Downloaded 391 times

The document discusses the impact of COSO's 2009 monitoring guidance on smaller companies and practical steps for SOX compliance, emphasizing the importance of internal controls and monitoring effectiveness. It outlines the purpose of the guidance, application strategies, and suggestions for leveraging monitoring principles in organizational processes. Additionally, it addresses key considerations for dealing with external auditors and remediation of internal control weaknesses.

Introduction to COSO's 2009 Monitoring Guidance and its impact on smaller companies and SOX compliance.

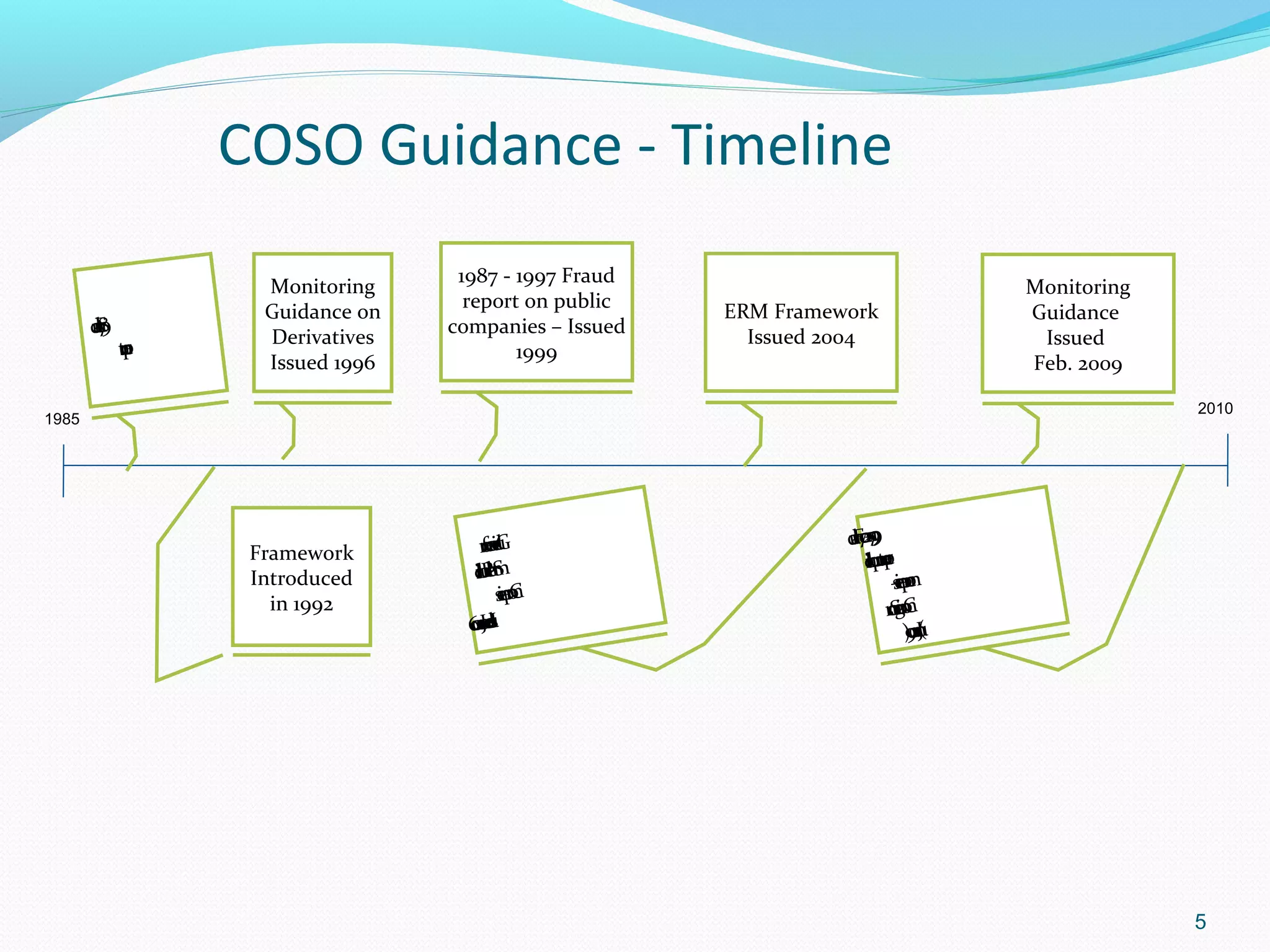

Overview of COSO's formation, functions, and key milestones in guidance including monitoring.

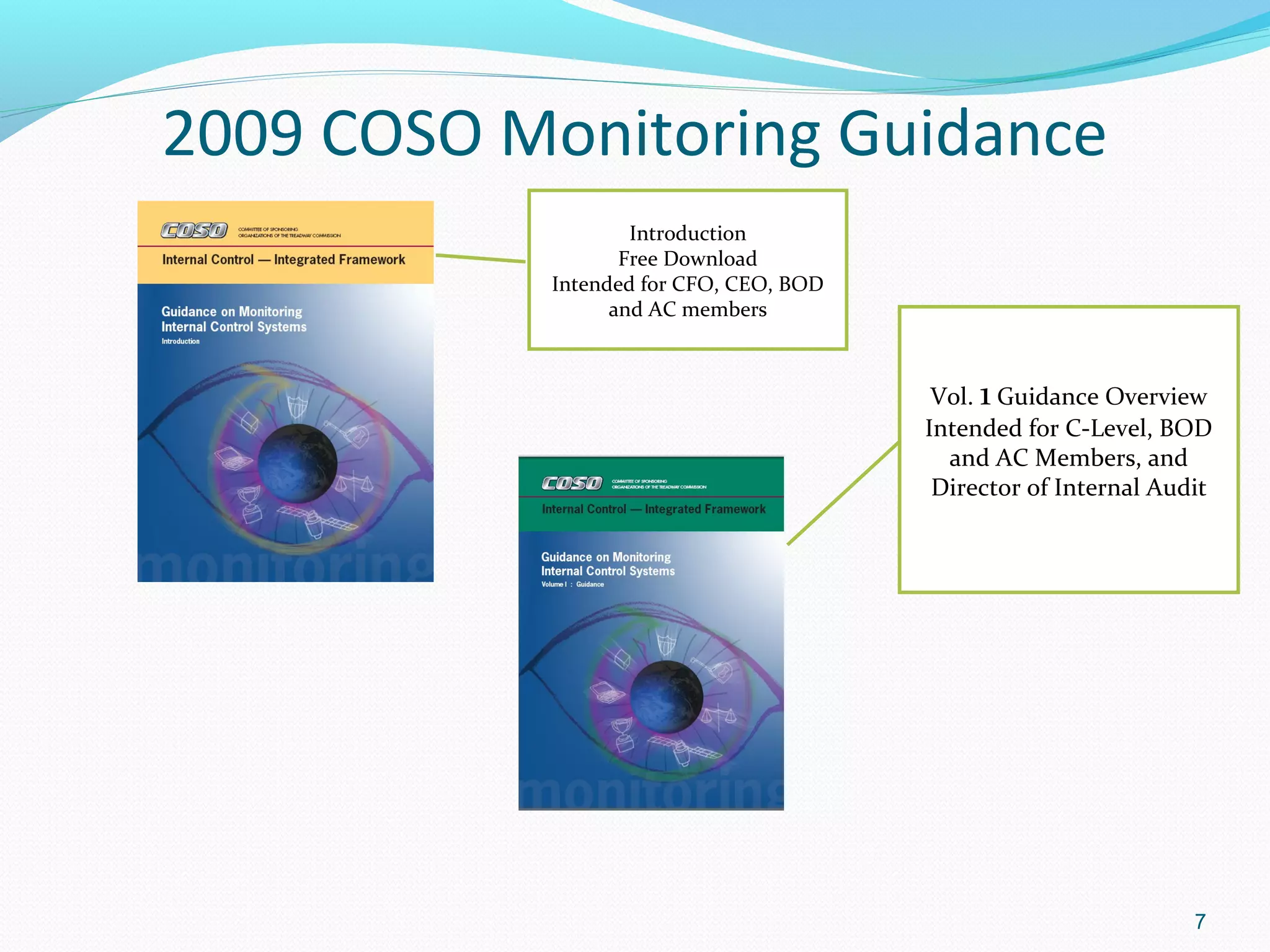

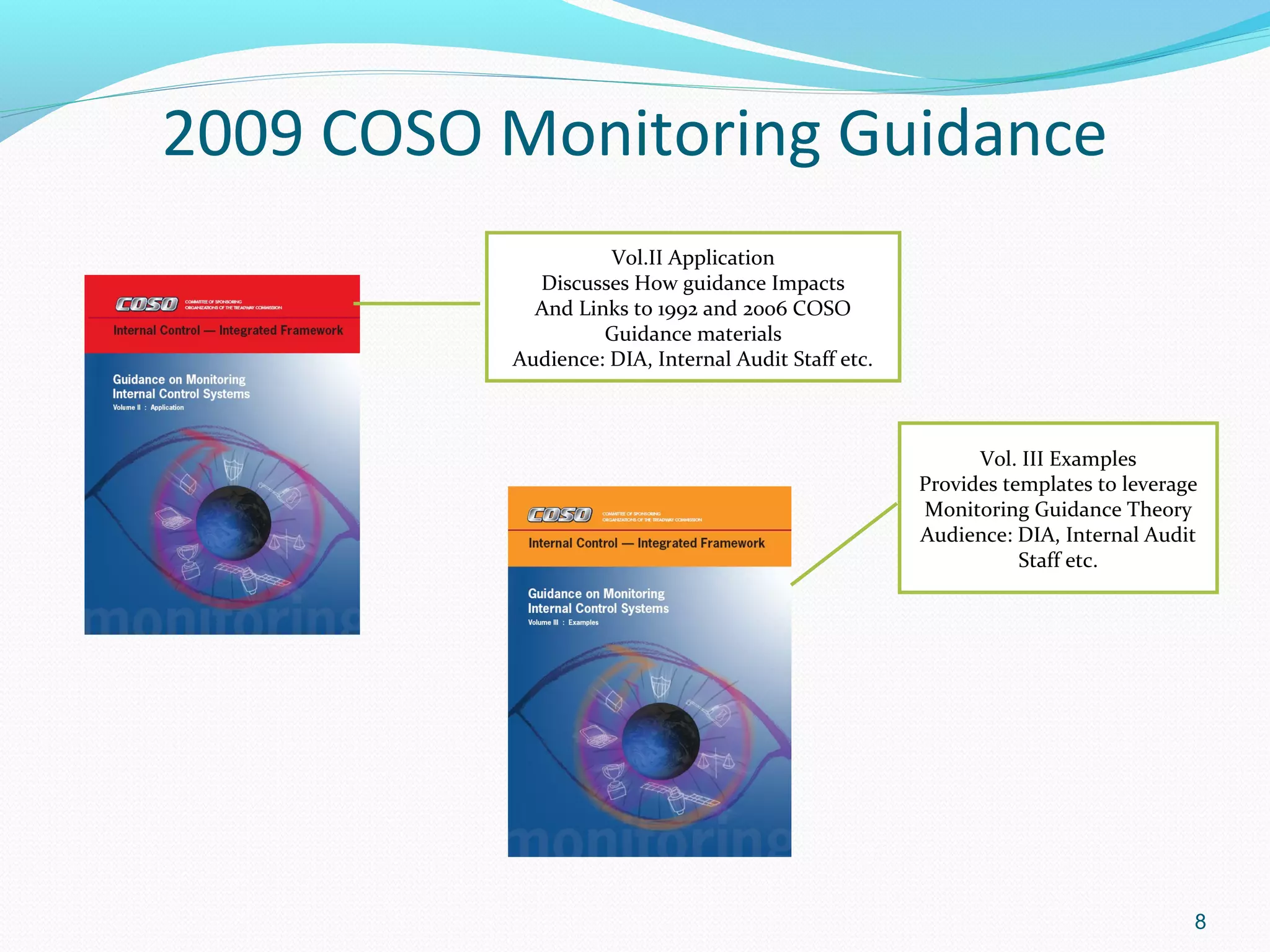

Information on where to access COSO guidance materials, aimed at executives and internal audit.

