Understanding the Demand

Function

•The demand function represents the mathematical relationship

between the quantity demanded of a product and its

determinants, such as price, income, prices of related goods, and

consumer preferences. It is typically expressed as:

• Q = f(P, Y, PR, T, O)

• Q: Quantity demanded of the product

• P: Price of the product

• Y: Consumer income

• PR: Prices of related goods (substitutes and complements)

• T: Tastes and preferences of consumers

• O: Other factors influencing demand (e.g., demographics,

advertising)

3.

Factors Affecting Demand

1.Price: As the price of a product increases, the quantity demanded tends to decrease, assuming other factors

remain constant. This relationship is known as the law of demand.

2. Income: Changes in consumer income affect the demand for different goods. For normal goods, an increase

in income leads to an increase in the quantity demanded, while for inferior goods, the opposite is true.

3. Prices of Related Goods: The prices of substitutes and complements impact the demand for a product. If

the price of a substitute increases, the demand for the product may increase as consumers switch to the

cheaper alternative. Conversely, if the price of a complement increases, the demand for the product may

decrease.

A substitute good is a good that serves the same purpose as another good for consumers.

A complementary good is a good that adds value to another good when they are consumed together.

Pepsi and Coke are a typical example of substitute goods, whereas fries and ketchup may be considered

complements of each other.

4. Tastes and Preferences: Consumer preferences, influenced by factors like trends, advertising, and cultural

influences, play a significant role in shaping demand. Changes in tastes and preferences can lead to shifts in

the demand curve.

5. Other Factors: Various other factors, such as demographics, seasonality, technological advancements, and

government policies, can influence demand. For instance, changes in population demographics may affect the

demand for certain products or services.

4.

Law of Demand

•The law of demand states that the quantity demanded of a

good shows an inverse relationship with the price of a good

when other factors are held constant (cetris peribus). It

means that as the price increases, demand decreases.

• The law of demand is a fundamental principle in

macroeconomics. It is used together with the law of supply

to determine the efficient allocation of resources in an

economy and find the optimal price and quantity of goods.

5.

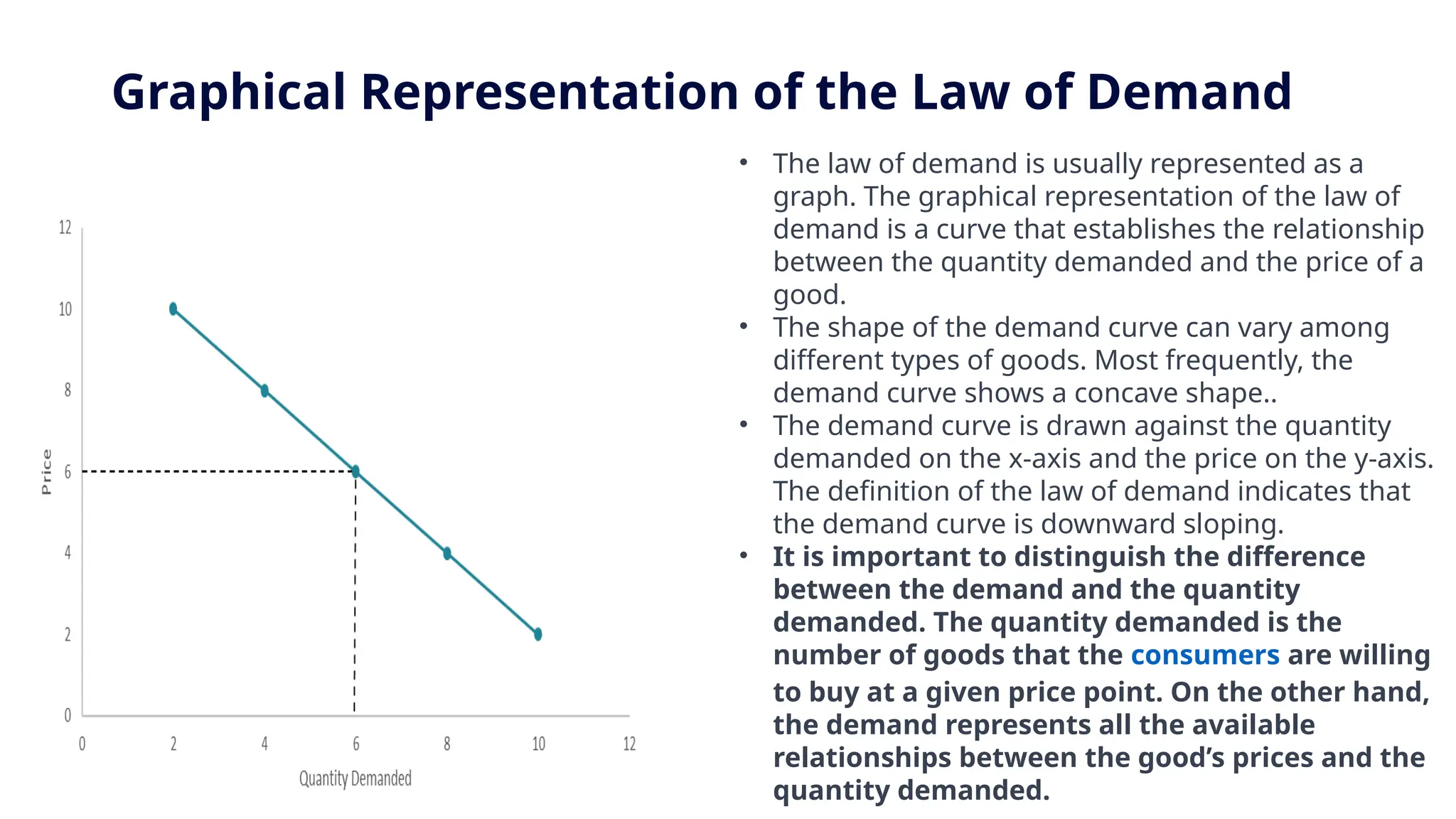

Graphical Representation ofthe Law of Demand

• The law of demand is usually represented as a

graph. The graphical representation of the law of

demand is a curve that establishes the relationship

between the quantity demanded and the price of a

good.

• The shape of the demand curve can vary among

different types of goods. Most frequently, the

demand curve shows a concave shape..

• The demand curve is drawn against the quantity

demanded on the x-axis and the price on the y-axis.

The definition of the law of demand indicates that

the demand curve is downward sloping.

• It is important to distinguish the difference

between the demand and the quantity

demanded. The quantity demanded is the

number of goods that the consumers are willing

to buy at a given price point. On the other hand,

the demand represents all the available

relationships between the good’s prices and the

quantity demanded.

6.

Types of Demand

Demandcan be classified into different types based on various

factors. Here are a few common types of demand:

1.Price Demand: Price demand refers to the quantity of a product

that consumers are willing and able to purchase at different price

levels, holding other factors constant.

2.Income Demand: Income demand refers to the quantity of a

product that consumers are willing and able to purchase at

different income levels, assuming other factors remain the same.

3.Cross Demand: Cross demand refers to the quantity of one

product that is demanded due to a change in the price of

another related product, either as a substitute or a complement.

4.Derived Demand: Derived demand occurs when the demand for

one product is influenced by the demand for another product

that it helps produce. For example, the demand for steel is

derived from the demand for automobiles or construction.

7.

5.Elastic Demand: Elasticdemand refers to a situation where

a change in price leads to a relatively larger change in

quantity demanded. In elastic demand, consumers are highly

responsive to price changes.

6.Inelastic Demand: In contrast to elastic demand, inelastic

demand refers to a situation where a change in price leads to

a relatively smaller change in quantity demanded. In this

case, consumers are less responsive to price changes.

8.

Exceptions to theLaw of Demand

• Unlike the laws of mathematics or physics, the laws of economics are not universal. For example,

the law of demand comes with a few exceptions. Some goods do not show an inverse relationship

between the price and the quantity. Therefore, the demand curve for these goods is upward-

sloping.

1. Giffen goods

• These are inferior goods that lack close substitutes that represent a large portion of the consumer’s

income. Scottish economist Sir Robert Giffen proposed the existence of such goods in the

19th

century. Giffen goods violate the law of demand because the prices of these goods increase

with the increase in the quantity demanded. However, Giffen goods remain mostly a theoretical

concept as there is limited empirical evidence of their existence in the real world.

2. Veblen goods

• Certain types of luxury goods violate the law of demand. Veblen goods are named after American

economist Thorstein Veblen. Generally, they are luxury goods that indicate the economic and social

status of the owner. Therefore, consumers are willing to consume Veblen goods even more when

the price increases. Some examples of Veblen goods include luxury cars, expensive wines, and

designer clothes.

9.

Movement of theDemand Curve

• When there is a change in the quantity demanded of a particular

commodity, because of a change in price, with other factors remaining

constant, there is a movement of the quantity demanded along the

same curve.

• The important aspect to remember is that other factors like the

consumer’s income and tastes along with the prices of other goods, etc.

remain constant and only the price of the commodity changes.

• In such a scenario, the change in price affects the quantity demanded

but the demand follows the same curve as before the price changes. This

is Movement of the Demand Curve. The movement can occur either in an

upward or downward direction along the demand curve.

10.

