Download to read offline

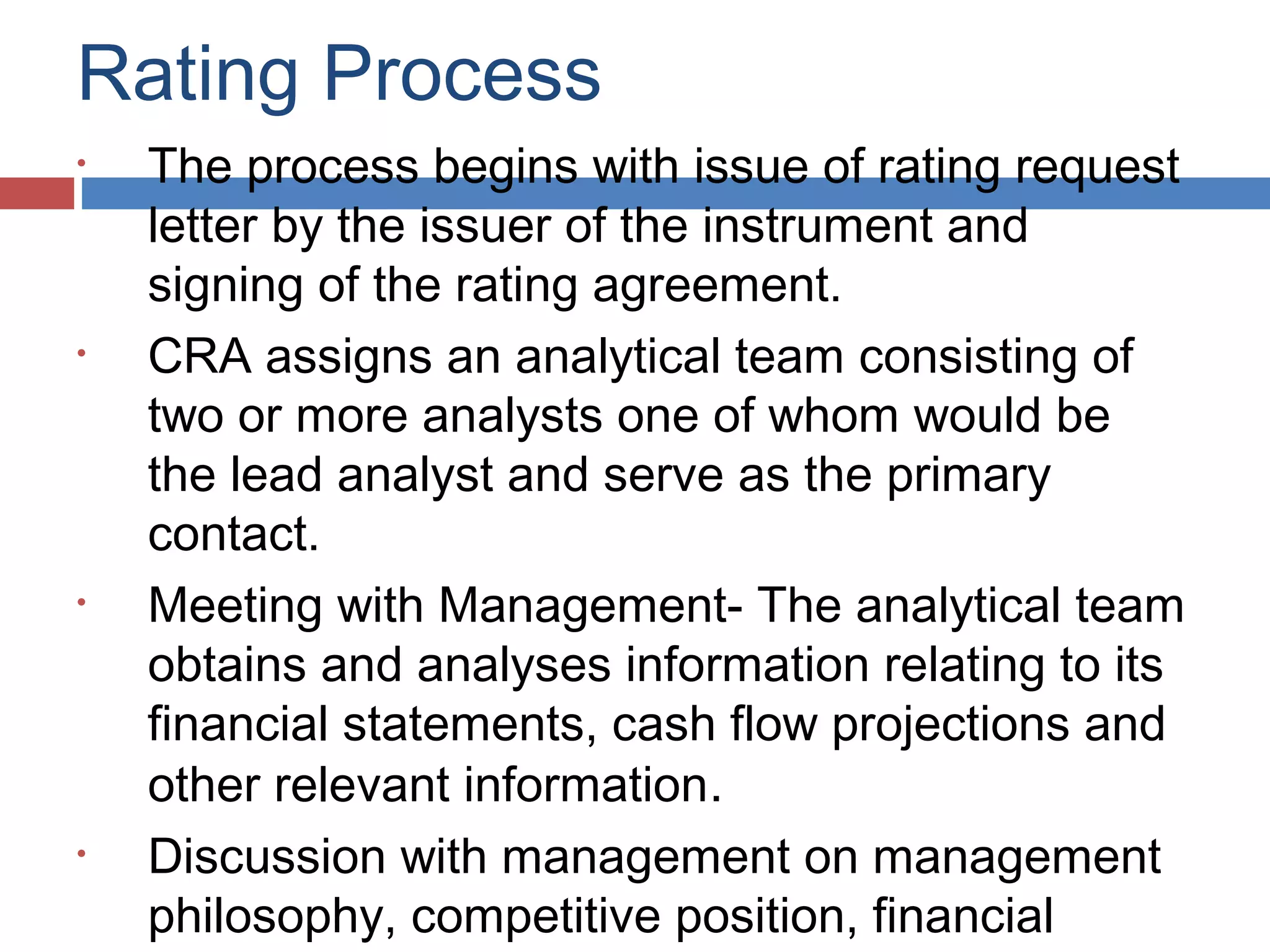

![Rating Process [Contd.]

Discussions on financial projections based on

objectives and growth plan , risks and

opportunities.

Rating committee- after meeting with the

management the analysts present their report

to a rating committee which then decides on

the rating.