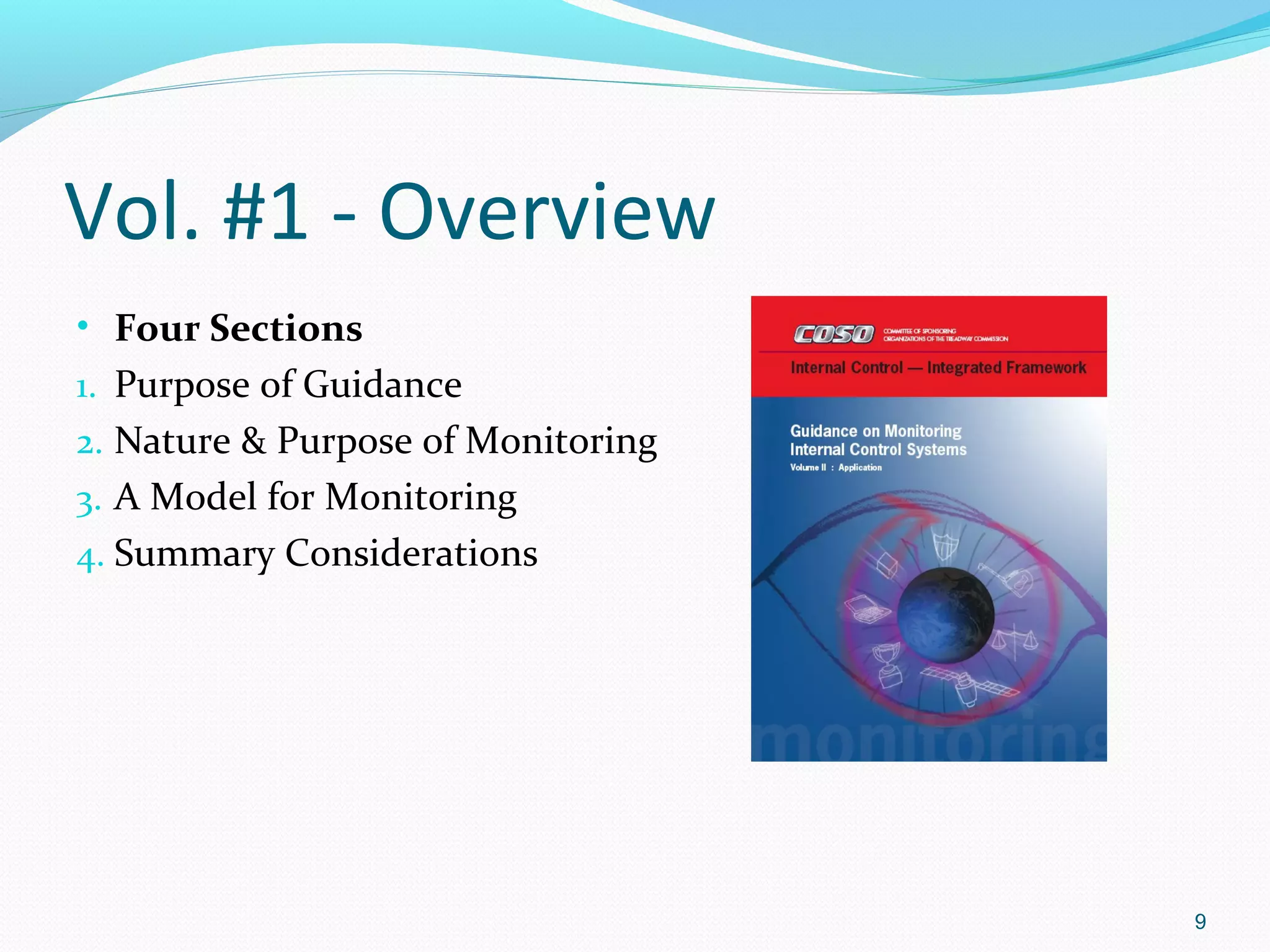

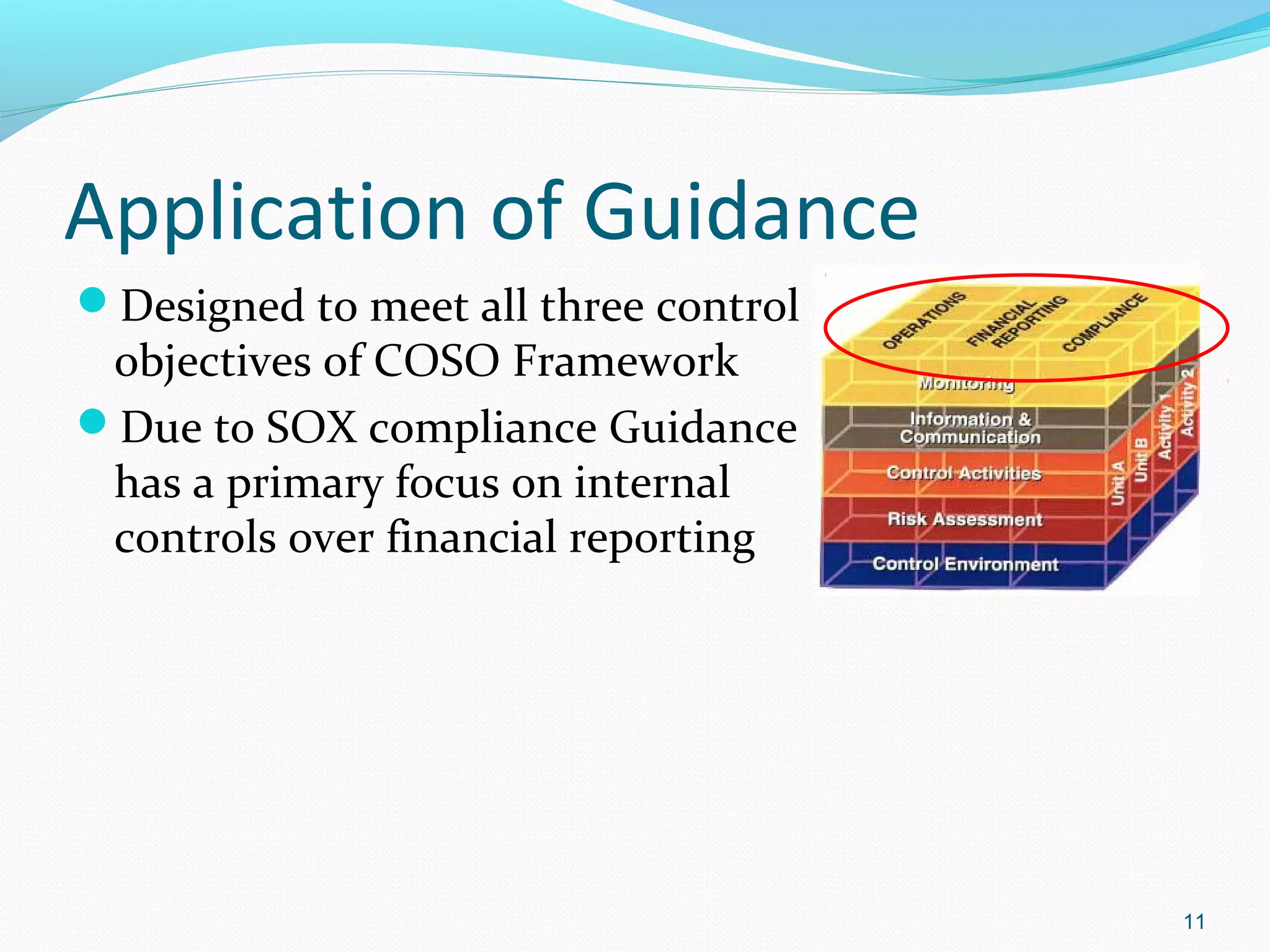

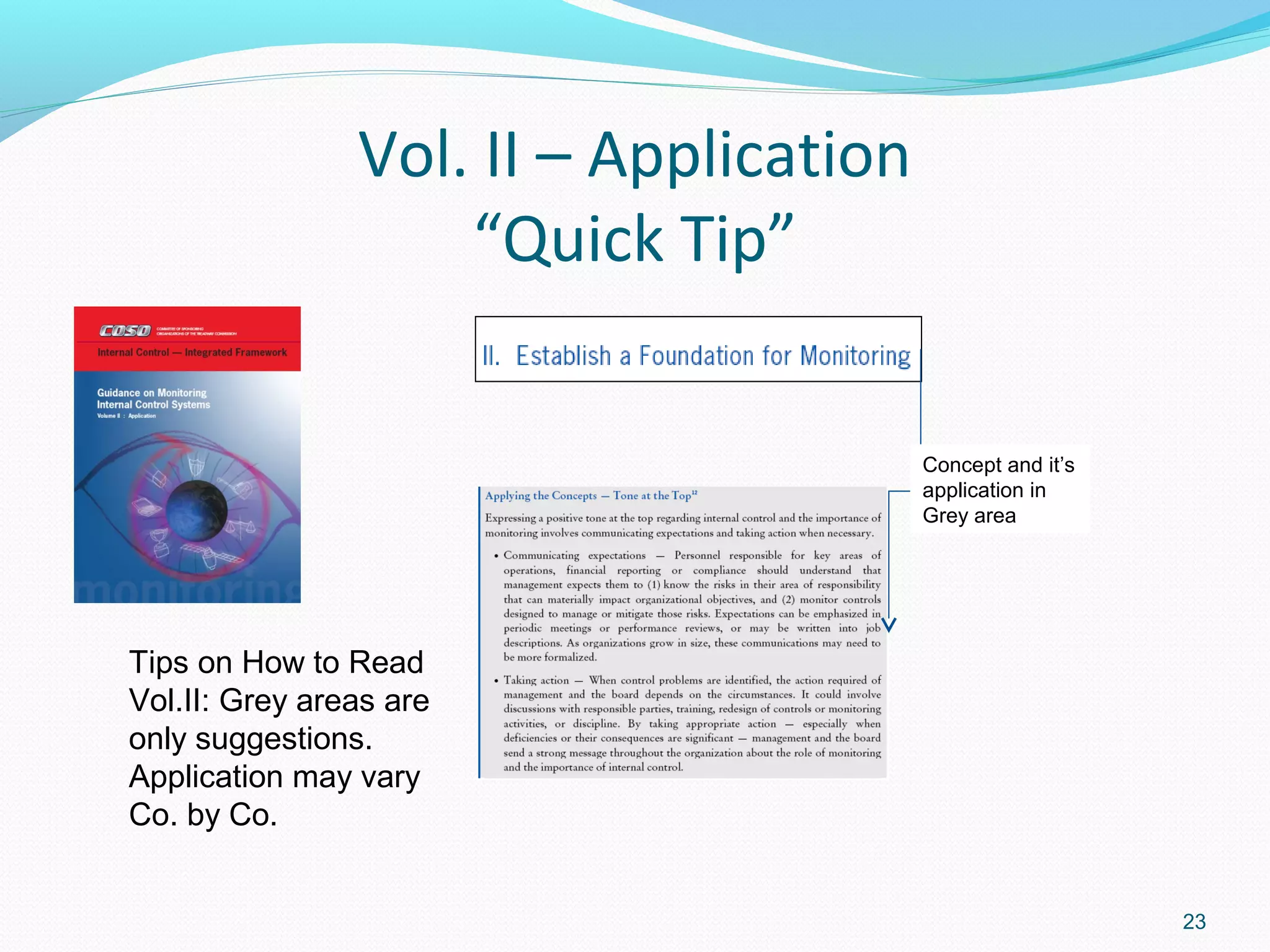

Breakdown of the 2009 COSO guidance, its objectives, and focus on improving internal controls.

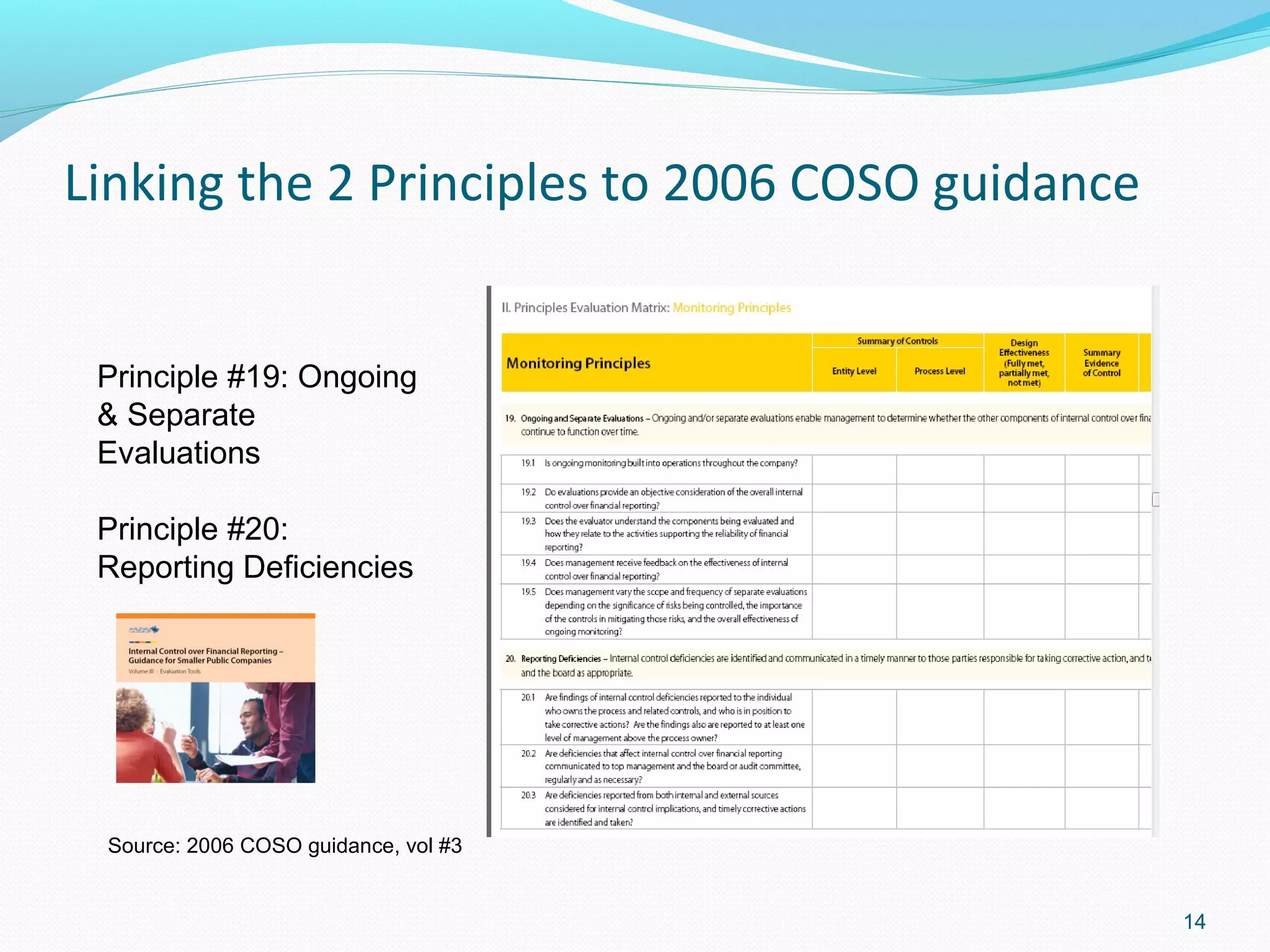

Discussion of monitoring principles to ensure effective internal control operations and timely reporting.

