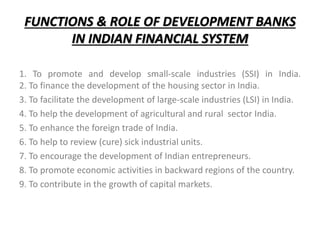

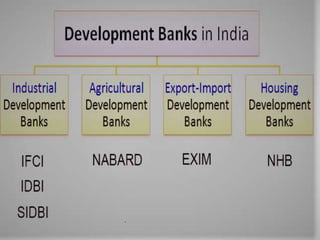

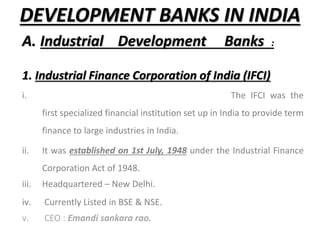

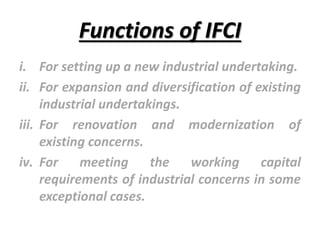

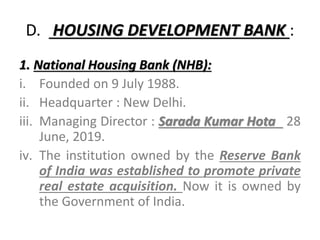

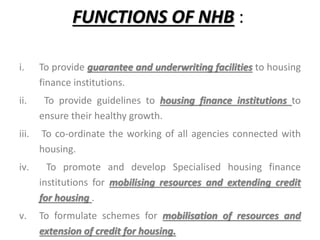

The document discusses Indian financial institutions and development banks, outlining their definitions, types, features, roles, and functions. It highlights key institutions such as commercial banks, investment banks, and various development banks like NABARD and IDBI, emphasizing their importance in financing sectors like agriculture and industry. Additionally, it explains the specific roles of these banks in promoting economic growth and providing long-term credit to facilitate development in India.