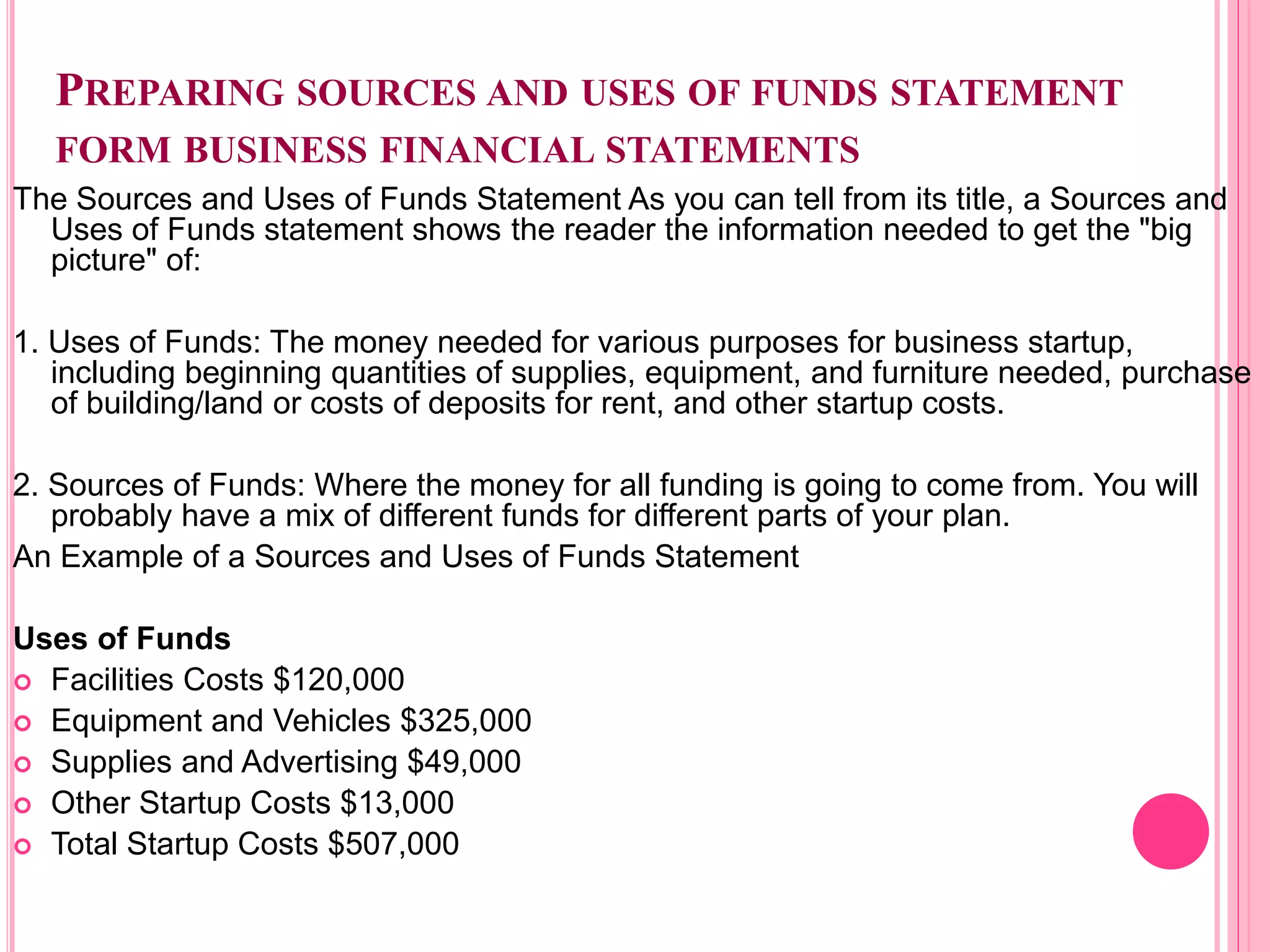

The document discusses various topics related to providing loans to businesses and consumers by banks. It covers the types of loans banks offer like real estate loans, personal loans, and educational loans. It also discusses factors that influence the growth and mix of bank loans, regulations around lending, establishing a written loan policy, the lending process, credit analysis, sources of information about loan customers, lending to business firms, analyzing business loan applications, preparing sources and uses of funds statements, and pricing business loans.