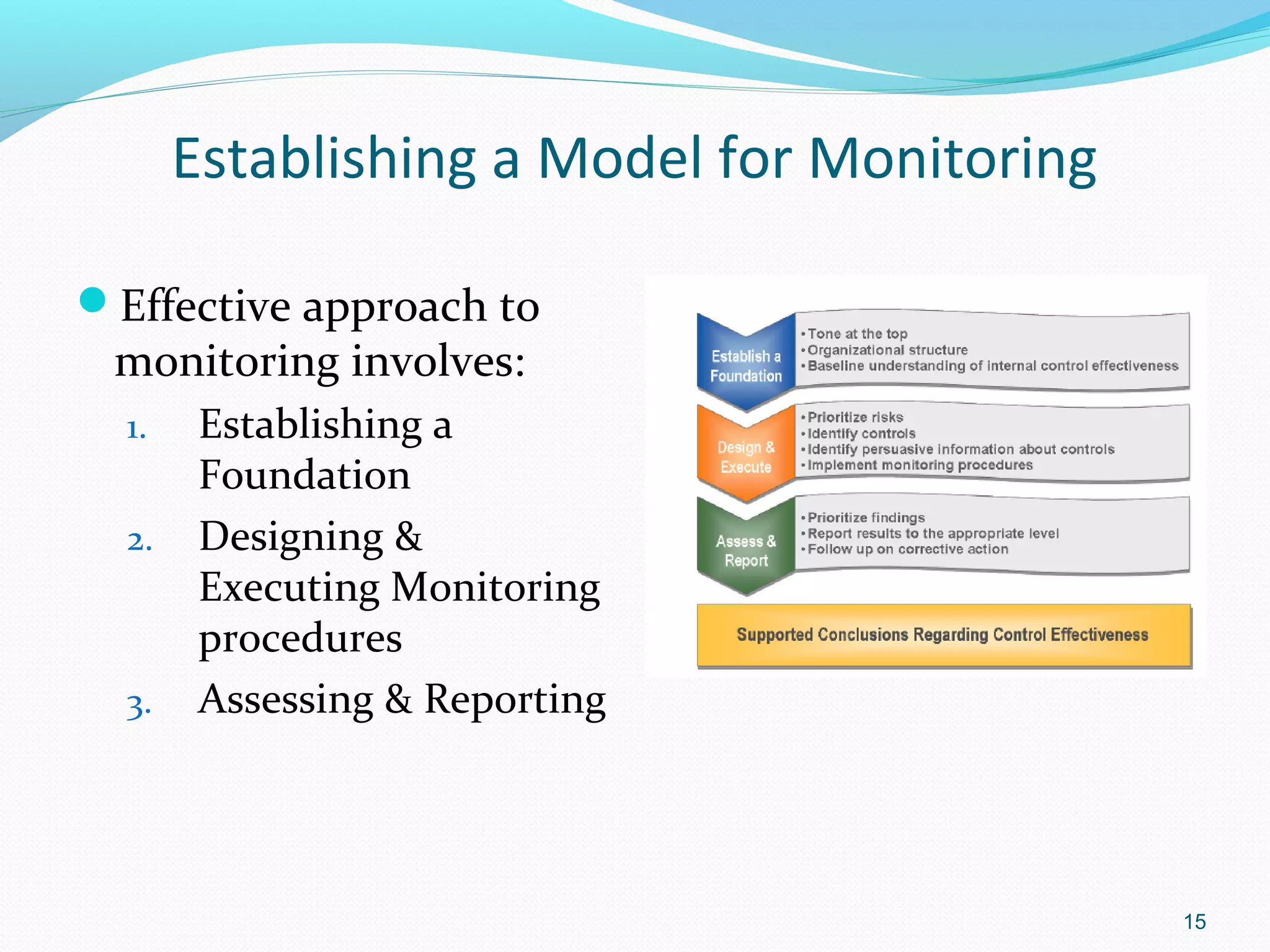

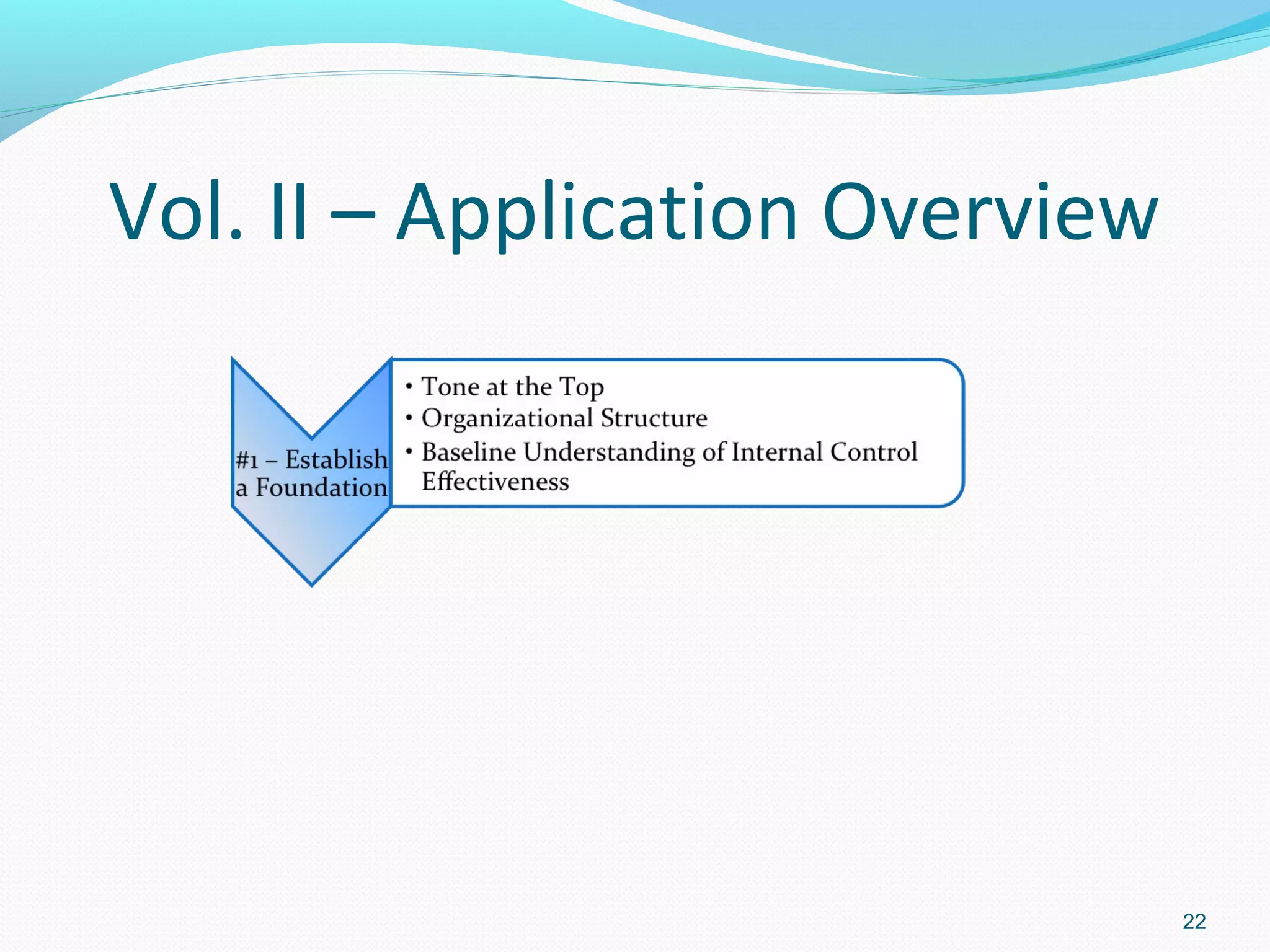

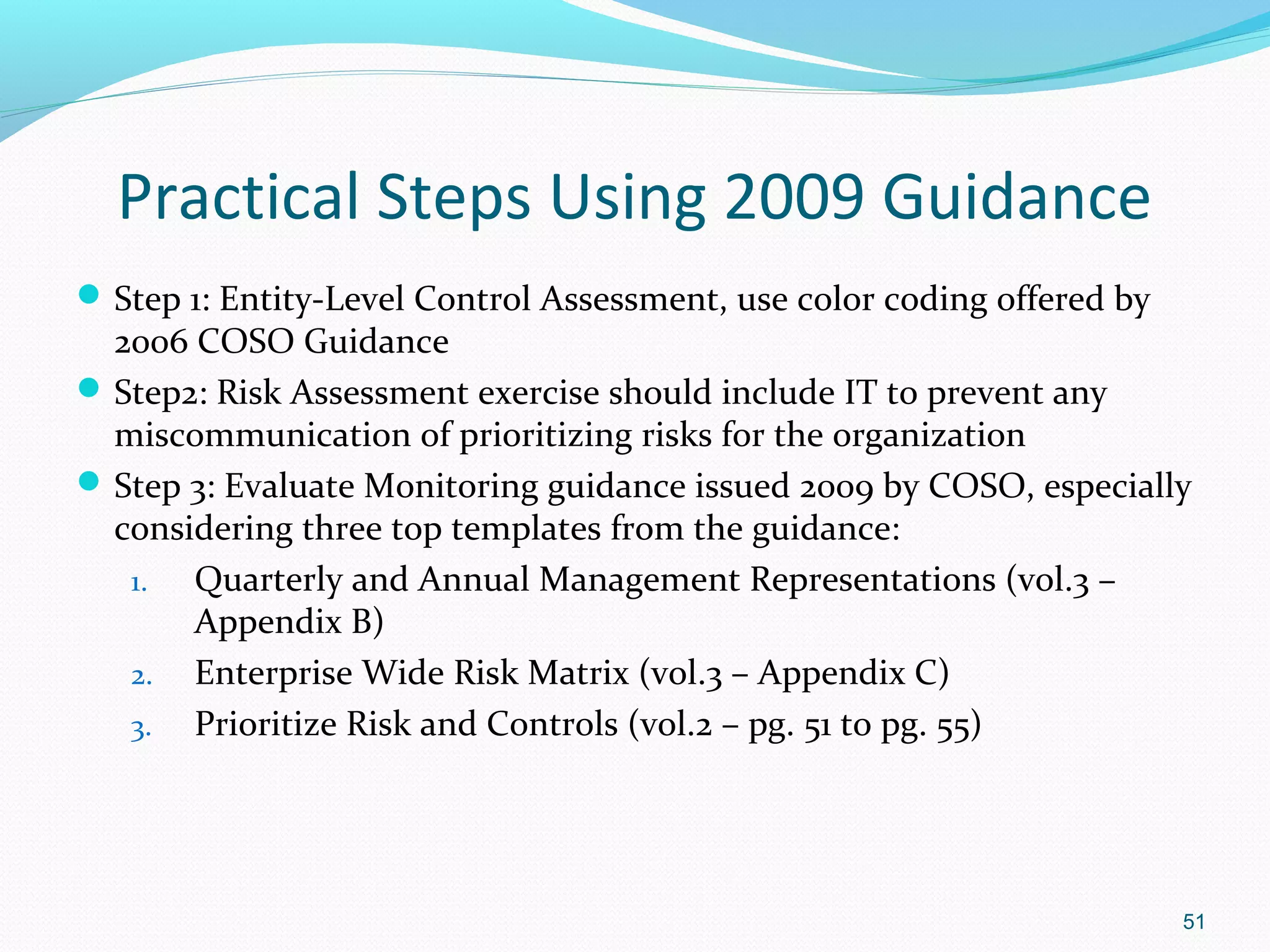

Steps to establish a monitoring model, including foundations, procedures, assessments, and reporting.

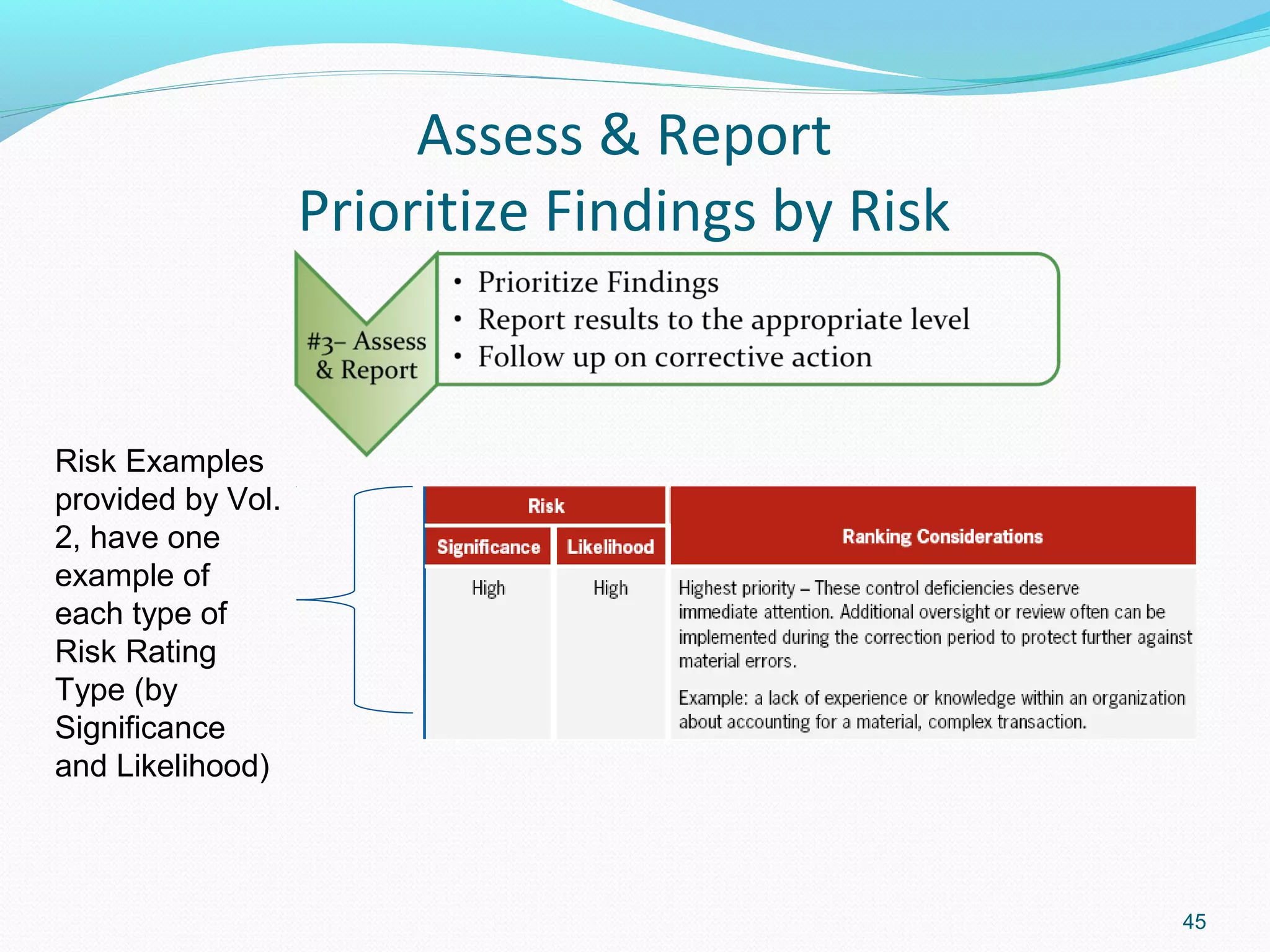

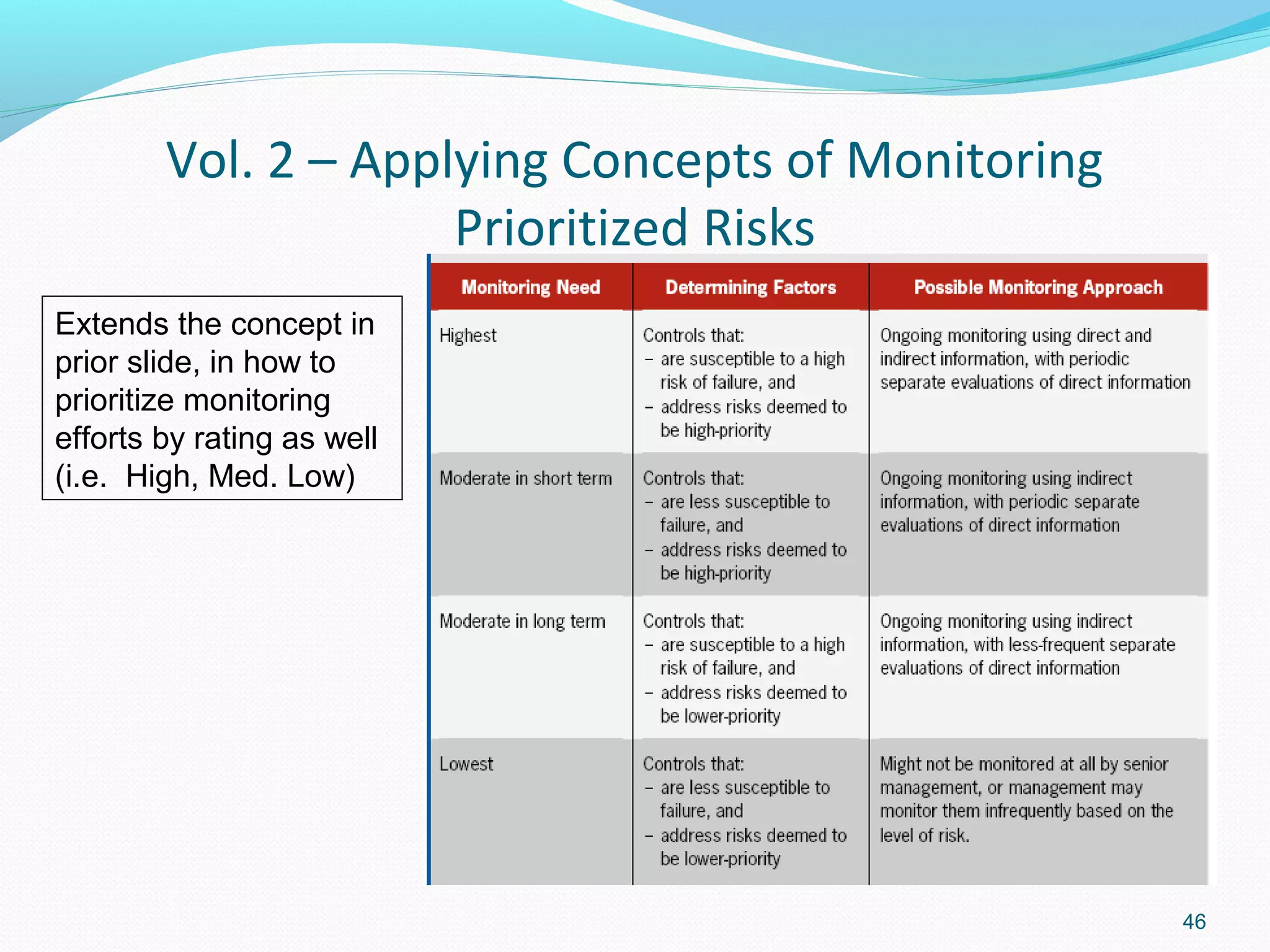

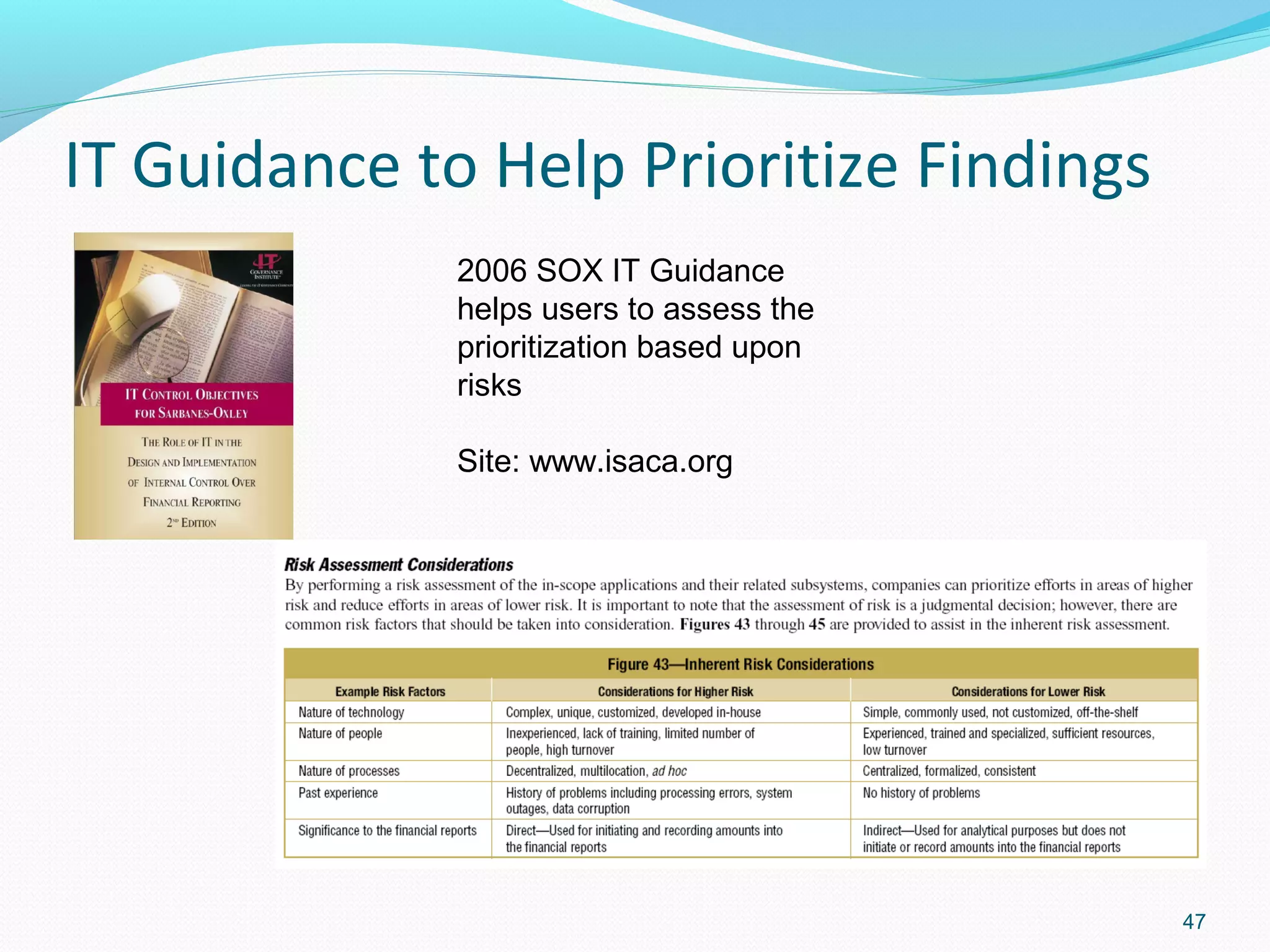

Procedures for assessing and prioritizing control deficiencies and reporting requirements internally and externally.

