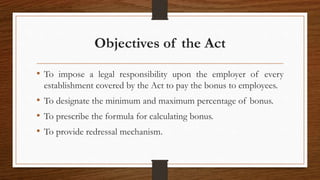

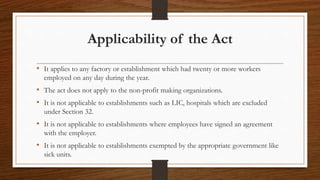

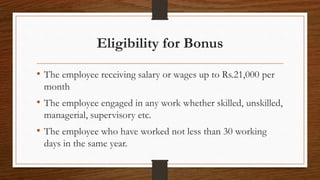

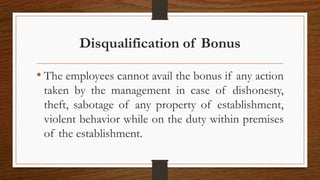

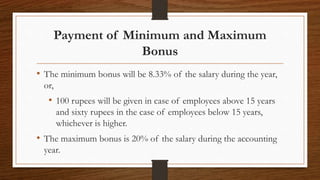

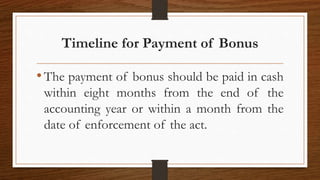

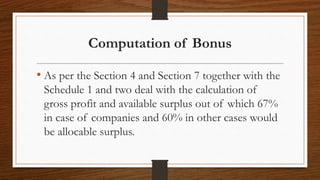

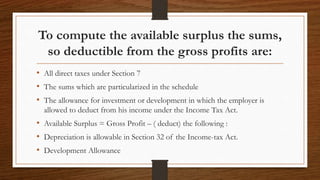

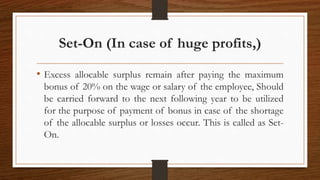

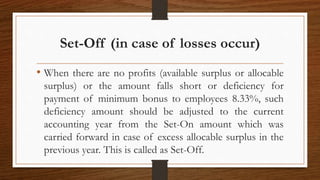

The Payment of Bonus Act, 1965 aims to regulate bonus payments to employees in establishments with 20 or more workers. Key objectives include imposing responsibility on employers to pay bonus, designating minimum/maximum bonus percentages, and prescribing a bonus calculation formula. The Act applies to factories and establishments with 20+ employees but excludes certain organizations. To qualify for bonus, employees must earn up to Rs. 21,000/month and work at least 30 days. Employers who violate the Act face penalties like imprisonment or fines.

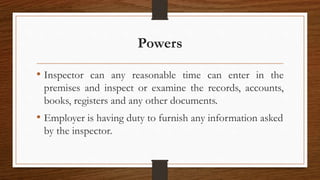

![Inspectors. [Sec 27]

• The Government may, by notification in the official

Gazette, appoint such persons as it thinks fit to be

Inspectors for the purpose of this Act and may

define the limits within which they shall exercise

jurisdiction.](https://image.slidesharecdn.com/paymentofbonusact1-200616135353/85/Payment-of-bonus_act-14-320.jpg)

![Offences and Penalties [Sec 28 & 29]

• For contravention of the provisions of the Act or rules the penalty is

imprisonment up to 6 months or fine up to Rs.1000, or both.

• In case of offences by companies, every person who, at the time the offence

was committed, was in charge of, and was responsible to, the company for

the conduct of business of the company, as well as the company, shall be

deemed to be guilty of the offence and shall be liable to be proceeded

against and punished accordingly: any such person liable to any punishment

if he proves that the offence was committed without his knowledge or that

he exercised all due diligence to prevent the commission of such offence.](https://image.slidesharecdn.com/paymentofbonusact1-200616135353/85/Payment-of-bonus_act-16-320.jpg)