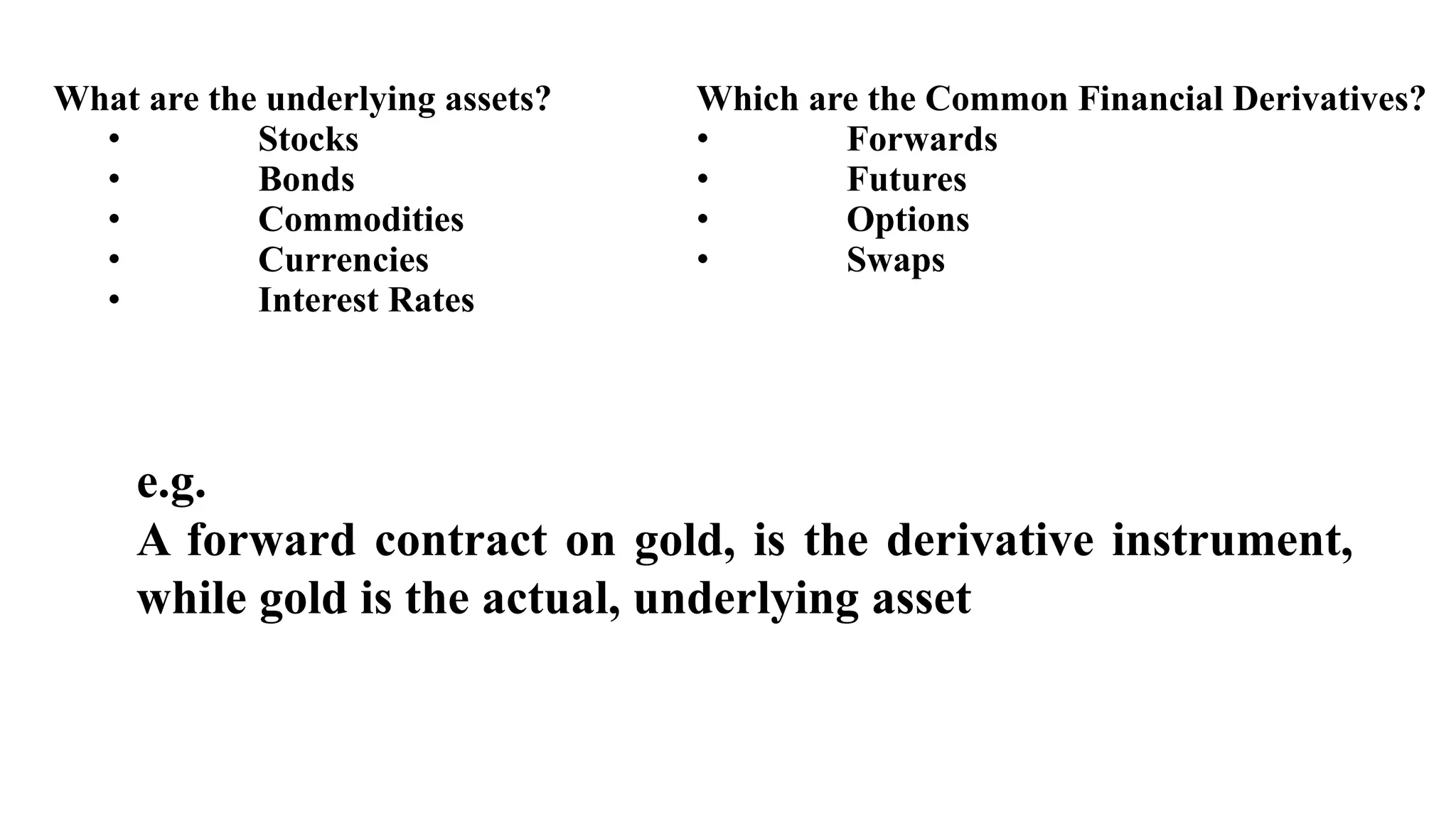

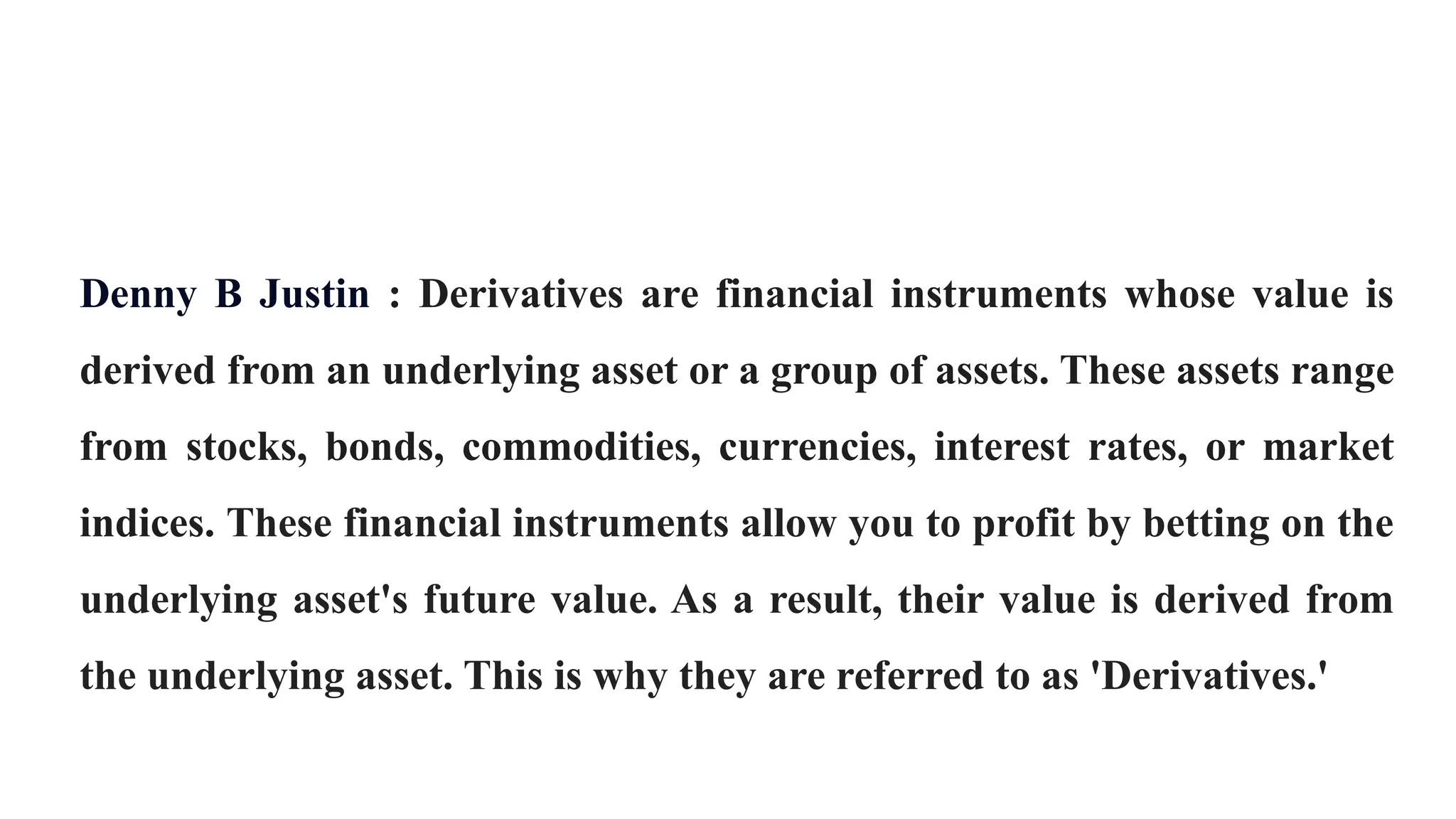

