Downloaded 10 times

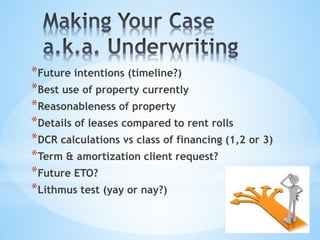

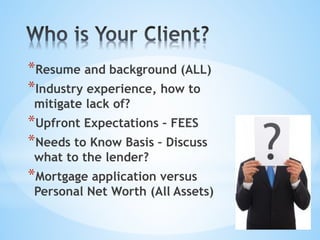

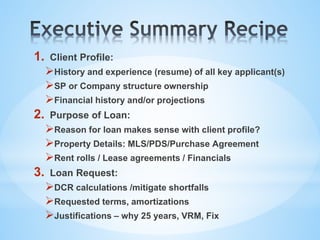

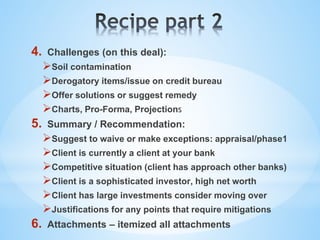

The document outlines key strategies for commercial financing, including identifying potential leads, assessing property value, and preparing necessary documentation for lenders. It emphasizes the importance of building relationships with lenders, understanding client profiles, and addressing potential challenges in loan requests. Additionally, it discusses mentorship and collaboration as vital components for success in the commercial mortgage business.

![Awareness of digital currency[1] (1).pptx](https://cdn.slidesharecdn.com/ss_thumbnails/awarenessofdigitalcurrency11-260125155504-b1badee4-thumbnail.jpg?width=640&height=640&fit=bounds)