1. Page 1 of 6

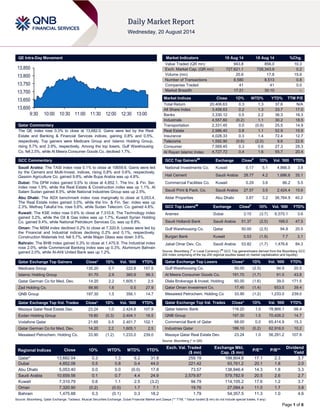

QE Intra-Day Movement

Qatar Commentary

The QE index rose 0.3% to close at 13,682.0. Gains were led by the Real

Estate and Banking & Financial Services indices, gaining 0.8% and 0.5%,

respectively. Top gainers were Medicare Group and Islamic Holding Group,

rising 5.7% and 2.9%, respectively. Among the top losers, Gulf Warehousing

Co. fell 2.5%, while Al Meera Consumer Goods Co. declined 1.7%.

GCC Commentary

Saudi Arabia: The TASI index rose 0.1% to close at 10659.6. Gains were led

by the Cement and Multi-Invest. indices, rising 0.8% and 0.6%, respectively.

Qassim Agriculture Co. gained 9.8%, while Bupa Arabia was up 4.8%.

Dubai: The DFM index gained 0.5% to close at 4,852.1. The Inv. & Fin. Ser.

index rose 1.9%, while the Real Estate & Construction index was up 1.1%. Al

Salam Sudan gained 8.5%, while National Industries Group was up 2.5%.

Abu Dhabi: The ADX benchmark index rose marginally to close at 5,053.4.

The Real Estate index gained 3.0%, while the Inv. & Fin. Ser. index was up

2.3%. Methaq Takaful Ins. rose 5.6%, while Sudan Telecom. Co. gained 4.8%.

Kuwait: The KSE index rose 0.6% to close at 7,310.8. The Technology index

gained 3.2%, while the Oil & Gas index was up 1.7%. Kuwait Syrian Holding

Co. gained 9.4%, while National Petroleum Services Co. was up 8.8%.

Oman: The MSM index declined 0.2% to close at 7,320.9. Losses were led by

the Financial and Industrial indices declining 0.2% and 0.1%, respectively.

Construction Materials Ind. fell 5.7%, while Majan Glass was down 3.6%.

Bahrain: The BHB index gained 0.3% to close at 1,475.9. The Industrial index

rose 2.0%, while Commercial Banking index was up 0.3%. Aluminium Bahrain

gained 2.0%, while Al-Ahli United Bank was up 1.2%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Medicare Group 135.20 5.7 222.8 157.5

Islamic Holding Group 91.70 2.9 360.9 99.3

Qatar German Co for Med. Dev. 14.20 2.2 1,605.1 2.5

Zad Holding Co. 88.90 1.6 0.5 27.9

QNB Group 197.30 1.5 356.1 14.7

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Mazaya Qatar Real Estate Dev. 23.24 1.0 2,424.8 107.9

Ezdan Holding Group 19.80 (0.3) 2,404.1 16.5

Vodafone Qatar 21.65 0.5 2,401.7 102.1

Qatar German Co for Med. Dev. 14.20 2.2 1,605.1 2.5

Mesaieed Petrochem. Holding Co. 33.90 (1.2) 1,233.0 239.0

Market Indicators 19 Aug 14 18 Aug 14 %Chg.

Value Traded (QR mn) 943.8 856.0 10.3

Exch. Market Cap. (QR mn) 727,621.1 726,343.9 0.2

Volume (mn) 20.6 17.8 15.6

Number of Transactions 8,580 8,513 0.8

Companies Traded 41 41 0.0

Market Breadth 17:21 30:10 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 20,406.63 0.3 1.3 37.6 N/A

