More Related Content

What's hot

What's hot (17)

Viewers also liked

Similar to Daily livestock report mar 25 2013

Similar to Daily livestock report mar 25 2013 (20)

More from joseleorcasita

More from joseleorcasita (20)

Daily livestock report mar 25 2013

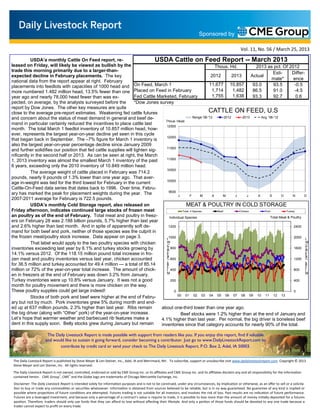

- 1. Sponsored by Vol. 11, No. 56 / March 25, 2013 USDA’a monthly Cattle On Feed report, re- USDA Cattle on Feed Report -- March 2013 leased on Friday, will likely be viewed as bullish by the Thous. Hd. 2013 as pct. Of 2012 trade this morning primarily due to a larger-than- Esti- Differ- expected decline in February placements. The key 2012 2013 Actual mate* ence national data from the report appear at right. February placements into feedlots with capacities of 1000 head and On Feed, March 1 11,677 10,857 93.0 93.5 -0.5 more numbered 1.482 million head, 13.5% fewer than one Placed on Feed in February 1,714 1,482 86.5 91.0 -4.5 year ago and nearly 78,000 head fewer than was ex- Fed Cattle Marketed, February 1,755 1,638 93.3 92.7 0.6 pected, on average, by the analysts surveyed before the *Dow Jones survey report by Dow Jones. The other key measures are quite close to the average pre-report estimates. Weakening fed cattle futures CATTLE ON FEED, U.S and concern about the status of meat demand in general and beef de- Range '08-'12 2012 2013 Avg. '08-'12 Thous. Head mand in particular certainly reduced the incentives to place cattle last 12500 month. The total March 1 feedlot inventory of 10.857 million head, how- ever, represents the largest year-on-year decline yet seen in this cycle 12000 that began back in September. The –7% figure for March 1 inventory is also the largest year-on-year percentage decline since January 2009 11500 and further solidifies our position that fed cattle supplies will tighten sig- nificantly in the second half or 2013. As can be seen at right, the March 11000 1, 2013 inventory was almost the smallest March 1 inventory of the past 6 years, exceeding only the 2010 inventory of 10.849 million head. 10500 The average weight of cattle placed in February was 714.2 pounds, nearly 9 pounds of 1.3% lower than one year ago. That aver- 10000 age in-weight was tied for the third lowest for February in the current Cattle-On-Feed data series that dates back to 1996. Over time, Febru- 9500 ary has marked the peak for placement weights during the year. The J F M A M J J A S O N D 2007-2011 average for February is 722.5 pounds. USDA’s monthly Cold Storage report, also released on MEAT & POULTRY IN COLD STORAGE Friday afternoon, indicates continued large stocks of frozen meat Total, 4 Species Beef Chicken Pork Turkey an poultry as of the end of February. Total meat and poultry in freez- Individual Species Total Meat & Poultry ers on February 28 was 2.188 billion pounds, 5.7% higher than last year and 2.6% higher than last month. And in spite of apparently soft de- 1200 2400 mand for both beef and pork, neither of those species was the culprit in the frozen meat/poultry stock increase. Data appear on page 3. t 1000 . 2000 t . That label would apply to the two poultry species with chicken W W C C inventories exceeding last year by 6.1% and turkey stocks growing by T 800 R 1600 T R / / 14.1% versus 2012. Of the 118.15 million pound total increase in fro- c r c r a a zen meat and poultry inventories versus last year, chicken accounted C 600 , . 1200 C , . for 36.5 million and turkey accounted for 49.4 million — a total of 85.14 s s b b L L million or 72% of the year-on-year total increase. The amount of chick- . l i 400 800 . l i M M en in freezers at the end of February was down 3.2% from January. Turkey inventories were up 10.8% versus January. It was not a good 200 400 month for poultry movement and there is more chicken on the way. These poultry supplies could get large indeed! 0 0 00 01 02 03 04 05 06 07 08 09 10 11 12 13 Stocks of both pork and beef were higher at the end of Febru- ary but not by much. Pork inventories grew 5% during month and end- ed up at 637 million pounds, 2.3% higher than last year. Ribs remain about one-third lower than one year ago. the big driver (along with “Other” pork) of the year-on-year increase. Beef stocks were 1.2% higher than at the end of January and Let’s hope that warmer weather and barbecued rib features make a 4.1% higher than last year. Per normal, the big driver is boneless beef dent in this supply soon. Belly stocks grew during January but remain inventories since that category accounts for nearly 90% of the total. The Daily Livestock Report is made possible with support from readers like you. If you enjoy this report, find if valuable and would like to sustain it going forward, consider becoming a contributor. Just go to www.DailyLivestockReport.com to contribute by credit card or send your check to The Daily Livestock Report, P.O. Box 2, Adel, IA 50003. The Daily Livestock Report is published by Steve Meyer & Len Steiner, Inc., Adel, IA and Merrimack, NH. To subscribe, support or unsubscribe visit www.dailylivestockreport.com. Copyright © 2013 Steve Meyer and Len Steiner, Inc. All rights reserved. The Daily Livestock Report is not owned, controlled, endorsed or sold by CME Group Inc. or its affiliates and CME Group Inc. and its affiliates disclaim any and all responsibility for the informa on contained herein. CME Group®, CME® and the Globe logo are trademarks of Chicago Mercan le Exchange, Inc. Disclaimer: The Daily Livestock Report is intended solely for informa on purposes and is not to be construed, under any circumstances, by implica on or otherwise, as an offer to sell or a solicita‐ on to buy or trade any commodi es or securi es whatsoever. Informa on is obtained from sources believed to be reliable, but is in no way guaranteed. No guarantee of any kind is implied or possible where projec ons of future condi ons are a empted. Futures trading is not suitable for all investors, and involves the risk of loss. Past results are no indica on of future performance. Futures are a leveraged investment, and because only a percentage of a contract’s value is require to trade, it is possible to lose more than the amount of money ini ally deposited for a futures posi on. Therefore, traders should only use funds that they can afford to lose without affec ng their lifestyle. And only a por on of those funds should be devoted to any one trade because a trader cannot expect to profit on every trade.

