UiPath Test Automation using UiPath Test Suite series, part 4DianaGray10

Welcome to UiPath Test Automation using UiPath Test Suite series part 4. In this session, we will cover Test Manager overview along with SAP heatmap.

The UiPath Test Manager overview with SAP heatmap webinar offers a concise yet comprehensive exploration of the role of a Test Manager within SAP environments, coupled with the utilization of heatmaps for effective testing strategies.

Participants will gain insights into the responsibilities, challenges, and best practices associated with test management in SAP projects. Additionally, the webinar delves into the significance of heatmaps as a visual aid for identifying testing priorities, areas of risk, and resource allocation within SAP landscapes. Through this session, attendees can expect to enhance their understanding of test management principles while learning practical approaches to optimize testing processes in SAP environments using heatmap visualization techniques

What will you get from this session?

1. Insights into SAP testing best practices

2. Heatmap utilization for testing

3. Optimization of testing processes

4. Demo

Topics covered:

Execution from the test manager

Orchestrator execution result

Defect reporting

SAP heatmap example with demo

Speaker:

Deepak Rai, Automation Practice Lead, Boundaryless Group and UiPath MVP

Epistemic Interaction - tuning interfaces to provide information for AI supportAlan Dix

Paper presented at SYNERGY workshop at AVI 2024, Genoa, Italy. 3rd June 2024

https://alandix.com/academic/papers/synergy2024-epistemic/

As machine learning integrates deeper into human-computer interactions, the concept of epistemic interaction emerges, aiming to refine these interactions to enhance system adaptability. This approach encourages minor, intentional adjustments in user behaviour to enrich the data available for system learning. This paper introduces epistemic interaction within the context of human-system communication, illustrating how deliberate interaction design can improve system understanding and adaptation. Through concrete examples, we demonstrate the potential of epistemic interaction to significantly advance human-computer interaction by leveraging intuitive human communication strategies to inform system design and functionality, offering a novel pathway for enriching user-system engagements.

JMeter webinar - integration with InfluxDB and GrafanaRTTS

Watch this recorded webinar about real-time monitoring of application performance. See how to integrate Apache JMeter, the open-source leader in performance testing, with InfluxDB, the open-source time-series database, and Grafana, the open-source analytics and visualization application.

In this webinar, we will review the benefits of leveraging InfluxDB and Grafana when executing load tests and demonstrate how these tools are used to visualize performance metrics.

Length: 30 minutes

Session Overview

-------------------------------------------

During this webinar, we will cover the following topics while demonstrating the integrations of JMeter, InfluxDB and Grafana:

- What out-of-the-box solutions are available for real-time monitoring JMeter tests?

- What are the benefits of integrating InfluxDB and Grafana into the load testing stack?

- Which features are provided by Grafana?

- Demonstration of InfluxDB and Grafana using a practice web application

To view the webinar recording, go to:

https://www.rttsweb.com/jmeter-integration-webinar

Connector Corner: Automate dynamic content and events by pushing a buttonDianaGray10

Here is something new! In our next Connector Corner webinar, we will demonstrate how you can use a single workflow to:

Create a campaign using Mailchimp with merge tags/fields

Send an interactive Slack channel message (using buttons)

Have the message received by managers and peers along with a test email for review

But there’s more:

In a second workflow supporting the same use case, you’ll see:

Your campaign sent to target colleagues for approval

If the “Approve” button is clicked, a Jira/Zendesk ticket is created for the marketing design team

But—if the “Reject” button is pushed, colleagues will be alerted via Slack message

Join us to learn more about this new, human-in-the-loop capability, brought to you by Integration Service connectors.

And...

Speakers:

Akshay Agnihotri, Product Manager

Charlie Greenberg, Host

Generating a custom Ruby SDK for your web service or Rails API using Smithyg2nightmarescribd

Have you ever wanted a Ruby client API to communicate with your web service? Smithy is a protocol-agnostic language for defining services and SDKs. Smithy Ruby is an implementation of Smithy that generates a Ruby SDK using a Smithy model. In this talk, we will explore Smithy and Smithy Ruby to learn how to generate custom feature-rich SDKs that can communicate with any web service, such as a Rails JSON API.