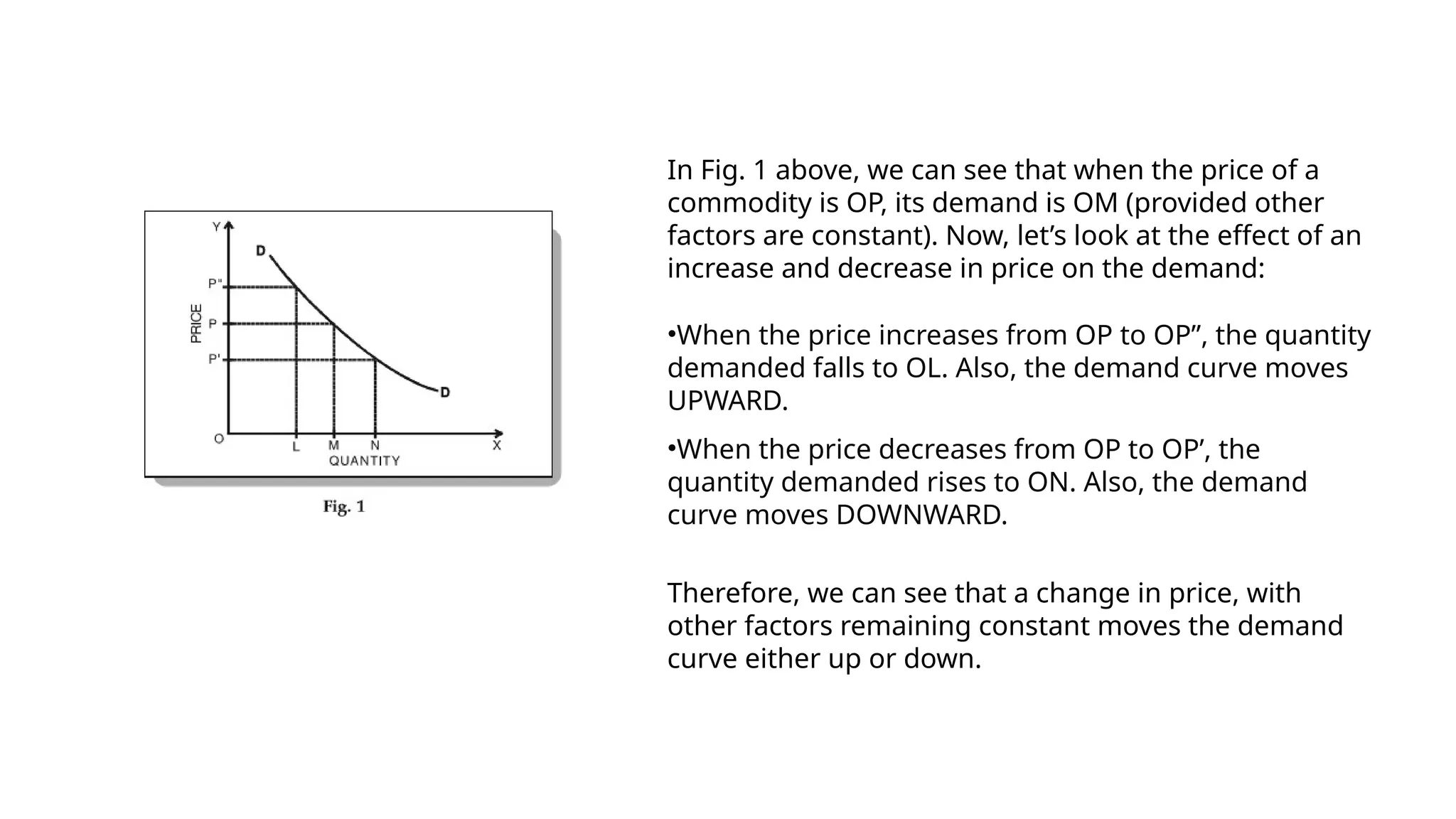

In Fig. 1above, we can see that when the price of a

commodity is OP, its demand is OM (provided other

factors are constant). Now, let’s look at the effect of an

increase and decrease in price on the demand:

•When the price increases from OP to OP”, the quantity

demanded falls to OL. Also, the demand curve moves

UPWARD.

•When the price decreases from OP to OP’, the

quantity demanded rises to ON. Also, the demand

curve moves DOWNWARD.

Therefore, we can see that a change in price, with

other factors remaining constant moves the demand

curve either up or down.

11.

The shift ofthe Demand Curve

• When there is a change in the quantity demanded of a particular

commodity, at each possible price, due to a change in one or more other

factors, the demand curve shifts. The important aspect to remember is

that other factors like the consumer’s income and tastes along with the

prices of other goods, etc., which were expected to remain constant,

changed.

• In such a scenario, the change in price, along with a change in one/more

other factors, affects the quantity demanded. Therefore, the demand

follows a different curve for every price change.

• This is the Shift of the Demand Curve. The demand curve can shift either

to the left or the right, depending on the factors affecting it.

12.

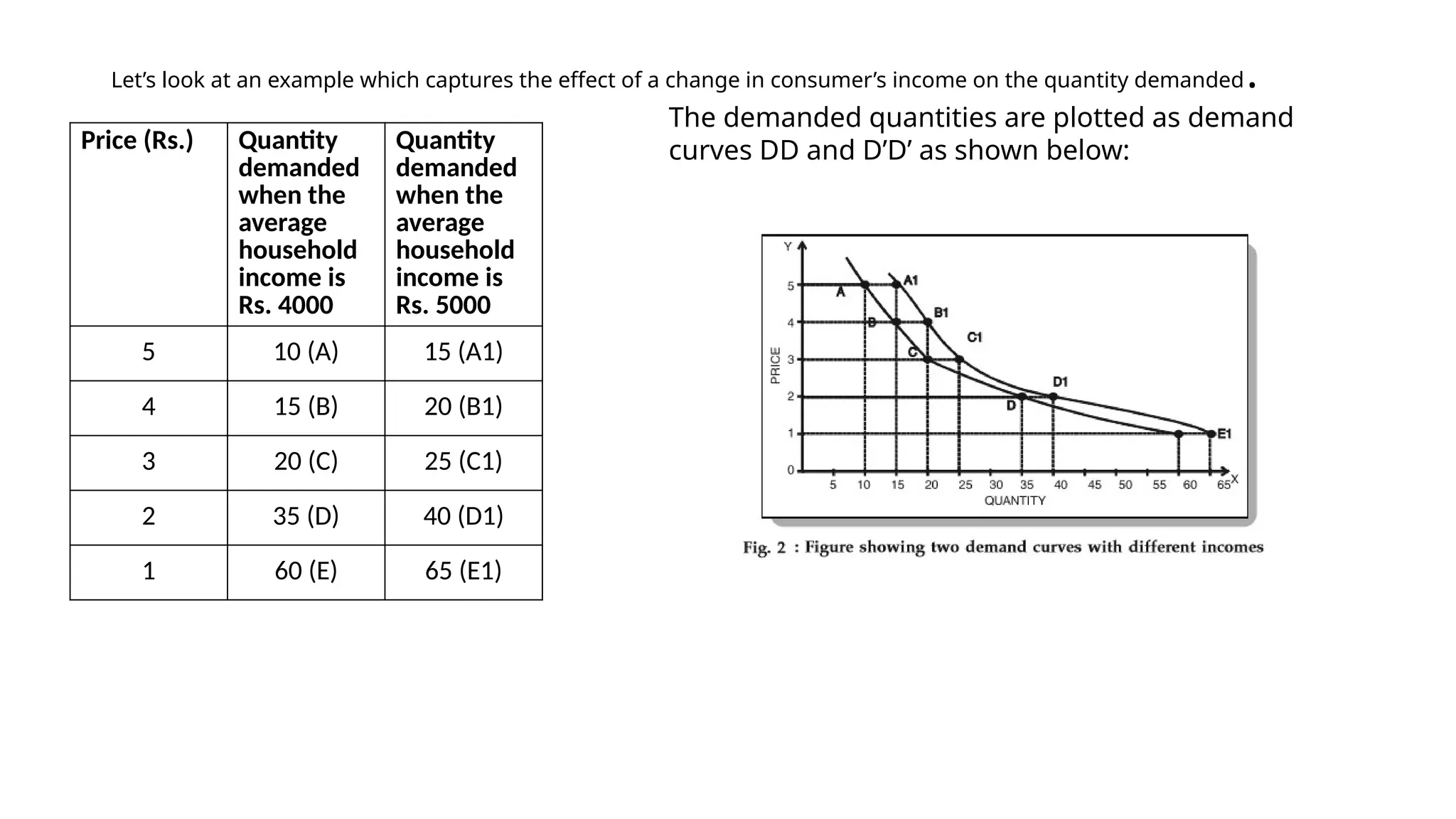

Let’s look atan example which captures the effect of a change in consumer’s income on the quantity demanded.

Price (Rs.) Quantity

demanded

when the

average

household

income is

Rs. 4000

Quantity

demanded

when the

average

household

income is

Rs. 5000

5 10 (A) 15 (A1)

4 15 (B) 20 (B1)

3 20 (C) 25 (C1)

2 35 (D) 40 (D1)

1 60 (E) 65 (E1)

The demanded quantities are plotted as demand

curves DD and D’D’ as shown below:

13.

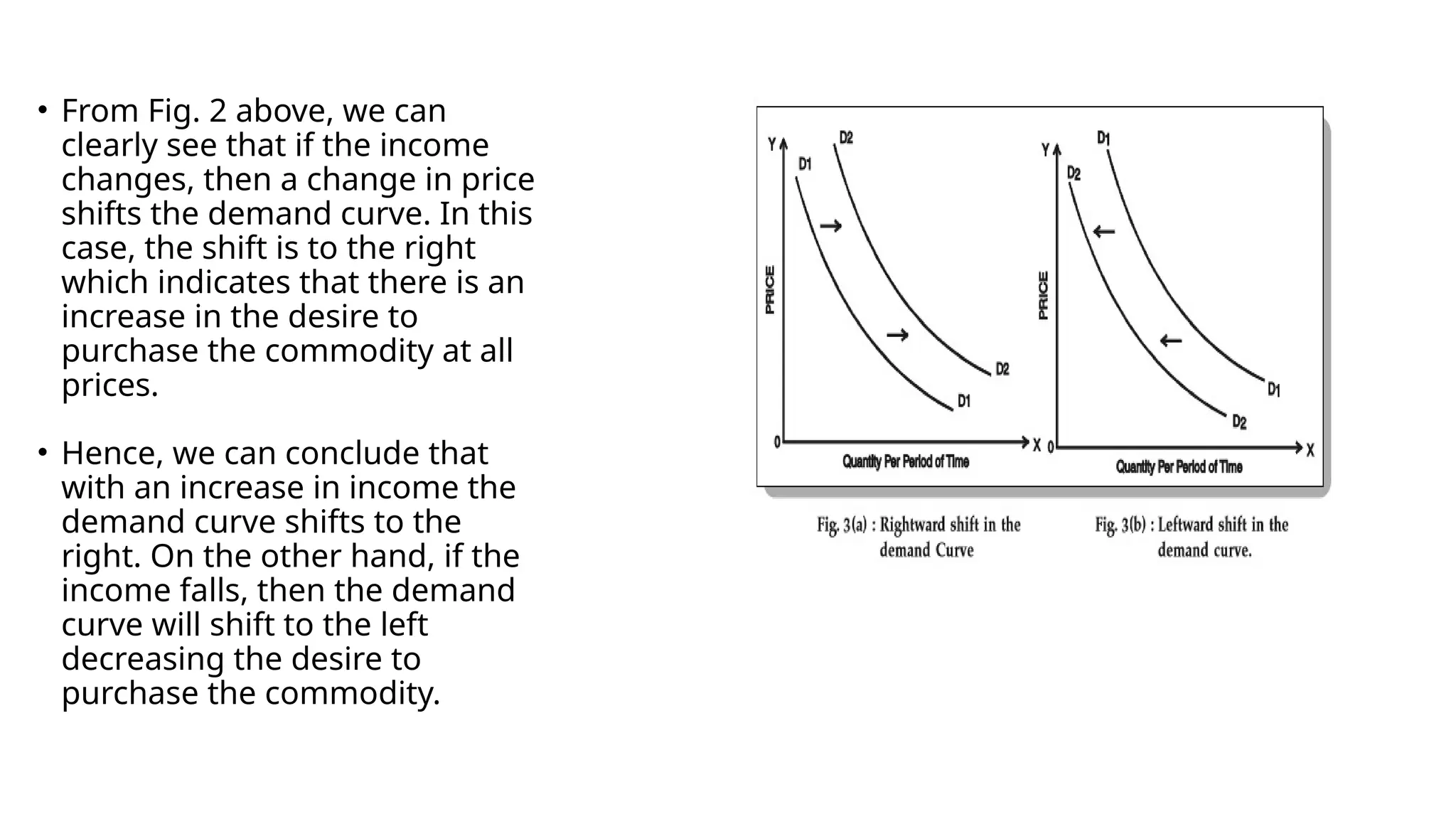

• From Fig.2 above, we can

clearly see that if the income

changes, then a change in price

shifts the demand curve. In this

case, the shift is to the right

which indicates that there is an

increase in the desire to

purchase the commodity at all

prices.