All Share Index 3,458.63 0.2 1.3 33.7 17.0

Banks 3,330.12 0.5 2.2 36.3 16.3

Industrials 4,557.60 (0.2) 1.1 30.2 18.5

Transportation 2,331.45 0.0 (0.9) 25.5 14.9

Real Estate 2,986.40 0.8 1.1 52.9 15.9

Insurance 4,028.33 0.3 1.4 72.4 12.7

Telecoms 1,592.90 (0.6) (2.0) 9.6 22.6

Consumer 7,569.45 0.3 0.6 27.3 28.3

Al Rayan Islamic Index 4,727.72 0.4 1.6 55.7 20.4

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

National Investments Co. Kuwait 0.17 5.1 4,866.0 3.8

Hail Cement Saudi Arabia 28.77 4.2 1,686.6 35.1

Commercial Facilities Co. Kuwait 0.29 3.6 86.2 5.5

Saudi Print & Pack. Co. Saudi Arabia 27.57 3.5 2,424.4 15.6

Aldar Properties Abu Dhabi 3.87 3.2 36,764.9 40.2

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Aramex Dubai 3.15 (3.7) 6,575.1 3.6

Saudi Hollandi Bank Saudi Arabia 51.37 (2.5) 168.0 47.5

Gulf Warehousing Co. Qatar 50.00 (2.5) 94.9 20.5

Burgan Bank Kuwait 0.53 (1.9) 7.7 3.1

Jabal Omar Dev. Co. Saudi Arabia 53.82 (1.7) 1,476.6 84.3

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Gulf Warehousing Co. 50.00 (2.5) 94.9 20.5

Al Meera Consumer Goods Co. 191.70 (1.7) 91.0 43.8

Dlala Brokerage & Invest. Holding 60.00 (1.6) 39.0 171.5

Qatar Oman Investment Co. 17.45 (1.4) 653.5 39.4

Mesaieed Petrochem. Holding Co 33.90 (1.2) 1,233.0 239.0

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Qatar Islamic Bank 116.20 1.0 78,866.1 68.4

QNB Group 197.30 1.5 70,426.2 14.7

Commercial Bank of Qatar 68.00 0.0 65,414.9 15.3

Industries Qatar 186.10 (0.2) 62,916.0 10.2

Mazaya Qatar Real Estate Dev. 23.24 1.0 56,291.2 107.9

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 13,682.04 0.3 1.3 6.2 31.8 259.19 199,804.8 17.1 2.3 3.7

Dubai 4,852.06 0.5 0.8 0.4 44.0 221.42 93,761.2 20.1 1.8 2.0

Abu Dhabi 5,053.40 0.0 0.0 (0.0) 17.8 73.57 138,946.4 14.3 1.8 3.3

Saudi Arabia 10,659.56 0.1 0.7 4.4 24.9 2,579.87 579,782.9 20.5 2.6 2.7

Kuwait 7,310.79 0.6 1.1 2.5 (3.2) 94.79 114,105.2 17.6 1.2 3.7

Oman 7,320.90 (0.2) (0.0) 1.7 7.1 19.76 27,084.4 11.0 1.7 3.8

Bahrain 1,475.88 0.3 (0.1) 0.3 18.2 1.79 54,357.5 11.3 1.0 4.6

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

13,600

13,650

13,700

13,750

13,800

13,850

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 6

Qatar Market Commentary

The QE index rose 0.3% to close at 13,682.0. The Real Estate

and Banking & Financial Services indices led the gains. The

index rose on the back of buying support from non-Qatari

shareholders despite selling pressure from Qatari shareholders.

Medicare Group and Islamic Holding Group were the top

gainers, rising 5.7% and 2.9%, respectively. Among the top

losers, Gulf Warehousing Co. fell 2.5%, while Al Meera

Consumer Goods Co. declined 1.7%.