- 2. Sponsored by Vol. 11, No. 56 / March 25, 2013 USDA Cold Storage Report March 22, 2013 Product Quantity in All Warehouses Current as pct. of: 2/28/12 1/31/13 2/28/13 2/28/12 1/31/13 Chicken -------------- Thous. Lbs. ---------------- Whole Chickens 13937 18,741 16,372 117.5 87.4 Hens, Mature Chickens 4051 3,474 1,505 37.2 43.3 Breasts & Breast Meat 122332 129,741 127,276 104.0 98.1 Drumsticks 15040 17,032 12,824 85.3 75.3 Leg Quarters 94769 116,367 109,227 115.3 93.9 Legs 9715 13,055 10,020 103.1 76.8 Thigh & Thigh Quarters 9620 8,836 7,673 79.8 86.8 Thigh Meat 20834 17,914 17,627 84.6 98.4 Wings 33732 59,737 62,788 186.1 105.1 Paws and Feet 27681 22,546 19,684 71.1 87.3 Other 247987 250,105 251,226 101.3 100.4 Total Chicken 599,698 657,548 636,222 106.1 96.8 Turkey Whole Turkeys 141,002 146,967 171,734 121.8 116.9 Toms (Whole) 59,607 68,418 83,145 139.5 121.5 Hens (Whole) 81,395 78,549 88,589 108.8 112.8 Breasts 59,759 63,914 66,800 111.8 104.5 Legs 21,533 20,930 19,683 91.4 94.0 Mech. Deboned Turkey 10,427 9,660 13,036 125.0 134.9 Other Turkey 36,041 33,232 30,451 84.5 91.6 Unclassified 80,815 85,315 97,229 120.3 114.0 Total Turkey 349,577 360,018 398,933 114.1 110.8 Ducks 2,222 1,444 1,482 66.7 102.6 Total Poultry 951,497 1,019,010 1,036,637 108.9 101.7 Frozen Pork Picnics, Bone-in 12,068 12,267 15,581 129.1 127.0 Hams, Total 110,238 108,450 110,506 100.2 101.9 Bone-in 55,591 50,539 53,462 96.2 105.8 Boneless 3/ 54,647 57,911 57,044 104.4 98.5 Bellies 61,577 36,425 42,667 69.3 117.1 Loins, Total 43,440 43,989 41,867 96.4 95.2 Bone-in 14,253 13,755 15,083 105.8 109.7 Boneless 4/ 29,187 30,234 26,784 91.8 88.6 Ribs 5/ 96,043 114,370 122,620 127.7 107.2 Butts 27,822 31,091 28,640 102.9 92.1 Trimmings 6/ 64,964 57,826 64,328 99.0 111.2 Other 7/ 94,597 109,891 111,654 118.0 101.6 Variety Meats 8/ 37,466 28,109 32,416 86.5 115.3 Unclassified 9/ 74,458 64,007 66,414 89.2 103.8 Total Pork 622,673 606,425 636,693 102.3 105.0 Frozen Beef Boneless 1/ 412,908 420,786 433,597 105.0 103.0 Beef Cuts 2/ 57,900 63,824 56,716 98.0 88.9 Total Beef 470,808 484,610 490,313 104.1 101.2 Other Meat Veal 4,363 5,012 4,858 111.3 96.9 Lamb & Mutton 20,851 18,768 19,841 95.2 105.7 Total Other Meat 25,214 23,780 24,699 98.0 103.9 Total Meat 1,118,695 1,114,815 1,151,705 103.0 103.3 Total Meat & Poultry 2,070,192 2,133,825 2,188,342 105.7 102.6

