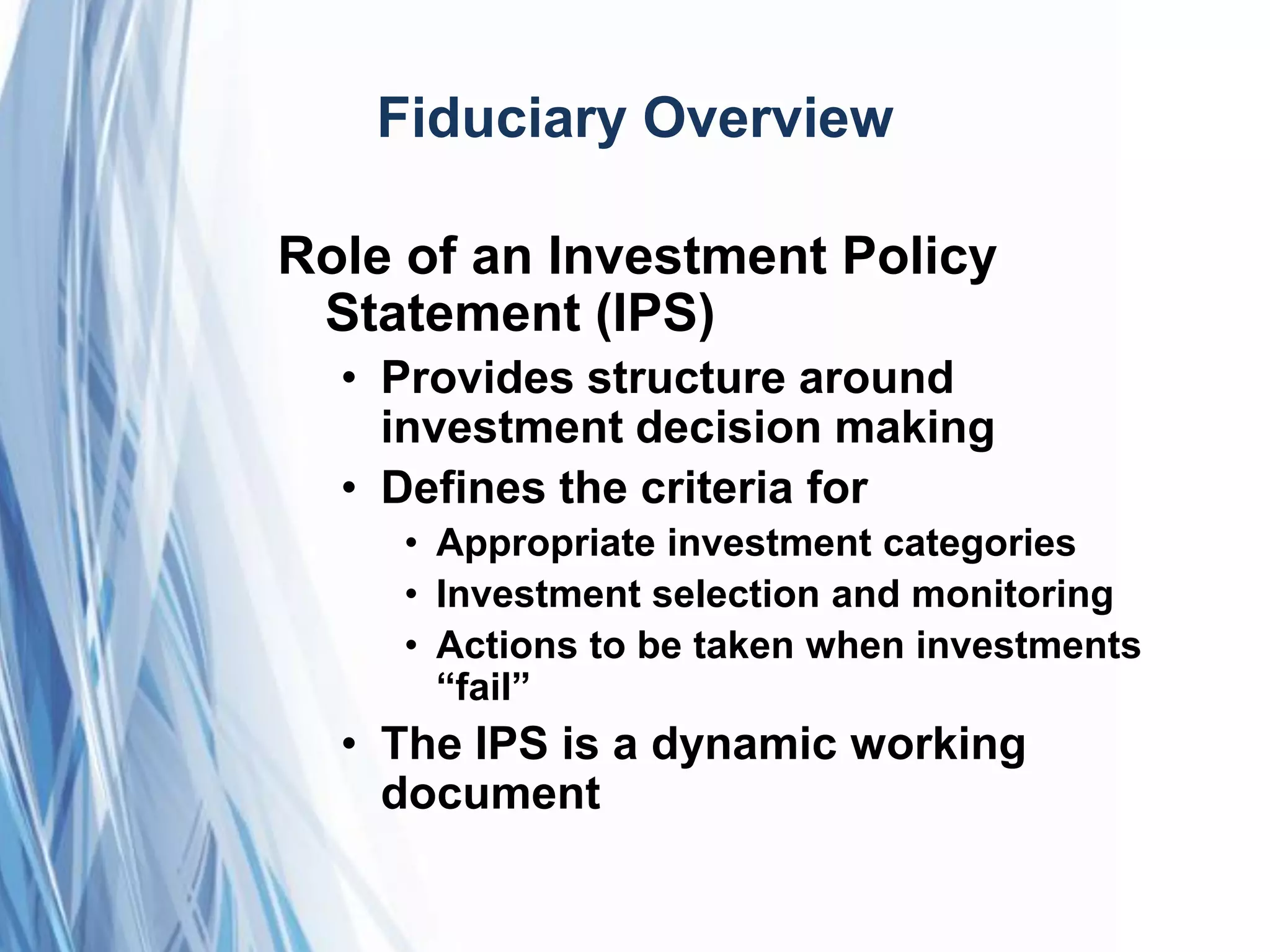

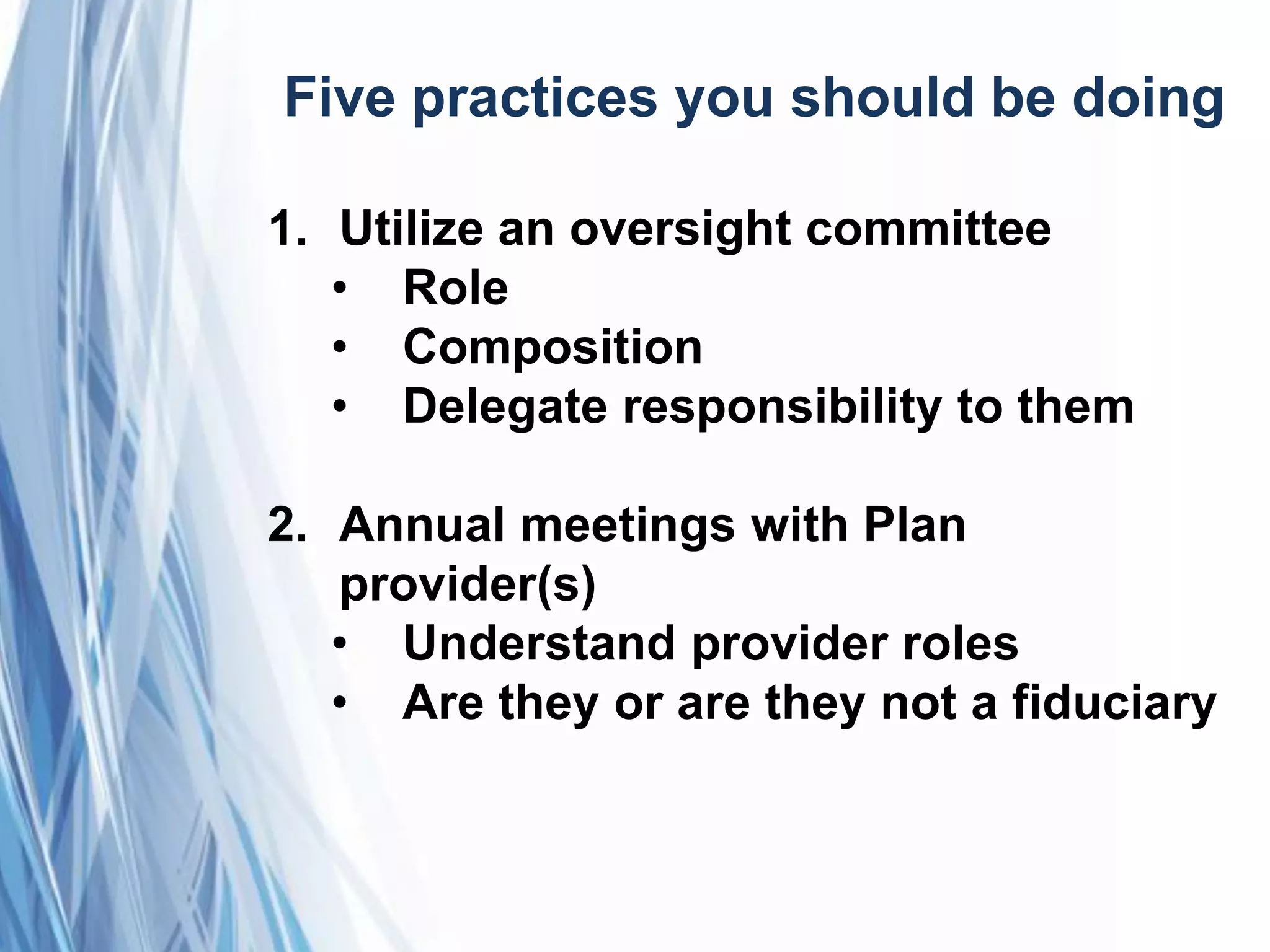

The document outlines a program on fiduciary responsibilities under ERISA, emphasizing the regulatory roles of the IRS and DOL, and detailing the obligations of fiduciaries. Key topics include the definition of fiduciary duties, the roles of employers and plan sponsors, and recommended practices for effective fiduciary management. It highlights essential actions and common pitfalls to avoid for fiduciaries to ensure compliance and protect the interests of plan participants.