Volume of shares traded on Tuesday rose by 15.6% to 20.6mn

from 17.8mn on Monday. However, as compared to the 30-day

moving average of 17.1mn, volume for the day was 20.3%

higher. Mazaya Qatar Real Estate Dev. and Ezdan Holding

Group were the most active stocks, contributing 11.8% and

11.7% to the total volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Earnings and Global Economic Data

Earnings Releases

Company Market Currency

Revenue

(mn)2Q2014

% Change

YoY

Operating Profit

(mn) 2Q2014

% Change

YoY

Net Profit (mn)

2Q2014

% Change

YoY

Red Sea Housing Services

Co. (RSH)

Saudi SR – – – – 40.8 NA

NMC Health* UAE USD 314.3 – – – 40.9 26.6%

Source: Company data, DFM, ADX, MSM (* 1H2014 results)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

08/19 US Bureau of Labor Stat. CPI MoM July 0.10% 0.10% 0.30%

08/19 US Bureau of Labor Stat. CPI Ex Food and Energy MoM July 0.10% 0.20% 0.10%

08/19 US Bureau of Labor Stat. CPI YoY July 2.00% 2.00% 2.10%

08/19 US Bureau of Labor Stat. CPI Ex Food and Energy YoY July 1.90% 1.90% 1.90%

08/19 US Bureau of Labor Stat. CPI Core Index SA July 238.3 238.5 238.1

08/19 US Bureau of Labor Stat. CPI Index NSA July 238.3 238.3 238.3

08/19 US US Census Bureau Housing Starts July 1,093K 965K 945K

08/19 US US Census Bureau Housing Starts MoM July 15.70% 8.10% -4.00%

08/19 US US Census Bureau Building Permits July 1,052K 1,000K 973K

08/19 US US Census Bureau Building Permits MoM July 8.10% 2.80% -3.20%

08/19 EU European Central Bank ECB Current Account SA June 13.1B – 19.8B

08/19 EU European Central Bank Current Account NSA June 20.8B – 9.3B

08/19 UK UK ONS CPI MoM July -0.30% -0.20% 0.20%

08/19 UK UK ONS CPI YoY July 1.60% 1.80% 1.90%

08/19 UK UK ONS CPI Core YoY July 1.80% 1.90% 2.00%

08/19 UK UK ONS Retail Price Index July 256.0 256.2 256.3

08/19 UK UK ONS RPI MoM July -0.10% -0.10% 0.20%

08/19 UK UK ONS ONS House Price YoY June 10.20% 10.20% 10.40%

08/19 UK LBMA Silver Price London Silver Market Fixing 19-August – – 19.6

08/19 UK London Gold Market Fix. London Gold Market PM Fix 19-August 1,296.5 – 1,296.8

08/19 Italy Banca D'Italia Current Account Balance June 3,050M – 1,889M

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

Nakilat takes delivery of two mooring boats to boost its

towage unit – Nakilat (QGTS) has taken delivery of two 16

meter mooring boats built by Nakilat Damen Shipyards Qatar

(NDSQ) for towage operator Nakilat SvitzerWijsmuller (NSW).

The two Stan Tug 1606 mooring boats — Ras Al Allaj Qatar and

Al Esaiwed — are the first set of a seven-vessel order that

NDSQ is currently working on for NSW. These vessels will work

on a long-term charter for Qatar Petroleum and will be part of

the growing fleet of NSW vessels in the Port of Ras Laffan.

NSW already operates a fleet of 25 vessels at Ras Laffan and

another 5 vessels at Halul Island, performing around 12,500 tug

jobs per year in the Port of Ras Laffan. NDSQ is a JV between

Nakilat and Dutch shipbuilder Damen and is based at Erhama

Bin Jaber Al Jalahma Shipyard in Ras Laffan, Qatar. (Gulf-

Times.com)

ORDS adds Joyalukkas to its Nojoom partner network –

Ooredoo (ORDS) announced that Joyalukkas has joined as the

first jewelry retailer in its expanding Nojoom partner network.

Members can earn and redeem points at Joyalukkas Jewellery

Overall Activity Buy %* Sell %* Net (QR)

Qatari 60.99% 71.54% (99,594,486.66)

Non-Qatari 39.01% 28.46% 99,594,486.66

3. Page 3 of 6

retail outlets in Qatar as part of the Nojoom Loyalty Program.

