Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (20)

Similar to Derogatory Seasoning Matrix

Similar to Derogatory Seasoning Matrix (20)

Derogatory Seasoning Matrix

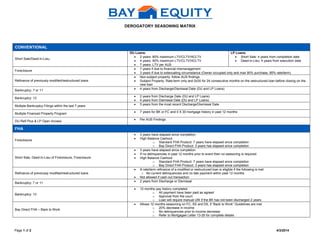

- 1. DEROGATORY SEASONING MATRIX Page 1 of 2 4/3/2014 CONVENTIONAL Short Sale/Deed-In-Lieu DU Loans: 2 years: 80% maximum LTV/CLTV/HCLTV 4 years: 90% maximum LTV/CLTV/HCLTV 7 years: LTV per AUS LP Loans: Short Sale: 4 years from completion date Deed-in-Lieu: 4 years from execution date Foreclosure 7 years if due to financial mismanagement 3 years if due to extenuating circumstance (Owner occupied only and max 90% purchase, 95% rate/term) Refinance of previously modified/restructured loans Non-subject property: follow AUS findings Subject Property: Rate-term only and 0x30 for 24 consecutive months on the restructured loan before closing on the new loan Bankruptcy: 7 or 11 4 years from Discharge/Dismissal Date (DU and LP Loans) Bankruptcy: 13 2 years from Discharge Date (DU and LP Loans) 4 years from Dismissal Date (DU and LP Loans) Multiple Bankruptcy Filings within the last 7 years 5 years from the most recent Discharge/Dismissal Date Multiple Financed Property Program 7 years for BK or FC and 0 X 30 mortgage history in past 12 months DU Refi Plus & LP Open Access Per AUS Findings FHA Foreclosure 3 years have elapsed since completion High Balance Cashout: o Standard FHA Product: 7 years have elapsed since completion o Bay Direct FHA Product: 3 years has elapsed since completion Short Sale, Deed-In-Lieu of Foreclosure, Foreclosure 3 years have elapsed since completion If no delinquencies in past 12 months prior to event then no seasoning is required High Balance Cashout: o Standard FHA Product: 7 years have elapsed since completion o Bay Direct FHA Product: 3 years has elapsed since completion Refinance of previously modified/restructured loans A rate/term refinance of a modified or restructured loan is eligible if the following is met o No current delinquencies and no late payment within past 12 months Not allowed if cash out transaction Bankruptcy: 7 or 11 2 years from Discharge or Dismissal Bankruptcy: 13 12 months pay history completed o All payment have been paid as agreed o Approval from the court o Loan will require manual UW if the BK has not been discharged 2 years Bay Direct FHA – Back to Work Allows 12 months seasoning on FC, SS and DIL if “Back to Work” Guidelines are met o 20% decrease in income o No delinquencies prior to income decrease o Refer to Mortgagee Letter 13-26 for complete details

- 2. DEROGATORY SEASONING MATRIX Page 2 of 2 4/3/2014 VA Short Sale, Deed-In-Lieu of Foreclosure 2 years have elapsed since completion If no delinquencies in past 12 months prior to event then no seasoning is required High Balance o Standard VA Product: 7 years have elapsed since completion o Bay Direct VA Product: 2 years has elapsed since completion Foreclosure 2 years have elapsed since completion High Balance o Standard VA Product: 7 years have elapsed since completion o Bay Direct VA Product: 2 years has elapsed since completion Bankruptcy: 7 or 11 2 years from Discharge Date High Balance o Standard VA Product: 7 years have elapsed since completion o Bay Direct VA Product: 2 years has elapsed since completion Bankruptcy: 13 12 months pay history completed o All payment have been paid as agreed o Approval from the court High Balance o Standard VA Product: 7 years have elapsed since completion o Bay Direct VA product: follow the above USDA Short Sale/Preforeclosure 3 years from recorded date of Deed of Trust o Less than 3 years is acceptable if GUS approved and 640+ score. See USDA Guidelines Foreclosure 3 years have elapsed since completion Bankruptcy: 7 or 11 3 years from Discharge Date Bankruptcy: 13 3 years from Discharge Date 12 months from repayment period. o All payments made on time with written permission from the bankruptcy court/trustee