Downloaded 14 times

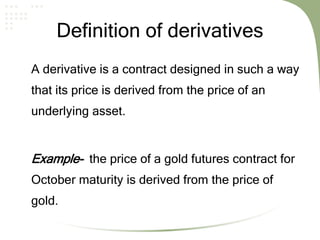

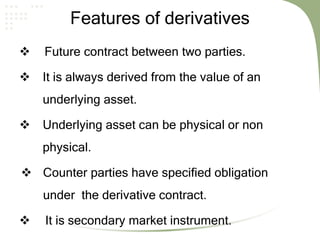

This document provides an overview of derivatives, including definitions, key features, and types. It defines a derivative as a contract whose price is derived from an underlying asset. There are three main types of derivative market participants: hedgers who face risk, speculators who bet on price movements, and arbitrageurs who trade to profit from pricing discrepancies. The document discusses forward contracts, futures contracts, and options, explaining their features, advantages/disadvantages, and how their prices are determined. It also covers some options terminology and factors that affect options pricing.

![Senior Project [Hien Truong, 4204745]](https://cdn.slidesharecdn.com/ss_thumbnails/a82856d9-6fc7-4bef-9d6b-c3ea4bbadfc0-150720053419-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)