Nojoom members can earn 1 Nojoom point for every QR8 spent

on gold jewelry or QR3 spent on diamond jewelry. As part of a

special offer to mark the launch of this partnership, Nojoom

members can also earn double points until November 18. (Gulf-

Times.com)

Halcrow to upgrade Qatar roads – Halcrow, a global full-

service consulting company under CH2M HILL, has been

awarded a call-off consultancy services contract to provide

professional road safety engineering, road design, quantity

surveying consultancy and contractor supervision services to the

Assets Affairs – Roads Operations & Maintenance Department

of the Public Works Authority (Ashghal). The new contract will

put Halcrow at the forefront of the program of initiatives outlined

in Qatar’s National Road Safety Action Plan, which sets Qatar

on a path toward an ambitious long-term vision of a safe road

transport system. (Peninsula Qatar)

TechSci Research: Qatar tire market to grow at 6% CAGR

till 2019 – Rising automobile sales, increasing demand for cost

effective Chinese tires and an imposition of ban on balloon tires

are the key trends emerging in the Qatari tire market. According

to a recent report by TechSci Research titled, "Qatar Tyre

Market Forecast & Opportunities – 2019'', the tire market in

Qatar is forecasted to grow at a CAGR of about 6% during

2014-19. Moreover, the retreading tire market in the country is

projected to outperform and grow at a CAGR of around 9%

during the same period. Sales of passenger vehicles,

commercial vehicles, construction equipment are expected to

increase over the next five years in Qatar, creating a positive

market outlook for the country's tire market. (Bloomberg)

International

Housing starts rebound in US as inflation eases – The

Commerce Department said home construction in the US

rebounded in July 2014 and the cost of living rose at a slower

pace, indicating that a strengthening US economy is yet to

generate a sustained pickup in inflation. A 15.7% jump took

housing starts to a 1.09mn annualized rate, which is the

strongest since November, halting a two-month slide.

Meanwhile, the Labor Department reported that the consumer

price index rose 0.1% in July after rising 0.3% in June. An

improving job market and cheaper borrowing costs are helping

revive the residential real estate, helping boost sales at

companies such as Home Depot Inc. As inflation continues to

run below the Federal Reserve’s target, it gives the central bank

room to keep interest rates low well after the projected end of its

bond-buying program in October. (Bloomberg)

UK inflation falls to 1.6% in July; 2014 rate rise less likely –

Inflation in Britain fell more than expected in July and the

surging house price growth also slowed in June, making it less

likely for the Bank of England (BoE) to raise interest rates this

year. According to official data, inflation dropped to 1.6% in July

from June's five-month high of 1.9%, pulling down the sterling to

a four-month low against the dollar. Economists had expected

consumer price inflation to tick down to 1.8%. Last week, the

BoE had curbed expectations for a rate rise in 2014 by slashing

forecasts for wage growth. Any remaining pressure to raise

record-low rates this year receded further after the recent data.

The first annual fall in factory-gate prices since 2009 underlined

the weakness in domestic inflation pressures. Still, the outlook

for inflation depends on estimates about the amount of slack left

in Britain's economy, something that divides members of the

BoE Monetary Policy Committee. (Reuters)

European gas reverses biggest drop since 2009 on Ukraine

– European natural gas prices are reversing their biggest slump

in five years as concern mounts for the tension between Russia

and Ukraine to disrupt flows to the region. Gas price for next

month’s delivery in the UK rallied 21% over the past six weeks

as Ukraine said it may ban OAO Gazprom, Europe’s biggest

supplier, from shipping the fuel through its territory because of

Russia’s support of separatists. The Russian company, which

meets 15% of European gas demand through Soviet-era

pipelines across Ukraine, halted supplies to its neighbor on June

16 due to a debt and price dispute. Gas storage in Ukraine is

less than half full and the nation began this month to limit

domestic use to conserve fuel. UK prices, the regional

benchmark, fell to their lowest since 2010 after a mild winter left

storage sites across the 28-nation European Union at their

fullest for this time of year since 2008. According to a forecast

by Societe Generale, wholesale prices for the next quarter will

be 11% higher than what companies are paying for that period

now. (Bloomberg)

Japanese exports rebound in tailwind for Abe’s policies –

Exports from Japan rose more than forecast in July, bouncing

back from two straight declines to support an economy that

contracted last quarter by the most since 2011. The finance

ministry said overseas shipments rose 3.9% from a year earlier.

