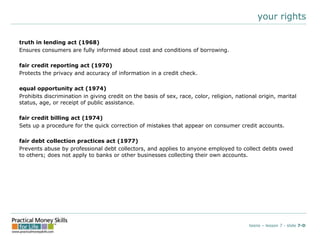

This document discusses advantages and disadvantages of credit, the three Cs of creditworthiness (character, capital, and capacity), responsibilities and rights of credit users, how to build a credit history, how to read a credit report, types of credit, and how much debt one can reasonably afford based on a 20/10 rule of thumb. It is a teaching document about credit for teenagers.

![Debt and Credit Management [Autosaved].PPT](https://cdn.slidesharecdn.com/ss_thumbnails/debtandcreditmanagementautosaved-241107201915-4ccebcf5-thumbnail.jpg?width=640&height=640&fit=bounds)