The document is a South Carolina tax form for deferring income taxes on increases in foreign trading receipts. Taxpayers can defer taxes on the portion of income attributable to increases in foreign sales over a three year average. To defer taxes, taxpayers must pay annual interest on the deferred tax amount. The deferred tax is due no later than the fifth year after it was first deferred.

Income Tax Basics by Burnie Maybank, South Carolina Economic Development 101,...Nexsen Pruet

Burnie Maybank hosted the Nexsen Pruet Newbie Seminar on December 1, 2011. The Newbie Seminar is designed for those new to the economic development field in South Carolina or those who would like some brushing up. Covered topics included basic property, sales and income taxes, as well as Bonds, the utility tax credit and FOIA.

Income Tax Basics by Burnie Maybank, South Carolina Economic Development 101,...Nexsen Pruet

Burnie Maybank hosted the Nexsen Pruet Newbie Seminar on December 1, 2011. The Newbie Seminar is designed for those new to the economic development field in South Carolina or those who would like some brushing up. Covered topics included basic property, sales and income taxes, as well as Bonds, the utility tax credit and FOIA.

International tax reporting requirements relevant to U.S. persons engaged in cross-border transactions. Foreign information returns discussed include Forms 926, 5471, 5472, 8858, and 8865. The discussion focuses upon proper execution of the Forms and potential penalties for noncompliance.

View the video recording here: https://youtu.be/UyNXjUoFxYA

Learn more about Citrin Cooperman's International Tax Services here: http://bit.ly/2veYkrO

Speeding Through 2020 Auto Webinar Series - Year-End ReviewCitrin Cooperman

As 2020 nears completion, we discuss what automotive dealerships need to record and what files need to be kept in order to ensure that 2020 is closed properly and that the new year starts off right.

US Expatriate Tax Presentation given in Puerto Vallarta and Melaque Mexico for Americans living there concerning filing FBAR forms, form 8938 and other required IRS foreign reporting forms by Don D. Nelson, Attorney, CPA. His website at www.taxmeless.com has a wealth of additional information

The Department of Treasury issued additional guidance on FATCA compliance including final versions of various disclosure forms, statement of specified foreign financial assets, and new regulations for foreign financial institutions - O'Connor Davies - New York CPA Firm, New York City

US Expat Taxes Explained is a summary overview of our new series about US Expatriate Tax Returns and have the components work. By Greenback Expat Tax Services

International tax reporting requirements relevant to U.S. persons engaged in cross-border transactions. Foreign information returns discussed include Forms 926, 5471, 5472, 8858, and 8865. The discussion focuses upon proper execution of the Forms and potential penalties for noncompliance.

View the video recording here: https://youtu.be/UyNXjUoFxYA

Learn more about Citrin Cooperman's International Tax Services here: http://bit.ly/2veYkrO

Speeding Through 2020 Auto Webinar Series - Year-End ReviewCitrin Cooperman

As 2020 nears completion, we discuss what automotive dealerships need to record and what files need to be kept in order to ensure that 2020 is closed properly and that the new year starts off right.

US Expatriate Tax Presentation given in Puerto Vallarta and Melaque Mexico for Americans living there concerning filing FBAR forms, form 8938 and other required IRS foreign reporting forms by Don D. Nelson, Attorney, CPA. His website at www.taxmeless.com has a wealth of additional information

The Department of Treasury issued additional guidance on FATCA compliance including final versions of various disclosure forms, statement of specified foreign financial assets, and new regulations for foreign financial institutions - O'Connor Davies - New York CPA Firm, New York City

US Expat Taxes Explained is a summary overview of our new series about US Expatriate Tax Returns and have the components work. By Greenback Expat Tax Services

CTP’s Threat Update series is a weekly update and assessment of Iran and the al Qaeda network. CTP’s Iran team follows developments on the internal politics, nuclear negotiations, and regional conflicts closely. The al Qaeda network update includes detailed assessments of al Qaeda’s affiliates in Yemen, the Horn of Africa, and the Maghreb and Sahel.

Below are the top three takeaways from the week:

1. Pro-ISIS groups are expanding operations into eastern Yemen, where AQAP has traditionally had a dominant naval presence.

2. IRGC naval forces detained the Maersk Tigris in the Strait of Hormuz on April 28 based on a lawsuit filed by Iranian oil company Pars Talaei against Danish shipping group Maersk.