That is higher than the median estimate for a 3.8% gain in a

Bloomberg News survey of 28 economists. Imports rose 2.3%,

leaving a deficit of 964bn yen. The rebound in shipments may

help Prime Minister Shinzo Abe to raise the sales tax again after

boosting it to 8% in April. The economy is forecast to expand at

an annualized 2.9% this quarter after contracting 6.8% in the

April-June period, as consumers and businesses cut spending

after the tax increase. (Bloomberg)

Bank of China doubles money for bad loans as growth

slows – The Bank of China Ltd. more than doubled its

provisions set aside for bad loans as profit growth cooled to the

slowest pace in five quarters due to weakness in the Chinese

economy. Based on half-yearly figures released by China’s

fourth-largest bank, provisions for potential soured debt climbed

to 12.7bn Yuan in the second quarter, up 116% from a year

earlier. Net income rose 8.5% to 44.4bn Yuan. The bank’s net

income compared well with the 44.9bn Yuan median estimated

in a Bloomberg News survey. The bank’s net interest margin

narrowed to 2.27% at the end of June from 2.29% at the end of

the first quarter. Non-performing loans amounted to 1.02% of

total advances, up from 0.98% in the previous quarter. Non-

performing loans surged to 85.9bn Yuan, the highest in more

than five years, as client companies struggled with repayments

in an economy at risk of the weakest full-year GDP growth since

1990. The nation’s lenders are already trading at the cheapest

P/E valuations of global banks. (Bloomberg)

Moody’s downgrades biggest South African lenders on ABL

collapse – Moody’s Investors Service downgraded the local-

currency ratings of South Africa’s four biggest lenders and kept

them on review for a further cut following the collapse of African

Bank Investments Ltd. (ABL). Moody’s said the local-currency

deposit ratings of Standard Bank Group Ltd., FirstRand Ltd.,

Nedbank Group Ltd. and Absa Bank Ltd., were cut one level to

Baa1, the third lowest investment grade, from A3. Standard

Bank’s issuer rating was lowered to Baa2 from Baa1. All ratings

of the four banks, including their long-term foreign-currency

ratings, were placed on review for a downgrade. Absa,

FirstRand and Nedbank’s senior unsecured debt was also cut

one level to Baa1. On August 10, the South African Reserve

Bank had placed ABL, an unsecured lender, under curatorship

after it reported a record loss and said it needed ZAR8.5bn of

capital. The rescue included a 10% impairment of ABL’s senior

and wholesale debt, a move that Moody’s said suggested the

4. Page 4 of 6

South African authorities will not fully protect creditors in the

case of a bank failure. (Bloomberg)

Regional

OPEC unruffled by oil price decline; expects market

rebound – OPEC is not worried about a slide in oil prices

toward $100 a barrel with current levels seen as acceptable for

producers while higher seasonal demand in the coming weeks

was expected to support the market. According to an OPEC

source, Saudi Arabia, Kuwait and the United Arab Emirates

could trim supply informally if needed, such as to make room for

a further recovery in Libya or to support prices. (Reuters)

Al-Eqtisadiah: Saudi banks’ distressed loans down 4% to

SR16bn in 2Q2014 – According to a report by Al-Eqtisadiah

daily, the volume of non-performing (distressed) loans in the

Saudi banks dropped by 4% to SR16bn by the end of 2Q2014,

as compared to SR16.8bn in 2Q2013. The coverage of

accumulated provisions to the distressed loans in the Saudi

banks grew by 165% in 2Q2014 as compared to 157% in

2Q2013. The accumulated provisions grew by 1% to SR26.5bn

as compared to SR26.3bn in the comparable periods. The Saudi

banks set aside provisions worth SR1.33bn in 2Q2014 as

compared to SR1.26bn in 2Q2013, reflecting an increase of 5%.

(GulfBase.com)

Zain KSA inaugurates new flagship in Saudi Arabia – Mobile

Telecommunications Company Saudi Arabia (Zain KSA) has

inaugurated the latest flagship in Albatha’a, Riyadh, to be a part

of its many main flagships around Saudi Arabia. This new

flagship enables the company to expand and reach more

subscribers in order to provide its distinguished services in the

most modern ways. Zain’s main flagships offer subscribers

solutions for voice and data exchange services, as part of its

efforts to raise the quality of service for subscribers.