- 3. Sponsored by Vol. 11, No. 56 / March 25, 2013 PRODUCTION AND PRICE SUMMARY Week Ending 3/23/2013 Current Pct. Pct. Pct. Item Units Week Last Week Change Last Year Change YTD Change Total Meat & Poultry Prod. Million lbs. 1693.7 1713.7 -1.17% 1683.6 0.60% 19,394 0.34% C FI Slaughter Thou. Head 601 606 -0.83% 603 -0.32% 7,041 -3.38% A FI Cow Slaughter Thou. Head 123.7 116.9 5.87% 124.6 -0.72% 1,228 -2.11% T Avg. Live Weight Lbs. 1315 1312 0.23% 1297 1.39% 1,324 1.34% T Avg. Dressed Weight Lbs. 796 798 -0.25% 787 1.14% 799 1.49% L Beef Production Million Lbs. 476.9 482.3 -1.12% 473.6 0.70% 5,577 -2.57% E Live Fed Steer $/cwt live wt. 124.77 126.66 -1.50% 126.59 -1.44% Dressed Steer $/cwt carcass 197.71 200.46 -1.37% 203.15 -2.68% & OKC Feeder Steer 700-800 Lbs. 139.10 136.65 1.80% 157.18 -11.50% Beef Cutout 600-750 Choice 193.57 196.75 -1.62% 189.63 2.08% B Hide/Offal $/cwt live wt. 14.25 13.96 2.08% 13.71 3.94% E Rib Choice 287.08 286.18 0.31% 282.41 1.65% E Round Choice 167.72 172.50 -2.77% 160.51 4.49% F Chuck Choice 168.91 173.71 -2.76% 151.63 11.40% Trimmings, 50% Fresh 88.09 88.05 0.05% 89.23 -1.28% Trimmings, 90% Fresh 219.41 219.19 0.10% 218.89 0.24% H FI Slaughter Thou. Head 2176 2203 -1.23% 2132 2.06% 25,476 -1.12% O FI Sow Slaughter Thou. Head 57.0 54.9 3.68% 54.8 3.98% 556 -0.19% G Avg. Dressed Weight Lbs. 208 207 0.48% 209 -0.48% 208 -0.68% S Pork Production Million Lbs. 451.7 457 -1.16% 445.4 1.41% 5,285 -1.69% Iowa-S. Minn. Direct Avg. 72.36 74.49 -2.86% 84.37 -14.23% & Natl. Base Carcass Price Weighted Avg. 75.74 76.42 -0.89% 84.82 -10.71% Natl. Net Carcass Price Weighted Avg. 78.17 78.83 -0.84% 87.29 -10.45% P Pork Cutout 200 Lbs 77.98 78.46 -0.61% 80.50 -3.13% O Hams Primal Cutout 56.50 58.30 -3.09% 61.34 -7.89% R Loins Primal Cutout 86.15 87.28 -1.29% 97.68 -11.80% K Trimmings, 72% Lean Fresh 53.00 53.61 -1.14% 59.29 -10.61% Bellies Primal Cutout 128.69 128.68 0.01% 102.27 25.83% C Young Chicken Slaughter* Million Head 151.26 153.39 -1.39% 153.06 -1.17% 1,663 1.10% H Avg. Weight Lbs., RTC 4.37 4.34 0.51% 4.28 2.09% 4.3 1.86% I Broiler Production Million Lbs., RTC 660.4 666.2 -0.88% 654.5 0.89% 7,371 4.34% C Eggs Set Million 200.2 199.4 0.42% 197.6 1.34% 2,179 1.48% K Chicks Placed Million Head 164.9 164.8 0.02% 163.0 1.14% 1,796 0.93% E 12-City Broiler Composite 106.68 107.78 -1.00% 91.82 16.20% N Georgia Dock Broiler 2.5-3 Lbs. 101.86 101.69 0.20% 92.34 10.30% Northeast Breast Skinlss/Bonelss 148.8 145.48 2.30% 134.51 10.60% Northeast Leg Quarters 66.85 66.59 3.00% 72.10 -6.90% T Young Turkey Slaughter* Million Head 4.15 4.31 -3.78% 4.45 -6.74% 46.4 0.03% U Avg. Weight Lbs. 25.24 25.08 0.64% 24.74 2.00% 25.1 -0.26% R Turkey Production Million Lbs. 104.7 108.2 -3.17% 110.1 -4.87% 1,161 -0.28% K Eastern Region Hen 8-16 Lbs. 95.50 95.50 0.00% 104.5 -8.60% F Corn, Omaha $ per Bushel 7.66 7.54 1.59% 6.50 17.94% E DDGS, Minnesota $ per ton 257.50 257.50 0.00% 201.50 27.79% E Wheat, Kansas City $ per Bushel 7.35 7.20 2.08% 6.68 10.03% D Soybeans, S. Iowa $ per Bushel 14.87 14.81 0.41% 13.57 9.50% SB Meal, 48% Central Illinois $ per Ton 435.90 437.00 -0.25% 366.10 19.10% * Chicken & turkey slaughter, production and prices are 1 week earlier than the date at the top of this table. Cow & sow slaughter are for 2 weeks earlier