3. Rebel violence is increasing in northen Mali as Tuareg rebels attacked a town near the Mauritanian border.

Sample Company Profile at www.formsbirds.com/company-profile-sampleAnne Thornshberry

A company profile is a professional introduction of the business and aims to inform the audience about its products and services. It can be used as a marketing tool, to attract investors and clients who might be interested in the product or service provided by the company. Usually, a company profile includes several items, such as a firm’s history, number and quality of its human, physical resource, management structures, goods or services, reputation as well as its past, current and anticipated performance etc.. Writing a concise, creative and attention-grabbing corporate profile is very important. Sample company profile formats or company profile templates listed below will give you inspirations. With these company profile sample templates, you will make a perfect company profile quickly.

Meet more Company Profile Samples at http://www.formsbirds.com/company-profile-sample

Concepts coveredFINAL EXAM - Part IOutline of Topics coveredTopicW.docxmaxinesmith73660

Concepts coveredFINAL EXAM - Part IOutline of Topics coveredTopicWeek CoveredPerm Ms1, 2Temp Ms1, 2AMT3Tax Credits3Valuation Allowance3 (lesson 2)State Blended Rate4Interim Financial reporting5FIN 486, 7True-up9FS Disclosures8, 9Foreign - APB 2311, 12Stock Options13, 14

INDEXDELTA Corporation & SubsidiaryFINAL EXAM Part 1INDEX to workpaperstab #Tab DescriptionQQuestions to be answeredYellow tab - Facts providedFDELTA Corporation FactsFADelta Fixed Asset RollforwardFCFoxtrot Corporation FactsI2009 Interim ScheduleCDelta Current ProvisionPDelta 2011 Provision-to-Return scheduleDDelta Deferred Rollforward scheduleTATax Account Rollforward scheduleRRate ReconciliationFS2012 Consolidated Income Tax Footnote disclosure

&A

&Z&F

Printed on: &D &T

Q - Questions to be answeredDELTA Corporation & SubsidiaryFINAL EXAM Part 1TasksConsidering the facts outlined on tab "F" determine the following -1For 2009 only - determine the interim tax expense by completing the schedule on tab IConsider only pre-tax income, perms and credits from facts tab. Assume no VA recorded for this portion of the exercise.2Prepare a current provision and deferred rollforward schedule for each of the years 2009 through 2012.see example for 2009 at tabs C and D3Compute the 2011 provision-to-return JE and post as part of the 2012 provision - use the template on tab P as a guide4Complete the Tax Account Analysis schedule tab TA for each year 2009 to 2012.Note - actual taxes paid are reflected on this tab5Complete a Rate Reconciliation schedule tab R for each year 2009 to 2012.see example for 20096Prepare a current and deferred tax provision for Foxtrot Corporation for the year 2012 (in FC and RC). - see facts at tab FC and complete the yellow highlighted cells in the trial balance.7For 2012 only - create the Consolidated Income Tax footnotes (with 2011 comparison) (i.e., Delta + Foxtrot). - use the templates on tab FS as a guidePlease show all your work (to provide for maximum credit).Feel free to add columns, rows, & worksheets as necessary to complete the above tasksPlease reference your workpapers to make the review easier.Note - there are hidden columns on tabs C, D, and P that you may want to use

&A

&Z&F

Printed on: &D &T

F - Delta FactsDELTA CorporationFACTSlinkDELTA is a "C" corporation (SEC registrant) operating entirely within the U.S. on the basis of a calendar year end. Delta was formed 1/1/2009.Year 2009Year 2010Year 2011Year 2012per returnper returnper provisionper return (only if different)per provisionFederal Tax Rate35%35%35%35%States - 100% NV - 0% rate100% NV - 0% rate100% OR @ 7.6% flat tax rate80% OR @ 7.6% rate20% IL @ 7.00% flat tax rateAssume no fed/state differences other than state tax deduction which is not deductible for state tax purposes.Assume states do not have an AMT tax concept.Assume headquarters moved from Reno Nevada to Portland Oregon on 1/1/2011. Assume began operations in Illinois on 1/1/2012. [Hint - Prior YE deferred tax balance sho.