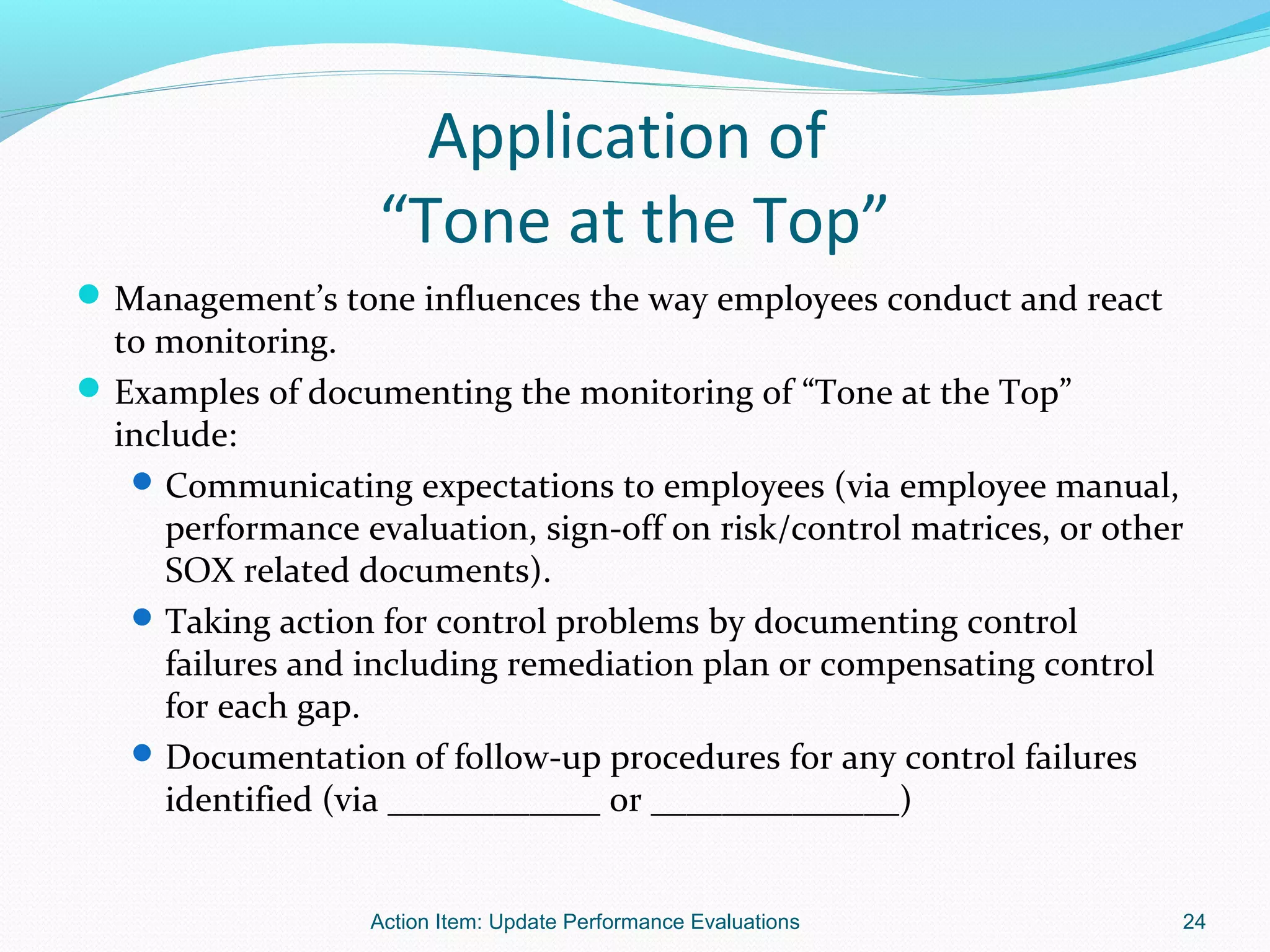

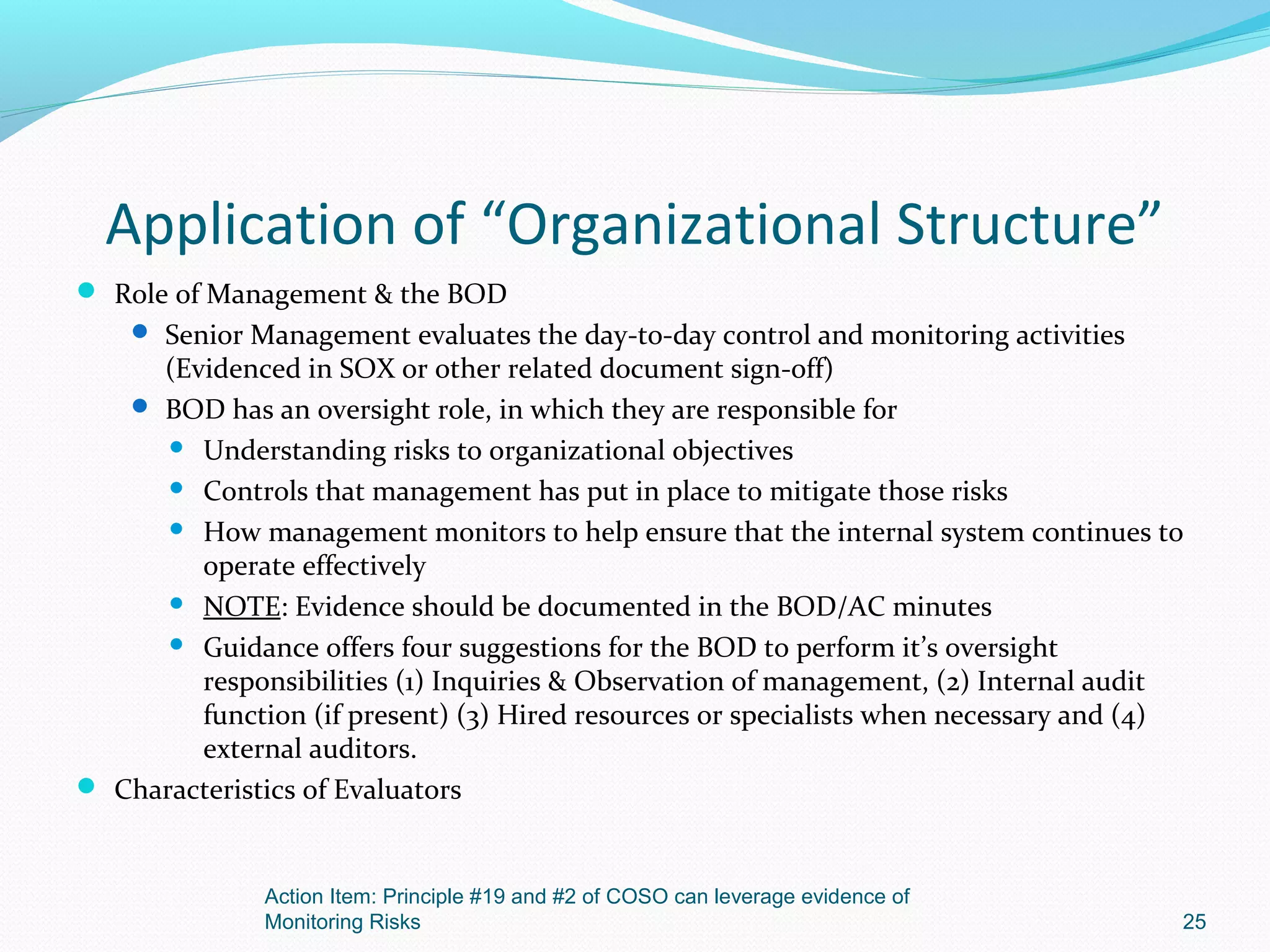

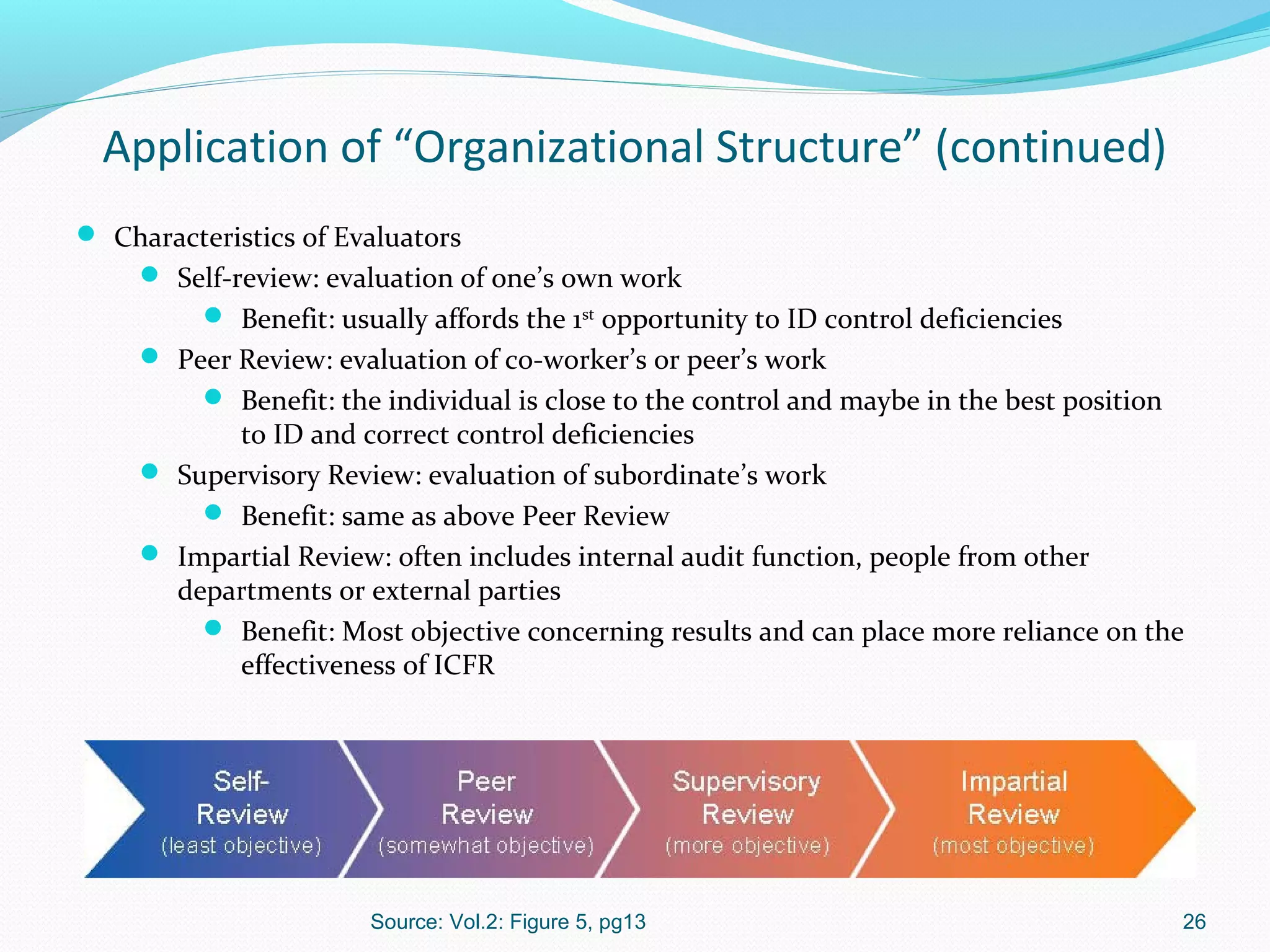

Application of tone at the top and organizational structure for effective control monitoring and evaluation.

Reasons for internal control failures and the importance of establishing a control baseline for monitoring.

