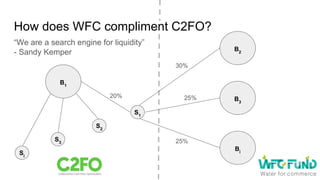

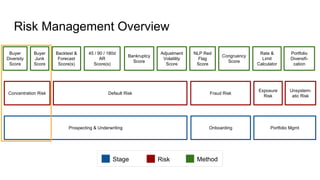

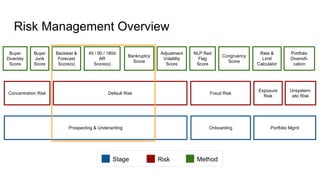

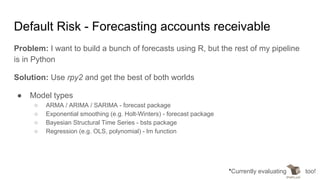

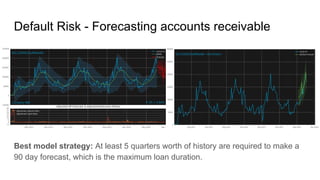

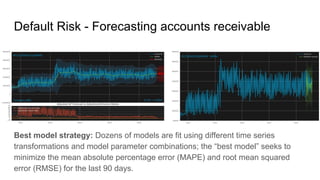

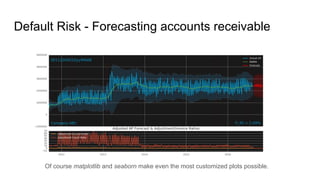

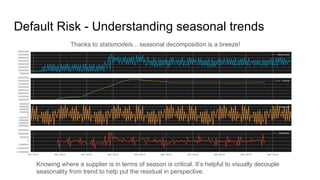

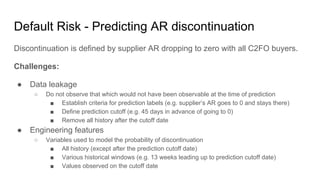

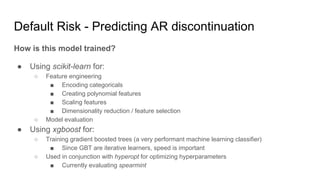

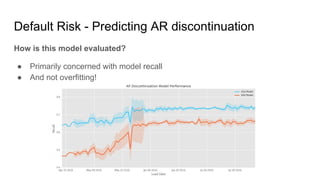

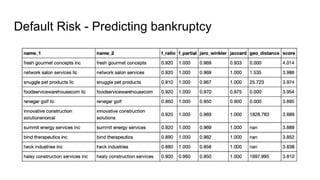

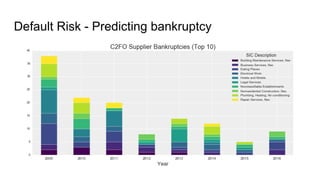

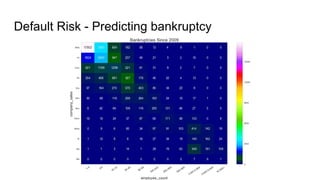

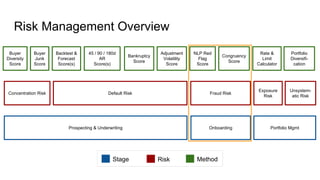

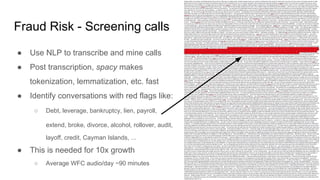

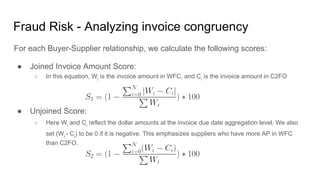

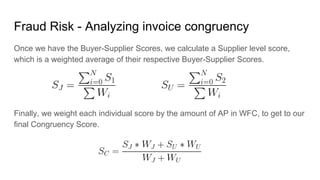

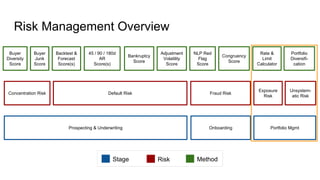

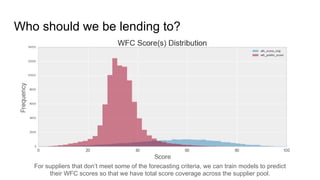

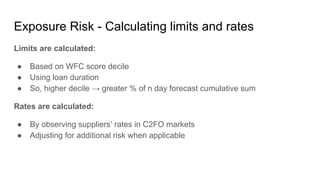

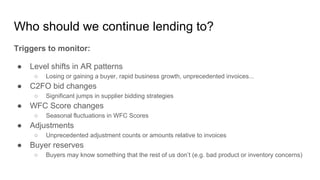

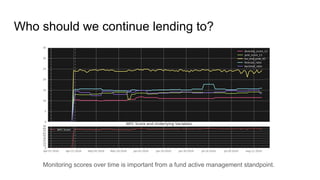

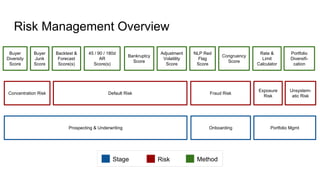

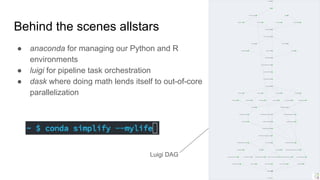

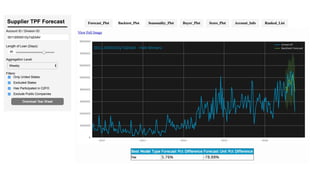

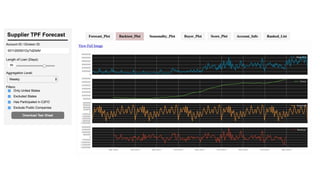

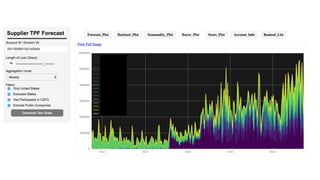

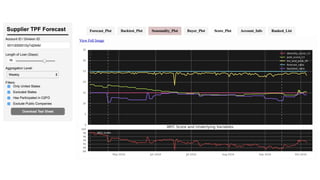

The document outlines the development of a contemporary risk management system utilizing Python, focusing on two key platforms: C2FO, which facilitates collaborative cash flow optimization for buyers and suppliers, and WFC, a lending platform for small businesses. It discusses various risk management strategies and tools for prospecting, underwriting, and evaluating default risks, including advanced data analysis techniques and machine learning models. Ultimately, it emphasizes the importance of leveraging data and innovative approaches to improve financial solutions for suppliers and investors.

![ai it hw mst prac[1] - Read-Offnly.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/aiithwmstprac1-read-only-250118093323-c97d352c-thumbnail.jpg?width=640&height=640&fit=bounds)

![제 23회 보아즈(BOAZ) 빅데이터 컨퍼런스 - [MBOAX] : ABSA를 활용한 소비자 반응 분석 기반 운영 효율화 대시보드 설계](https://cdn.slidesharecdn.com/ss_thumbnails/3-1boaz23rdconferencemboax-260203102709-9d519923-thumbnail.jpg?width=640&height=640&fit=bounds)