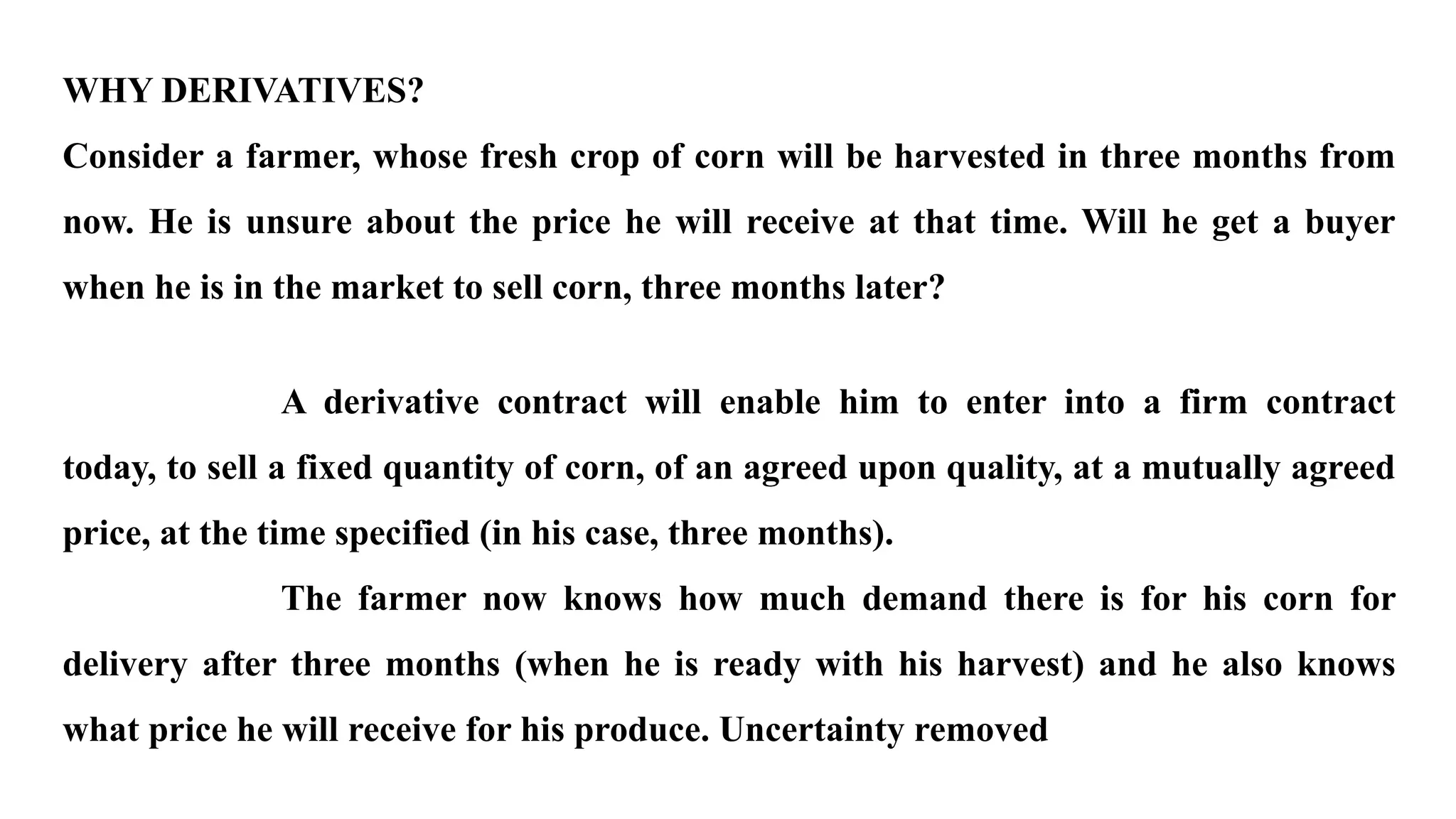

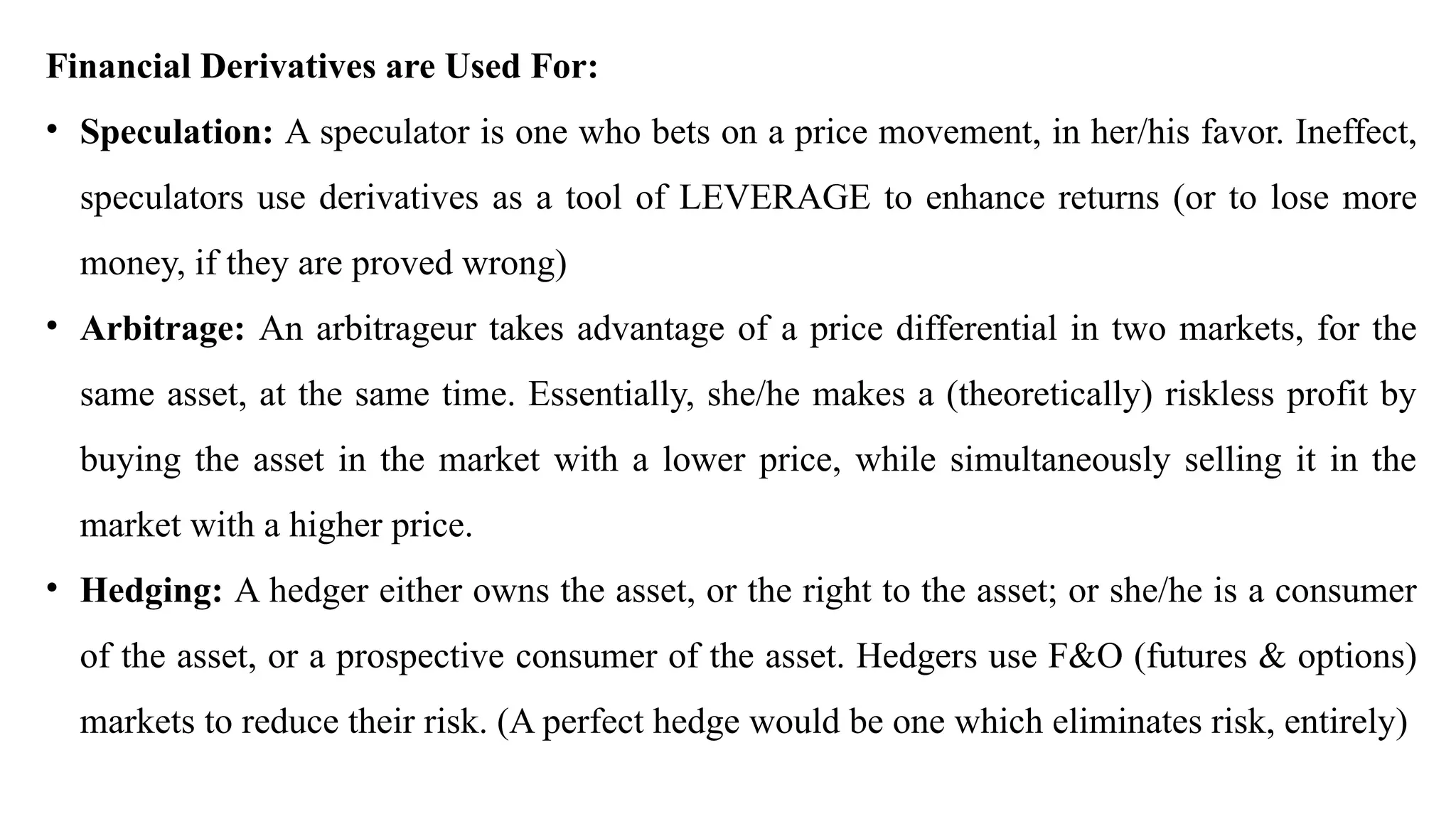

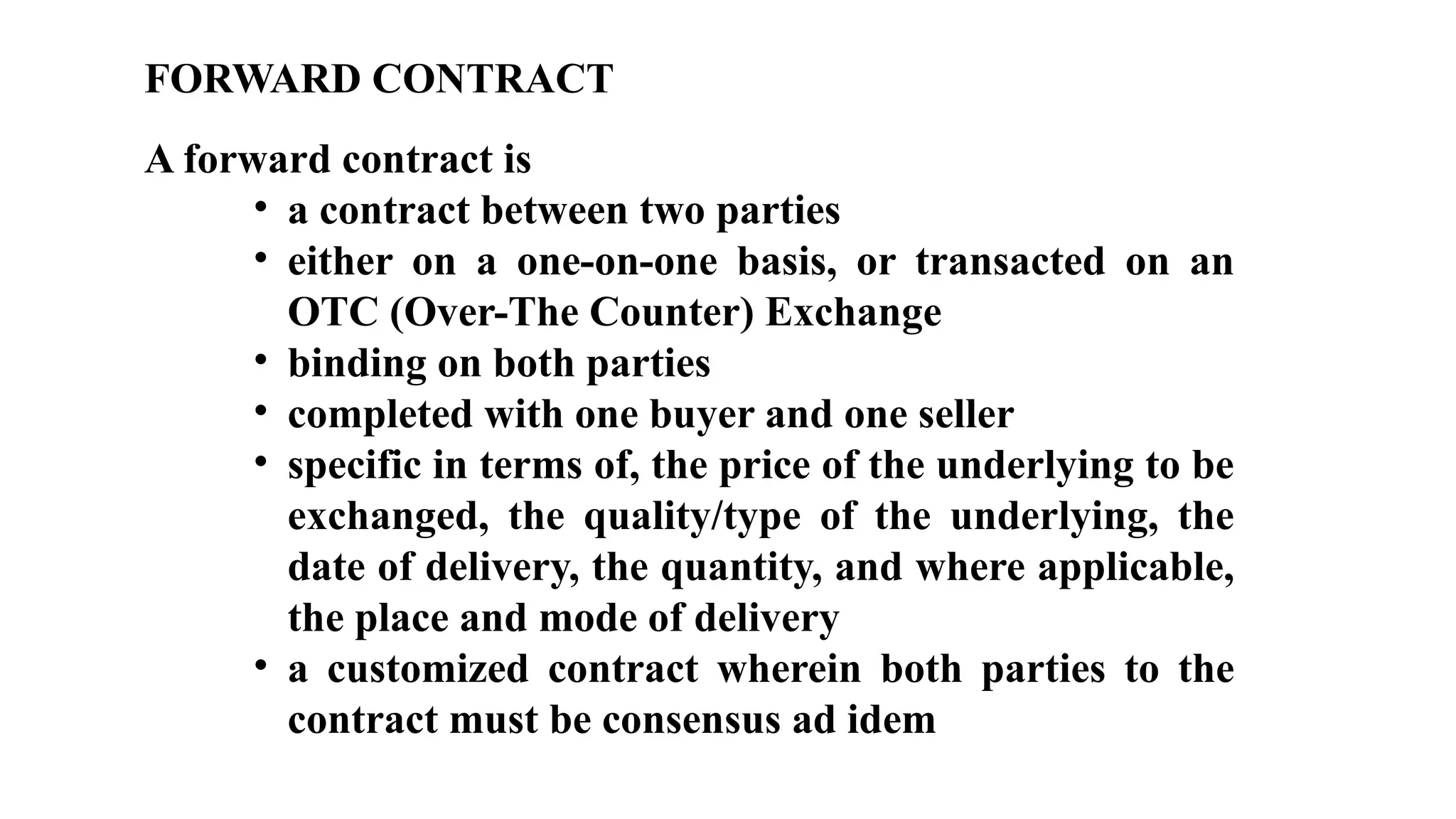