• Hence, we can conclude that

with an increase in income the

demand curve shifts to the

right. On the other hand, if the

income falls, then the demand

curve will shift to the left

decreasing the desire to

purchase the commodity.

14.

Bandwagon Effect &Snob Effect;

• Bandwagon Effect: - The bandwagon effect is a well-documented form of group think in behavioral science

and has many applications. Some of the people purchase commodity not because of necessity but because

their neighbours have bought these goods. It is otherwise called as Band-Wagon effect. These effects have

positive effect on demand. The tendency to follow the actions or beliefs of others can occur because

individuals directly prefer to conform, or because individuals derive information from others. In layman’s

term the bandwagon effect refers to people doing certain things because other people are doing them,

regardless of their ow n beliefs, which they may ignore or override.

For example, people might buy a new electronic item because of its popularity, regardless of whether they need

it, can afford it, or even really want it.

• Snob Effect: - when the commodities are commonly used rich class people decrease the consumption. Or

there are also consumers who like to behave differently from the others. This is known as Snob effect and it

has negative effect on demand. This situation is derived by the desire too have unusual, expensive or unique

goods.

Example - Designer clothing: People may buy designer clothing to signal their wealth and sophistication.

Rare art: People may buy rare works of art to signal their wealth and sophistication.

15.

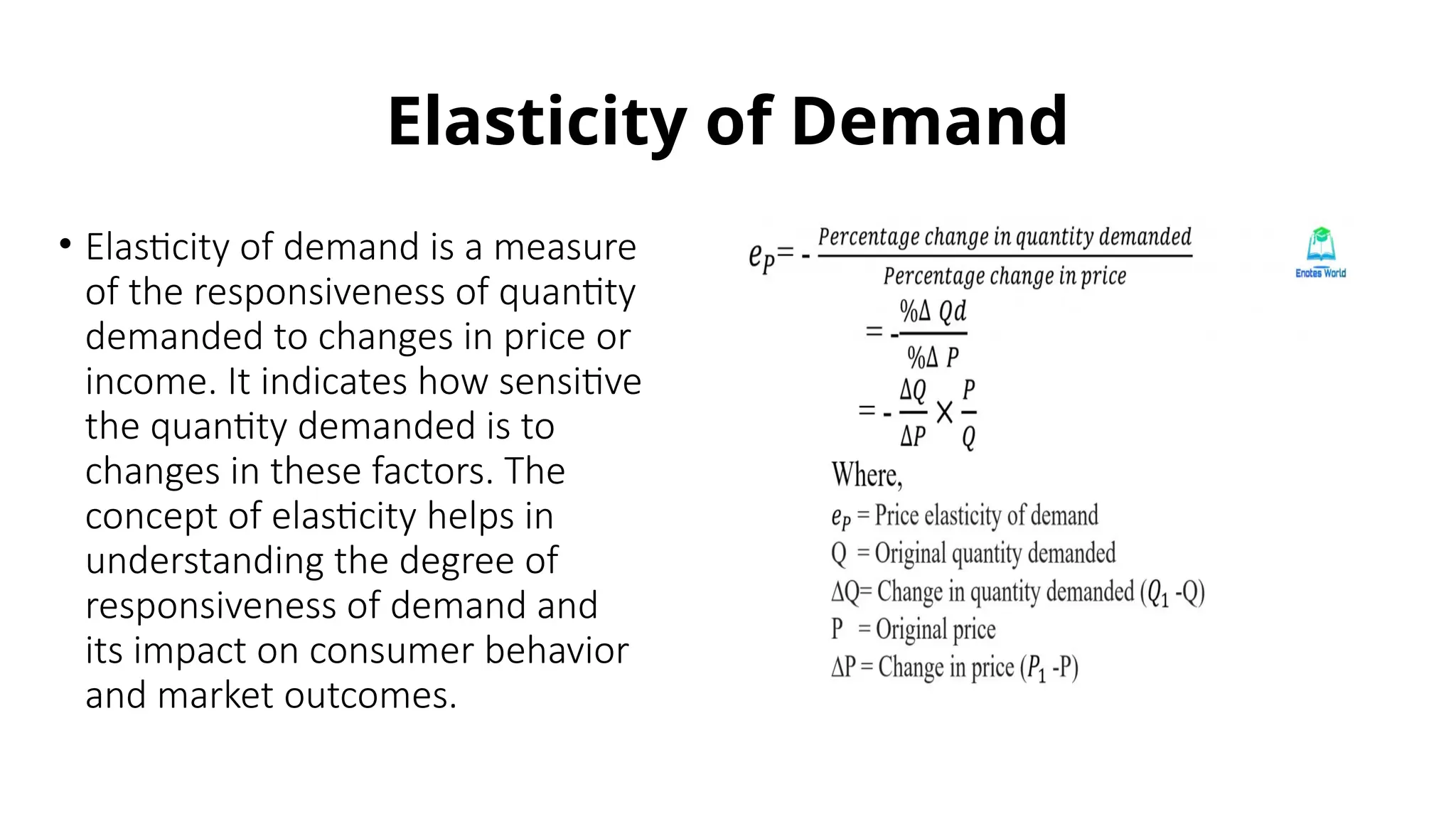

Elasticity of Demand

•Elasticity of demand is a measure

of the responsiveness of quantity

demanded to changes in price or

income. It indicates how sensitive

the quantity demanded is to

changes in these factors. The

concept of elasticity helps in

understanding the degree of

responsiveness of demand and

its impact on consumer behavior

and market outcomes.

16.

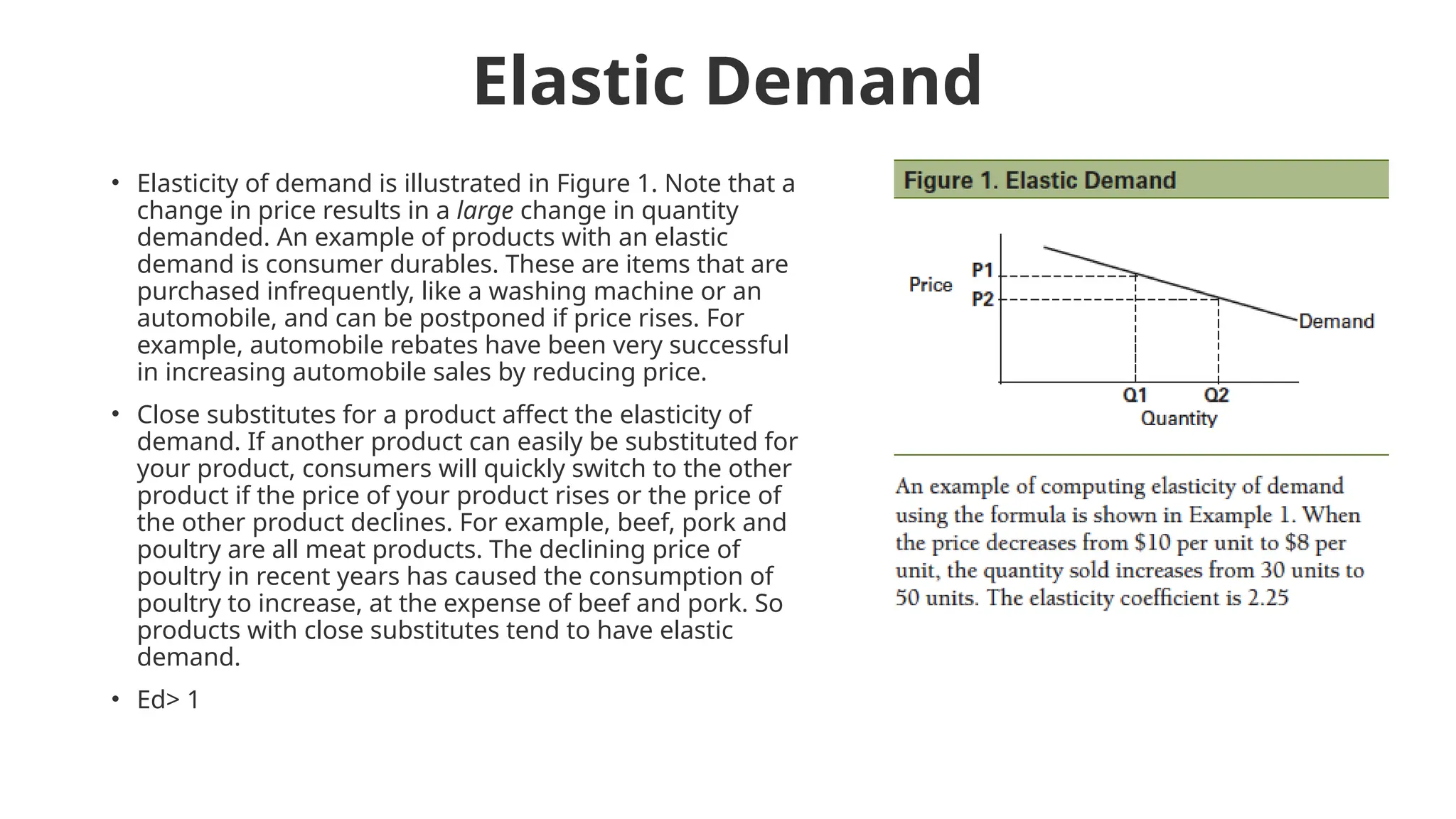

Elastic Demand

• Elasticityof demand is illustrated in Figure 1. Note that a

change in price results in a large change in quantity

demanded. An example of products with an elastic

demand is consumer durables. These are items that are

purchased infrequently, like a washing machine or an

automobile, and can be postponed if price rises. For

example, automobile rebates have been very successful

in increasing automobile sales by reducing price.