DevOps and Testing slides at DASA ConnectKari Kakkonen

My and Rik Marselis slides at 30.5.2024 DASA Connect conference. We discuss about what is testing, then what is agile testing and finally what is Testing in DevOps. Finally we had lovely workshop with the participants trying to find out different ways to think about quality and testing in different parts of the DevOps infinity loop.

Accelerate your Kubernetes clusters with Varnish CachingThijs Feryn

A presentation about the usage and availability of Varnish on Kubernetes. This talk explores the capabilities of Varnish caching and shows how to use the Varnish Helm chart to deploy it to Kubernetes.

This presentation was delivered at K8SUG Singapore. See https://feryn.eu/presentations/accelerate-your-kubernetes-clusters-with-varnish-caching-k8sug-singapore-28-2024 for more details.

Kubernetes & AI - Beauty and the Beast !?! @KCD Istanbul 2024Tobias Schneck

As AI technology is pushing into IT I was wondering myself, as an “infrastructure container kubernetes guy”, how get this fancy AI technology get managed from an infrastructure operational view? Is it possible to apply our lovely cloud native principals as well? What benefit’s both technologies could bring to each other?

Let me take this questions and provide you a short journey through existing deployment models and use cases for AI software. On practical examples, we discuss what cloud/on-premise strategy we may need for applying it to our own infrastructure to get it to work from an enterprise perspective. I want to give an overview about infrastructure requirements and technologies, what could be beneficial or limiting your AI use cases in an enterprise environment. An interactive Demo will give you some insides, what approaches I got already working for real.

Software Delivery At the Speed of AI: Inflectra Invests In AI-Powered QualityInflectra

In this insightful webinar, Inflectra explores how artificial intelligence (AI) is transforming software development and testing. Discover how AI-powered tools are revolutionizing every stage of the software development lifecycle (SDLC), from design and prototyping to testing, deployment, and monitoring.

Learn about:

• The Future of Testing: How AI is shifting testing towards verification, analysis, and higher-level skills, while reducing repetitive tasks.

• Test Automation: How AI-powered test case generation, optimization, and self-healing tests are making testing more efficient and effective.

• Visual Testing: Explore the emerging capabilities of AI in visual testing and how it's set to revolutionize UI verification.

• Inflectra's AI Solutions: See demonstrations of Inflectra's cutting-edge AI tools like the ChatGPT plugin and Azure Open AI platform, designed to streamline your testing process.

Whether you're a developer, tester, or QA professional, this webinar will give you valuable insights into how AI is shaping the future of software delivery.

GDG Cloud Southlake #33: Boule & Rebala: Effective AppSec in SDLC using Deplo...James Anderson

Effective Application Security in Software Delivery lifecycle using Deployment Firewall and DBOM

The modern software delivery process (or the CI/CD process) includes many tools, distributed teams, open-source code, and cloud platforms. Constant focus on speed to release software to market, along with the traditional slow and manual security checks has caused gaps in continuous security as an important piece in the software supply chain. Today organizations feel more susceptible to external and internal cyber threats due to the vast attack surface in their applications supply chain and the lack of end-to-end governance and risk management.

The software team must secure its software delivery process to avoid vulnerability and security breaches. This needs to be achieved with existing tool chains and without extensive rework of the delivery processes. This talk will present strategies and techniques for providing visibility into the true risk of the existing vulnerabilities, preventing the introduction of security issues in the software, resolving vulnerabilities in production environments quickly, and capturing the deployment bill of materials (DBOM).

Speakers:

Bob Boule

Robert Boule is a technology enthusiast with PASSION for technology and making things work along with a knack for helping others understand how things work. He comes with around 20 years of solution engineering experience in application security, software continuous delivery, and SaaS platforms. He is known for his dynamic presentations in CI/CD and application security integrated in software delivery lifecycle.

Gopinath Rebala

Gopinath Rebala is the CTO of OpsMx, where he has overall responsibility for the machine learning and data processing architectures for Secure Software Delivery. Gopi also has a strong connection with our customers, leading design and architecture for strategic implementations. Gopi is a frequent speaker and well-known leader in continuous delivery and integrating security into software delivery.

GDG Cloud Southlake #33: Boule & Rebala: Effective AppSec in SDLC using Deplo...