Form 1040Form 1040 Department of the Treasury Internal Revenue Ser.docxhanneloremccaffery

Form 1040Form 1040 Department of the Treasury Internal Revenue Service2013U.S. Individual Tax FormOMB No.1545-0074IRS Use Only--Do not write or staple in this spaceFor the year Jan.1--Dec. 31,2013, or any other tax year beginning,2013,,20See Separate InstructionsYour first name and initialLast nameSocial Security NumberIf a joint return, spouses first name and initialLast nameSpouse Social Security NumberHome address( number and street). If you have a P.O. Box, see instructionsMake Sure that the SSN(s) above and on line 6c are correct.City, town, or post office, state, and zip code. If you have a foreign address, also complete spaces below (see instructions).Presidential Election CampaignCheck here if you, or your spouse if filing jointly,Foreign country nameForeign province/state/countryForeign postal codechecking this box below will not change your taxrefund.youspouseFiling Status1. Single4.Head of Household (with qualifying person.) (See instructions.) IfCheck only one box2.. married filing jointlythe qualifying person is a child but not your dependent, enter this3. Married filing separately. Enter spouse's SSN abovechild's name hereand full name here.5. Qualifying Window(er) with dependent childExemptions6a Yourself. If someone can claim you as a dependent, do not check box 6a]Boxes checkedb spouse]on 6a and 6bIf more than fourc. Dependentsdependents, see(1) First nameLast name(2) dependents(3) dependents (4) check if child under age 17No. of childreninstructions and social security numberrelationship to youqualifying for tax credit seeon 6c who:check hereinstructions.lived with youdid not live with youdue to divorce orseparation(see instructions)Dependents on6c not entered aboved. Total number of Exemptions ClaimedAdd numbers on lines aboveIncome7Wages, salaries, tips, etc. Attach Forms (W-2)78aTaxable interest. Attach Schedule B if required8aAttach Form(s)bTax-exempt interest. Do not include on line 8a8bW-2 here. Also9aOrdinary dividends. Attach Schedule B if required9aattach Forms(s) bQualified dividends9bW-2 and 1099-R10Taxable refunds, credits, or offsets state or local income taxes10if tax was withheld.11Alimony received1112Business income or (loss). Attach Schedule C or C-EZ12If you did not 13Capital gain or (loss). Attach Schedule D if required. If not required, check here13get a W-2,14other gains or (losses). Attach Form 479714see instructions15aIRA distributions15ab Taxable amount15b16aPensions and annuities16ab Taxable amount16b17Rental real estate, royalties, partnerships, S corporations, trusts, etc. Attach Schedule E1718Farm income or (loss). Attach Schedule F1819Unemployment compensation1920aSocial security benefits20ab Taxable amount20b21other income. List type and amount2122combine the amounts in the far right column for lines 7 through 21. This is your total incomeThis is your total income.22Adjusted 23Educator expenses23Gross24Certain business expenses of reservists, performing artists, and fee-basis government. Atta ...

RMD24 | Debunking the non-endemic revenue myth Marvin Vacquier Droop | First ...BBPMedia1

Marvin neemt je in deze presentatie mee in de voordelen van non-endemic advertising op retail media netwerken. Hij brengt ook de uitdagingen in beeld die de markt op dit moment heeft op het gebied van retail media voor niet-leveranciers.

Retail media wordt gezien als het nieuwe advertising-medium en ook mediabureaus richten massaal retail media-afdelingen op. Merken die niet in de betreffende winkel liggen staan ook nog niet in de rij om op de retail media netwerken te adverteren. Marvin belicht de uitdagingen die er zijn om echt aansluiting te vinden op die markt van non-endemic advertising.

What is the TDS Return Filing Due Date for FY 2024-25.pdfseoforlegalpillers

It is crucial for the taxpayers to understand about the TDS Return Filing Due Date, so that they can fulfill your TDS obligations efficiently. Taxpayers can avoid penalties by sticking to the deadlines and by accurate filing of TDS. Timely filing of TDS will make sure about the availability of tax credits. You can also seek the professional guidance of experts like Legal Pillers for timely filing of the TDS Return.

Affordable Stationery Printing Services in Jaipur | Navpack n PrintNavpack & Print

Looking for professional printing services in Jaipur? Navpack n Print offers high-quality and affordable stationery printing for all your business needs. Stand out with custom stationery designs and fast turnaround times. Contact us today for a quote!

Falcon stands out as a top-tier P2P Invoice Discounting platform in India, bridging esteemed blue-chip companies and eager investors. Our goal is to transform the investment landscape in India by establishing a comprehensive destination for borrowers and investors with diverse profiles and needs, all while minimizing risk. What sets Falcon apart is the elimination of intermediaries such as commercial banks and depository institutions, allowing investors to enjoy higher yields.