• Close substitutes for a product affect the elasticity of

demand. If another product can easily be substituted for

your product, consumers will quickly switch to the other

product if the price of your product rises or the price of

the other product declines. For example, beef, pork and

poultry are all meat products. The declining price of

poultry in recent years has caused the consumption of

poultry to increase, at the expense of beef and pork. So

products with close substitutes tend to have elastic

demand.

• Ed> 1

17.

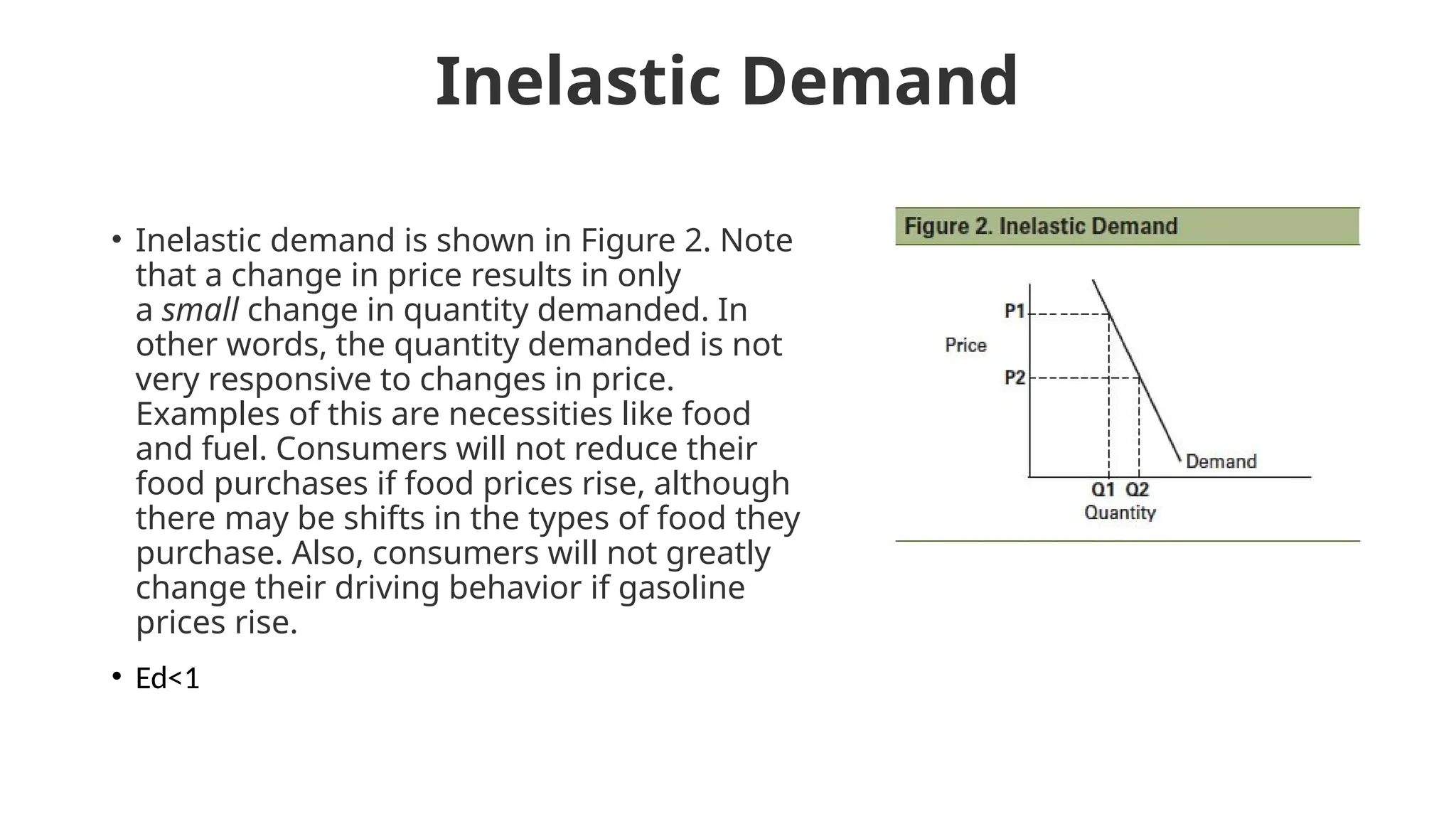

Inelastic Demand

• Inelasticdemand is shown in Figure 2. Note

that a change in price results in only

a small change in quantity demanded. In

other words, the quantity demanded is not

very responsive to changes in price.

Examples of this are necessities like food

and fuel. Consumers will not reduce their

food purchases if food prices rise, although

there may be shifts in the types of food they

purchase. Also, consumers will not greatly

change their driving behavior if gasoline

prices rise.

• Ed<1

18.

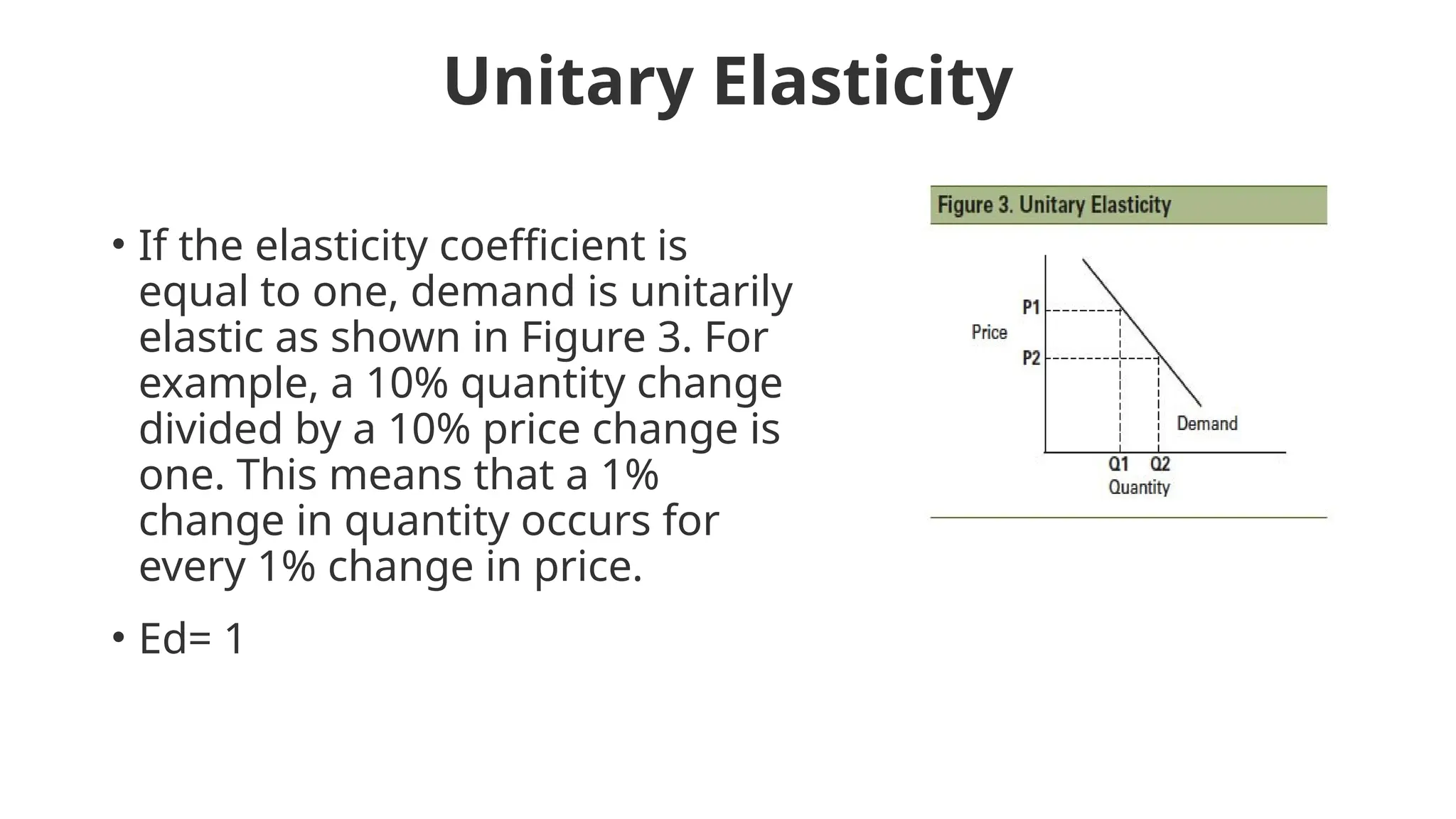

Unitary Elasticity

• Ifthe elasticity coefficient is

equal to one, demand is unitarily

elastic as shown in Figure 3. For

example, a 10% quantity change

divided by a 10% price change is

one. This means that a 1%

change in quantity occurs for

every 1% change in price.

• Ed= 1

19.