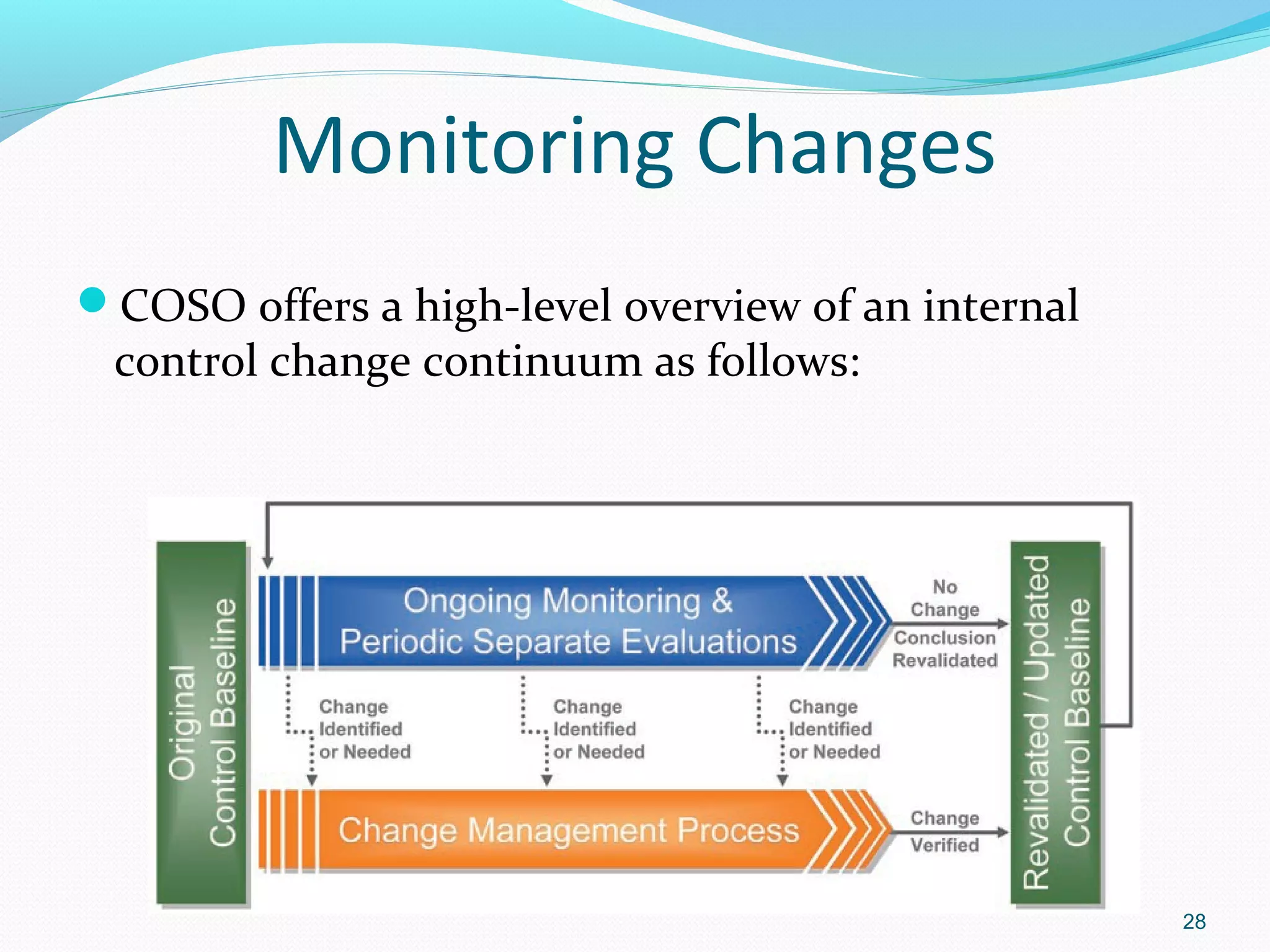

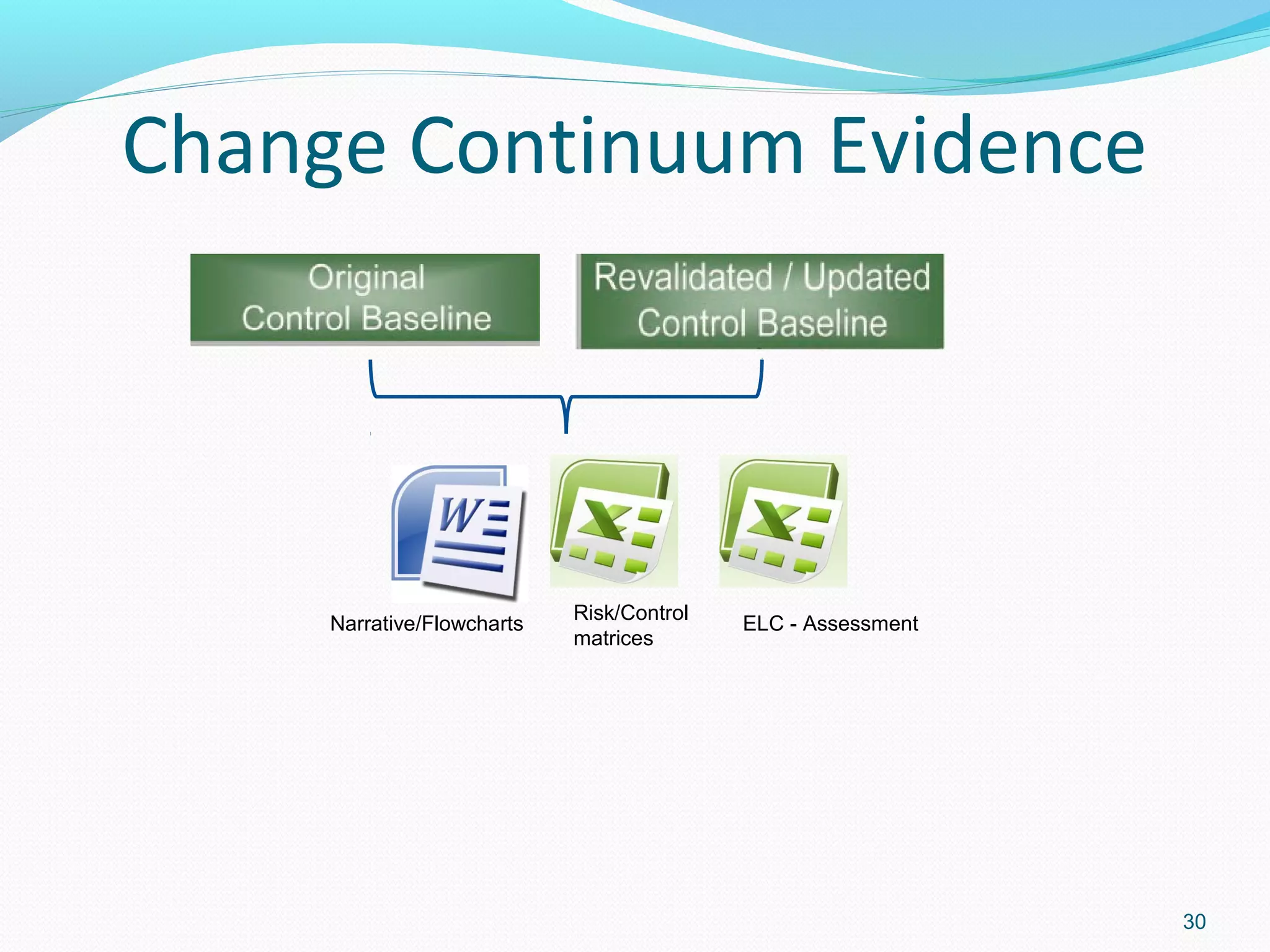

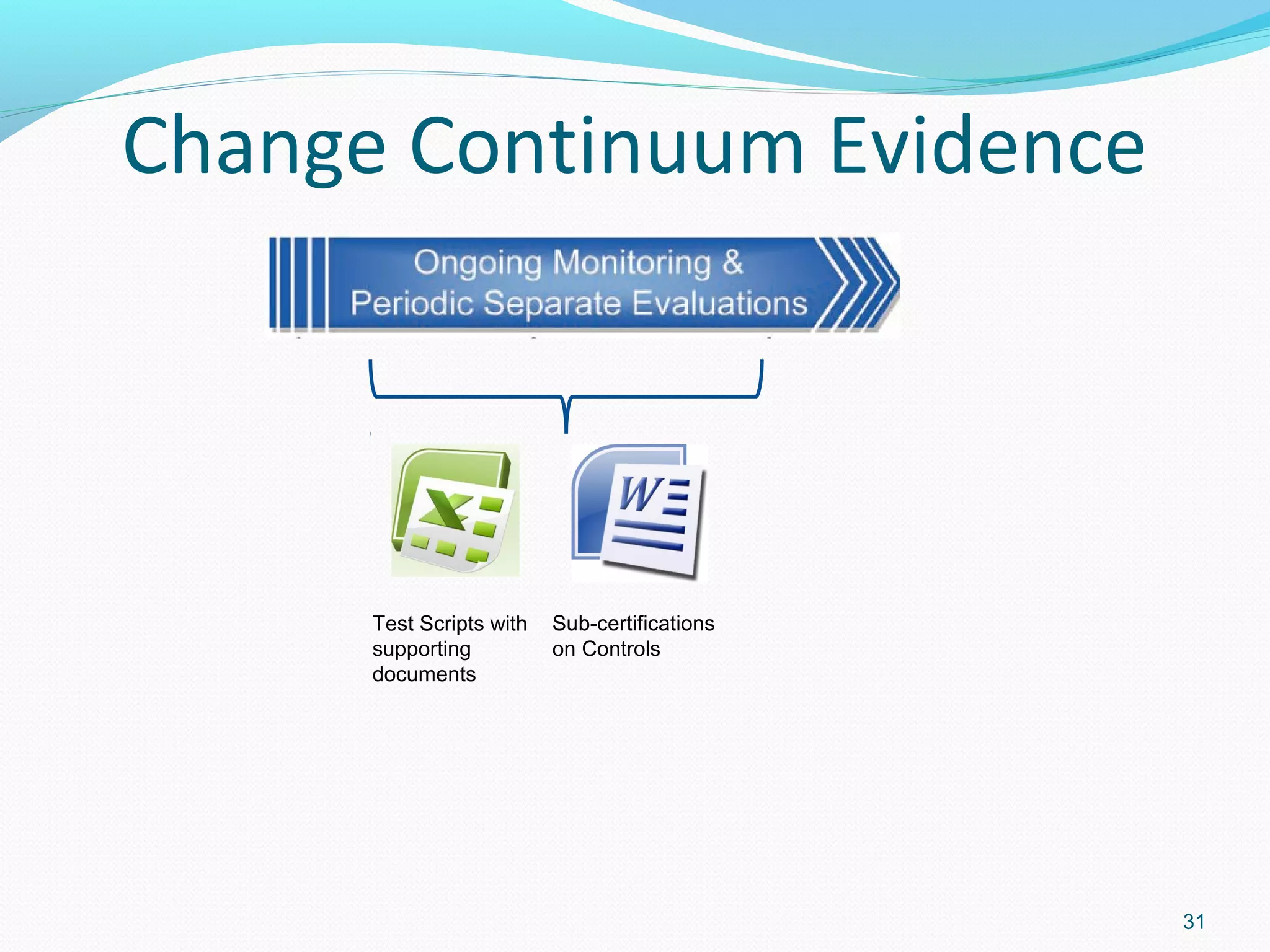

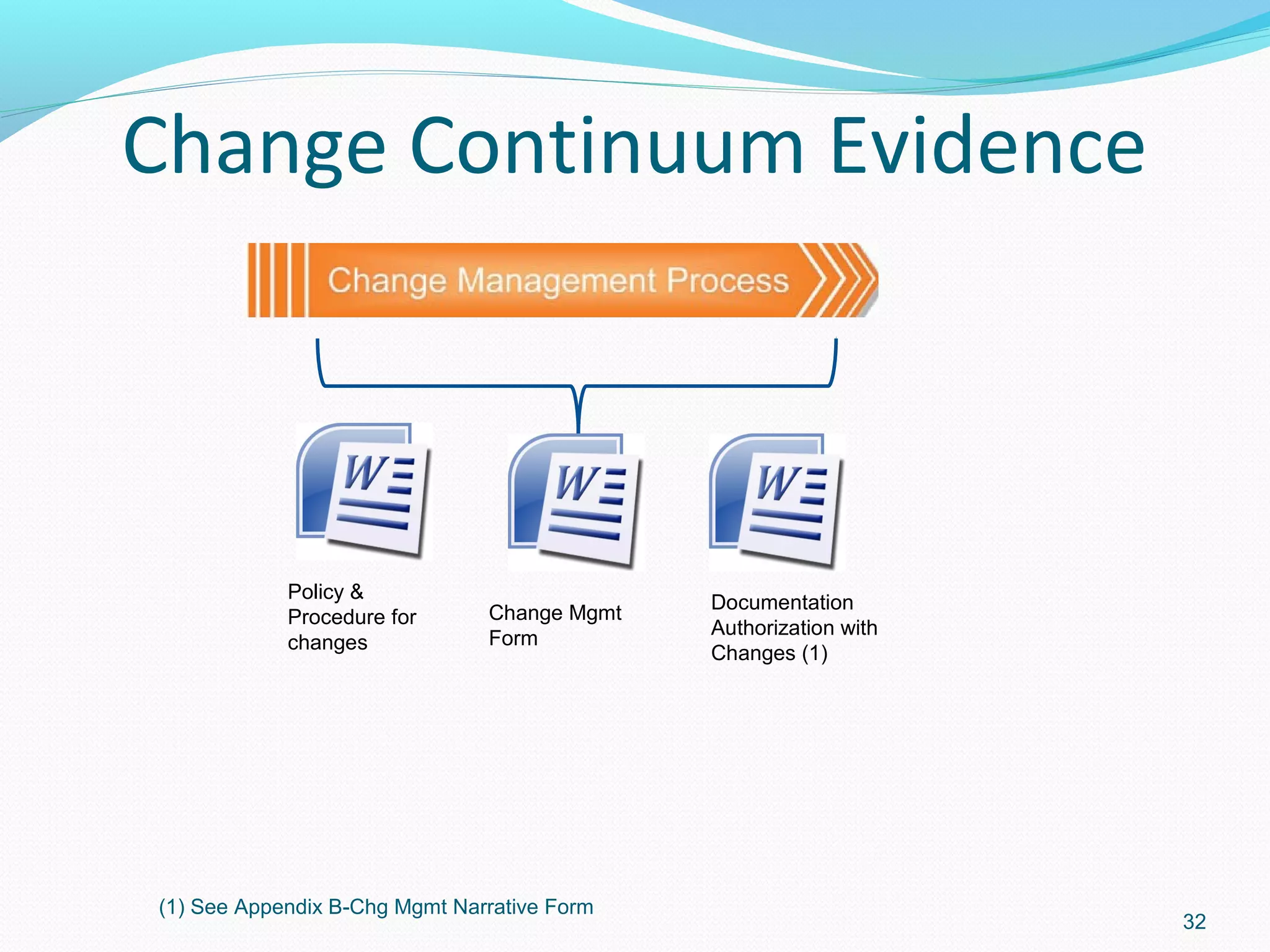

Description of change continuum in monitoring and types of supporting documentation for effective controls.

