Daily Market Report February 14, 2016

•

0 likes•318 views

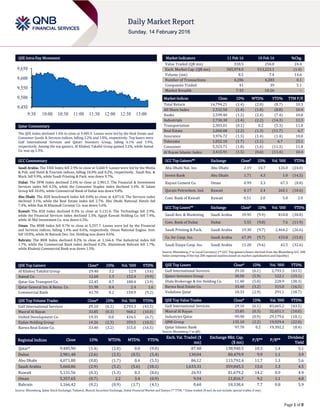

The QSE Index declined 1.4% to close at 9,485.9.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Daily Market Report February 14, 2016

Similar to Daily Market Report February 14, 2016 (20)

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

Daily Market Report February 14, 2016

- 1. Page 1 of 8 QSE Intra-Day Movement Qatar Commentary The QSE Index declined 1.4% to close at 9,485.9. Losses were led by the Real Estate and Consumer Goods & Services indices, falling 2.2% and 1.8%, respectively. Top losers were Gulf International Services and Qatari Investors Group, falling 6.1% and 5.9%, respectively. Among the top gainers, Al Khaleej Takaful Group gained 3.2%, while Aamal Co. was up 1.3%. GCC Commentary Saudi Arabia: The TASI Index fell 2.9% to close at 5,660.9. Losses were led by the Media & Pub. and Hotel & Tourism indices, falling 10.0% and 8.2%, respectively. Saudi Res. & Mark. fell 9.9%, while Saudi Printing & Pack. was down 9.7%. Dubai: The DFM Index declined 2.6% to close at 2,981.5. The Financial & Investment Services index fell 4.5%, while the Consumer Staples index declined 3.4%. Al Salam Group fell 10.0%, while Commercial Bank of Dubai was down 9.8%. Abu Dhabi: The ADX benchmark index fell 0.8% to close at 4,071.8. The Services index declined 3.1%, while the Real Estate index fell 2.7%. Abu Dhabi National Hotels fell 7.4%, while Ras Al Khaimah Ceramic Co. was down 5.6%. Kuwait: The KSE Index declined 0.3% to close at 5,131.6. The Technology fell 2.9%, while the Financial Services index declined 1.3%. Egypt Kuwait Holding Co. fell 7.4%, while Al-Mal Investment Co. was down 6.5%. Oman: The MSM Index fell 0.7% to close at 5,357.7. Losses were led by the Financial and Services indices, falling 1.4% and 0.6%, respectively. Oman National Engine. Invt. fell 10.0%, while Al Batinah Dev. Inv. Holding was down 8.6%. Bahrain: The BHB Index declined 0.2% to close at 1,166.4. The Industrial index fell 1.7%, while the Commercial Bank index declined 0.2%. Aluminium Bahrain fell 1.7%, while Khaleeji Commercial Bank was down 1.5%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Al Khaleej Takaful Group 29.40 3.2 12.9 (3.6) Aamal Co. 12.60 1.3 152.4 (9.9) Qatar Gas Transport Co. 22.45 0.7 180.4 (3.9) Qatar General Ins. & Reins. Co . 51.90 0.4 2.4 1.6 Commercial Bank 41.70 0.2 150.9 (9.2) QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% Gulf International Services 29.10 (6.1) 2,793.3 (43.5) Masraf Al Rayan 33.85 (0.3) 960.2 (10.0) United Development Co. 19.35 0.0 434.5 (6.7) Ezdan Holding Group 14.26 (2.3) 359.5 (10.3) Barwa Real Estate Co. 33.40 (3.2) 315.0 (16.5) Market Indicators 11 Feb 16 10 Feb 16 %Chg. Value Traded (QR mn) 318.5 256.0 24.4 Exch. Market Cap. (QR mn) 505,974.0 513,223.1 (1.4) Volume (mn) 8.5 7.4 14.6 Number of Transactions 4,286 4,283 0.1 Companies Traded 41 39 5.1 Market Breadth 7:33 10:26 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 14,794.21 (1.4) (2.0) (8.7) 10.3 All Share Index 2,532.50 (1.4) (1.8) (8.8) 10.4 Banks 2,599.40 (1.2) (2.4) (7.4) 10.8 Industrials 2,730.30 (1.4) (2.2) (14.3) 12.3 Transportation 2,303.01 (0.1) 0.2 (5.3) 11.0 Real Estate 2,060.08 (2.2) (1.3) (11.7) 6.7 Insurance 3,976.72 (1.5) (1.4) (1.4) 10.0 Telecoms 1,052.10 (1.7) (1.1) 6.7 23.1 Consumer 5,323.71 (1.8) (1.6) (11.3) 11.8 Al Rayan Islamic Index 3,415.91 (1.5) (0.6) (11.4) 10.4 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% Abu Dhabi Nat. Ins. Abu Dhabi 2.19 14.7 126.0 (24.0) Invest Bank Abu Dhabi 1.71 4.3 1.0 (14.5) Raysut Cement Co. Oman 0.99 3.3 67.3 (0.8) Qurain Petrochem. Ind. Kuwait 0.17 2.4 265.1 (10.6) Com. Bank of Kuwait Kuwait 0.51 2.0 5.0 2.0 GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% Saudi Res. & Marketing Saudi Arabia 39.95 (9.9) 810.8 (30.8) Com. Bank of Dubai Dubai 5.55 (9.8) 7.6 (11.9) Saudi Printing & Pack. Saudi Arabia 19.30 (9.7) 2,464.2 (26.6) Co. for Coop. Ins. Saudi Arabia 67.39 (9.7) 433.8 (15.0) Saudi Enaya Coop. Ins. Saudi Arabia 11.20 (9.6) 42.5 (32.6) Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Gulf International Services 29.10 (6.1) 2,793.3 (43.5) Qatari Investors Group 30.50 (5.9) 122.1 (19.1) Dlala Brokerage & Inv Holding Co. 11.40 (5.0) 228.9 (38.3) Barwa Real Estate Co. 33.40 (3.2) 315.0 (16.5) Vodafone Qatar 10.33 (2.9) 291.1 (18.7) QSE Top Value Trades Close* 1D% Val. ‘000 YTD% Gulf International Services 29.10 (6.1) 83,665.2 (43.5) Masraf Al Rayan 33.85 (0.3) 32,651.1 (10.0) Industries Qatar 99.90 (0.9) 29,179.6 (10.1) QNB Group 135.10 (2.2) 19,929.4 (22.8) Qatar Islamic Bank 97.70 0.2 19,392.2 (8.4) Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 9,485.90 (1.4) (2.0) 0.0 (9.0) 87.48 138,940.5 10.3 1.4 5.1 Dubai 2,981.48 (2.6) (2.5) (0.5) (5.4) 130.04 80,479.9 9.9 1.1 3.9 Abu Dhabi 4,071.80 (0.8) (1.7) 0.4 (5.5) 86.12 113,792.4 11.7 1.3 5.6 Saudi Arabia 5,660.86 (2.9) (5.2) (5.6) (18.1) 1,633.31 359,845.3 13.0 1.3 4.5 Kuwait 5,131.56 (0.3) (1.3) 0.3 (8.6) 26.93 81,679.2 14.2 0.9 4.9 Oman 5,357.65 (0.7) 2.2 3.4 (0.9) 9.54 21,816.7 9.2 1.1 4.8 Bahrain 1,166.42 (0.2) (0.9) (1.7) (4.1) 0.60 18,338.4 7.7 0.8 5.9 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) 9,450 9,500 9,550 9,600 9,650 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 8 Qatar Market Commentary The QSE Index declined 1.4% to close at 9,485.9. The Real Estate and Consumer Goods & Services indices led the losses. The index fell on the back of selling pressure from non-Qatari and GCC shareholders despite buying support from Qatari shareholders. Gulf International Services and Qatari Investors Group were the top losers, falling 6.1% and 5.9%, respectively. Among the top gainers, Al Khaleej Takaful Group gained 3.2%, while Aamal Co. was up 1.3%. Volume of shares traded on Thursday rose by 14.6% to 8.5mn from 7.4mn on Wednesday. Further, as compared to the 30-day moving average of 7.4mn, volume for the day was 14.4% higher. Gulf International Services and Masraf Al Rayan were the most active stocks, contributing 32.9% and 11.3% to the total volume, respectively. Source: Qatar Stock Exchange (* as a % of traded value) Earnings Releases, Global Economic Data and Earnings Calendar Earnings Releases Company Market Currency Revenue (mn) 4Q2015 % Change YoY Operating Profit (mn) 4Q2015 % Change YoY Net Profit (mn) 4Q2015 % Change YoY Takaful Emarat – Insurance* Dubai AED 377.9 216.5% 42.1 213.0% 10.2 42.3% Alliance Insurance* Dubai AED 306.2 -4.5% 22.8 -16.2% 44.0 -8.6% Dubai Parks and Resorts Dubai AED 0.0 NA 0.0 NA -110.9 421.2% Damac Properties Dubai Co.* Dubai AED 8,536.1 128.2% 4,543.8 30.1% 4,514.8 66.1% Abu Dhabi National Hotels Co. (ADNH)* Abu Dhabi AED 1,376.1 2.7% 0.0 NA 237.0 18.2% Abu Dhabi Aviation* Abu Dhabi AED 2,181.6 35.4% 0.0 NA 267.1 25.1% RAK Properties* Abu Dhabi AED 367.8 23.5% 0.0 NA 160.0 2.8% Finance House Co.* Abu Dhabi AED 0.0 NA 0.0 NA 61.7 -15.8% Fujairah Building Industries Co.* Abu Dhabi AED 246.3 -7.0% 7.5 8.5% 5.4 -12.4% Raysut Cement Co.* Oman OMR 94.7 0.4% 26.4 -13.3% 21.0 -23.6% Takaful Oman Insurance* Oman OMR 0.0 NA 0.0 NA 1,696.3 NA Arab Insurance Group (ARIG)* Bahrain USD 220.4 -30.1% 0.8 -87.1% 0.0 NA Source: Company data, DFM, ADX, MSM (*FY2015 results) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 02/11 US Department of Labor Initial Jobless Claims 6-February 269k 280k 285k 02/11 US Department of Labor Continuing Claims 30-January 2,239k 2,245k 2,260k 02/11 US Bloomberg Bloomberg Consumer Comfort 7-February 44.5 – 44.2 02/12 US Bureau of Labor Statistics Import Price Index MoM January -1.10% -1.50% -1.10% 02/12 US Bureau of Labor Statistics Import Price Index YoY January -6.20% -6.80% -8.10% 02/12 US Census Bureau Business Inventories December 0.10% 0.10% -0.10% 02/12 EU Eurostat Industrial Production SA MoM December -1.00% 0.30% -0.50% 02/12 EU Eurostat Industrial Production WDA YoY December -1.30% 0.70% 1.40% 02/12 EU Eurostat GDP SA QoQ 4Q2015 0.30% 0.30% 0.30% 02/12 EU Eurostat GDP SA YoY 4Q2015 1.50% 1.50% 1.60% 02/12 France French Labor Office Wages QoQ 4Q2015 0.10% – 0.20% 02/12 France INSEE Non-Farm Payrolls QoQ 4Q2015 0.20% 0.00% 0.00% 02/12 Germany Destatis GDP SA QoQ 4Q2015 0.30% 0.30% 0.30% 02/12 Germany Destatis GDP WDA YoY 4Q2015 1.30% 1.40% 1.70% 02/12 Germany Destatis GDP NSA YoY 4Q2015 2.10% 1.70% 1.70% 02/11 UK Royal Institution of Chartered RICS House Price Balance January 49% 52% 49% 02/12 UK ONS Construction Output SA MoM December 1.50% 2.00% -1.10% 02/12 UK ONS Construction Output SA YoY December 0.50% 0.80% -0.90% 02/12 Spain INE CPI Core MoM January -1.60% – 0.00% 02/12 Spain INE CPI Core YoY January 0.90% 0.70% 0.90% 02/12 Italy ISTAT GDP WDA QoQ 4Q2015 0.10% 0.30% 0.20% 02/12 Italy ISTAT GDP WDA YoY 4Q2015 1.00% 1.20% 0.80% Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) Overall Activity Buy %* Sell %* Net (QR) Qatari Individuals 57.36% 36.32% 67,012,209.49 Qatari Institutions 18.53% 20.23% (5,410,124.58) Qatari 75.89% 56.55% 61,602,084.91 GCC Individuals 2.09% 1.49% 1,887,469.17 GCC Institutions 4.83% 6.54% (5,454,756.58) GCC 6.92% 8.03% (3,567,287.41) Non-Qatari Individuals 12.18% 10.92% 4,002,167.27 Non-Qatari Institutions 5.02% 24.50% (62,036,964.77) Non-Qatari 17.20% 35.42% (58,034,797.50)

- 3. Page 3 of 8 Earnings Calendar Tickers Company Name Date of reporting 4Q2015 results No. of days remaining Status SIIS Salam International Investment 14-Feb-16 0 Due MCGS Medicare Group 14-Feb-16 0 Due UDCD United Development Company 14-Feb-16 0 Due DBIS Dlala Brokerage & Investment Holding Company 15-Feb-16 1 Due AKHI Al Khaleej Takaful Insurance 15-Feb-16 1 Due AHCS Aamal Company 15-Feb-16 1 Due ERES Ezdan Real Estate Company 16-Feb-16 2 Due QGTS Qatar Gas Transport Company (Nakilat) 17-Feb-16 3 Due BRES Barwa Real Estate Company 21-Feb-16 7 Due MERS Al Meera Consumer Goods Company 21-Feb-16 7 Due MCCS Mannai Corp. 24-Feb-16 10 Due ORDS Ooredoo 1-Mar-16 16 Due Source: QSE News Qatar WDAM net profit declines 4.0% QoQ in 4Q2015 – Widam Food Company’s (WDAM) net profit declined 4.0% QoQ to QR17.74mn in 4Q2015. However, on a YoY basis, net profit surged 102.3%. Meanwhile, the Board of Directors (BoD) has proposed distribution of QR2.7 per share cash dividend, which translates into