LA HUG - Video Testimonials with Chynna Morgan - June 2024Lital Barkan

Have you ever heard that user-generated content or video testimonials can take your brand to the next level? We will explore how you can effectively use video testimonials to leverage and boost your sales, content strategy, and increase your CRM data.🤯

We will dig deeper into:

1. How to capture video testimonials that convert from your audience 🎥

2. How to leverage your testimonials to boost your sales 💲

3. How you can capture more CRM data to understand your audience better through video testimonials. 📊

VAT Registration Outlined In UAE: Benefits and Requirementsuae taxgpt

Vat Registration is a legal obligation for businesses meeting the threshold requirement, helping companies avoid fines and ramifications. Contact now!

https://viralsocialtrends.com/vat-registration-outlined-in-uae/

Buy Verified PayPal Account | Buy Google 5 Star Reviewsusawebmarket

Buy Verified PayPal Account

Looking to buy verified PayPal accounts? Discover 7 expert tips for safely purchasing a verified PayPal account in 2024. Ensure security and reliability for your transactions.

PayPal Services Features-

🟢 Email Access

🟢 Bank Added

🟢 Card Verified

🟢 Full SSN Provided

🟢 Phone Number Access

🟢 Driving License Copy

🟢 Fasted Delivery

Client Satisfaction is Our First priority. Our services is very appropriate to buy. We assume that the first-rate way to purchase our offerings is to order on the website. If you have any worry in our cooperation usually You can order us on Skype or Telegram.

24/7 Hours Reply/Please Contact

usawebmarketEmail: support@usawebmarket.com

Skype: usawebmarket

Telegram: @usawebmarket

WhatsApp: +1(218) 203-5951

USA WEB MARKET is the Best Verified PayPal, Payoneer, Cash App, Skrill, Neteller, Stripe Account and SEO, SMM Service provider.100%Satisfection granted.100% replacement Granted.

[Note: This is a partial preview. To download this presentation, visit:

https://www.oeconsulting.com.sg/training-presentations]

Sustainability has become an increasingly critical topic as the world recognizes the need to protect our planet and its resources for future generations. Sustainability means meeting our current needs without compromising the ability of future generations to meet theirs. It involves long-term planning and consideration of the consequences of our actions. The goal is to create strategies that ensure the long-term viability of People, Planet, and Profit.

Leading companies such as Nike, Toyota, and Siemens are prioritizing sustainable innovation in their business models, setting an example for others to follow. In this Sustainability training presentation, you will learn key concepts, principles, and practices of sustainability applicable across industries. This training aims to create awareness and educate employees, senior executives, consultants, and other key stakeholders, including investors, policymakers, and supply chain partners, on the importance and implementation of sustainability.

LEARNING OBJECTIVES

1. Develop a comprehensive understanding of the fundamental principles and concepts that form the foundation of sustainability within corporate environments.

2. Explore the sustainability implementation model, focusing on effective measures and reporting strategies to track and communicate sustainability efforts.

3. Identify and define best practices and critical success factors essential for achieving sustainability goals within organizations.

CONTENTS

1. Introduction and Key Concepts of Sustainability

2. Principles and Practices of Sustainability

3. Measures and Reporting in Sustainability

4. Sustainability Implementation & Best Practices

To download the complete presentation, visit: https://www.oeconsulting.com.sg/training-presentations

Business Valuation Principles for EntrepreneursBen Wann

This insightful presentation is designed to equip entrepreneurs with the essential knowledge and tools needed to accurately value their businesses. Understanding business valuation is crucial for making informed decisions, whether you're seeking investment, planning to sell, or simply want to gauge your company's worth.

Unveiling the Secrets How Does Generative AI Work.pdfSam H

At its core, generative artificial intelligence relies on the concept of generative models, which serve as engines that churn out entirely new data resembling their training data. It is like a sculptor who has studied so many forms found in nature and then uses this knowledge to create sculptures from his imagination that have never been seen before anywhere else. If taken to cyberspace, gans work almost the same way.

Unveiling the Secrets How Does Generative AI Work.pdf

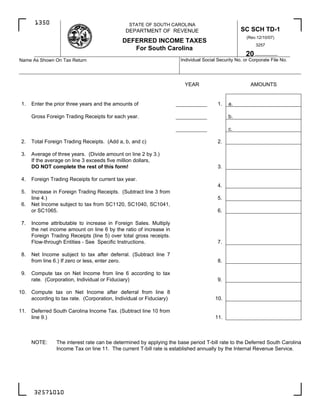

Deferred Income Taxes for South Carolina

1. 1350 STATE OF SOUTH CAROLINA

SC SCH TD-1

DEPARTMENT OF REVENUE

(Rev.12/10/07)

DEFERRED INCOME TAXES

3257

For South Carolina

20

Individual Social Security No. or Corporate File No.

Name As Shown On Tax Return

YEAR AMOUNTS

1. Enter the prior three years and the amounts of 1. a.

Gross Foreign Trading Receipts for each year. b.

c.

