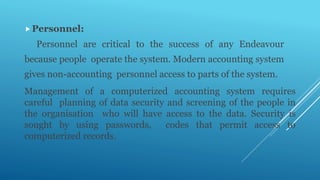

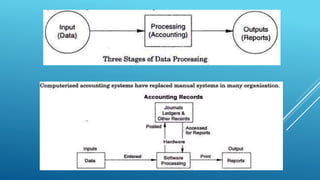

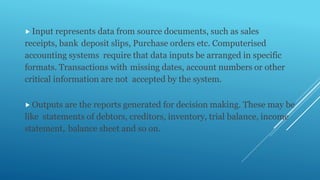

The document discusses the key components of a computerized accounting system: hardware, software, and company personnel. Hardware includes computers, disk drives, monitors, and printers connected through a network. Software programs allow the computer to process transactions and generate reports. Personnel are critical to operating the system and require careful planning around data security and access. Each component is essential for the overall success of the computerized accounting system.