Numericals

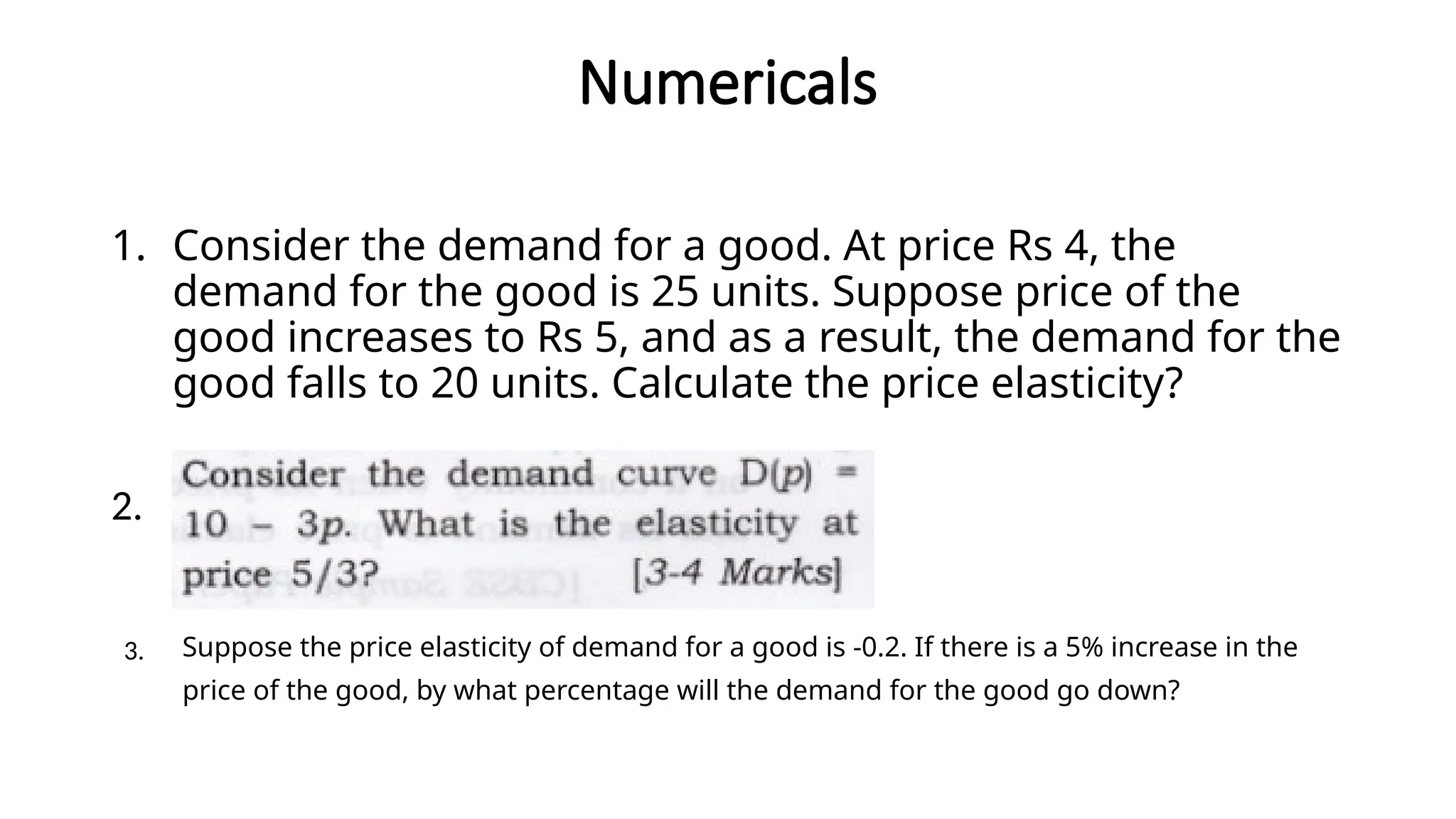

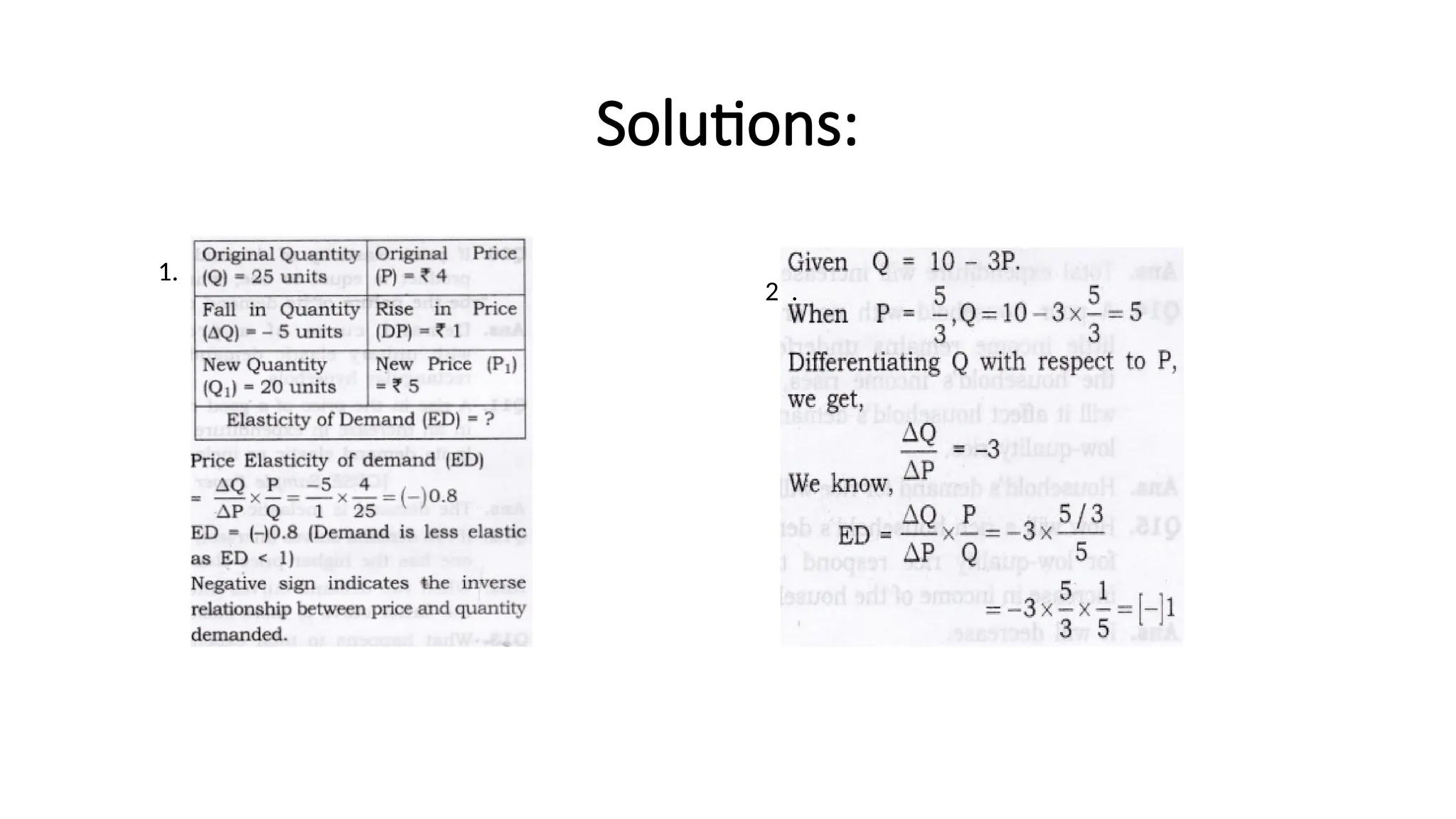

1. Consider thedemand for a good. At price Rs 4, the

demand for the good is 25 units. Suppose price of the

good increases to Rs 5, and as a result, the demand for the

good falls to 20 units. Calculate the price elasticity?

2.

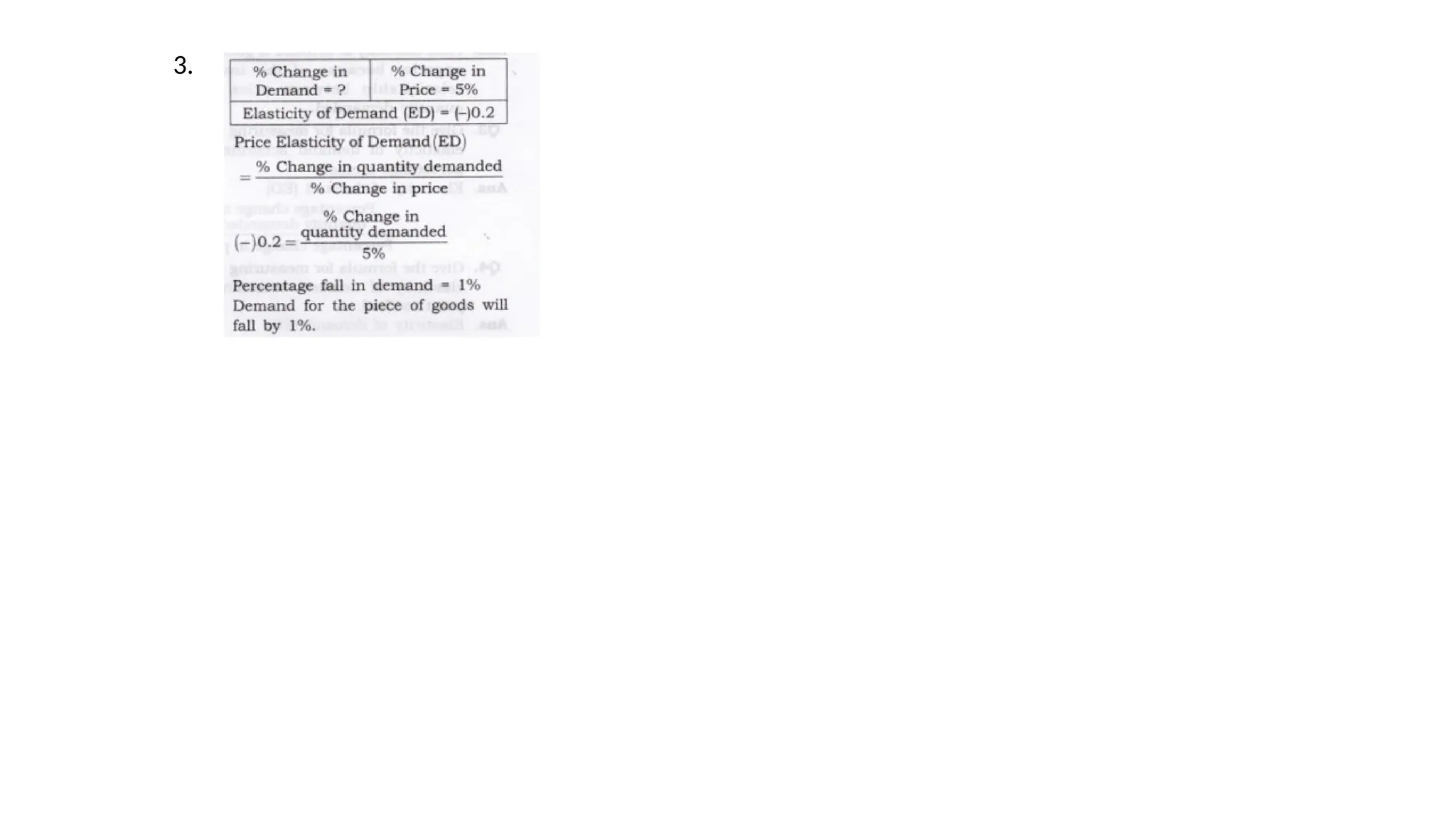

Suppose the price elasticity of demand for a good is -0.2. If there is a 5% increase in the

price of the good, by what percentage will the demand for the good go down?

3.

ESTIMATING DEMAND USINGREGRESSION ANALYSIS

• Estimating demand is a critical aspect of managerial

economics that helps businesses make informed decisions

about pricing, production, and marketing strategies.

Regression analysis is a widely used statistical technique

that allows businesses to estimate demand by analyzing the

relationship between the quantity demanded of a product

and its key determinants.

23.

Estimating Demand UsingRegression Analysis

EstimUnderstanding Regression Analysis

ting Demand Using Regression Analysis

• Regression analysis is a statistical technique that examines the

relationship between a dependent variable and one or more

independent variables. In the context of demand estimation, the

dependent variable is the quantity demanded of a product, while

the independent variables are factors that influence demand, such

as price, income, advertising expenditure, and competitor’s price.

• By analyzing historical data on the quantity demanded and the

corresponding values of the independent variables, regression

analysis allows businesses to quantify the impact of these

variables on demand and develop an equation that can be used to

estimate future demand.

