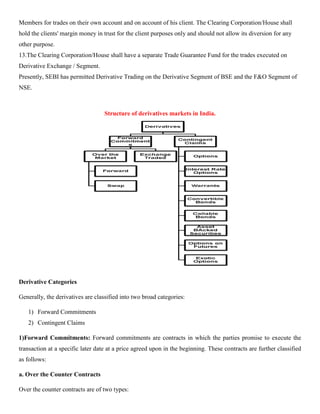

The document provides a comprehensive overview of financial derivatives, defining their nature, types, features, and functions in financial markets, as well as the regulatory framework surrounding them in India. It categorizes derivatives into types such as forwards, futures, options, and swaps, and discusses their uses in managing risks, enhancing market liquidity, while also outlining critiques regarding speculation and market stability. Additionally, it includes recommendations from the Dr. L.C. Gupta Committee for the development of the derivatives market in India, emphasizing the potential benefits of well-functioning derivatives for enhancing market efficiency.