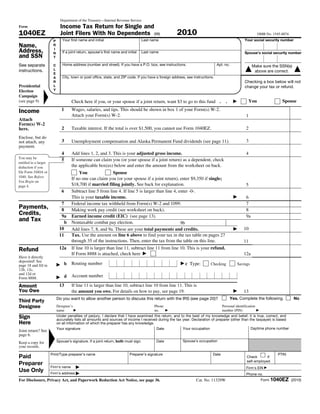

F1040ez

1. Department of the Treasury—Internal Revenue Service

Form Income Tax Return for Single and

1040EZ Joint Filers With No Dependents (99) 2010 OMB No. 1545-0074

P Your first name and initial Last name Your social security number

Name, R

Hye Hyun Bahng 5 2 5 9 3 1 2 3 4

Address, I

N If a joint return, spouse’s first name and initial Last name Spouse’s social security number

and SSN T

See separate C Home address (number and street). If you have a P.O. box, see instructions. Apt. no. Make sure the SSN(s)

instructions. L

2235 Ashley Crossing Drive 18

▲ above are correct. ▲

E

A City, town or post office, state, and ZIP code. If you have a foreign address, see instructions.

R Checking a box below will not

Presidential L Charleston, SC change your tax or refund.

Election Y

▲

Campaign

(see page 9) Check here if you, or your spouse if a joint return, want $3 to go to this fund . . ▶ You Spouse

Income 1 Wages, salaries, and tips. This should be shown in box 1 of your Form(s) W-2.

Attach your Form(s) W-2. 1 40,000 00

Attach

Form(s) W-2

here. 2 Taxable interest. If the total is over $1,500, you cannot use Form 1040EZ. 2 0 00

Enclose, but do

not attach, any 3 Unemployment compensation and Alaska Permanent Fund dividends (see page 11). 3 0 00

payment.

4 Add lines 1, 2, and 3. This is your adjusted gross income. 4 40,000 00

You may be

5 If someone can claim you (or your spouse if a joint return) as a dependent, check

entitled to a larger

deduction if you the applicable box(es) below and enter the amount from the worksheet on back.

file Form 1040A or You Spouse

1040. See Before

If no one can claim you (or your spouse if a joint return), enter $9,350 if single;

You Begin on

page 4. $18,700 if married filing jointly. See back for explanation. 5 9,350 00

6 Subtract line 5 from line 4. If line 5 is larger than line 4, enter -0-.

This is your taxable income. ▶ 6 30,650 00

7 Federal income tax withheld from Form(s) W-2 and 1099. 7 0 00

Payments, 8 Making work pay credit (see worksheet on back). 8 0 00

Credits, 9a Earned income credit (EIC) (see page 13). 9a 0 00

and Tax b Nontaxable combat pay election. 9b 0 00

10 Add lines 7, 8, and 9a. These are your total payments and credits. ▶ 10 0 00

11 Tax. Use the amount on line 6 above to find your tax in the tax table on pages 27

through 35 of the instructions. Then, enter the tax from the table on this line. 11 4,183 00

Refund 12a If line 10 is larger than line 11, subtract line 11 from line 10. This is your refund.

If Form 8888 is attached, check here ▶ 12a 35,817 00

Have it directly

deposited! See

page 18 and fill in ▶ b Routing number ▶c Type: Checking Savings

12b, 12c,

and 12d or

Form 8888. ▶ d Account number

Amount 13 If line 11 is larger than line 10, subtract line 10 from line 11. This is

You Owe the amount you owe. For details on how to pay, see page 19. ▶ 13 4,183 00

Do you want to allow another person to discuss this return with the IRS (see page 20)? Yes. Complete the following. No

Third Party

Designee Designee’s Phone Personal identification

name ▶ no. ▶ number (PIN) ▶

Sign Under penalties of perjury, I declare that I have examined this return, and to the best of my knowledge and belief, it is true, correct, and

accurately lists all amounts and sources of income I received during the tax year. Declaration of preparer (other than the taxpayer) is based

Here on all information of which the preparer has any knowledge.

Your signature Date Your occupation Daytime phone number

▲

Joint return? See

page 6. Medical Resident

Keep a copy for Spouse’s signature. If a joint return, both must sign. Date Spouse’s occupation

your records.

Print/Type preparer’s name Preparer’s signature Date PTIN

Paid Check if

self-employed

Preparer

Firm’s name ▶ Firm's EIN ▶

Use Only Firm’s address ▶ Phone no.