24.

Advantages of DemandEstimation Using Regression

Analysis

1.Quantitative Analysis: Regression analysis provides a quantitative approach to estimating

demand, allowing businesses to obtain numerical estimates of the impact of different

factors on demand. This helps in making more precise and data-driven decisions.

2.Identification of Key Determinants: Regression analysis helps identify the key

determinants of demand by examining the relationship between the dependent variable

(quantity demanded) and the independent variables (factors affecting demand). This

understanding allows businesses to focus their efforts on the most influential factors when

developing strategies.

3.Forecasting: Once the demand equation is established using regression analysis,

businesses can utilize it for demand forecasting. By inputting values of the independent

variables into the equation, they can estimate the quantity demanded under different

scenarios, aiding in production planning, resource allocation, and inventory management.

4.Sensitivity Analysis: Regression analysis enables businesses to conduct sensitivity analysis

by assessing the responsiveness of demand to changes in independent variables. This

information helps in understanding the elasticity of demand and the potential impact of

pricing, advertising, or other strategic decisions on quantity demanded.

25.

Steps in ConductingDemand

Estimation Using Regression

Analysis

1.Data Collection: Gather historical data on the quantity demanded

and relevant independent variables, such as price, income,

advertising expenditure, and competitor’s price. Ensure that an

adequate amount of data is collected to capture variations in the

variables over time.

2.Specification of the Regression Equation: Based on economic

theory and knowledge of the industry, determine the form of the

regression equation. For example, if price is expected to have a linear

relationship with quantity demanded, the equation might take the

form: Quantity Demanded = β0 + β1 * Price + ε, where β0 and β1 are

the coefficients to be estimated, and ε is the error term.

26.

3. Estimation ofCoefficients: Use statistical software or

tools to estimate the coefficients of the regression equation.

The estimation process involves minimizing the sum of

squared differences between the observed quantity

demanded and the values predicted by the equation.

4. Interpretation of Coefficients: Interpret the estimated

coefficients to understand the impact of each independent

variable on demand. Positive coefficients indicate a positive

relationship with demand, while negative coefficients indicate

an inverse relationship.

5.Utilization and Analysis: Once the demand equation is

validated, utilize it to estimate demand under different

scenarios, conduct sensitivity analysis, and support decision-

making processes related to pricing, production, and

marketing strategies.

27.

Demand forecasting

• Demandforecasting is a critical aspect of managerial

economics that helps businesses estimate future consumer

demand for their products or services. Accurate demand

forecasting enables businesses to make informed decisions

about production planning, inventory management, pricing

strategies, and resource allocation. In this , we will explore

some commonly used demand forecasting techniques and

their application in business.

28.

Time Series Analysis

•Time series analysis is a widely used technique for demand forecasting, especially when

historical data is available. It involves analyzing past demand patterns to identify

trends, seasonality, and other recurring patterns that can be used to make future

predictions. Time series analysis techniques include:

1.Moving Averages: Moving averages calculate the average demand over a specified

period, smoothing out short-term fluctuations. Simple moving averages use a fixed

time period, while weighted moving averages assign different weights to each data

point based on their significance.

2.Exponential Smoothing: Exponential smoothing assigns exponentially declining

weights to past demand observations, giving more weight to recent data. This

technique is useful for capturing short-term changes in demand.

3.ARIMA Models: ARIMA (Auto Regressive Integrated Moving Average) models combine

autoregressive (This component represents the relationship between the current value and past

values) and moving average components to model and forecast time series data. They

can capture trends, seasonality, and irregularities in demand patterns.

29.

Causal Methods

• Causalmethods focus on identifying cause-and-effect relationships between

demand and related factors such as price, income, advertising expenditure, or

competitor’s actions. These methods use historical data on both the

dependent variable (demand) and the independent variables (factors

influencing demand). Common causal methods include:

1.Regression Analysis: Regression analysis estimates the relationship between

the dependent variable (demand) and one or more independent variables. By

analyzing historical data, businesses can identify the factors that significantly

affect demand and develop a regression equation for forecasting.

2.Econometric Models: Econometric models use statistical techniques to

estimate demand by incorporating economic variables, market dynamics, and

consumer behavior. These models can be complex and involve multiple

equations to capture the relationships among various factors.

30.

Judgmental Methods

• Judgmentalmethods rely on expert opinions, market surveys, or qualitative assessments

to forecast demand. These methods are useful when historical data is limited or when

demand is influenced by factors that are difficult to quantify. Some judgmental methods

include:

1.Market Research Surveys: Market research surveys collect data directly from

consumers, allowing businesses to gather insights into their preferences, intentions, and

buying behavior. These surveys can provide valuable information for demand forecasting.

2.Delphi Method: The Delphi method involves collecting opinions from a panel of experts

anonymously and iteratively. The experts’ responses are aggregated and shared with the

group, leading to a convergence of opinions over multiple rounds. This iterative process

helps to achieve a consensus forecast.

3.Sales Force Composite: Sales force composite involves soliciting input from the sales

team based on their knowledge of the market and customer interactions. The sales team

provides their own estimates of future demand, which are aggregated to create a

forecast.

31.

