Downloaded 60 times

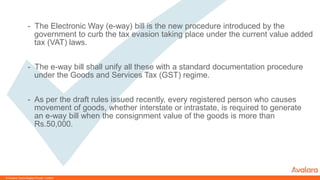

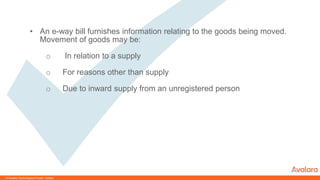

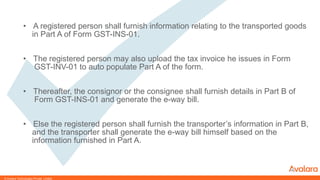

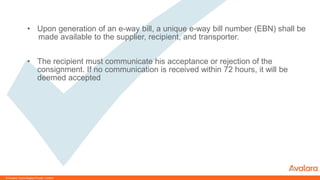

The e-way bill is a new procedure introduced to curb tax evasion under GST, requiring registered individuals to generate it for consignment values exceeding ₹50,000. Key rules include the generation of e-way bills by consignors or transporters, communication of acceptance by the recipient, and responsibilities of transporters in handling multiple consignments. The government aims to reduce human intervention and minimize penalties during the initial phase of implementation.

![20260201 [FOSDEM] gomodjail - library sandboxing for Go modules.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/20260201fosdemgomodjail-librarysandboxingforgomodules-260201225659-76609ec4-thumbnail.jpg?width=640&height=640&fit=bounds)