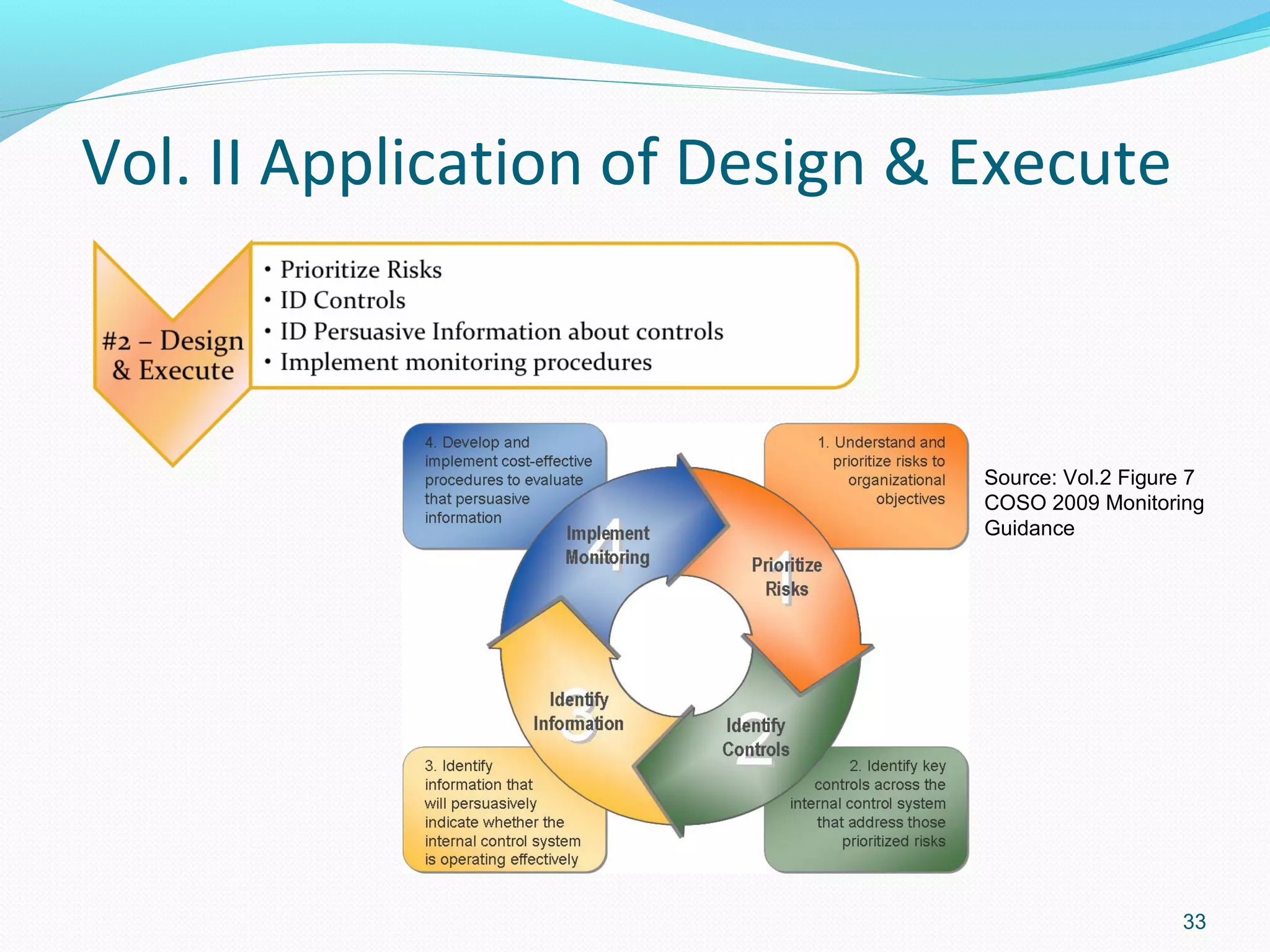

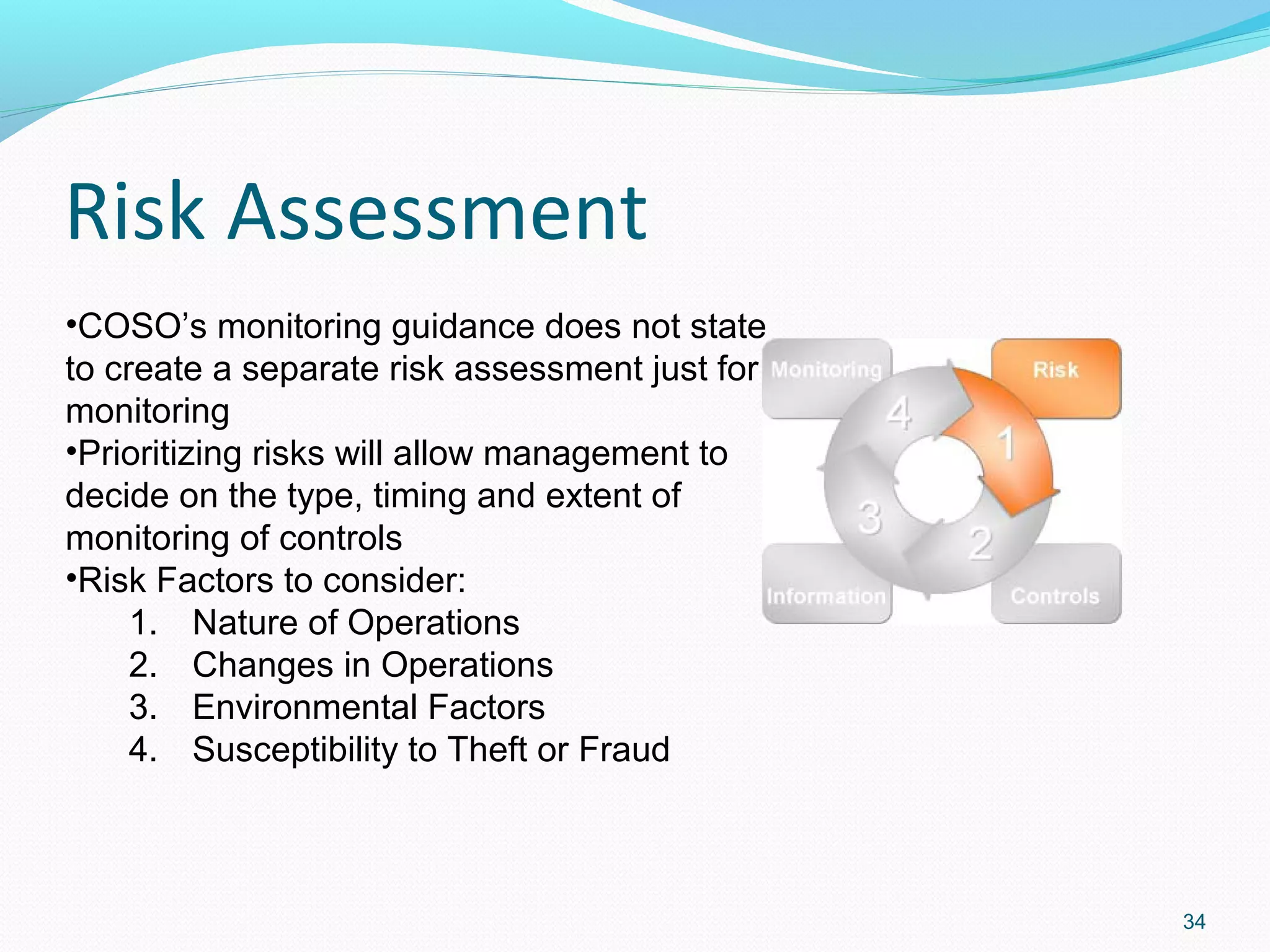

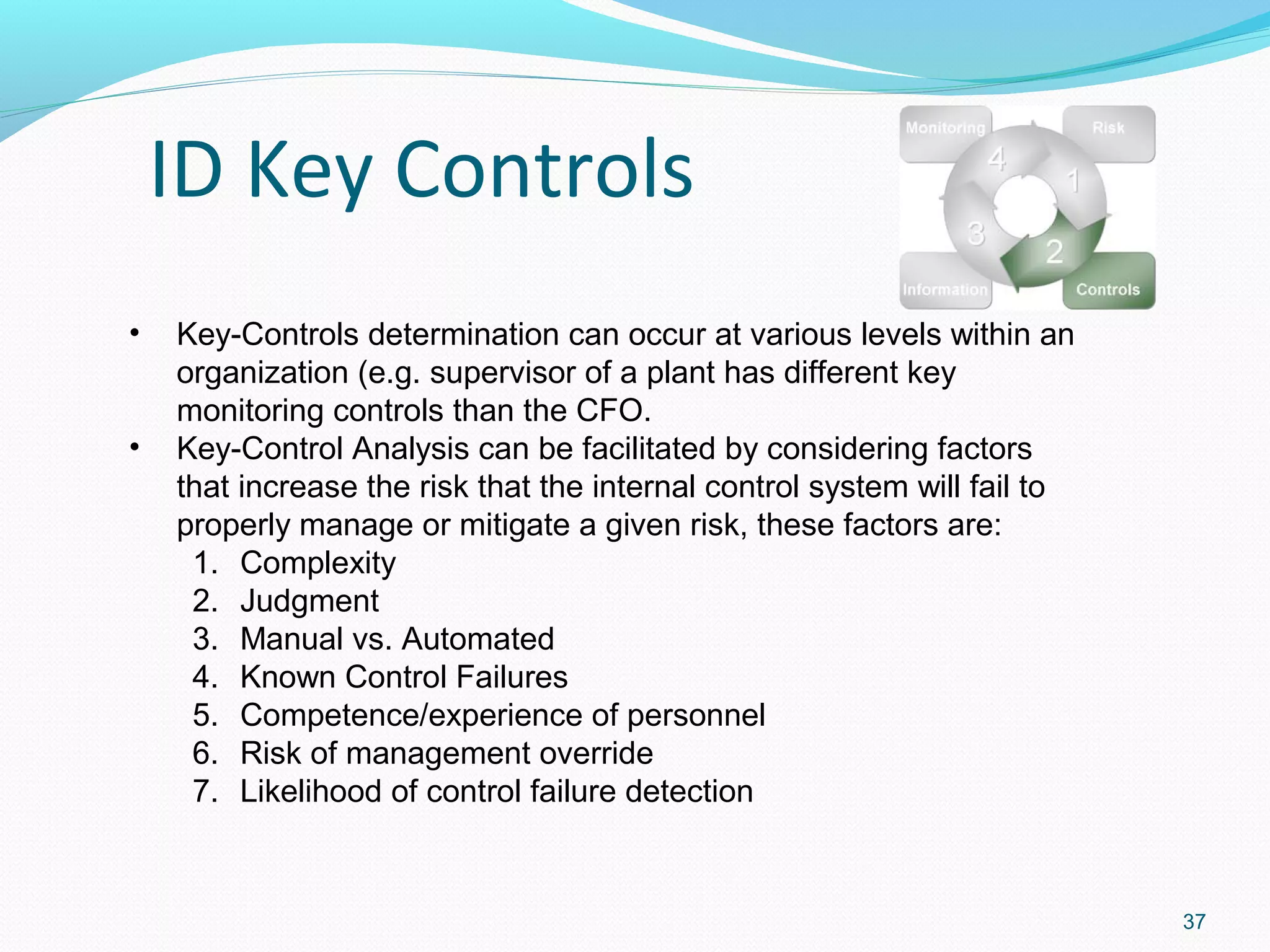

Guidance on implementing effective monitoring, risk assessment, and identification of key controls.

