Downloaded 37 times

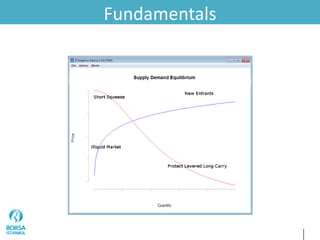

The document discusses advanced derivatives market practices, focusing on option trading strategies and mathematical tools used by traders for risk management and valuation. It explores the behavior of market participants, outlines various trading strategies, and highlights the impact of cognitive biases on trading decisions. Additionally, it emphasizes the importance of understanding supply and demand dynamics in the volatility surface and the role of behavioral economics in market pricing.