Downloaded 85 times

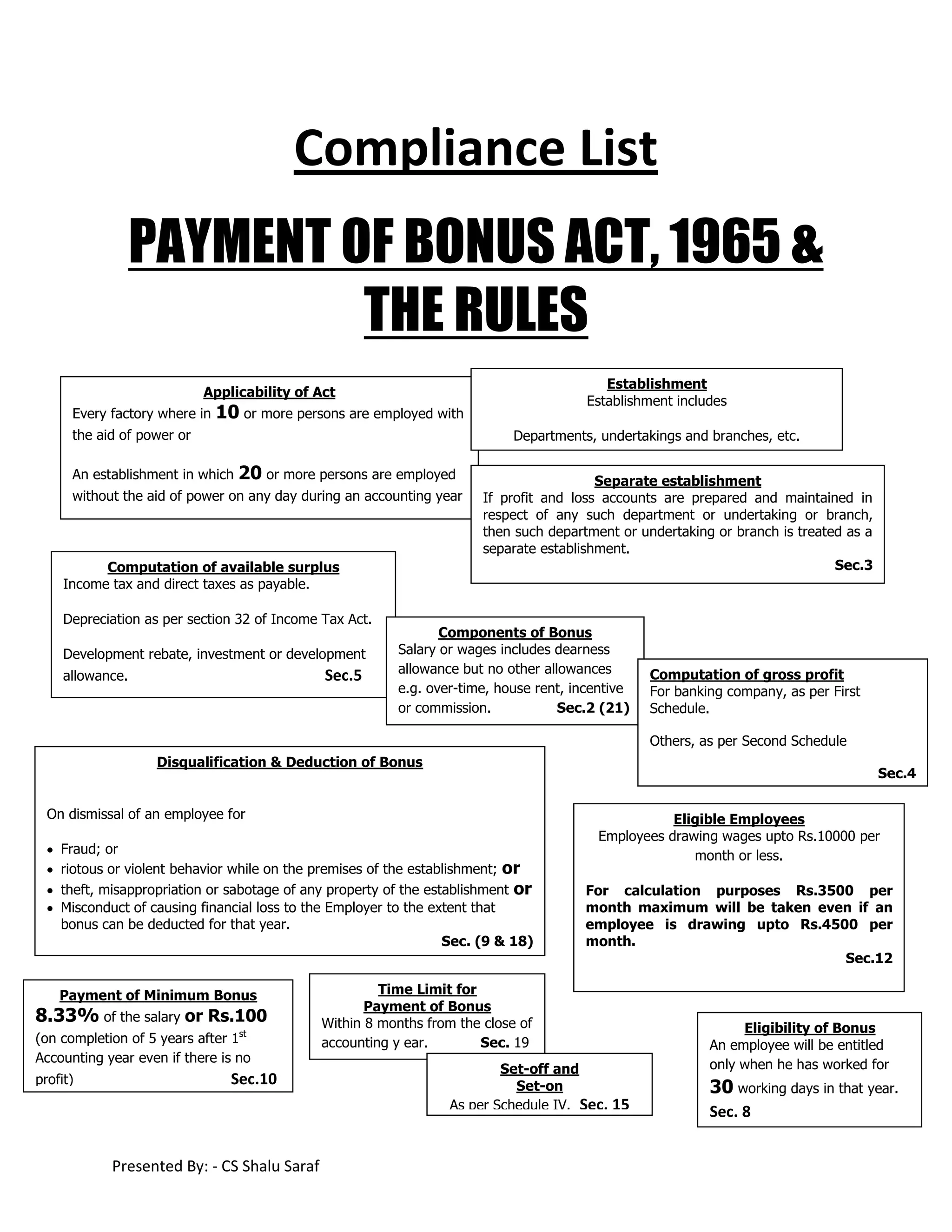

The document summarizes the key provisions of the Payment of Bonus Act 1965 and Rules. It outlines that the Act applies to establishments with 10 or more employees and requires the payment of an annual bonus equivalent to 8.33% of salary or Rs. 100. Eligible employees are those earning less than Rs. 10,000 per month. Bonus must be computed based on the establishment's available surplus and paid within 8 months of the accounting year close. Employers must maintain registers showing bonus computations and payments, and submit an annual return by December 30 each year. Non-compliance may result in penalties up to 6 months imprisonment or Rs. 1,000 fine.