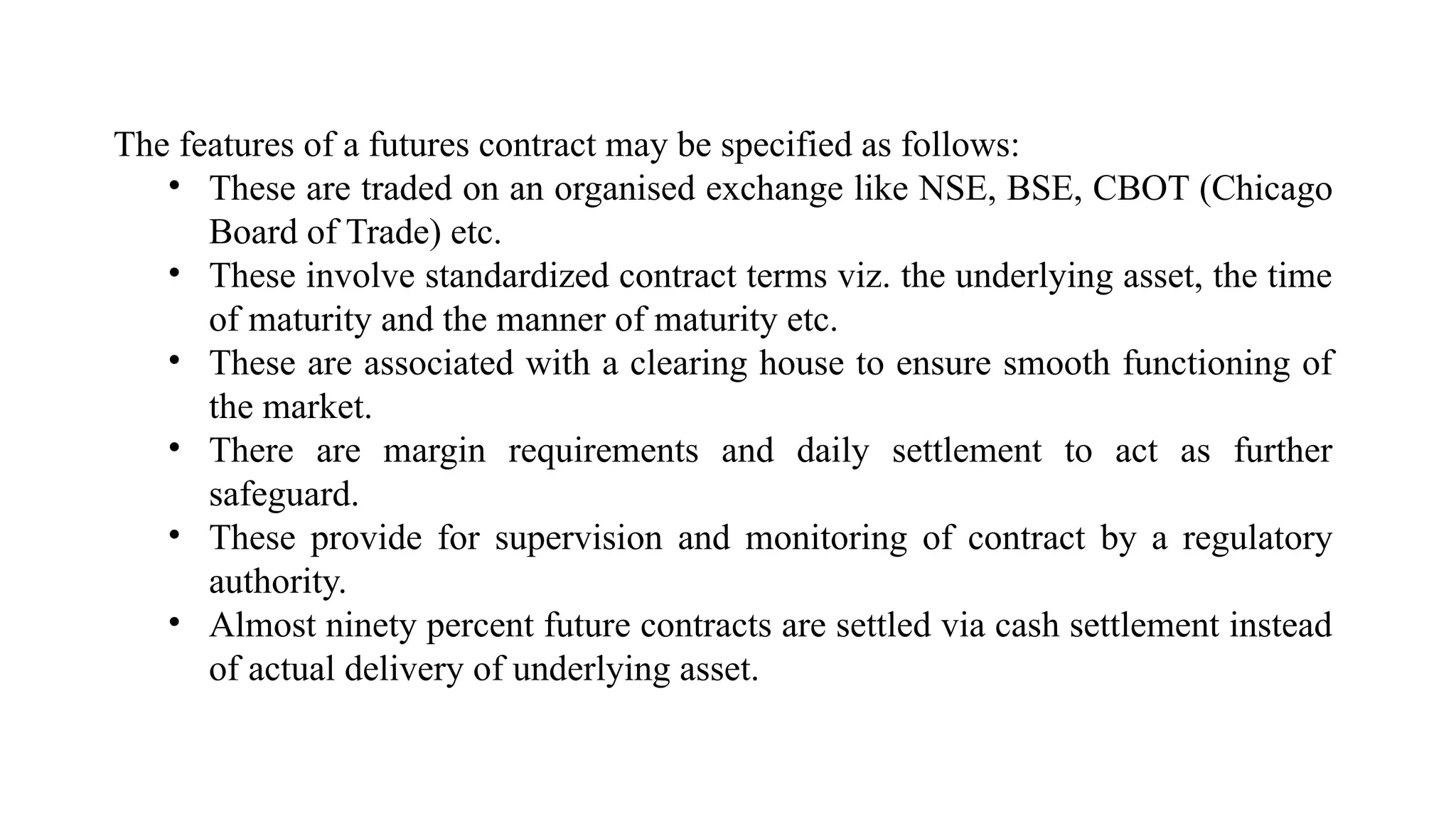

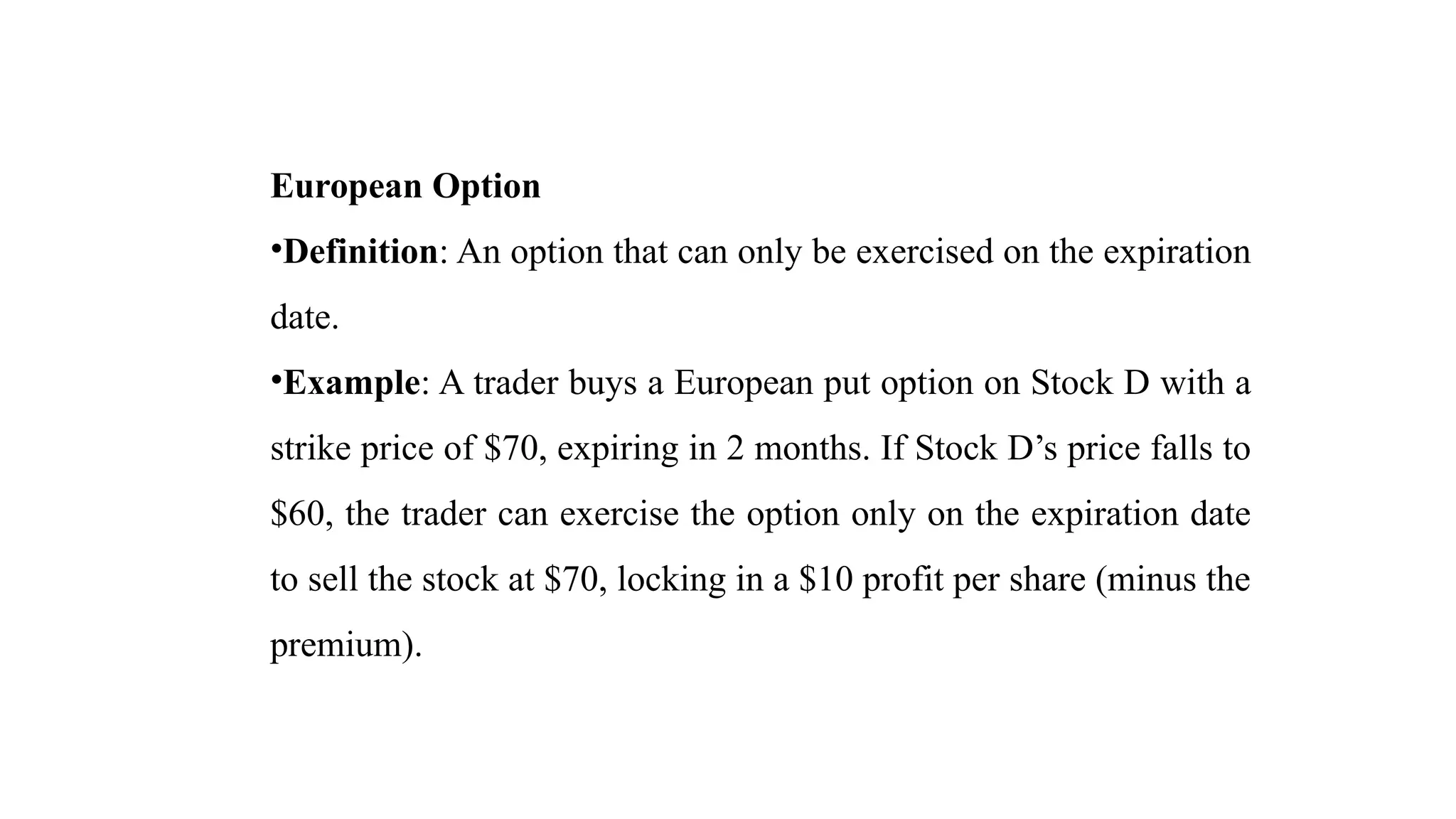

