Download to read offline

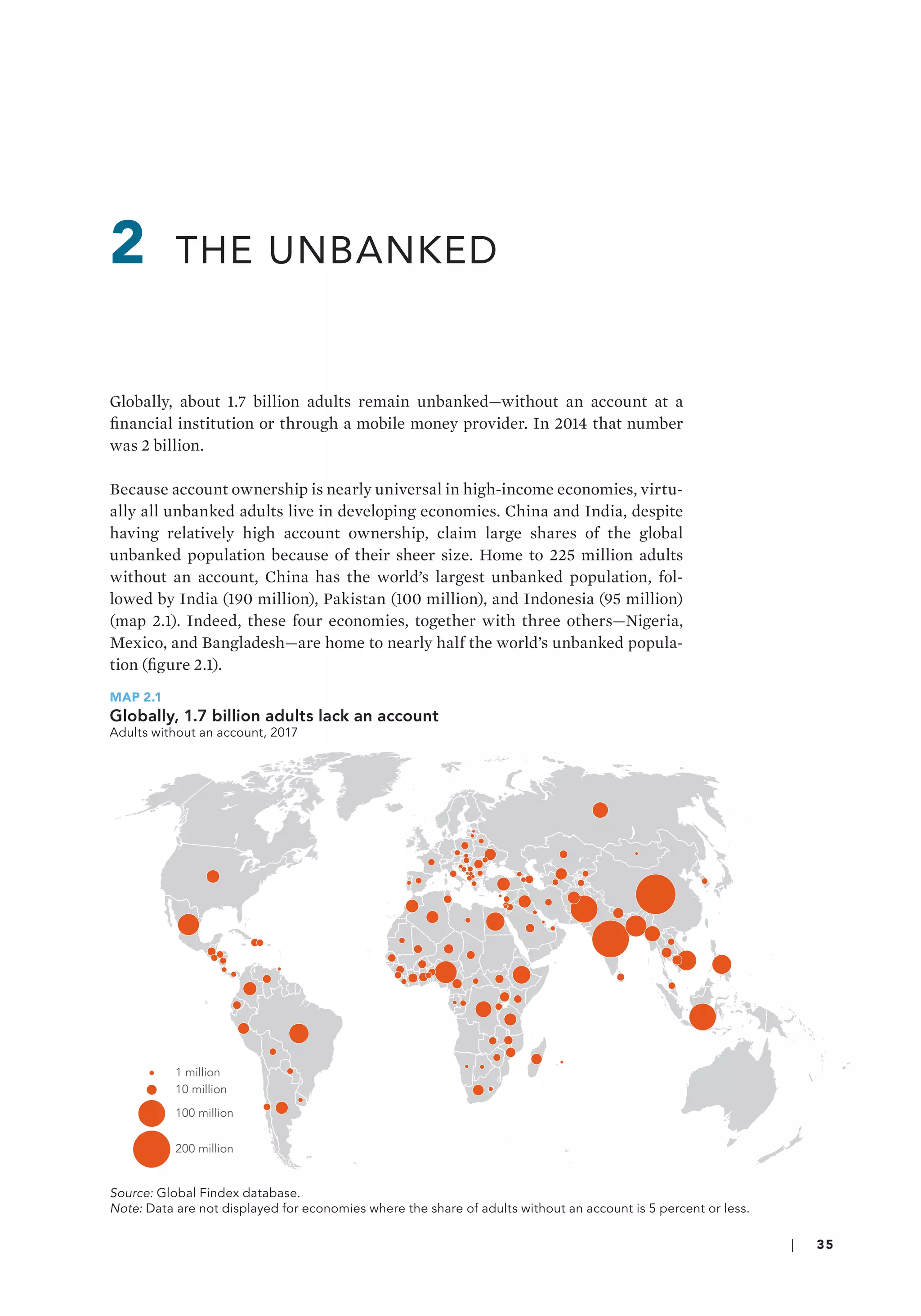

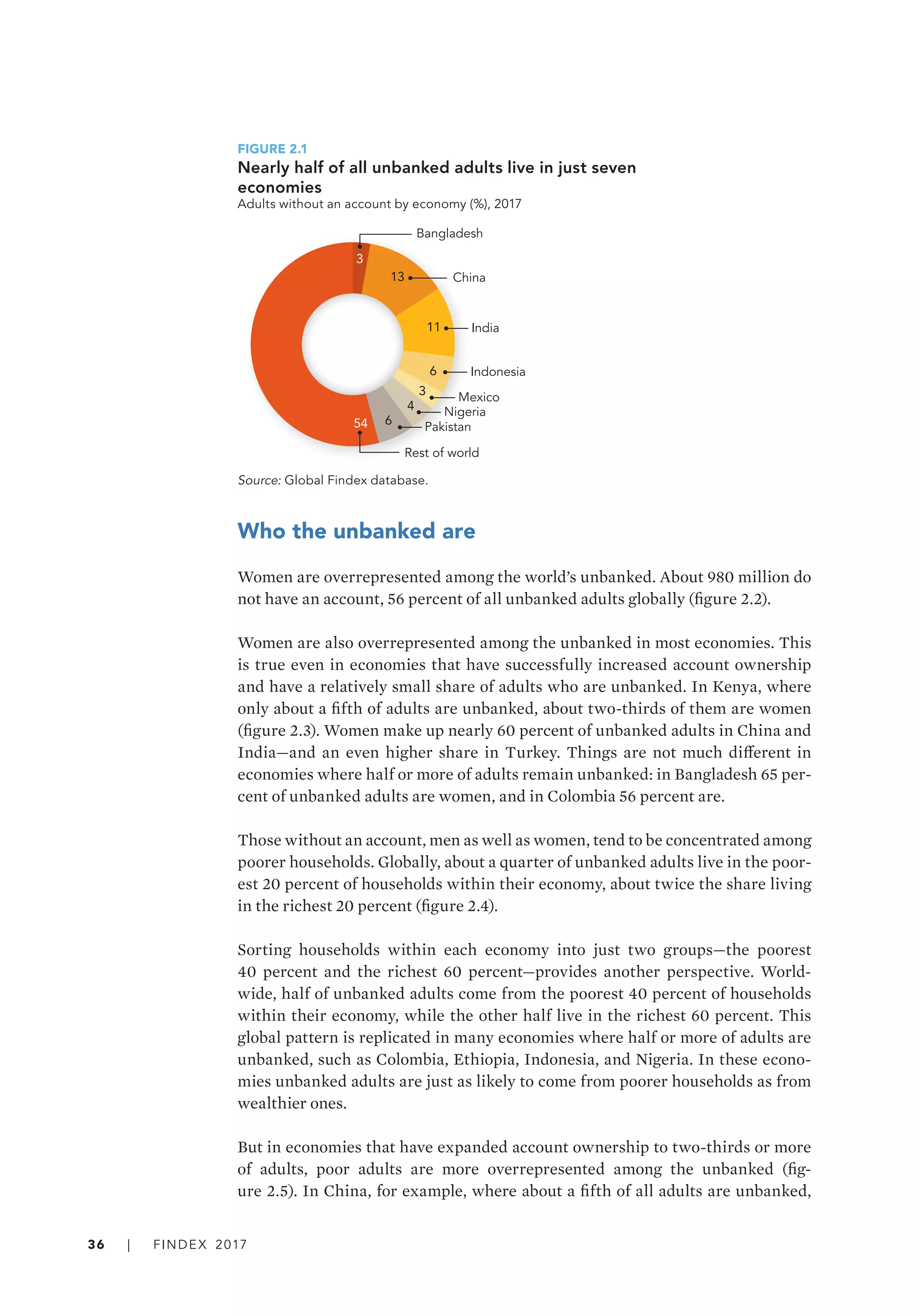

Globally, about 1.7 billion adults remain unbanked without a bank account. Women are overrepresented among the unbanked, comprising 56% of the unbanked population. Those without accounts tend to be poorer, younger, and less educated than average. The most commonly cited barrier to account ownership is lack of enough money, reported by nearly two-thirds of unbanked adults. Distance to financial institutions and documentation requirements also prevent many from opening accounts.