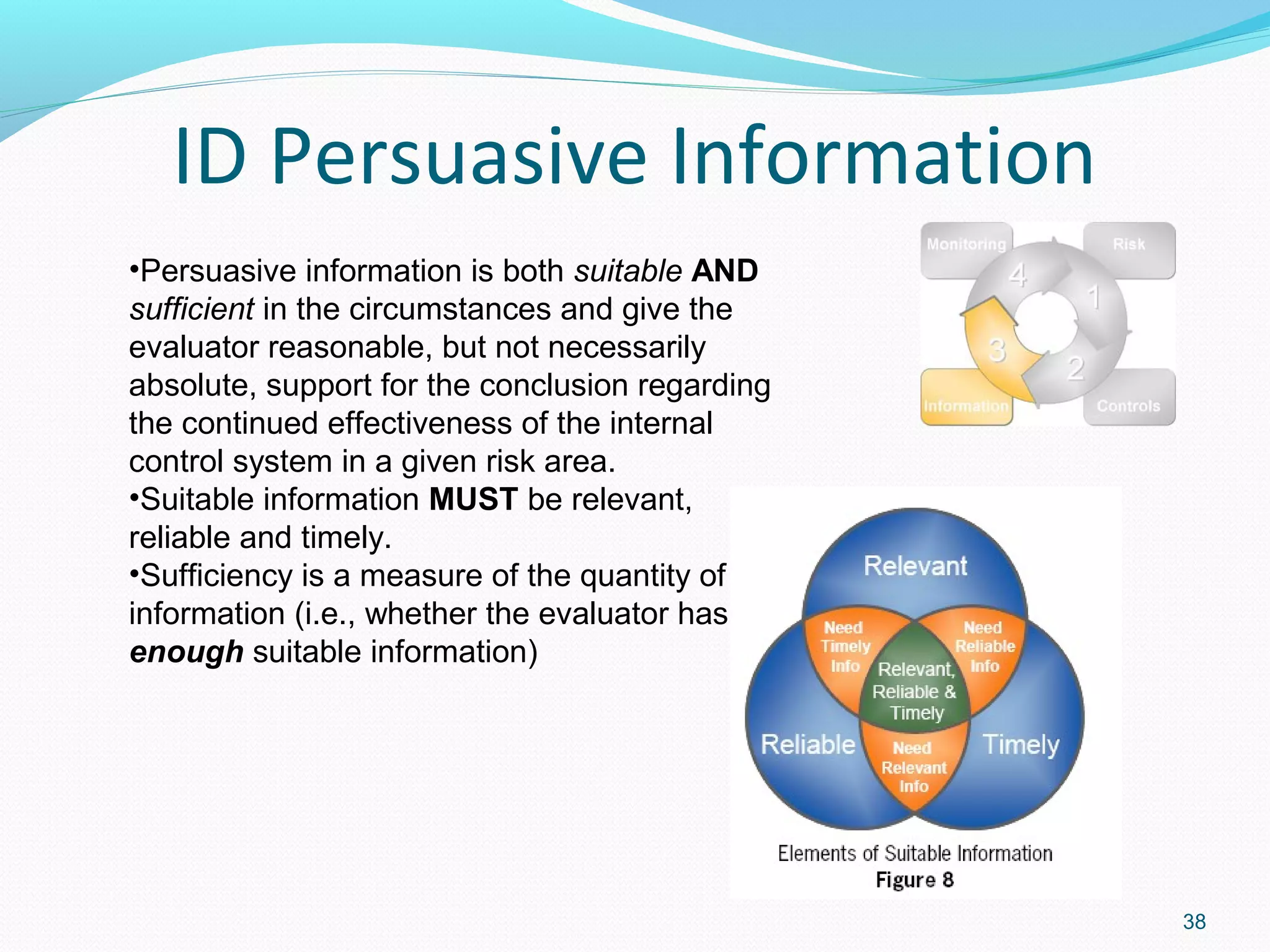

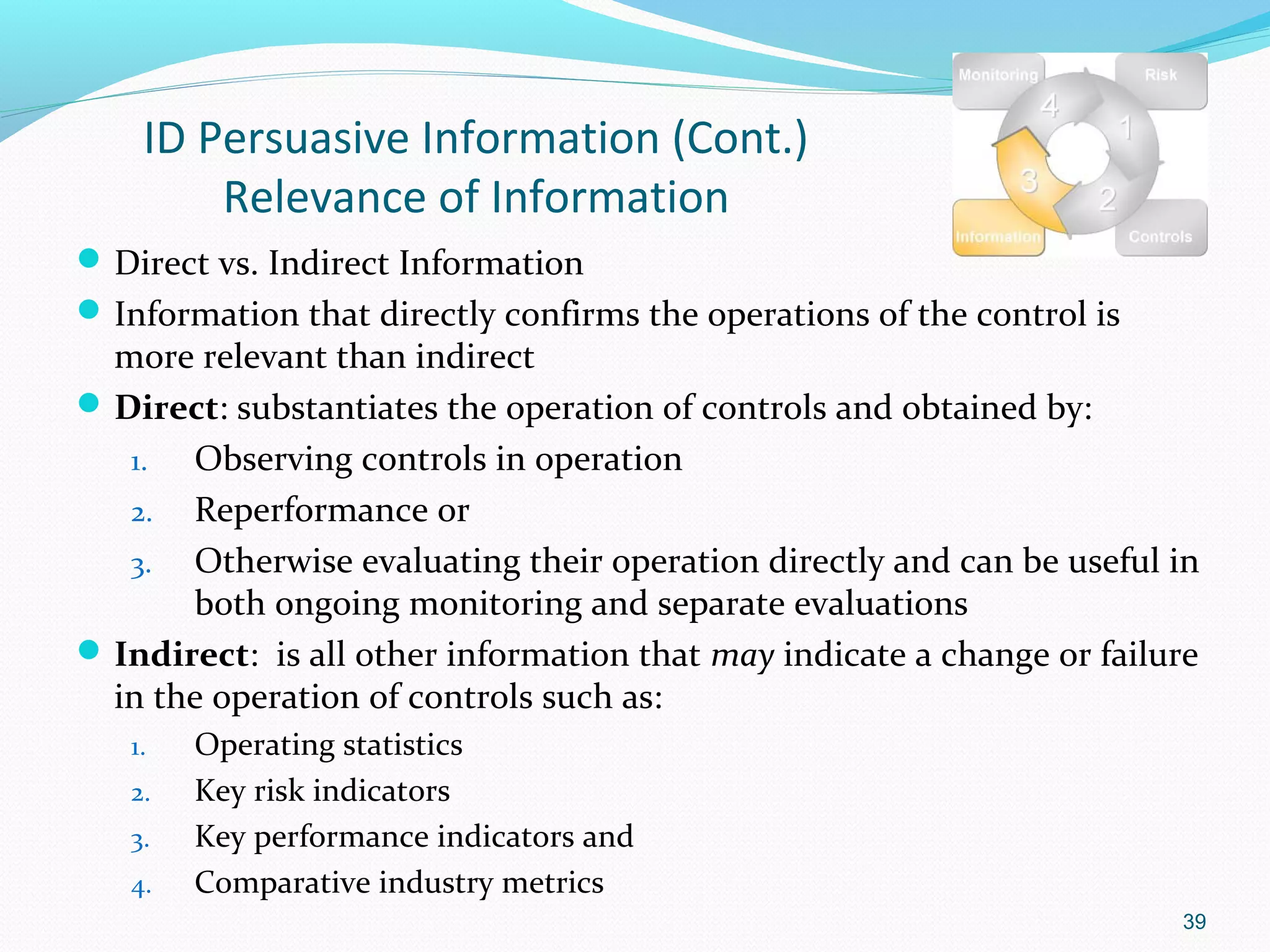

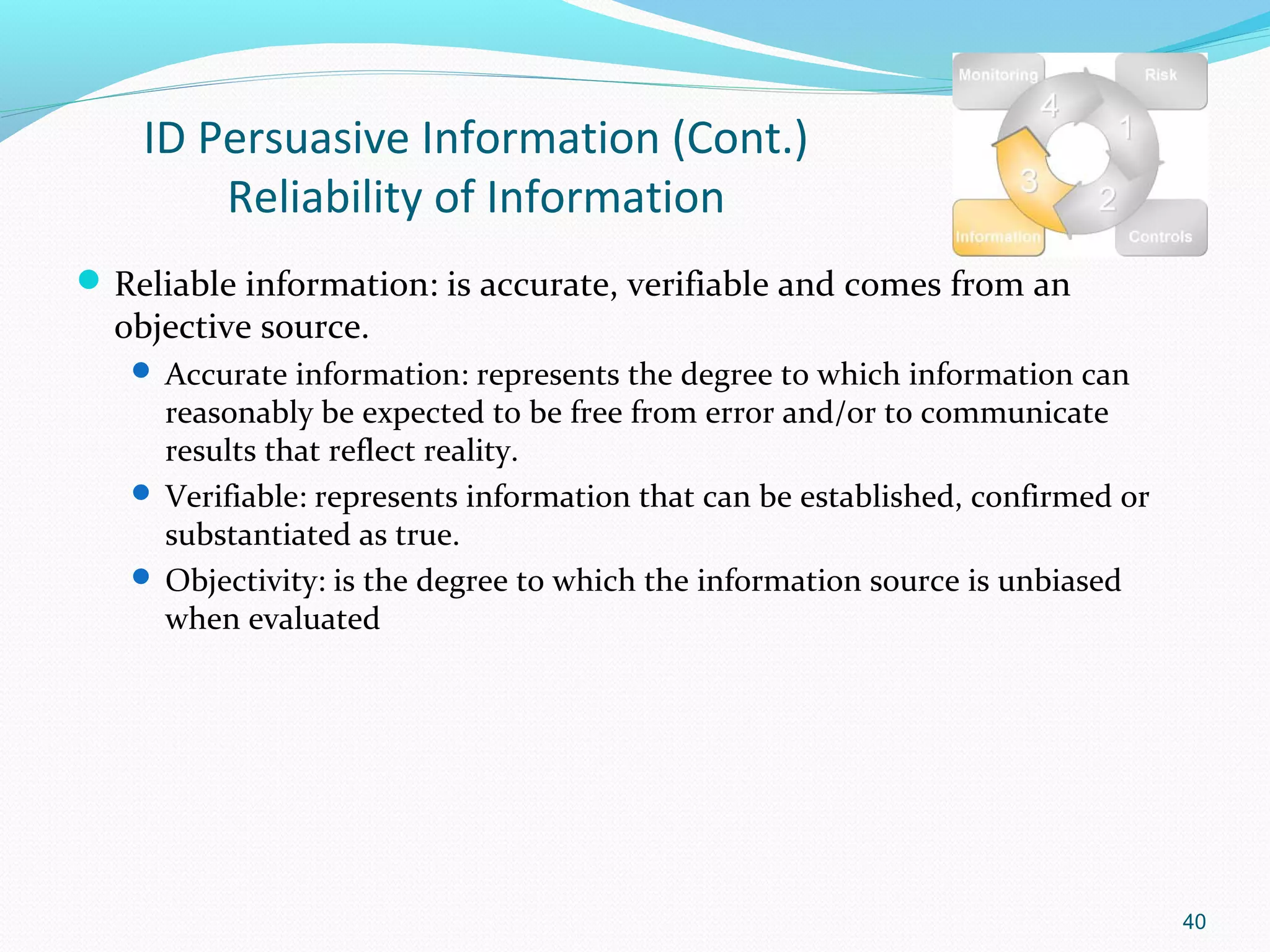

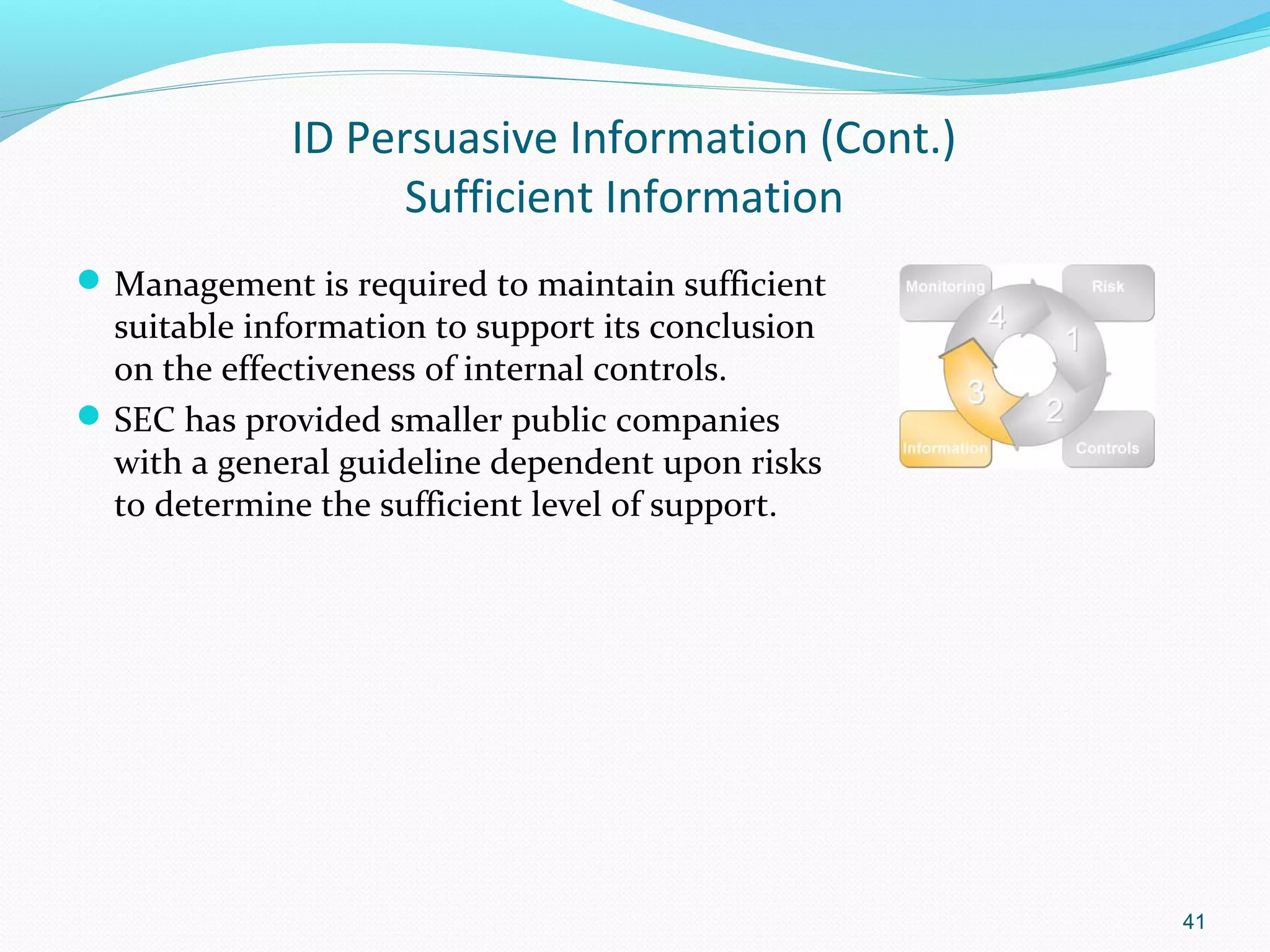

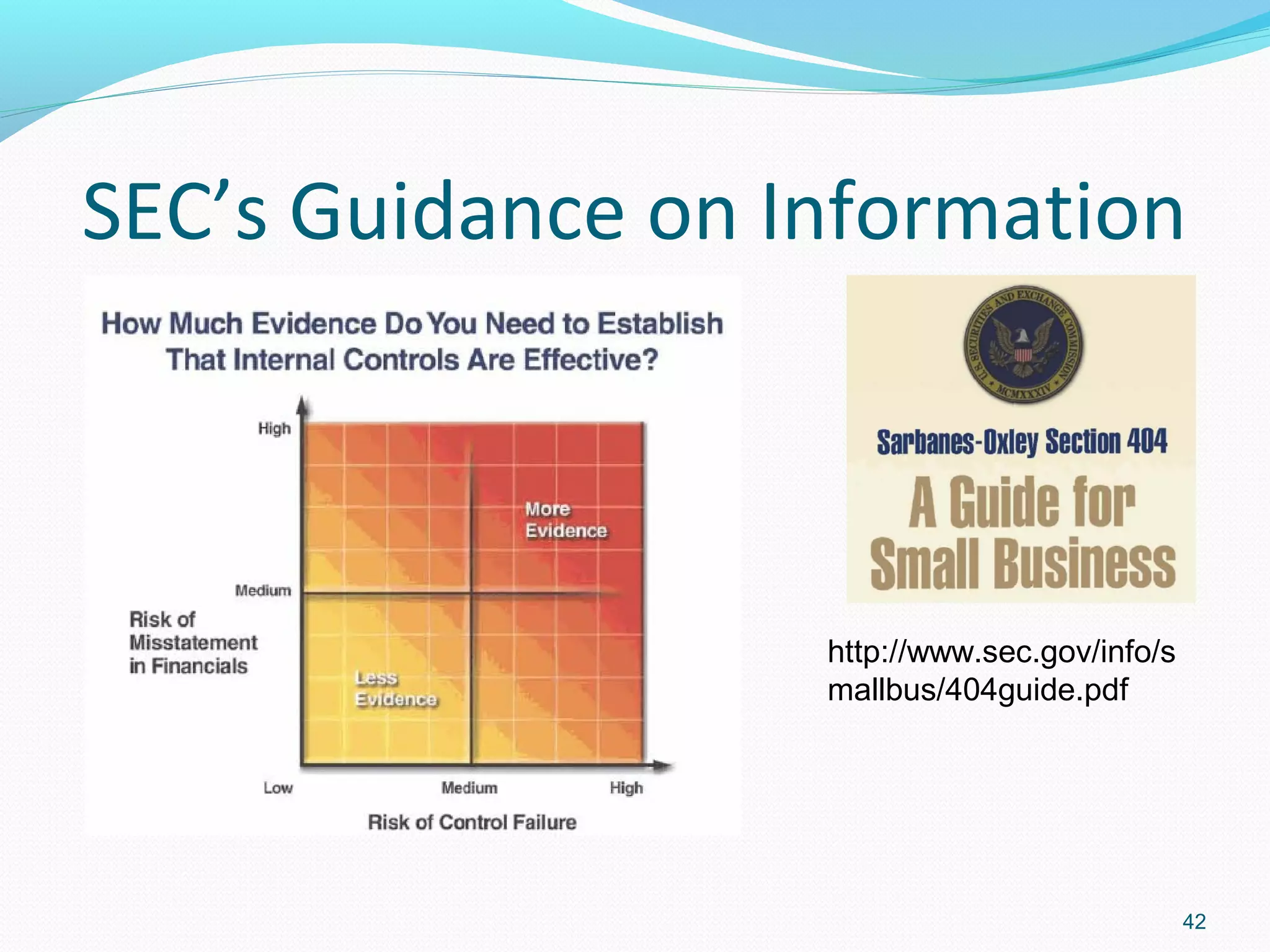

Identifying and maintaining persuasive information to assess effectiveness of internal controls.

New AICPA guidance on sampling for internal controls and risk-based approaches for multi-locations.

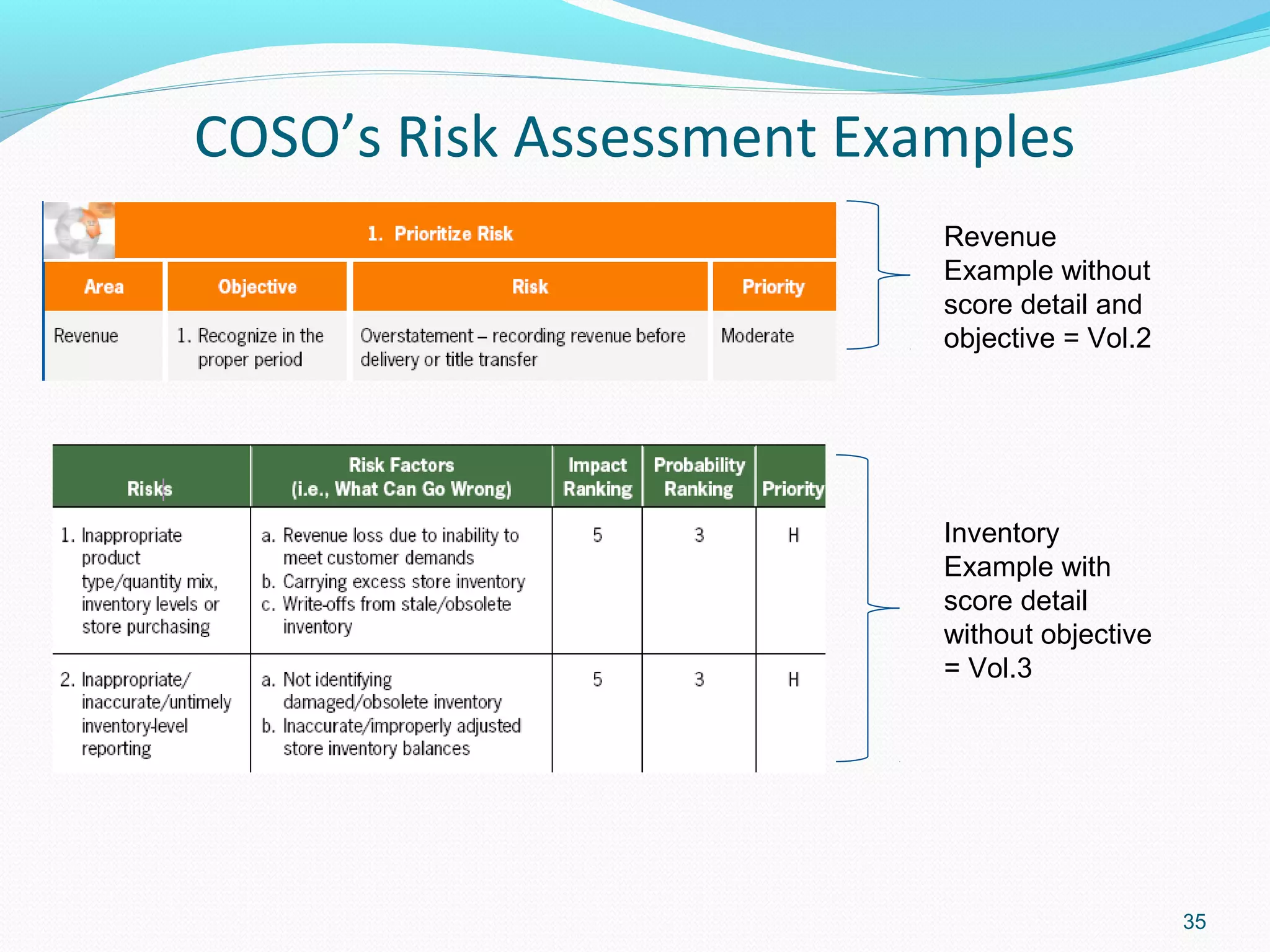

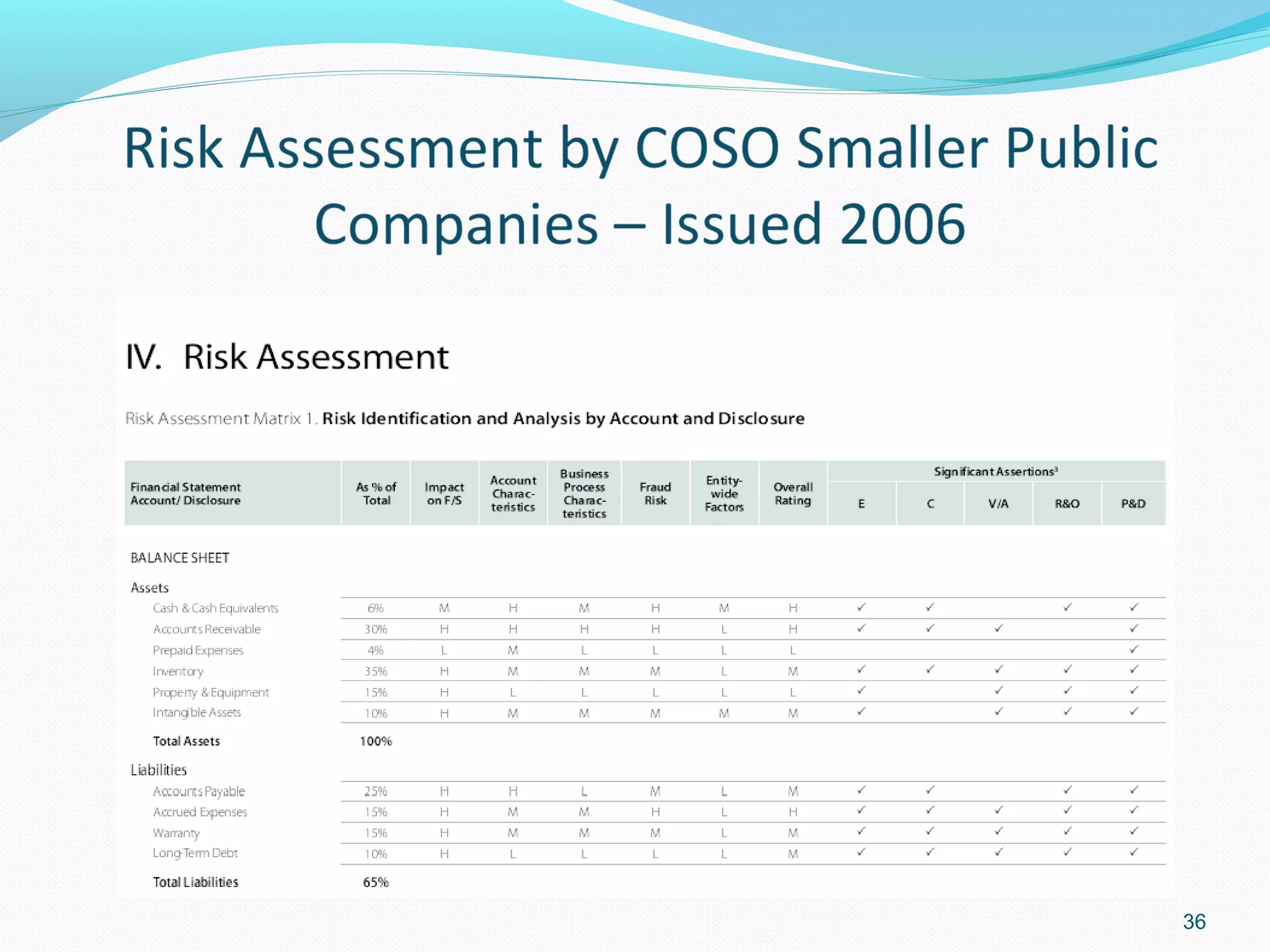

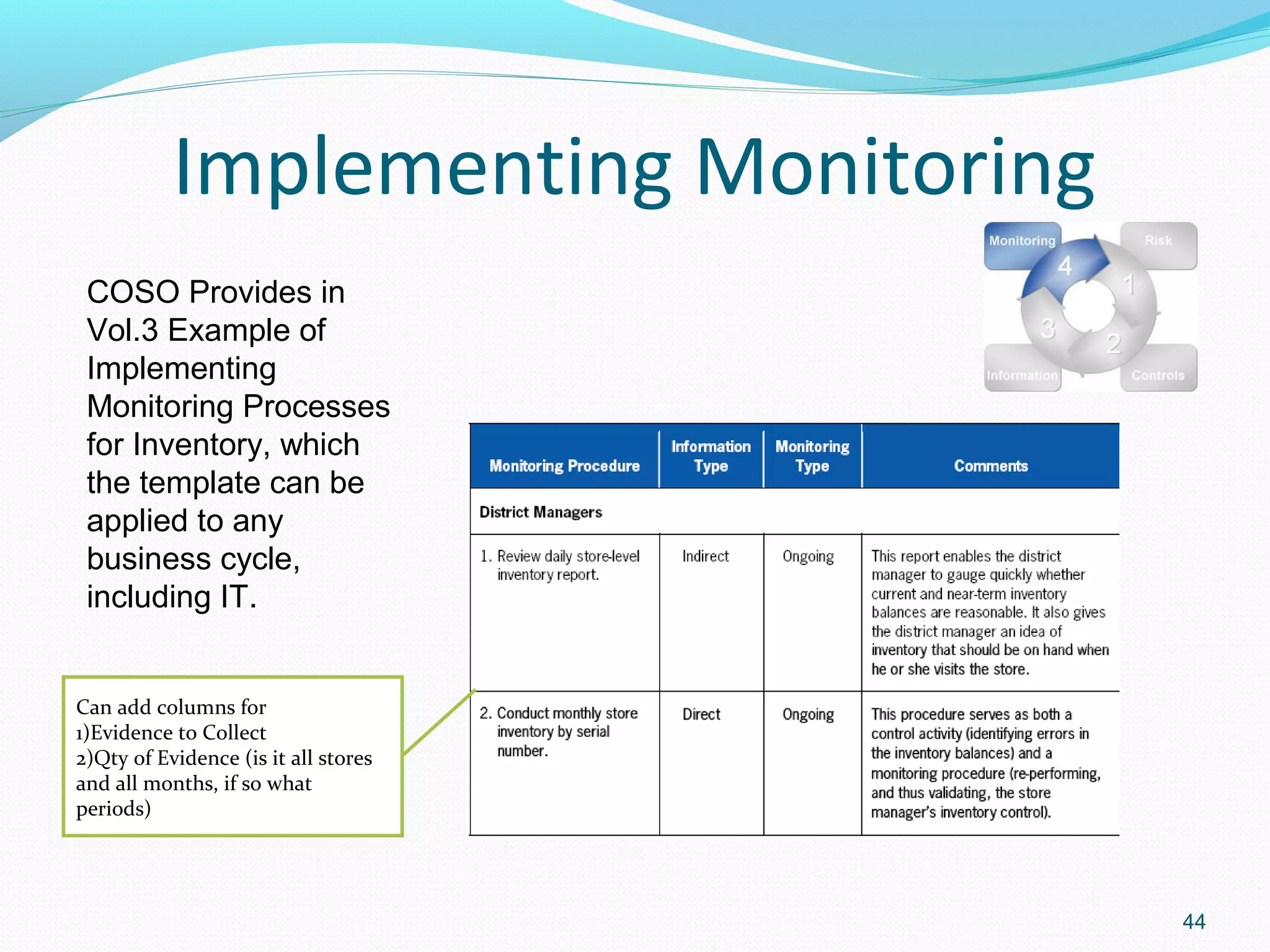

Examples of monitoring processes and prioritization of risks in effective monitoring practices.