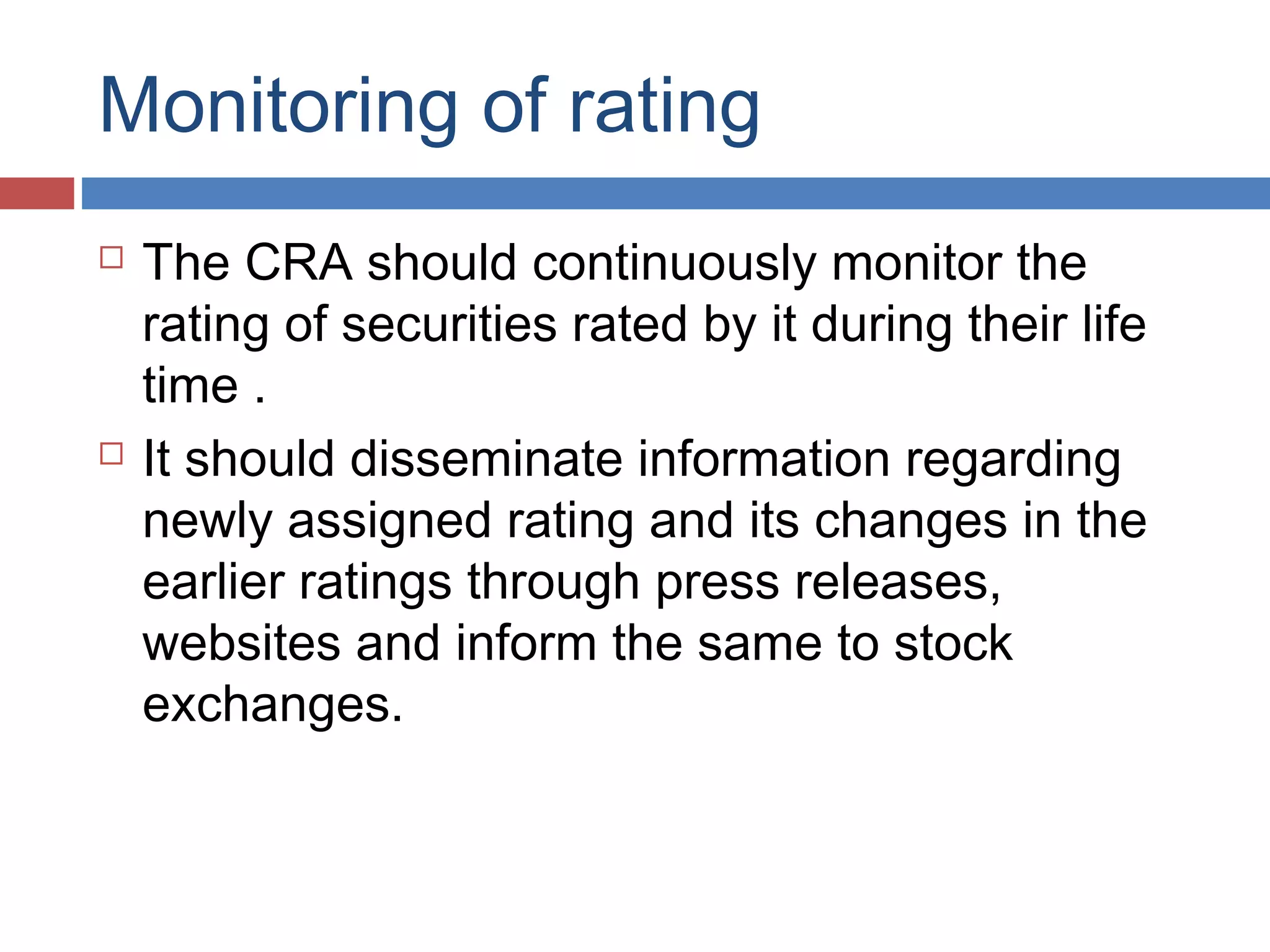

After the committee has assigned the rating,

the rating decision is communicated to the

issuer, with reasons or rationale supporting the

rating.

Dissemination to the Public: Once the issuer](https://image.slidesharecdn.com/creditrating-150311220821-conversion-gate01/75/Credit-rating-15-2048.jpg)

The document explains the concept of credit ratings, which assess the creditworthiness of individuals, corporations, or countries based on their financial history. It details the regulatory framework for credit rating agencies in India, including the requirements for registration and the factors influencing successful credit ratings. Additionally, it outlines the rating process, methodologies, symbols used to denote ratings, and specific considerations for various sectors such as financial services.