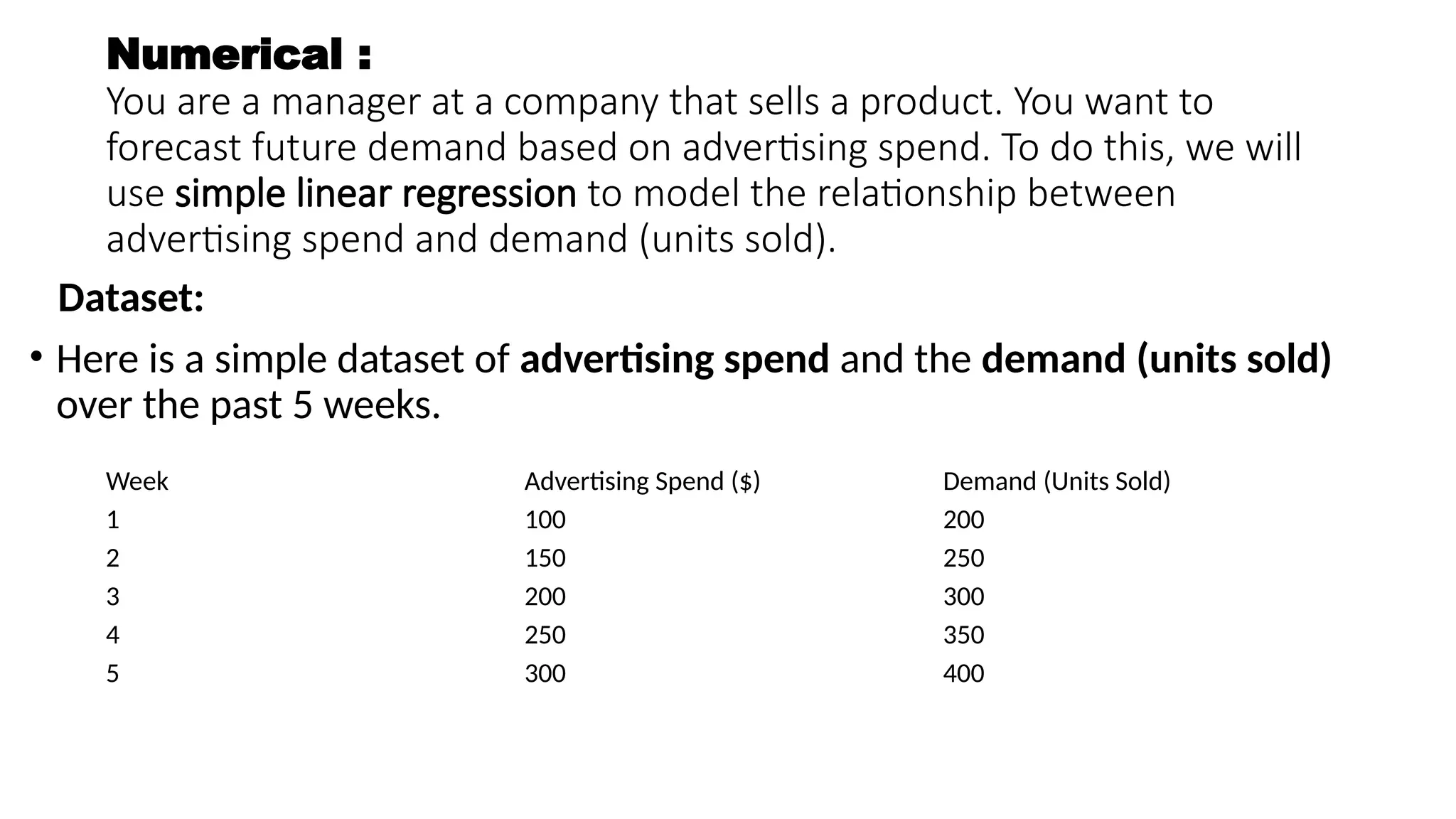

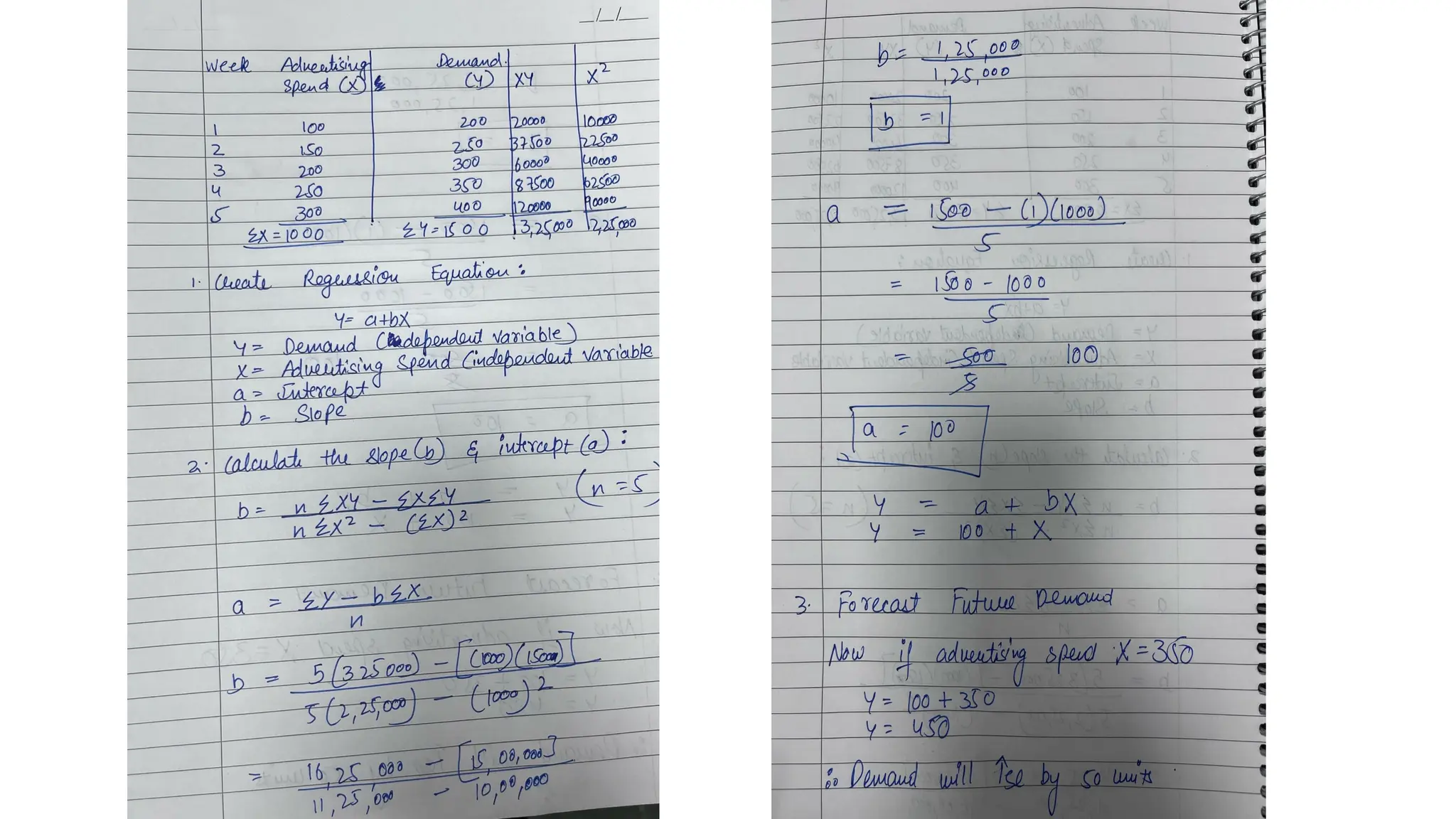

Numerical :

You area manager at a company that sells a product. You want to

forecast future demand based on advertising spend. To do this, we will

use simple linear regression to model the relationship between

advertising spend and demand (units sold).

Dataset:

• Here is a simple dataset of advertising spend and the demand (units sold)

over the past 5 weeks.

Week Advertising Spend ($) Demand (Units Sold)

1 100 200

2 150 250

3 200 300

4 250 350

5 300 400

33.

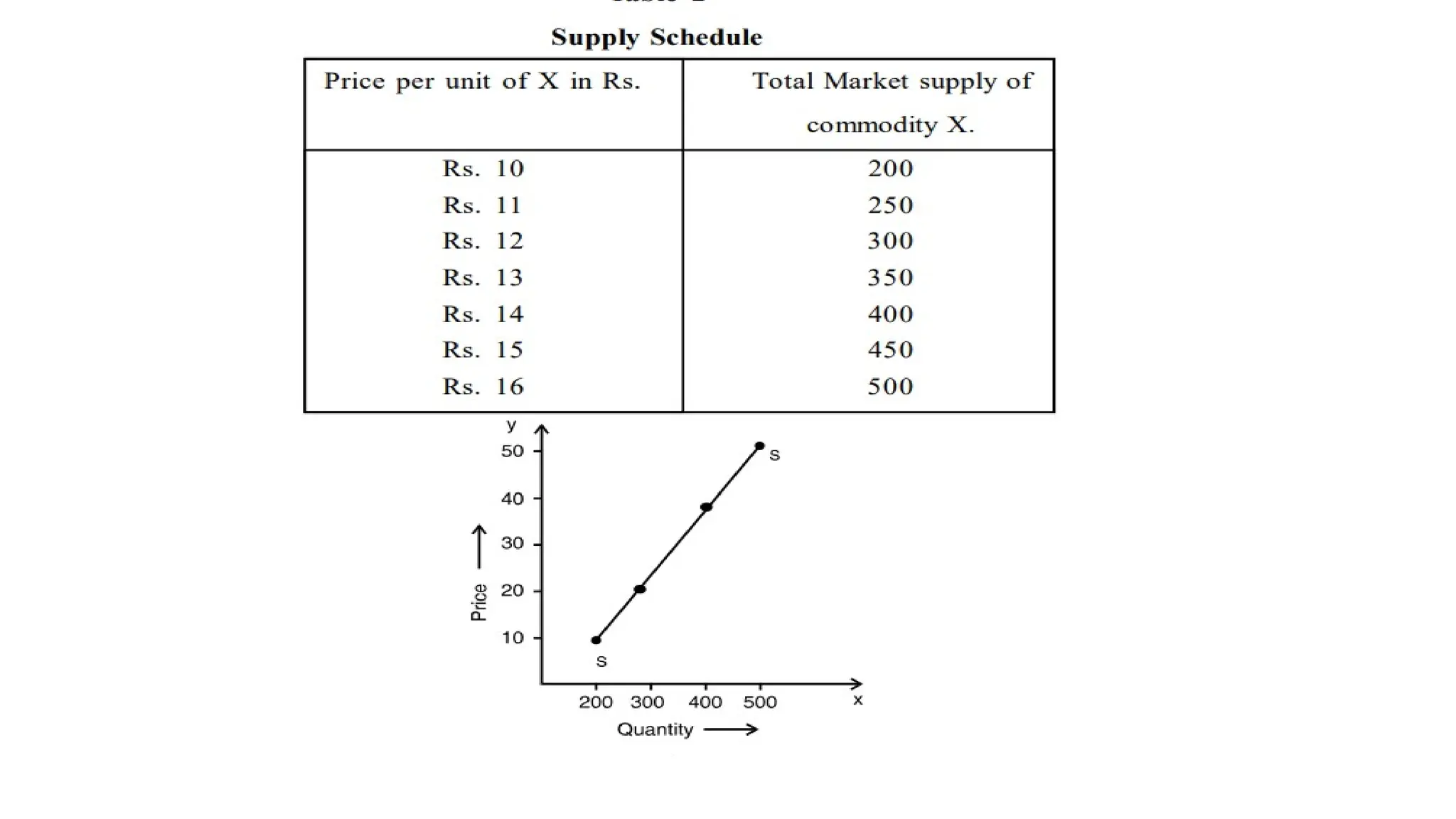

MEANING OF SUPPLY

Supplymeans the quantity offered for sale by producers at a particular

price.

Two important points are :– (i) Supply refers to what producers offer for

sale at a given price and

(ii) Supply is a flow concept. The quantity supplied is so much per unit

of time, per day, per week, per month or per year.

34.

Determinants of Supply

I.Price of the good : Ceteris Paribus, the higher price of a good the greater the quantity of

it that will be produced and offered for sale.

II. Production technology : The supply of a particular commodity depends upon the state

of technology and changes in it. As technology progresses, it becomes possible to produce

commodities more cheaply.

III. Prices of factors : Another important factor which influences the supply of a

commodity is cost of inputs i.e prices of factors of production. Decrease in the prices of

these inputs makes it possible to produce commodities more cheaply.

IV. Prices of other commodities : The supply of a commodity depends not only on the

prices of the concerned commodity but also on the prices of other commodities. If the

price of a substitute goes up, firms will be tempted to divert their resources to the

production of that substitute. If price of a complementary product goes up, the supply of

the product in question also rises.

35.

V. Objectives ofthe firm : Some firms want to maximise their profits. For that

they will produce and supply that much quantity which fetches maximum profits

to them. Some other firms may believe in lower margin and high sales turnover.

VI. Number of producers : If the number of firms is more, output also increases.

VII. Time : Supply is a function of time also. In the long run, it becomes possible

to overcome some constraints.

VIII. Govt. Policy : The govt. may levy taxes in the form of excise duty or sales tax

or import duty, or may grant subsidies. If tax is levied on a product, its cost of

production will go up and the quantity supplied will go down. Subsidies on the

other hand, reduce the cost of production and thus encourages the producers to

produce and sell more.

IX. Future price expectations : During inflation, sellers normally expect the

prices to rise further. Therefore, they will tend to hoard the commodity. This will

reduce supply and will cause its price to rise further.

36.

LAW OF SUPPLY

Thelaw of supply explains the functional relationship between price

and quantity supplied According to this law, ceteris paribus, an increase

in price of a commodity causes an increase in its quantity supplied and

a decrease in its price causes its quantity supplied to fall. Thus, we find

a positive relationship between price and quantity supplied. It is based

on the fact that higher profits provide the producers an incentive to

produce more.

The law of supply can be explained through supply schedule and supply

curve given below :

38.