a dividend payout of 70%. (QSE, QNBFS Research) QSE suspends trading of NLCS shares on February 14 – The Qatar Stock Exchange (QSE) has announced the trading suspension of Alijarah Holding’s (NLCS) shares on February 14, 2016 due to its AGM being held on that day. (QSE) QSE suspends trading of GWCS shares on February 14 – The Qatar Stock Exchange (QSE) has announced the trading suspension of Gulf Warehousing Company’s (GWCS) shares on February 14, 2016 due to its AGM and EGM being held on that day. (QSE) MPHC seeks shareholders’ nod for QR0.70 per share dividend – Mesaieed Petrochemical Holding Company (MPHC) will hold its ordinary general assembly meeting (AGM) on March 9, 2016. Shareholders at the AGM will consider approving board of directors’ recommendation for a dividend payment of QR0.70 per share, representing 7% of the nominal share value. The meeting will also discuss and approve the corporate governance report of MPHC for the year 2015. If a quorum is not met, the second meeting will be held on March 30, 2016 at the same time and place. (QSE) GISS seeks shareholders’ nod for QR1 per share dividend – Gulf International Services (GISS) will hold its ordinary general assembly meeting (AGM) on March 2, 2016. Shareholders at the AGM will consider approving board of directors’ recommendation for a dividend payment of QR1 per share, representing 10% of the nominal share value. The meeting will also discuss and approve the corporate governance report of GISS for the year 2015. If quorum is not met, the second meeting will be held on March 29, 2016 at the same time and place. (QSE) ERES subsidiary begins Sakin service to facilitate leasing – Ezdan Holding Group (ERES) subsidiary, Ezdan Real Estate Company, has launched a new service Sakin Centre to provide integrated leasing services and effectively manage its properties. Its branches operate from 7.30am to 9pm except on Fridays. The launch is within the framework of the company’s efforts to provide affordable and flexible solutions to facilitate contracting and leasing procedures. It is made available through two branches in Doha and Al Wakrah to provide leasing, maintenance, utility & customer care services and payment. (Peninsula Qatar) MCCS EGM approves amendment to Article of Association – Mannai Corporation’s (MCCS) extraordinary general meeting (EGM) has approved the board’s proposal to amend the company’s Article of Association, namely clause no.26 and 32-7. Clause no. 26 stipulates that MCCS shall be managed by a 10-member board for a renewable tenure of three years. The nomination of the Directors shall take into account, among other things, the ability of the candidates to give a sufficient time to their duties as Directors, in addition to their skills, knowledge, experiences, professional technical and academic qualifications and their personalities. Item 7 of the clause no.32 provides that the participation in the meeting of the Board of Directors may be by any of the common secure modern means of telecommunications which enables the participant to listen and effectively participate in the board’s activities. (QSE) QNBK: Qatar’s private consumption may increase on stable spending – QNB Group (QNBK), in its monthly report, has noted that Qatar’s investments, as a share of its gross domestic product (GDP), rose to 39.6% in 2Q2015 from 32.4% in 2014 on stable government capital spending. The country’s private consumption rose to 20.8% of GDP in 2Q2015 from 14.8% of GDP in 2014, with imports similarly increasing from 30.5% to 36.1% of GDP on growing population needs. QNBK expects the share of private consumption and investment to increase on high population growth and strong government investments, while lower expected oil prices in 2015 should reduce the share of exports. Qatar’s crude oil production decreased to 683k barrels per day (b/d) in November 2015 from 639k b/d in October 2015. QNBK expects oil prices to stabilize as excess supply in the global market would be reduced by both higher demand and production cuts among high- cost producers, such as US shale oil producers. QNBK analysts expect Qatar’s ongoing investment program to continue to attract expatriates, resulting in overall population growth of 4.1% in 2016. (Peninsula Qatar) BMI: Qatar’s total household spending may grow 12.9% to reach $45bn – Fitch Group company, BMI Research, in its recent ‘Qatar retail report’, has said that total household spending in Qatar is expected to grow by an average annual rate of 12.9% to reach $45bn by 2019. With increasing economic diversification driven by a growing population, strong and stable GDP growth and substantial per capita incomes, retailers would increasingly be attracted to the country and the retail market would expand. BMI said the number of households and level of household income are also expected to increase in Qatar, with the number of households set to reach 307,030 in 2019, while the average household income will exceed $137,884. Housing and utilities will remain the largest