For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see page 36. Cat. No. 11329W Form 1040EZ (2010)

2. Form 1040EZ (2010) Page 2

Worksheet Use this worksheet to figure the amount to enter on line 5 if someone can claim you (or your spouse if married

filing jointly) as a dependent, even if that person chooses not to do so. To find out if someone can claim you as a

for Line 5 — dependent, see Pub. 501.

Dependents

Who Checked A. Amount, if any, from line 1 on front . . . . . .

+ A.

One or Both 300.00 Enter total ▶

B. Minimum standard deduction . . . . . . . . . . . . . . . . . . . . . B. 950.00

Boxes

C. Enter the larger of line A or line B here . . . . . . . . . . . . . . . . . . C.

D. Maximum standard deduction. If single, enter $5,700; if married filing jointly, enter $11,400 . D.

E. Enter the smaller of line C or line D here. This is your standard deduction . . . . . . . . E.

}

F. Exemption amount.

• If single, enter -0-.

• If married filing jointly and — F.

—both you and your spouse can be claimed as dependents, enter -0-.

—only one of you can be claimed as a dependent, enter $3,650.

G. Add lines E and F. Enter the total here and on line 5 on the front . . . . . . . . . . G.

(keep a copy for If you did not check any boxes on line 5, enter on line 5 the amount shown below that applies to you.

your records) • Single, enter $9,350. This is the total of your standard deduction ($5,700) and your exemption ($3,650).

• Married filing jointly, enter $18,700. This is the total of your standard deduction ($11,400), your exemption ($3,650), and

your spouse's exemption ($3,650).

Worksheet Before you begin: ✓ If you can be claimed as a dependent on someone else's return, you do not qualify for this credit.

for Line 8 — ✓ If married filing jointly, include your spouse's amounts with yours when completing this worksheet.

Making Work

Pay Credit 1a. Important. See the instructions on page 12 if (a) you received a taxable scholarship or fellowship grant not reported on

a Form W-2, (b) your wages include pay for work performed while an inmate in a penal institution, or (c) you received

a pension or annuity from a nonqualified deferred compensation plan or a nongovernmental section 457 plan.

Do you (and your spouse if filing jointly) have 2010 wages of more than $6,451 ($12,903 if married filing jointly)?

Yes. Skip lines 1a through 3. Enter $400 ($800 if married filing jointly) on line 4 and go to line 5.

No. Enter your earned income (see instructions) . . . . . 1a.

Use this b. Nontaxable combat pay included on line la (see

worksheet to instructions) . . . . . . . . . . . 1b.

figure the amount 2. Multiply line 1a by 6.2% (.062) . . . . . . . . . . . . 2.

to enter on line 8 3. Enter $400 ($800 if married filing jointly) . . . . . . . . . 3.

if you cannot be 4. Enter the smaller of line 2 or line 3 (unless you checked "Yes" on line 1a) . . . . . . 4.

claimed as a 5. Enter amount from Form 1040EZ, line 4 (on front) . . . . . . 5.

dependent on 6. Enter $75,000 ($150,000 if married filing jointly) . . . . . . 6.

another person's 7. Is the amount on line 5 more than the amount on line 6?

return.

No. Skip line 8. Enter the amount from line 4 on line 9 below.

Yes. Subtract line 6 from line 5 . . . . . . . . . . . 7.

8. Multiply line 7 by 2% (.02) . . . . . . . . . . . . . . . . . . . . 8.

(keep a copy for 9. Subtract line 8 from line 4. If zero or less, enter -0- . . . . . . . . . . . . . 9.

your records) 10. Did you (or your spouse, if filing jointly) receive an economic recovery payment in 2010? You may have received this

payment in 2010 if you did not receive an economic recovery payment in 2009 but you received social security

benefits, supplemental security income, railroad retirement benefits, or veterans disability compensation or pension

benefits in November 2008, December 2008, or January 2009 (see instructions).

No. Enter -0- on line 10 and go to line 11.

Yes. Enter the total of the payments you (and your spouse, if filing

jointly) received in 2010. Do not enter more than $250 ($500

if married filing jointly). 10.

11. Making work pay credit. Subtract line 10 from line 9. If zero or less, enter -0-. Enter the result

here and on Form 1040EZ, line 8. . . . . . . . . . . . . . . . . . . 11.

Mailing Mail your return by April 18, 2011. Mail it to the address shown on the last page of the instructions.

Return

Form 1040EZ (2010)