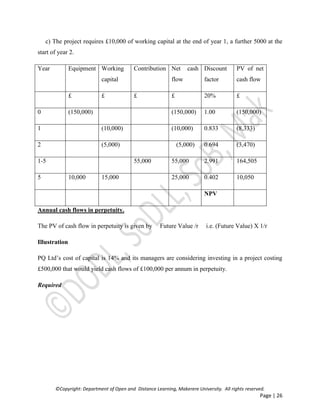

This document provides an overview of the Corporate Finance course offered by Makerere University. It includes the course description, objectives, learning outcomes, content, teaching methods, and assessment. The course aims to teach students about corporate stakeholders, financial objectives, capital structure theories, investment appraisals, mergers and acquisitions, share/bond valuations, and financial distress. Key topics covered include capital budgeting, cost of capital, capital structure, dividend policy, and company valuation. Students will be assessed through coursework assignments, presentations, tests, and a final examination.

![©Copyright: Department of Open and Distance Learning, Makerere University. All rights reserved.

Page | 25

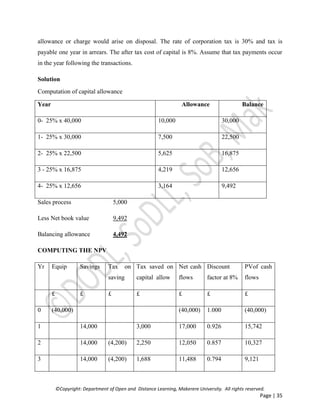

Unit costs would be as follows

£

Direct Labour – 4 hours at £2 per hour 8

Direct materials 7

Fixed costs including Depreciation 9

24

The project would have a five year life after which the new machine would have a net residual

value of £10,000. Because direct labour is continuously in short supply, labour resources would

have to be diverted from other work which currently earns a contribution of £1.50 per direct

labour hour. The fixed overhead absorption rate would be 2.25 per hour (£9 per unit) but actual

expenditure on fixed overhead would not alter:

Working capital requirements would be £10,000 in the first year, raising to £15,000 in the second

year and remaining at this level until the end of the project, when it will all be recovered. The

company’s cost of capital is 20%. Ignore taxation.

Assess whether the project is worthwhile.

Solution

Relevant cash flows are as follows

a) Year 0. purchase of machine £150,000

b) Year 1-5 contribution from new product

[5000 x (32-15)] 85,000

Less contribution foregone

[5.000 X (4x 1.5)] 30,000

55,000](https://image.slidesharecdn.com/e6911798-9877-4c3d-9e97-1f4480721f5e-161220182046/85/CORPORATE-FINANCE-COX-4131-25-320.jpg)

![©Copyright: Department of Open and Distance Learning, Makerere University. All rights reserved.

Page | 28

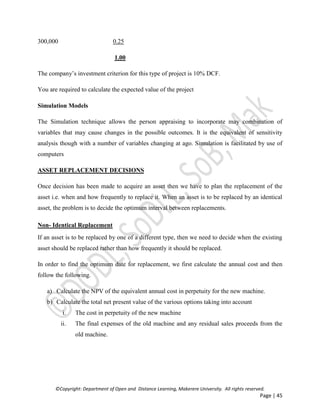

Then use the 2 sets to estimate the IRR using the formula.

IRR = a + [A/ (A-B) X (b-a)]

Where

a is the lower rate b is the higher rate A is NPV obtained using lower rate

B is NPV obtained using higher rate.

OR

IRR = N1R2 –N2 R1

N1-N2

Where N1 is the NPV at rate R1 N2 is the NPV at rate R2 R1 is the lower rate R2 is the higher

rate.

Illustration

A company is trying to decide whether to buy a machine for £80,000 which will save costs of

£20,000 per annum for 5 years and which will have a resale value of £10,000 at the end of year

5. It is the company’s policy to undertake projects only if they are expected to yield a DCF return

of 10% or more, ascertain whether this project should be undertaken.

Solution

At rate of 9%.

Year Cash flow PV factor at 9% PV of cash flow

0 (80,000) 1.000 (80,000)

1-5 20,000 3.890 77800

5 I0.000 0.650 6500

NPV 4300](https://image.slidesharecdn.com/e6911798-9877-4c3d-9e97-1f4480721f5e-161220182046/85/CORPORATE-FINANCE-COX-4131-28-320.jpg)

![©Copyright: Department of Open and Distance Learning, Makerere University. All rights reserved.

Page | 29

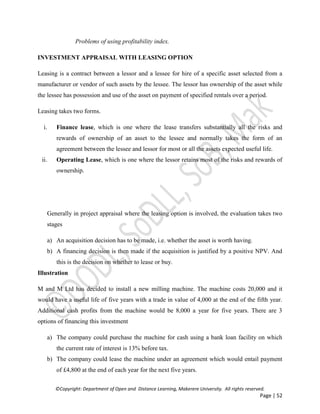

At rate of 12%

Year Cash flow PV factor at 12% PV of cash flows

0 80,000 1.000 (80,000)

1-5 20,000 3.605 72100

5 10,000 0.567 5670

NPV (2230)

Using the formula

IRR = a + [A/(A-B) X (b-a)]

= 9% + [4300/4300 +2230 X 3 %]

= 0.1098 ~ 11 %

OR, using

N1 R2 –N2 R1

N1 – N2

(4300 X 0.12 + 2230 X 0.09)

4300 + 2230 = 0.1098 ~ 11 %

NB

1) IRR of a project with cash flows to perpetuity is given by

Annual inflow x 100

Initial investment

2) NPV is a superior technique compared to IRR. So in case of conflict, the NPV indicator

should be taken.](https://image.slidesharecdn.com/e6911798-9877-4c3d-9e97-1f4480721f5e-161220182046/85/CORPORATE-FINANCE-COX-4131-29-320.jpg)