2. Total Foreign Trading Receipts. (Add a, b, and c) 2.

3. Average of three years. (Divide amount on line 2 by 3.)

If the average on line 3 exceeds five million dollars,

DO NOT complete the rest of this form! 3.

4. Foreign Trading Receipts for current tax year.

4.

5. Increase in Foreign Trading Receipts. (Subtract line 3 from

line 4.) 5.

6. Net Income subject to tax from SC1120, SC1040, SC1041,

or SC1065. 6.

7. Income attributable to increase in Foreign Sales. Multiply

the net income amount on line 6 by the ratio of increase in

Foreign Trading Receipts (line 5) over total gross receipts.

Flow-through Entities - See Specific Instructions. 7.

8. Net Income subject to tax after deferral. (Subtract line 7

from line 6.) If zero or less, enter zero. 8.

9. Compute tax on Net Income from line 6 according to tax

rate. (Corporation, Individual or Fiduciary) 9.

10. Compute tax on Net Income after deferral from line 8

according to tax rate. (Corporation, Individual or Fiduciary) 10.

11. Deferred South Carolina Income Tax. (Subtract line 10 from

line 9.) 11.

NOTE: The interest rate can be determined by applying the base period T-bill rate to the Deferred South Carolina

Income Tax on line 11. The current T-bill rate is established annually by the Internal Revenue Service.

32571010

2. GENERAL INSTRUCTIONS

For tax years beginning after 12-31-85, taxpayers, except Domestic International Sales Corporations (DISC) or Foreign

Sales Corporations, may elect to defer South Carolina Income Taxes attributable to the increase in Gross Income from

Foreign Trading Receipts.

quot;Foreign Trading Receiptsquot; means receipts from invoices issued by a seller directly to an unrelated purchaser

outside the United States from:

(a) the sale, exchange, or other disposition of export property outside the United States;

(b) the lease or rental of export property that is used by the leasee outside the United States;

(c) the performance of services that is related and subsidiary to the sale, exchange, lease, rental, or other

disposition of export property outside the United States by the South Carolina taxpayer including, but not

limited to, maintenance and training services;

(d) the performance of engineering, architectural, or consulting services for projects located outside the United

States.

A portion of the tax on Foreign Trading Receipts may be deferred as long as the base amount does not exceed five million

dollars and the taxpayer pays interest annually on the aggregate deferred tax at the quot;base period T-bill ratequot;. Tax on

Foreign Trading Receipts may NOT be deferred if the taxpayer intentionally ceases exporting property or after three

taxable years in which the taxpayer has no Gross Income from Foreign Trading Receipts.

The interest is due on the date the taxpayer is required to file the annual return without regard to any extension, but no

interest is due on amounts deferred for less than an entire taxable year. If the taxpayer fails to pay interest as required,

then all deferred taxes are due and payable on the annual return filing date.

The payment of deferred tax is due no later than the tax return filing date of the fifth tax year, following the taxable year for

which the tax was first deferred.

Example: Tax deferred in 2004 is due with the tax return filed in 2009. Deferred taxes may be paid at an

accelerated rate. Failure to pay deferred taxes when due renders the taxpayer ineligible to defer payment

of taxes for a subsequent tax year.

On Form SC1120 enter the payment of deferred tax on line 8 or its equivalent and attach a statement. For other returns,

enter the deferred tax on an quot;other quot; tax line and label in the dotted line.

SPECIFIC INSTRUCTIONS

Line 1 Foreign Trading Receipts are defined in the General Instructions.

Line 6 Enter the Net Income subject to South Carolina tax from the appropriate tax return. These returns include:

an individual, a corporation, a fiduciary of an estate or trust, a partnership or a limited liability company

(L.L.C.) taxed as either a partnership or a corporation.

Line 7 If a Partnership or S Corporation, or L.L.C. taxed as a partnership DO NOT complete lines 8 - 11 of this

form. The amount on line 7 is the amount of Deferred Income from Foreign Trading Receipts. Partners,

shareholders or members of an L.L.C. taxed as a partnership must be furnished their prorata share of the

Deferred Foreign Trading Receipts.

Line 10 Corporations must use the tax rate provided for form SC1120.

Individuals and Fiduciaries must use the tax rate schedule provided for forms SC1040 or SC1041.

File the original SC SCH TD-1 with your tax return. Taxpayers also are requested to send a copy of SCH TD-1 to the

address below.

South Carolina Department of Revenue

Research and Review

Columbia, SC 29214-0019

32572018