(GulfBase.com)

Sales of pharma products poised to exceed SR26bn in 2018

– The pharmaceutical market in Saudi Arabia has registered

significant growth over the years and sales of pharmaceutical

products are poised to exceed SR26.25bn by 2018 as compared

to sales of 2013, which were valued at SR4.4bn, said Saudi

daily newspaper Al-Eqtisadiah, quoting a study by Research and

Markets. The report said that the growth was driven by various

factors such as ever-increasing aging population, demographic

changes, rise in new lifestyle-related diseases, growing

spending of Saudis, and government initiatives to promote local

pharmaceutical firms. The Saudi Arabia pharmaceutical market

has accounted for more than 50% sales of all pharmaceutical

products in the GCC (Gulf Cooperation Council) region. The

pharmaceutical market is currently estimated at SR9.37bn. A

sizable number of new local drug companies have lined up

plans to enter the market, notably many foreign firms are keen

to set up drug plants in Saudi Arabia coupled with the expansion

plans of the operating companies. (GulfBase.com)

KAEC signs contract exceeding SR15mn – King Abdullah

Economic City (KAEC) has entered into a contract worth more

than SR15mn with Saud Barik Al-Subhi & Partners Company to

develop the initial phase of the road that will connect the

Haramain inner-city railway station with the Business Park at

Bay La Sun district and KAEC residential communities, thereby

enhancing access to the city via the Jeddah-Yanbu highway.

The initial phase of the project is expected to finish by 2015-end,

while the expected overall total cost of the project is worth

around SR235mn. (GulfBase.com)

Emirates Steel focuses on value-added products – Emirates

Steel is set to expand its global presence and add more value-

added steel to its product basket. The company plans to

sharpen its focus on high-margin, high-strength value-added

products (VAPs). VAPs are mainly finished steel and are termed

so depending on their treatment or their end use. The products

vary from sheet piles to high silica wire rod to long steel bars to

alloy steel. The end-users are primarily the construction and

fabrication sectors. Emirates Steel is also developing new

grades with higher mechanical properties to meet the market

demand in the oil & gas sector. (GulfBase.com)

Walaa files capital increase request to Saudi CMA – Saudi

United Cooperative Insurance Company (Walaa), further to its

earlier announcement about appointing financial advisor Al

Jazira Capital for the proposed rights issue, said it has filed an

application to the Capital Markets Authority (CMA) for approval

in relation to its proposed rights issue. (Tadawul)

Asharq al-Awsat: Saudi Arabia to impose 20% foreign

ownership limit on stocks – According to Saudi daily

newspaper Asharq al-Awsat, overseas investors in the Saudi

Arabian stock market will face restrictions, including a 20%

ceiling on combined foreign ownership of any listed stock.

Foreign funds will also not be permitted to hold more than 10%

of the market value of Saudi stocks. Foreigners are currently

limited to indirect investment through swaps and exchange-

traded funds. The foreign ownership limits could reduce Saudi

Arabia's weighting in major international equity indexes

compiled by companies such as the MSCI, if the index compilers

choose to include the country after foreign investors are allowed

in. (Reuters)

StanChart: Foreign banks struggling to compete in Saudi

Arabia – According to Standard Chartered Capital Saudi Arabia

(StanChart), local lenders in Saudi Arabia are dominating the

market, prompting overseas banks to surrender their licenses as

they struggle to compete. Some international banks have started

shrinking in Saudi Arabia even as the country plans to open its

$577bn stock exchange to direct international investment.