- 4. Page 4 of 8 retail sub-sector, accounting for just under one-third of total household spending. Unlike Saudi Arabia and Kuwait, the two most oil-dependent economies in the Gulf Cooperation Council (GCC), Qatar has managed to at least partially diversify its economy in the past decade. Thanks to some immunity to the fluctuations of oil & gas prices and rollout of new strategic projects, the growth of Qatar’s real economic output would have accelerated to 6.6% in 2015 from 6.2% in 2014. (Gulf-Times.com) MEC: New initiative to boost business environment – The Ministry of Economy and Commerce (MEC), in cooperation with the Ministry of Municipality and Environment (MME), has announced its second initiative to ease procedures and specify conditions for construction licenses of business centers. The initiative is part of MEC’s efforts to improve and develop the business environment in the country through providing comprehensive investment solutions for entrepreneurs. According to a statement issued by the MEC, the initiative will allow owners of business centers to subdivide the internal area into open spaces, semi-closed spaces, completely closed spaces, or partitioned sections with screens. The step would allow the lease of the property to a number of tenants, from large corporations to small enterprises. Business centers are equipped with all the necessary support services, wired and wireless communication infrastructure and furniture, in addition to other organizational services such as facilities for holding conferences and provision for transportation services. Owners of business centers can obtain the necessary approvals for the subdivision from the MME, the General Directorate of the Civil Defense and the MEC. (Gulf-Times.com) ORDS boosts fiber network speed – Ooredoo (ORDS) has announced that its free speed upgrade on the fiber network is now live. With the upgrade, all 50Mbps home fiber plans received a double speed increase to 100Mbps, while existing 100Mbps plans were boosted to 300Mbps – the fastest home fixed line connection ever offered. On top of the speed boost, ORDS is also offering to all fiber customers a QR100 discount on a new enhanced Supernet Fiber Wi-Fi Broadband Gateway for all 100Mbps and 300Mbps customers. The Supernet Fiber Wi-Fi Broadband Gateway is a new device that supports more than 40 simultaneous connections, to satisfy even the most demanding of homes and employs the latest 802.11ac Wi-Fi specifications. (Gulf-Times.com) QP awards EPIC deal to JV to supply HIA with jet fuel – Qatar Petroleum (QP) has awarded an engineering, procurement, installation and commissioning (EPIC) contract to supply jet fuel from Ras Laffan Industrial City to the Hamad International Airport (HIA) in Doha. The contract was awarded to a joint venture of Consolidated Contractors group & Teyseer Contracting Company to build a 24-inch pipeline and associated facilities that will be used to transport the jet fuel. The project will ensure meeting the long-term demand of Jet A1 supply to the HIA beyond 2030, with the option of the fuel availability from two distinct and separate sources: Ras Laffan and Mesaieed. (Gulf-Times.com) Algal technology to help Qatar achieve food security – French ambassador Eric Chevallier described the Algal Technologies Program (ATP) as “a very interesting and promising” research project aimed at helping Qatar achieve food security, environmental protection, and bioremediation. The project started in 2009 with funding from Qatar Airways (QA) and the Qatar Science and Technology Park. It collected over 200 local microalgae and cyanobacteria species from various parts of the country. The research team also started converting algae biomass to biodiesel, bioethanol and bio-crude oil as part of the experimental stage. (Gulf-Times.com) Qatar-US trade in goods at $5.54bn in 2015 – The combined value of Qatar-US bilateral trade in goods in 2015 stood at $5.54bn (around QR20.17bn), witnessing a sharp fall of nearly 20% as compared to $6.92bn (around QR25.20bn), the highest ever registered in 2014. The total value of Qatar’s imports of goods from the US in 2015 was $4.23bn (around QR15.40bn) and the value of exports was about $1.31bn (around QR4.77bn). The annual trade balance between the two countries was about $2.93bn (around QR10.67bn), which was skewed in favor of the US being one of the largest import destinations of Qatar. (Peninsula Qatar) International WSJ: US, UK likely to charge multiple banks in Libor rigging – According to Wall Street Journal , American and British regulators are likely to charge several banks with rigging interest rates, including Citigroup, the third-largest US bank and London-based HSBC Holdings. The US Commodity Futures Trading Commission and the UK Financial Conduct Authority were preparing a final round of civil charges against the banks for rate manipulation in the Libor scandal, the newspaper reported, citing people close to the investigation. The Journal said the CFTC was still investigating J.P. Morgan Chase, the largest American bank by assets, but that may not lead to charges. UK regulators said they dropped their probe of J.P. Morgan in 2015. The US and British regulators are leading a seven-year