Downloaded 177 times

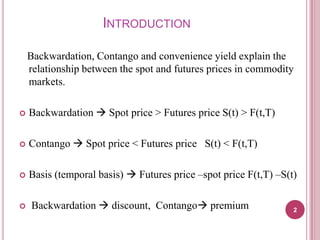

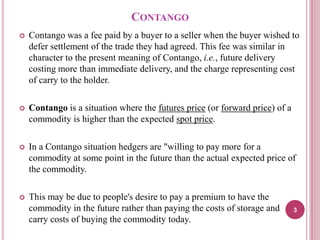

The document discusses the concepts of backwardation, contango, and convenience yield in commodity markets, which describe the relationship between spot and futures prices. Backwardation occurs when the spot price is higher than the futures price, while contango is when the futures price exceeds the spot price, often reflecting carrying costs. Convenience yield refers to the benefits of physically holding a commodity, such as the ability to profit from shortages, which can impact market perception and pricing.