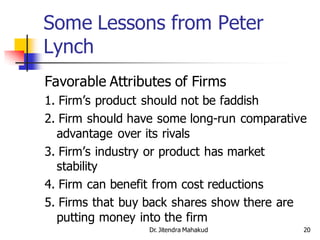

The document discusses company analysis and stock valuation. It provides guidance on analyzing a company's competitive strategies, growth potential, management quality, and financials to estimate intrinsic value. Key steps include conducting a SWOT analysis, comparing intrinsic value to market price, and monitoring assumptions to determine when to sell. The overall aim is to identify undervalued stocks by focusing on long-term prospects and downside protection.

![Awareness of digital currency[1] (1).pptx](https://cdn.slidesharecdn.com/ss_thumbnails/awarenessofdigitalcurrency11-260125155504-b1badee4-thumbnail.jpg?width=640&height=640&fit=bounds)