investigation into the manipulation of Libor, or the London interbank offered rate. (Reuters) Strong US consumer spending counters recession fears – US consumer spending regained momentum in January as households ramped up purchases of a variety of goods, in a hopeful sign that economic growth was picking up after slowing to a crawl at the end of 2015. However, the outlook for consumer spending was tempered by another report on Friday showing sentiment among households ebbed in early February. Still, the increase in consumer spending last month underscored the economy's resilience and challenged the view that a recession was looming. The Commerce Department said retail sales excluding automobiles, gasoline, building materials and food services increased 0.6% last month after an unrevised 0.3% decline in December. These so-called core retail sales correspond most closely with the consumer spending component of GDP. (Reuters) Policymakers : ECB rate cut likely but no appetite for now for radical easing – There is firm support for a deposit rate cut within the European Central Bank's (ECB) Governing Council but appetite for more radical action is still limited, conversations with policymakers indicate a month before the March rate decision. With long-term inflation expectations falling, the ECB will probably have to act and frame the rate cut as part of broader a package, with some measures involving changes to the bank's flagship asset-purchase program, policymakers told Reuters. However, with no consensus yet about which further measures to take and Europe's modest economic recovery still broadly on track, some of those spoken to cautioned against radical action. However they noted that their view could still change if recent market turmoil proved lasting, posing a risk to the real economy. (Reuters) Moody's sees Brexit hitting whole EU; watching Poland closely – Moody's Senior Analyst Dietmar Hornung said UK exit from the European Union (EU) would affect the whole region's sovereign ratings warning it would set a precedent that other countries could end up following. Hornung said Moody’s was monitoring Poland closely but was comfortable with its Portugal rating despite a bond market selloff. Britain is expected to hold a referendum on whether to quit the 28-country EU in June or shortly after. All the main credit agencies have warned a vote to leave could hurt the UK's rating, but Hornung said it could have a wider impact. (Reuters)

- 5. Page 5 of 8 Greek PM : Differences between lenders delaying bailout review – According to sources, Greek Prime Minister Alexis Tsipras said that differences between the country's international lenders over its pension reform plans are delaying the first review of its latest financial bailout. Reforming Greece's ailing pension system is a prerequisite for the conclusion of the review, which is expected to open the way for debt relief talks. The government has faced widespread protests over its reform plans however, as austerity- weary Greeks push back against yet more cuts to the country's welfare system. Tsipras said "There are differences among the lenders on Greece's pension reform that are delaying the whole process". He added that the negotiations for the review are in the final stage and repeated that he is willing to increase contributions to the pension funds to save pensioners' income. (Reuters) China Lunar New Year holiday retail sales up 11.2% YoY – According to the Ministry of Commerce Chinese retail sales grew 11.2% during the week-long Lunar New Year vacation compared with the same holiday period in 2015. Revenues of retailers and catering firms grew to about 754bn yuan during the Feb 7-13, 2016 "Golden Week" holiday. The holiday is especially important for retailers, which vie for customers by launching promotions and discounts. Millions of people take time off work to travel and generally spend more than usual during the break. (Reuters) India's retail inflation hits 17-month high, industrial output falls again – India's retail inflation unexpectedly edged up to a 17- month high in January, while industrial production contracted at a faster-than-expected pace in December, underscoring imbalances lurking in Asia's third-largest economy. Government data showed retail prices rose 5.69% YoY in January, their fastest pace since August 2014. Another release showed output at factories, utilities and mines shrank an annual 1.3% in December. However, the contraction was smaller than a revised 3.4% fall in November. Data shows no let-up in food inflation. Retail food prices were up 6.85% on the year in January, compared to 6.40% in December. (Reuters) Regional BofAML: GCC countries to maintain currency peg – According to Bank of America Merrill Lynch (BofAML), the GCC currencies’ US dollar (USD) pegging will continue at least for the medium-term period. Key to this view is a combination of still sizeable foreign assets in parts of the GCC and the apparent start of a regional multiyear fiscal adjustment process. While all GCC countries have expressed their commitment to the USD pegs, their ability to defend the