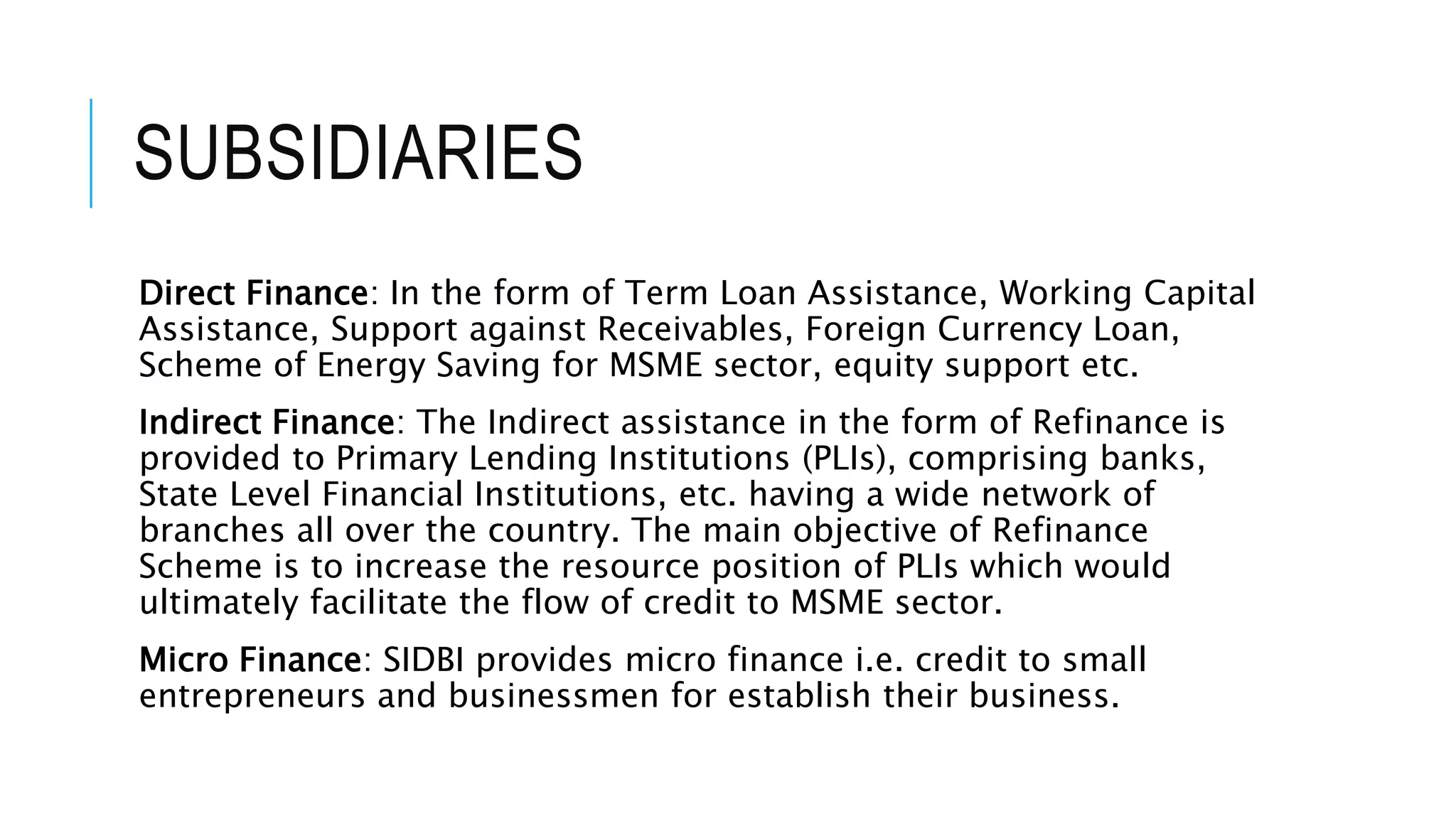

The document discusses the role and functions of NABARD and SIDBI in promoting agricultural and rural development in India. NABARD focuses on providing credit support and coordinating rural financing activities, while SIDBI aids small industries through refinancing and direct loans, particularly to micro-finance institutions. Both organizations aim to foster sustainable growth and development in rural and small industry sectors.