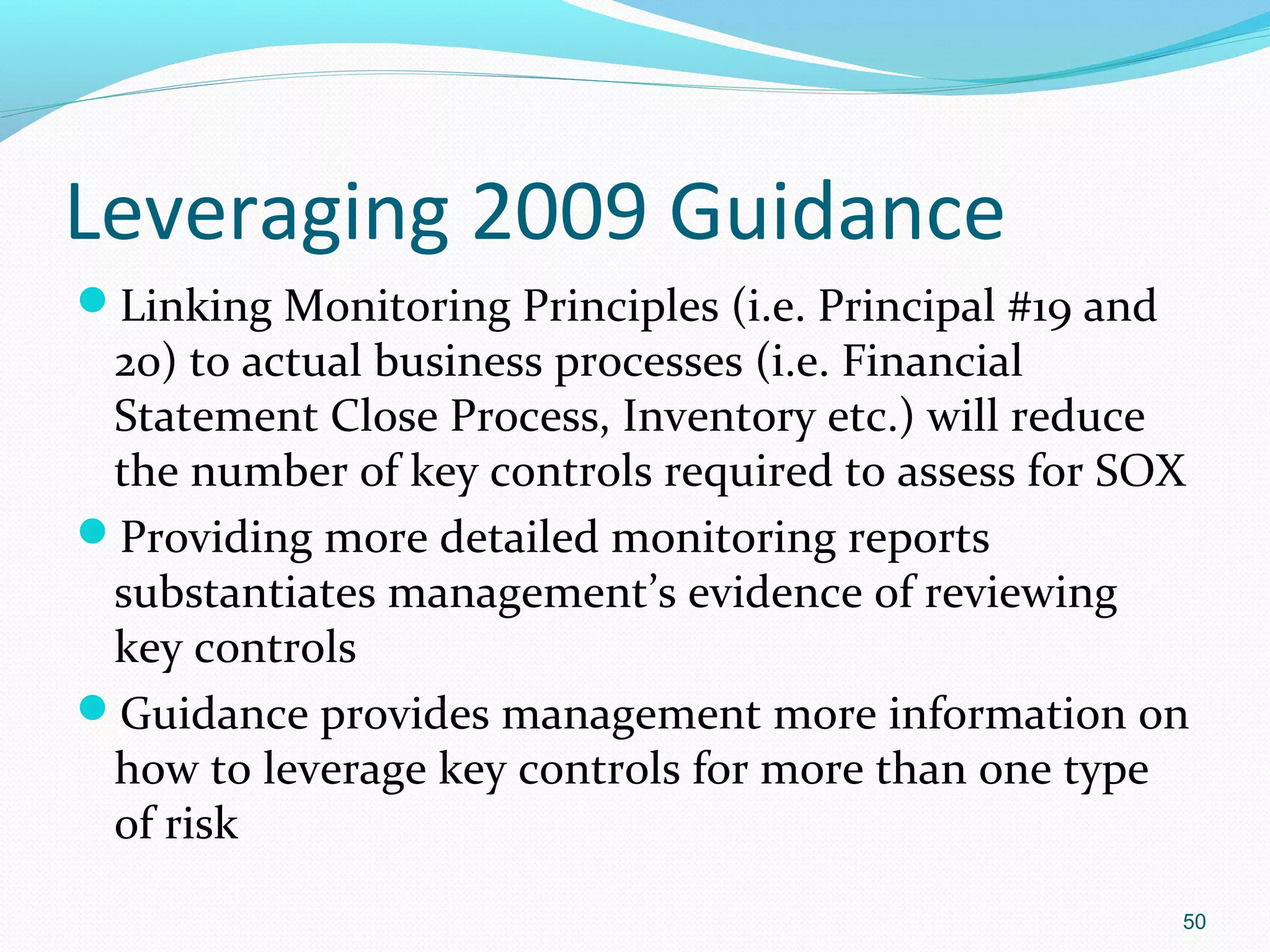

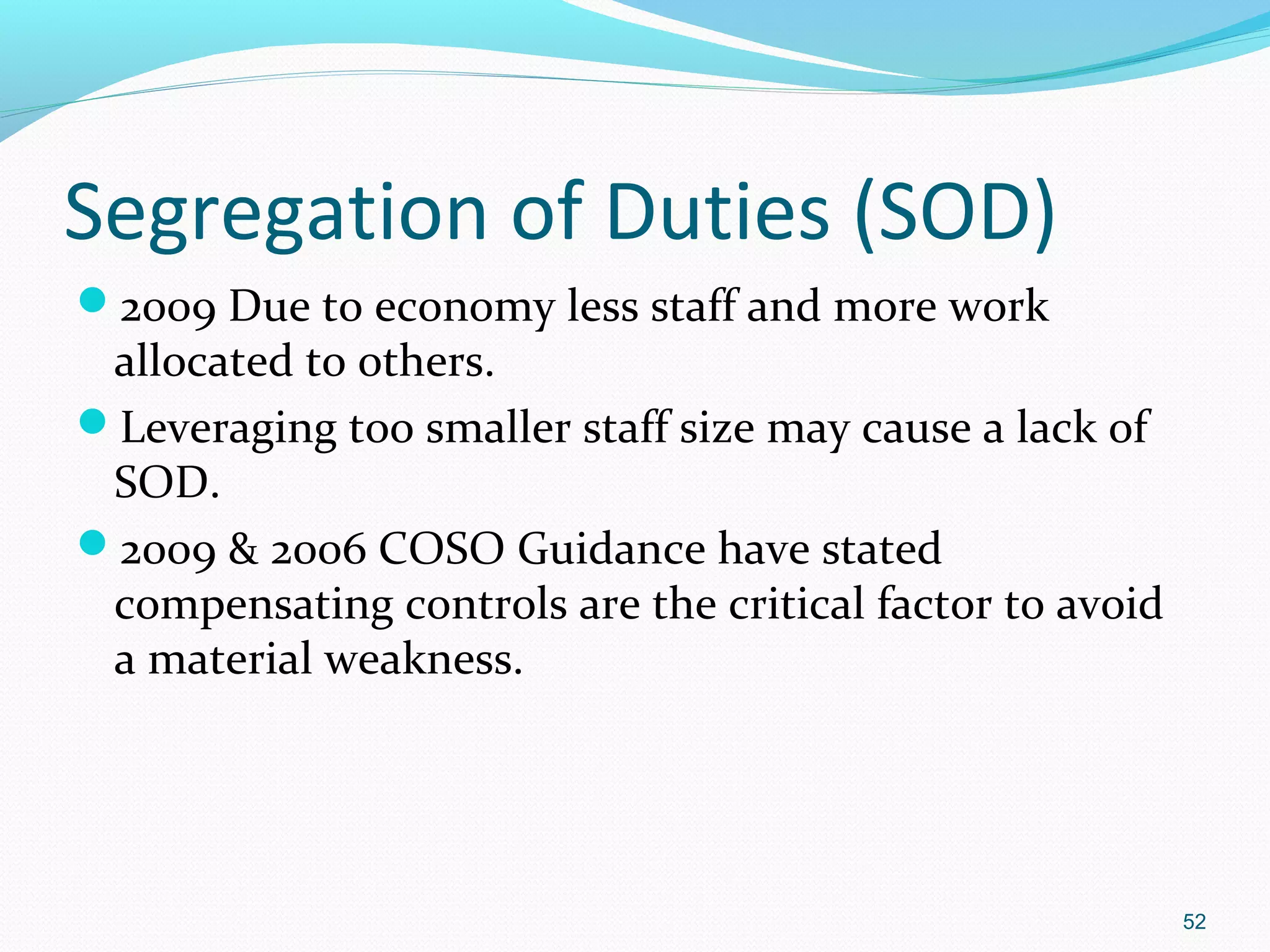

Strategies for reducing key controls through effective monitoring and addressing segregation of duties.

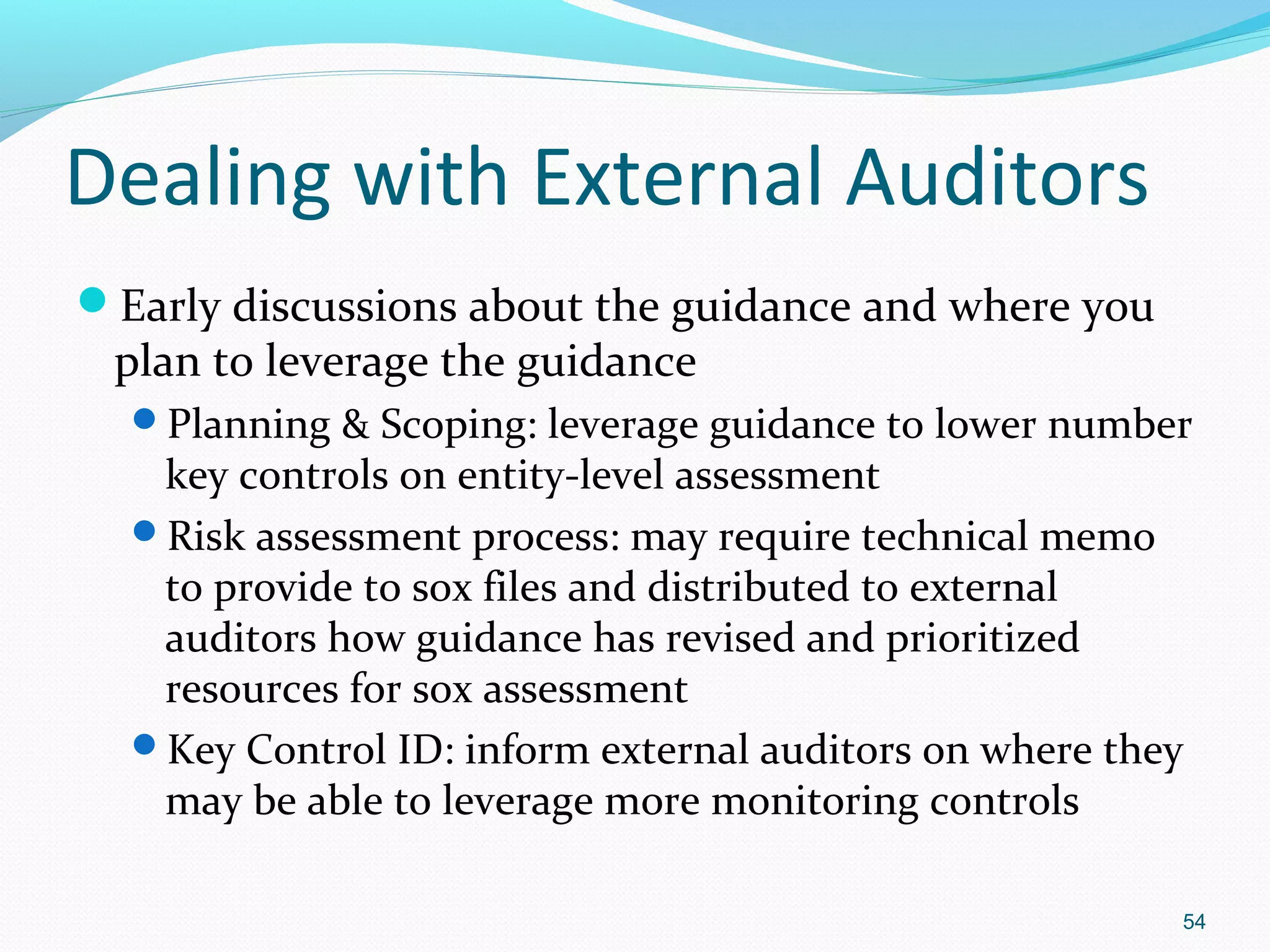

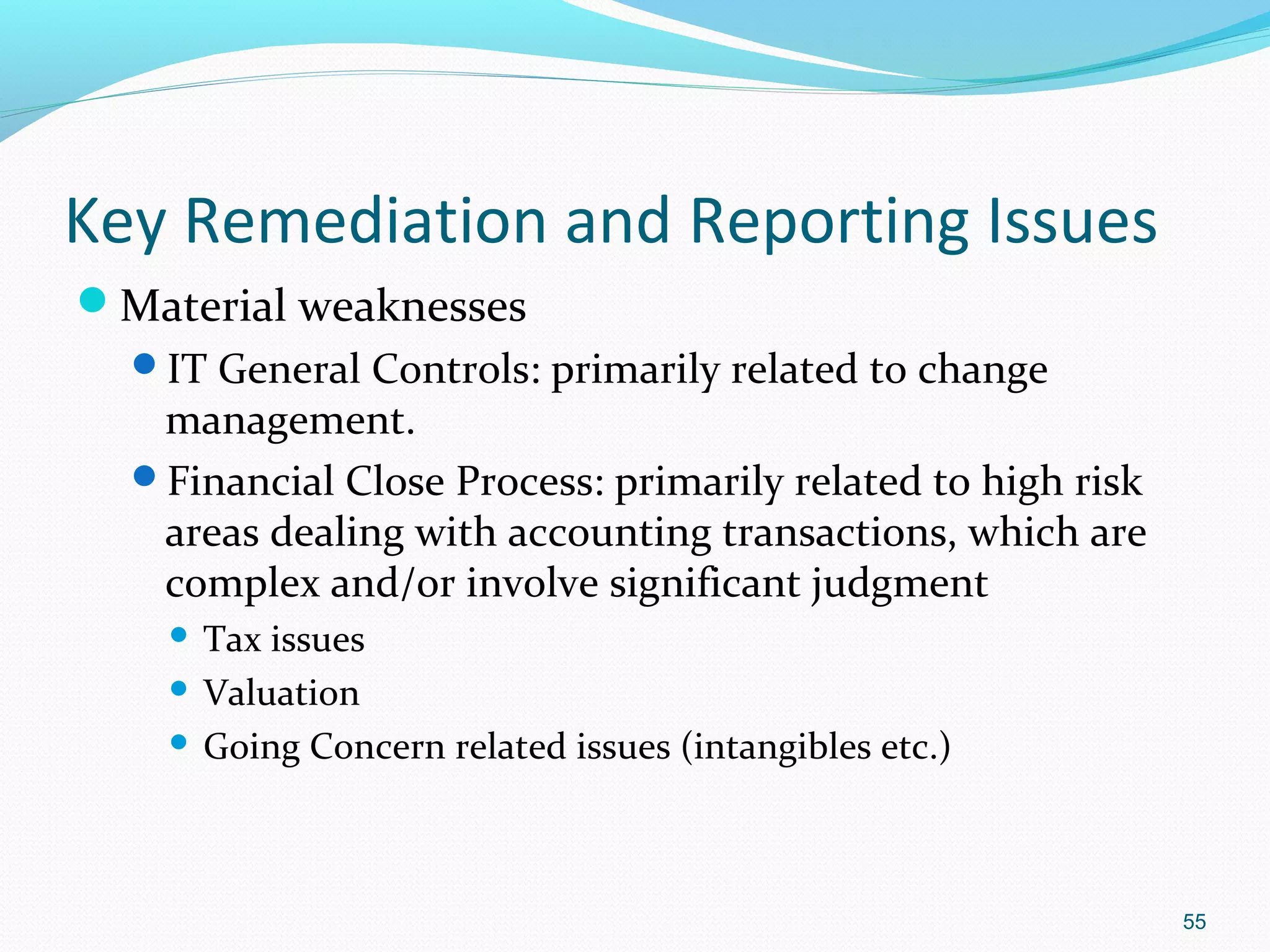

Approach to collaborating with external auditors regarding COSO guidance, key controls, and remediation.

End of presentation with contact information for further queries.

![Financial services intermediaries quality assurance and tcf questionnaire[fsa]](https://cdn.slidesharecdn.com/ss_thumbnails/financialservicesintermediaries-qualityassuranceandtcfquestionnairefsa-110303043559-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)