Barclays Saudi Arabia cancelled its license to conduct securities

business in June 2014, the same month that Goldman Sachs

ended its license for custody, underwriting and dealing as an

agent. Saudi Arabia's 12 domestic lenders benefit from being

able to offer a full range of banking services, while most foreign

banks are licensed by the Saudi Capital Market Authority to

conduct limited activities. (GulfBase.com)

Savola says had initial talks with Americana shareholder –

Saudi Arabian Savola Group said it had conducted preliminary

talks with one of the largest shareholders in Kuwait Food

Company (Americana) on a potential purchase of that

shareholder's stake. Savola said it had signed a non-disclosure

agreement with the shareholder, and repeated that it had not

entered into any binding commitments. However, it did not name

the shareholder. (Reuters)

EC Harris: Construction projects worth $315bn to bolster

UAE's economic activity – According to EC Harris' 2014

International Focus on the UAE report, the UAE's construction

market is expected to return to near full capacity with a number

of megaprojects in the pipeline and the ramping up of social

infrastructure spend. The volume of announced and planned

projects in the UAE in 2014 is expected to be worth $315bn, and

as of May 2014, $212bn worth of construction projects were

under implementation. According to EC Harris' Construction

Cost Index, construction prices in the UAE are set to rise by 4%-

5% during the year and approximately 6% in 2015.

(GulfBase.com)

Abraaj targets North Africa investments amid deal spree –

The buyout firm focused on emerging markets, Abraaj Group

5. Page 5 of 6

Ltd. (Abraaj), is targeting more acquisitions in North Africa to

benefit from rising demand for investments in health care,

consumer products and education. Abraaj announced six deals

in the region in 1H2014 and plans four more investments in

2014 with an average value of $50mn to $100mn. In the Gulf

region, Abraaj’s strategy is to focus on larger deals and the firm

would seek to make one or two investments in a year.

(Bloomberg)

Dubai creates new fund class to lure asset managers –

Dubai is changing its financial rules in an effort to attract more

asset managers such as hedge funds and private equity funds –

to base themselves in the emirate. The rules create a new class

of funds that can be domiciled in the Dubai International

Financial Center, facing less stringent regulation and thus lower

costs than existing funds. The new rules from the Dubai

Financial Services Authority seek to cut costs by creating a

class of funds that can be offered only to experienced

professional investors and so need less regulation. (Reuters)

DDF reprices $1.75bn loan for second time – Airport retailer

Dubai Duty Free (DDF) is repricing a $1.75bn syndicated loan

for the second time in just over a year to obtain more favorable

terms, a fresh sign of banks' willingness to lend cheaply to the

emirate. The six-year loan, originally signed in July 2012, was

split between dirham and US dollar-denominated tranches, both

priced at 325 basis points (bps) over the London interbank

offered rate. On August 19, DDF said it was repricing the dirham

tranche further to 150 bps and the dollar tranche to 175 bps.

(Reuters)

NBAD subsidiary in Americas renamed – National Bank of

Abu Dhabi (NBAD) has renamed its wholly-owned subsidiary in

the Americas to NBAD Americas. NBAD Americas serves UAE

investors who invest in the US, and US companies who do

business in the UAE and other countries where NBAD has a

presence. (GulfBase.com)

Aldar Properties: Strong demand for bulk lease deals –

Aldar Properties sees a strong demand for long-term, bulk lease

deals from corporate clients. The lease agreements signed with

corporate clients range from two to 30 years and currently

include 2,120 units, providing Aldar Properties with long-term

security of income. Most of the lease agreements comprise over

100 units, the largest reaching over 600 units. 60% of the units

at Al Rayyana and 45% of the apartments at The Arc are

currently leased through bulk deals. (GulfBase.com)

FGB appoints head of corporate finance advisory services –

First Gulf Bank (FGB) has appointed Michael Aissaoui as head

of its corporate finance advisory services. He will oversee the

expansion of the bank's advisory activities for clients regionally

and globally. (Reuters)

KIC to launch KD5mn investment fund – Kuwait Investment

Company (KIC) is planning to launch an investment fund in the

Gulf finance markets compatible with the Islamic Shari’ah (law).

KIC’s CEO Bader Nasser Al Subaiee said that the fund would be

launched with an initial capital of KD5mn. The company earned

KD5.2mn in 1H2014, at a rate of 9.53 fils. Shareholders’ equity

rose 6% to KD132.3mn as compared to KD124.8mn in 1H2013.