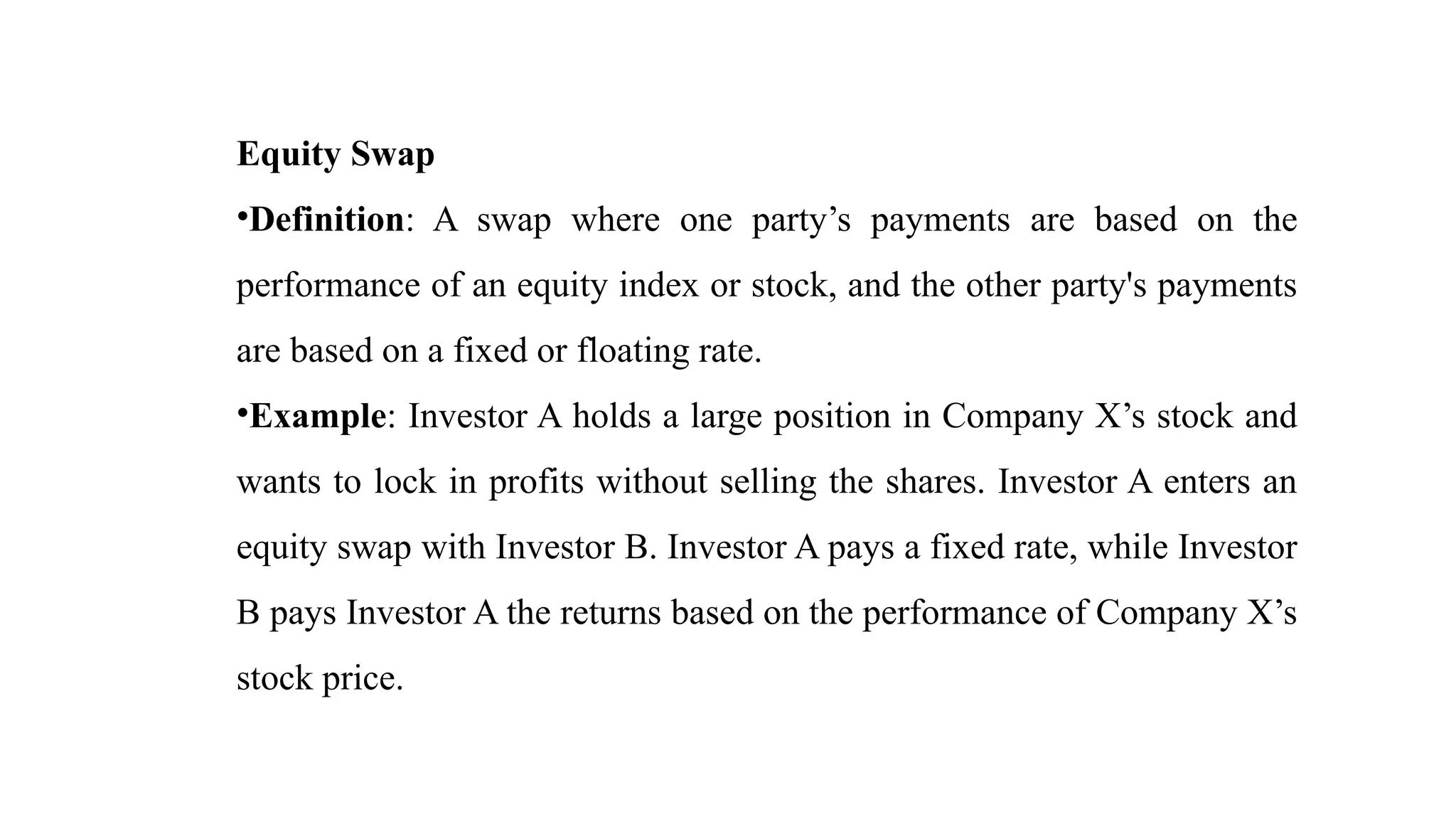

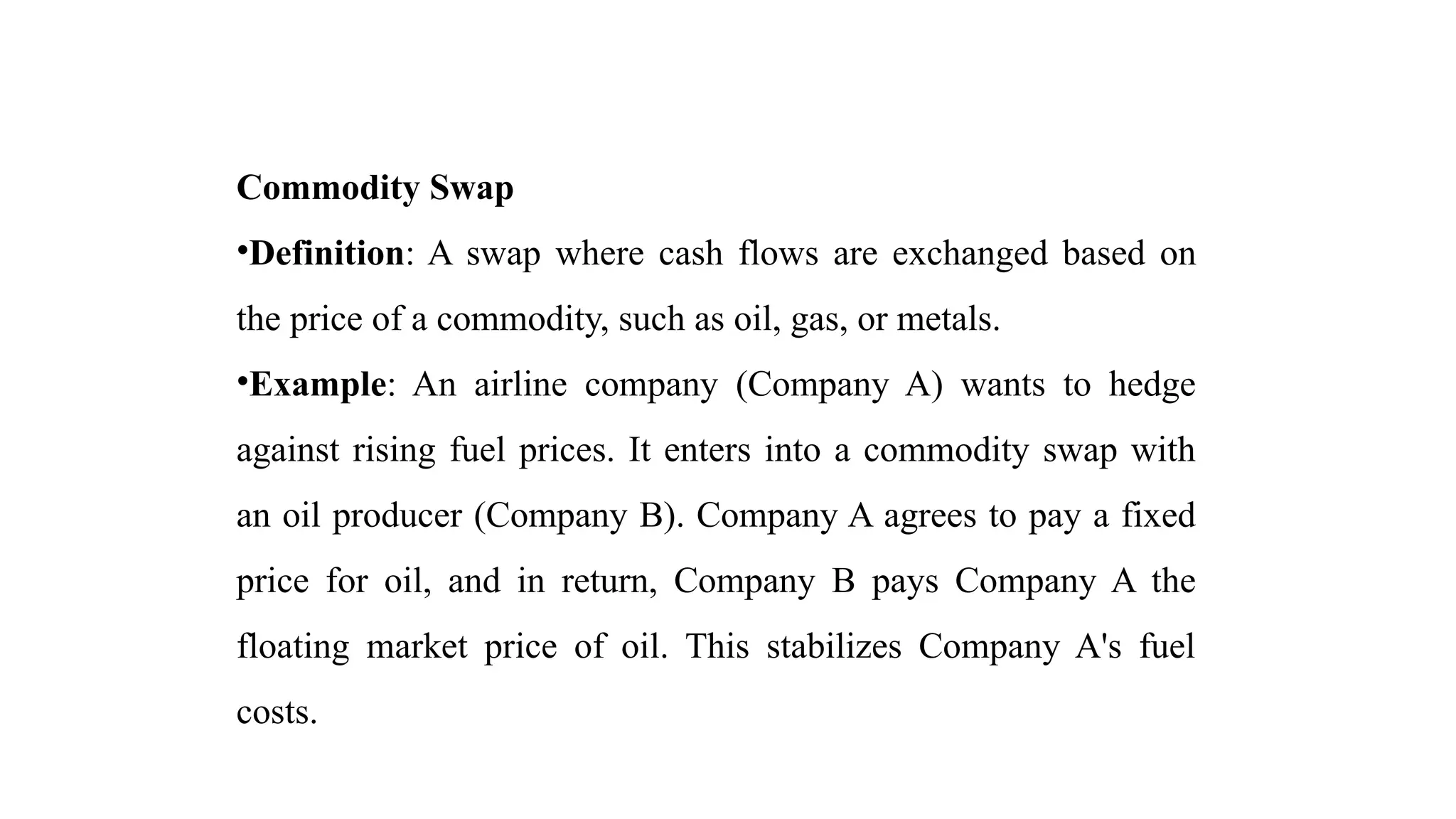

The document provides an overview of financial derivatives, which are instruments whose value is derived from underlying assets such as stocks, bonds, and commodities. It explains different types of derivatives, including forwards, futures, options, and swaps, as well as their purposes like speculation, arbitrage, and hedging. Additionally, it details the mechanics of various derivative contracts, including examples of their functions and risks involved.