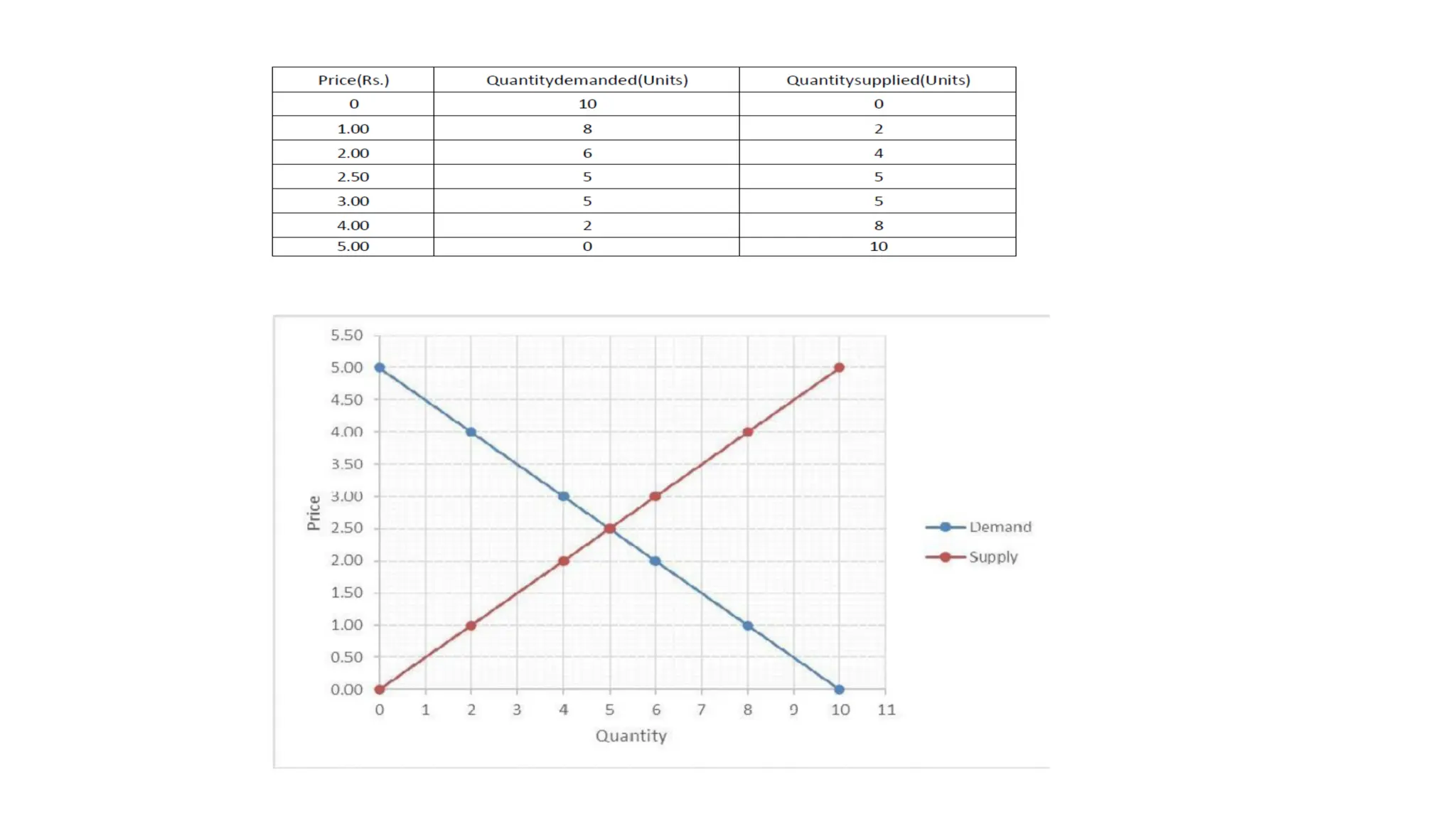

MARKET EQUILIBRIUM

• Marketequilibrium refers to a situation where quantity demanded for a commodity is equals to quantity

supplied. We have seen that the demand and supply of any product depend on its price. The equilibrium price

is that price at which the total demand for any product in the market is equal to the total supply of that

product.

• The market demand curve gives us an idea of the total quantity demanded by all the buyers in the market at

different price levels. In the same way, each seller takes the price as given and decides to offer a certain

quantity for sale in the market. Thus, each seller has a n individual supply curve and by summing up the

individual supply curves of all the sellers in the market, we get the market supply curve. From the market

supply curve we get to know the total supply by all sellers at different prices.

40.

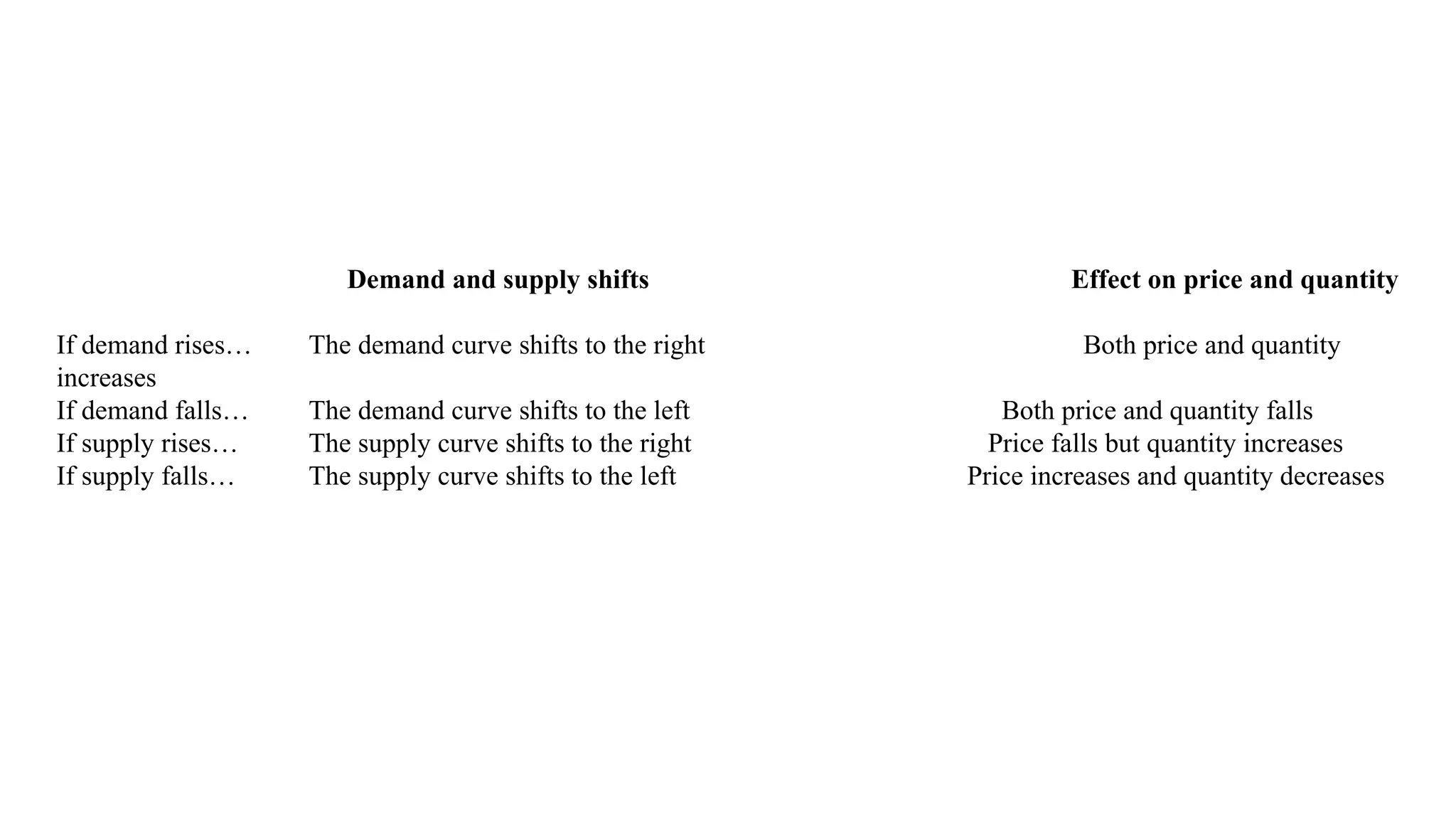

Demand and supplyshifts Effect on price and quantity

If demand rises… The demand curve shifts to the right Both price and quantity

increases

If demand falls… The demand curve shifts to the left Both price and quantity falls

If supply rises… The supply curve shifts to the right Price falls but quantity increases

If supply falls… The supply curve shifts to the left Price increases and quantity decreases

41.

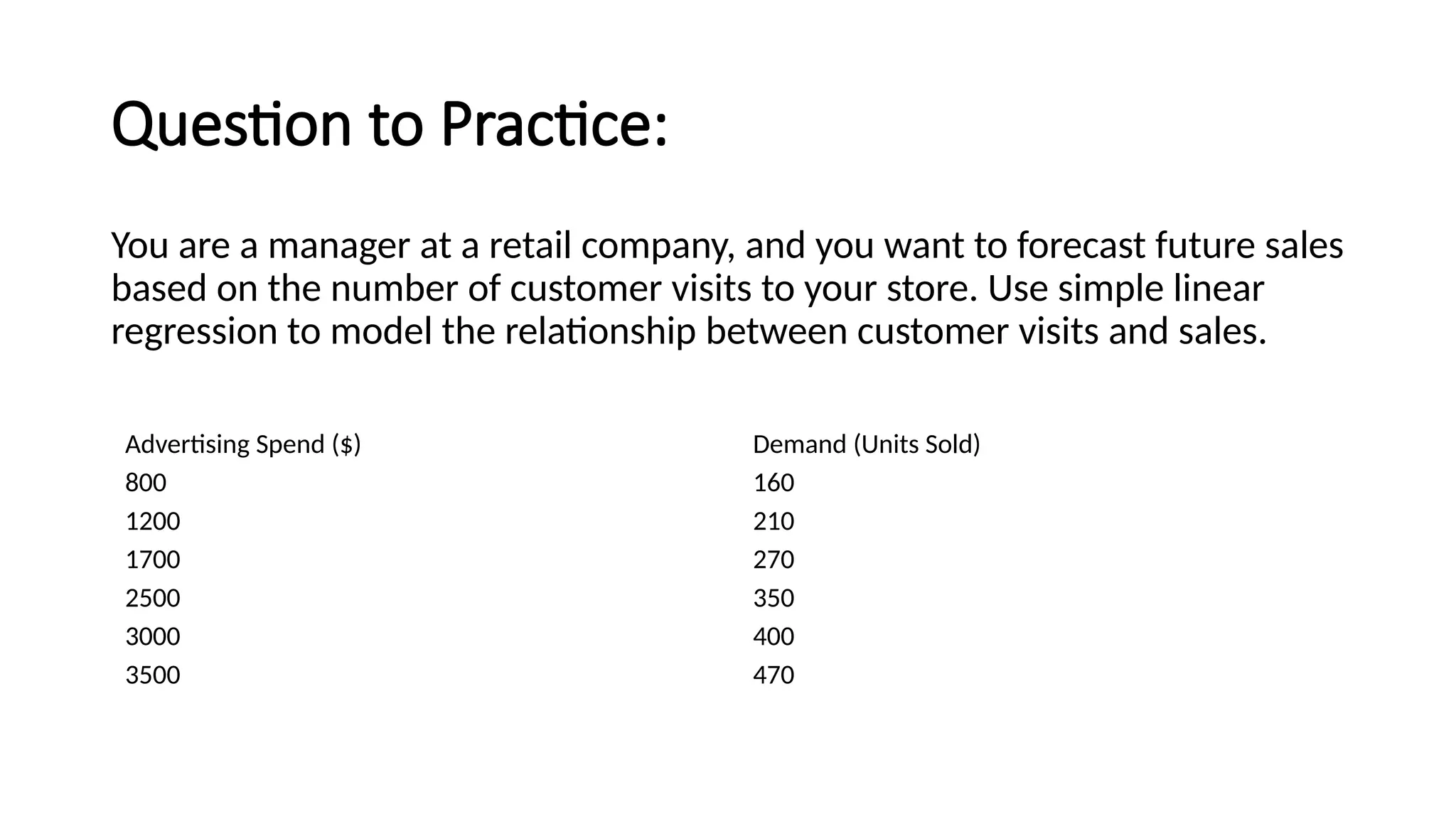

Question to Practice:

Youare a manager at a retail company, and you want to forecast future sales

based on the number of customer visits to your store. Use simple linear

regression to model the relationship between customer visits and sales.

Advertising Spend ($) Demand (Units Sold)

800 160

1200 210

1700 270

2500 350

3000 400

3500 470