arrangements in a sustained oil price slump varies greatly. Within the GCC, Kuwait, Qatar and the UAE are still in a comfortable position given fiscal breakeven oil prices of $50- 65/bbl and fiscal buffers that can cover deficits incurred under $30/bbl for 15-20 years. At the other end of the spectrum, Saudi Arabia, Bahrain and Oman are more challenged as fiscal buffers would be exhausted within five years under the same set of assumptions. (Peninsula Qatar) ACWA Power plans $8bn debt raising – ACWA Power CEO Paddy Padmanathan has said that the company is planning to raise $8bn of debt in 1H2016 to finance projects that will help to boost its generating capacity by a third by 2016-end. The plan comes in the face of difficult market conditions for Middle Eastern developers, with regional governments reassessing expenditure at a time of lower oil prices that have also served to squeeze liquidity in the region’s banking system. Among the projects earmarked for ACWA’s proposed new funding is the 1,200-megawatt (MW) Hassyan clean coal power plant in Dubai, which it is building in conjunction with China’s Harbin Electric and with Alstom as the lead contractor. He said the $8bn raised will also cover the Ibri/Sohar-3 scheme in Oman, in partnership with Japan’s Mitsui & Company, as well as the 100-MW Redstone solar plant in South Africa. Some of the money will also be used to help refinance debt against the Rabigh 1 power plant, run by Rabigh Electricity Company and part-owned by ACWA. The new projects are expected to raise ACWA’s power assets to 28,000 MW by 2016-end from almost 21,000 MW now. While Kuwait is expected to be one of the most active markets in 2016, ACWA is also watching for new projects being tendered in Jordan, Morocco and the UAE. In Egypt, ACWA expects to sign a power purchase agreement and secure financing for a 2,250-MW power plant in Dairut. (Reuters) SCTNH: KSA witnesses 7.4mn visitors in 1H2015 – According to official data from the Saudi Commission for Tourism & National Heritage (SCTNH), the Kingdom remains a popular destination for GCC tourists, with around 7.4mn visitors entering Saudi Arabia in 1H2015, which represented an increase of 25% against the same period in 2014. A total of 2.1mn visitors were ‘day visitors’ with the remaining 5.2mn spending nearly SR11.8bn and accounting for 30.5mn room nights. In 2014, 6.6mn Gulf tourists visited Saudi Arabia, spending SR22bn. Bahraini and Kuwaiti visitors accounted for a large percentage of total inbound GCC visitor numbers, with 33% each, followed by Qatar and the UAE. (GulfBase.com) Middle East Healthcare reschedules float for March 2016 – Middle East Healthcare Company has rescheduled its offering to run from March 3-9, 2016. The Saudi Capital Market Authority, on January 18, said the company requested postponing its initial public offering and added that the company had to determine a new date for its offering within six weeks and finalize its flotation by March 31, 2016 or its regulatory approval would be considered cancelled. Middle East Healthcare was to offer 30% of itself in its initial share sale, first to initial investors and then the public. The latter phase was supposed to run February 3-9, 2016. (Reuters) Chinese officials favour dual listing for Saudi Aramco – According to sources, Chinese officials pitched in for a dual listing of Saudi Arabian Oil Company (Saudi Aramco) that would put the government-owned oil giant’s shares on both the Hong Kong and Saudi exchanges in return for anchor investments from Chinese funds. The proposal was made earlier in 2015. However, no decision has been made as yet. In January 2015, Saudi Aramco had said that it was considering an initial public offering of the entire business or some of its units, which could make it one of the world’s biggest public companies. One option Saudi Aramco is reportedly considering is an IPO for part of its downstream and refining businesses, which could be valued at over $90bn and raise between $5-10bn. Sources reported that the company hasn’t mandated financial advisers and may choose Saudi Arabia as the sole listing venue. (Bloomberg) Saudi Enaya’s accumulated losses reach 51.28% of capital – Saudi Enaya Cooperative Insurance Company has said that its accumulated losses amounted to SR205.1mn as on January 31, 2016, which represents 51.28% of its paid-up capital. The accumulated losses are mainly attributed to the pre-incorporation expenses incurred by the company, the delay in commencement of commercial operations and slow market penetration during the start-up phase. The company, however, maintains a sound liquidity and solvency position. (Tadawul) India, UAE sign nine agreements – India and the UAE on February 11, 2016 signed nine agreements covering cooperation in the fields of currency swap, culture, investment in the infrastructure sector, renewable energy, space research, insurance supervision, cyber security, skill development, and commercial information sharing. (Bloomberg) CBI reports AED466.6mn net loss in 2015 – Commercial Bank International (CBI) reported a net loss of AED466.6mn during the year ended December 31, 2015. Non Performing loans (NPLs)