(GulfBase.com)

NBK’s BoD elects Chairman and Vice Chairman – National

Bank of Kuwait’s (NBK) board of directors has elected Nasser

Musaed Al-Sayer as the Chairman of NBK Group following the

demise of the long-serving Chairman Mohammad Abdul

Rahman Al-Bahar. The board has also elected Ghassan Ahmed

Saoud Al-Khalid as the Vice Chairman. (GulfBase.com)

Al Anwar’s associate Al Maha Ceramics plans IPO – Al

Anwar Holding announced that its associate, Al Maha Ceramics

has proposed to open the IPO for subscription between

September 16, 2014 and October 15, 2014. This is subject to

approval from the capital market authority (CMA) on the

prospectus and completion of necessary formalities related to

IPO. (MSM)

BP Oman to boost drilling in Khazzan project – BP Oman is

planning to increase its drilling activity in the Khazzan project to

unlock the massive unconventional gas reserves in the field. Till

date more than 15 wells have been drilled and five or six more

wells will be drilled by the end of 2014. Additionally, the

company officially inaugurated its Technicians Training Center in

Ghala to recruit and train over 100 Omani technicians over a

period of five years to support the field operations at the

Khazzan project. (GulfBase.com)

Double digit growth foreseen in Salalah Port general cargo

business – According to the CEO of Port of Salalah, David

Gledhill, ongoing investment in multimodal transport

infrastructure in Dhofar Governorate augurs well for volume

growth at Port of Salalah, especially in the general cargo

segment. But its long-term success hinges on a robust

commitment to its timely expansion and modernization.

(GulfBase.com)

Bahrain construction sector grows 40% – Bahrain’s

construction sector has grown by 40% since January. The

figures were released as Bahrain steps up preparations for the

annual GCC Construction Conference in October. (Bloomberg)

6. Contacts

Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian

Head of Research Senior Research Analyst Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509

saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa

Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC

Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025

sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

190.0

200.0

210.0

Jul-10 Jul-11 Jul-12 Jul-13 Jul-14

QE Index S&P Pan Arab S&P GCC

0.1%

0.3%

0.6%

0.3%

(0.2%)

0.0%

0.5%

(0.3%)

(0.1%)

0.1%

0.3%

0.5%

0.7%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,295.68 (0.2) (0.7) 7.5 DJ Industrial 16,919.59 0.5 1.5 2.1

Silver/Ounce 19.44 (1.0) (0.7) (0.2) S&P 500 1,981.60 0.5 1.4 7.2

Crude Oil (Brent)/Barrel (FM

Future)

101.56 (0.0) (1.9) (8.3) NASDAQ 100 4,527.51 0.4 1.4 8.4

Natural Gas (Henry

Hub)/MMBtu

3.84 2.2 2.0 (11.5) STOXX 600 335.49 0.6 1.7 2.2

LPG Propane (Arab Gulf)/Ton 102.25 0.9 (0.4) (19.2) DAX 9,334.28 1.0 2.7 (2.3)

LPG Butane (Arab Gulf)/Ton 120.00 0.3 (1.4) (11.6) FTSE 100 6,779.31 0.6 1.3 0.4

Euro 1.33 (0.3) (0.6) (3.1) CAC 40 4,254.45 0.6 1.9 (1.0)

Yen 102.92 0.3 0.5 (2.3) Nikkei 15,449.79 0.8 0.9 (5.2)

GBP 1.66 (0.7) (0.5) 0.4 MSCI EM 1,084.45 0.7 0.9 8.2

CHF 1.10 (0.3) (0.7) (1.8) SHANGHAI SE Composite 2,245.33 0.3 0.8 6.1

AUD 0.93 (0.2) (0.2) 4.3 HANG SENG 25,122.95 0.7 0.7 7.8

USD Index 81.88 0.4 0.6 2.3 BSE SENSEX 26,420.67 0.1 1.2 24.8

RUB 36.17 0.3 (0.0) 10.1 Bovespa 58,449.29 1.5 2.6 13.5

BRL 0.44 0.4 0.5 5.1 RTS 1,251.69 0.7 1.6 (13.2)

196.6

163.7

147.5