- 6. Page 6 of 8 reduced by AED1.38bn (or 58.4%) to AED983mn from December 31 ,2014. The bank’s total assets stood at AED16.48bn at the end of December 31, 2015 as compared to AED19.68bn in the year-ago period. Net loans & advances reached AED11.51bn, while customers’ deposits stood at AED11.11bn. The bank’s capital adequacy ratio remained at comfortable levels well above the regulatory requirement at 14.8%. (ADX) DI showcases pioneering concepts, projects at ACRES Middle East – Dubai Investments (DI) showcased pioneering real estate concepts and projects of its subsidiaries Dubai Investments Park (DIP) and Dubai Investments Real Estate Company (DIRC) at ACRES Middle East 2016 Investment, Real Estate Exhibition and Conference, at Expo Centre Sharjah from February 10 to 13, 2016. The projects on show included Mirdif Hills, a mixed-use, self-contained community project being developed by DIRC, adjacent to Mushrif Park in Dubai. DI had on show the project model of its pioneering concept Dubai Investments Park, the largest commercial, industrial & residential community-of-its-kind in the Middle East. The success of DIP prompted DI to consider replicating the DIP business model and developing similar integrated communities in other countries across the region and Africa. (DFM) Debt deal for Limitless closer after Silver Point sale – According to sources, Dubai’s Limitless debt restructuring deal moved closer after Silver Point Capital sold its share of AED4.45bn debt in January 2016. Silver Point, one of a minority of creditors holding up a deal, sold half of its roughly $80mn loan to Mashreq and the other half to Massar Investments, an investment firm controlled by Mashreq’s owners. A deal can only be agreed once all Limitless creditors have given their assent. Reportedly, the Silver Point move will increase pressure on Arab National Bank, another creditor that had not agreed to the plan as of late 2015, to review its position. (Reuters) DIAC Chairman: Dubai property disputes may rise as sector slows – Dubai International Arbitration Centre (DIAC) Chairman Dr. Habib Al Mulla has said that a slowdown in Dubai’s real estate and construction sector would lead to more cases being filed with the Emirate’s arbitration centre. As per the data provided by DIAC, the number and value of disputes soared following Dubai’s property crash that began in 2008, with 871 cases claiming a combined AED14bn logged in 2010-11. Case numbers fell to a six-year low in 2014 as property prices rebounded, but sales dropped about 15% in 2015 and are expected to decline further in 2016. (Reuters) Mubadala seeks $2bn loan refinancing – According to sources, Mubadala is in talks with local and international lenders to raise a loan worth up to $2bn, which it plans to close in 1H2016. The state-owned investment fund is discussing whether to borrow the cash over three or five years or split the financing between both. The funding will be reportedly used to roll over a three-year revolving credit facility. The fund has a $2bn facility due to mature in May 2016, which was provided by 19 banks and pays a margin of 75 basis points over the London interbank offered rate (LIBOR). (Reuters) Asteco: Abu Dhabi’s residential market may slow down in 2016 – According to a latest report by Asteco, Abu Dhabi’s residential property market is expected to witness a slowdown in demand in the next 12 months, after relatively slow but positive market performance in 2015. However, this may not lead to a major drop in rental rates due to the limited amount of new supply that is coming online in 2016. As per the report, the UAE’s overall market conditions are under pressure due to low oil prices, and this would lead to a reduction in government spending. In turn, this could impact future demand as growth slows down and salary levels remain stable. It added that while low demand may put pressure on both rental rates and sales prices, limited supply is likely to minimize the pressure, at least as compared to Dubai. In 2016, Abu Dhabi is expected to add 3,000 apartments and 850 villas to its residential supply. In 2015, a total of 2,000 apartments and 100 villas were delivered, including 1,010 units in two projects on Reem Island, and 312 units on the Corniche. Asteco said it did not expect to see any major drop in residential sales prices in 2016 for completed properties due to sustained demand by owners- occupiers and investors. (GulfBase.com) KPI CEO: Oil prices could reach $50-60 a barrel by mid-2017 – Kuwait Petroleum International (KPI) CEO Bakheet al-Rashidi has said that oil prices could reach up to a range of $50 to $60 a barrel by mid-2017. He said that prices could reach the range of $60 to $80 a barrel in three years’ time. Rashidi attributed the drop in oil prices to excess supply in the market and slow demand from Asia, particularly China. (Reuters) OADC announces results of offer to buy OADC minority shareholders’ shares – Oman Agriculture Development Company’s (OADC) majority shareholders had made an offer to the company's minority shareholders (who own 5,000 shares or less) to buy the latter’s shares at a price of OMR1.654per share during the period from December 20, 2015 to January 19, 2016. This offer was part of converting the company from SAOG to SAOC. The company said that at the end of the offer period, no minority shareholder presented to sell their shares to majority shareholders under the above-mentioned offer. (MSM) Sezad signs OMR55m deal for government berth infrastructure – Oman’s Special Economic Zone Authority in Duqm (Sezad) has signed an agreement with Combined Group Contracting Company to build infrastructure facilities for a government berth at the port. The total project cost is estimated at OMR55.4mn and implementation will take 30 months from the date of awarding, excluding 30 days of preparations. The government berth is the first integrated berth implemented in Oman ports to serve government agencies with a total length of 980 meters allocated to a number of government entities as well as for fast ferries. It is one of the most important security facilities at Duqm Port. It will provide readiness to manage logistics operations for these entities and the security aspect of the port and the entire special economic zone. The work for a new project includes the construction of buildings, roads, facilities and utilities necessary for the operation of the government berth. (GulfBase.com) MB Holding’s subsidiary inks mining deal with Rwanda government – Tri Metals Mining Limited has signed three large-scale mining agreements with the Rwandan government to undertake mining operations in Bisesero, Karongi District. With an estimated project value of $39mn, Tri Metals will carry out mining operations to extract mainly Cassiterite (Tin), Niobo-Tantalite (Tantalum and Niobium), and Wolframite (Tungsten) in Bisesero concessions in the Western Province. Tri Metals is a subsidiary of Mawarid Mining, a wholly-owned subsidiary of Oman’s MB Holding Company. (GulfBase.com) BMB reports $5.08mn net profit in 2015, recommends dividend freeze – Bahrain Middle East Bank (BMB) reported a net profit of $5.08mn in 2015 as compared to $4.52mn in 2014. Total operating income reached $12.57mn in 2015 as compared to $12.23mn in 2014. The bank’s total assets stood at $171.87mn at the end of December 31, 2015 as compared to $172.84mn in the year-ago period. Loans & advances reached $110.705mn, while deposits from financial institutions and customers stood at $125.1mn and $8.73mn, respectively. Meanwhile, the bank’s board of directors (BoD) has decided not to distribute any dividends to its shareholders for the financial year ended December 31, 2015. (Bahrain Bourse)

- 7. Page 7 of 8 ARIG BoD decides dividend freeze – Arab Insurance Group’s (ARIG) board of directors (BoD) has decided not to distribute any dividend to its shareholders for the financial year ended December 31, 2015. This dividend freeze is subject to the AGM and the regulatory approval. (Bahrain Bourse) TAKAUD signs MoU with BKIC – TAKAUD and Bahrain Kuwait Insurance Company (BKIC) have signed an MoU. They plan to create strong synergies between the two institutions, which in turn enhances the customer offerings and experiences for both firms. The partnership will allow both providers to explore areas of cooperation that will enhance their respective customer propositions. (Bahrain Bourse)

- 8. Contacts Saugata Sarkar Shahan Keushgerian Zaid al-Nafoosi, CMT, CFTe Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6509 Tel: (+974) 4476 6535 saugata.sarkar@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa zaid.alnafoosi@qnbfs.com.qa ` QNB Financial Services SPC Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 8 of 8 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg (*$ adjusted returns; #Market closed on February 12, 2016) 80.0 100.0 120.0 140.0 160.0 180.0 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 QSEIndex S&P Pan Ar ab S&P GCC (2.9%) (1.4%) (0.3%) (0.2%) (0.7%) (0.8%) (2.6%) (3.2%) (2.4%) (1.6%) (0.8%) 0.0% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,237.92 (0.7) 5.5 16.6 MSCI World Index 1,486.45 1.2 (2.5) (10.6) Silver/Ounce 15.75 0.0 4.9 13.7 DJ Industrial 15,973.84 2.0 (1.4) (8.3) Crude Oil (Brent)/Barrel (FM Future) 33.36 11.0 (2.1) (10.5) S&P 500 1,864.78 2.0 (0.8) (8.8) Crude Oil (WTI)/Barrel (FM Future) 29.44 12.3 (4.7) (20.5) NASDAQ 100 4,337.51 1.7 (0.6) (13.4) Natural Gas (Henry Hub)/MMBtu 2.07 (2.6) (0.9) (10.6) STOXX 600 312.41 2.1 (3.2) (11.6) LPG Propane (Arab Gulf)/Ton 37.38 7.9 1.7 (2.6) DAX 8,967.51 1.7 (2.5) (14.0) LPG Butane (Arab Gulf)/Ton 53.50 4.1 (9.1) (2.9) FTSE 100 5,707.60 3.2 (2.4) (10.2) Euro 1.13 (0.6) 0.9 3.6 CAC 40 3,995.06 1.8 (4.0) (10.8) Yen 113.25 0.7 (3.1) (5.8) Nikkei 14,952.61 (4.1) (8.2) (16.3) GBP 1.45 0.2 0.0 (1.6) MSCI EM 711.24 (0.3) (3.8) (10.4) CHF 1.02 (0.5) 1.4 2.5 SHANGHAI SE Composite# 2,763.49 0.0 0.0 (22.9) AUD 0.71 0.0 0.6 (2.4) HANG SENG 18,319.58 (1.1) (5.0) (16.8) USD Index 95.94 0.4 (1.1) (2.7) BSE SENSEX 22,986.12 0.6 (7.1) (14.5) RUB 78.66 (1.7) 1.5 8.5 Bovespa 39,808.05 1.1 (4.1) (8.9) BRL 0.25 (0.2) (2.5) (1.1) RTS 689.90 2.8 (5.0) (8.9) 108.1 91.1 90.8