Downloaded 303 times

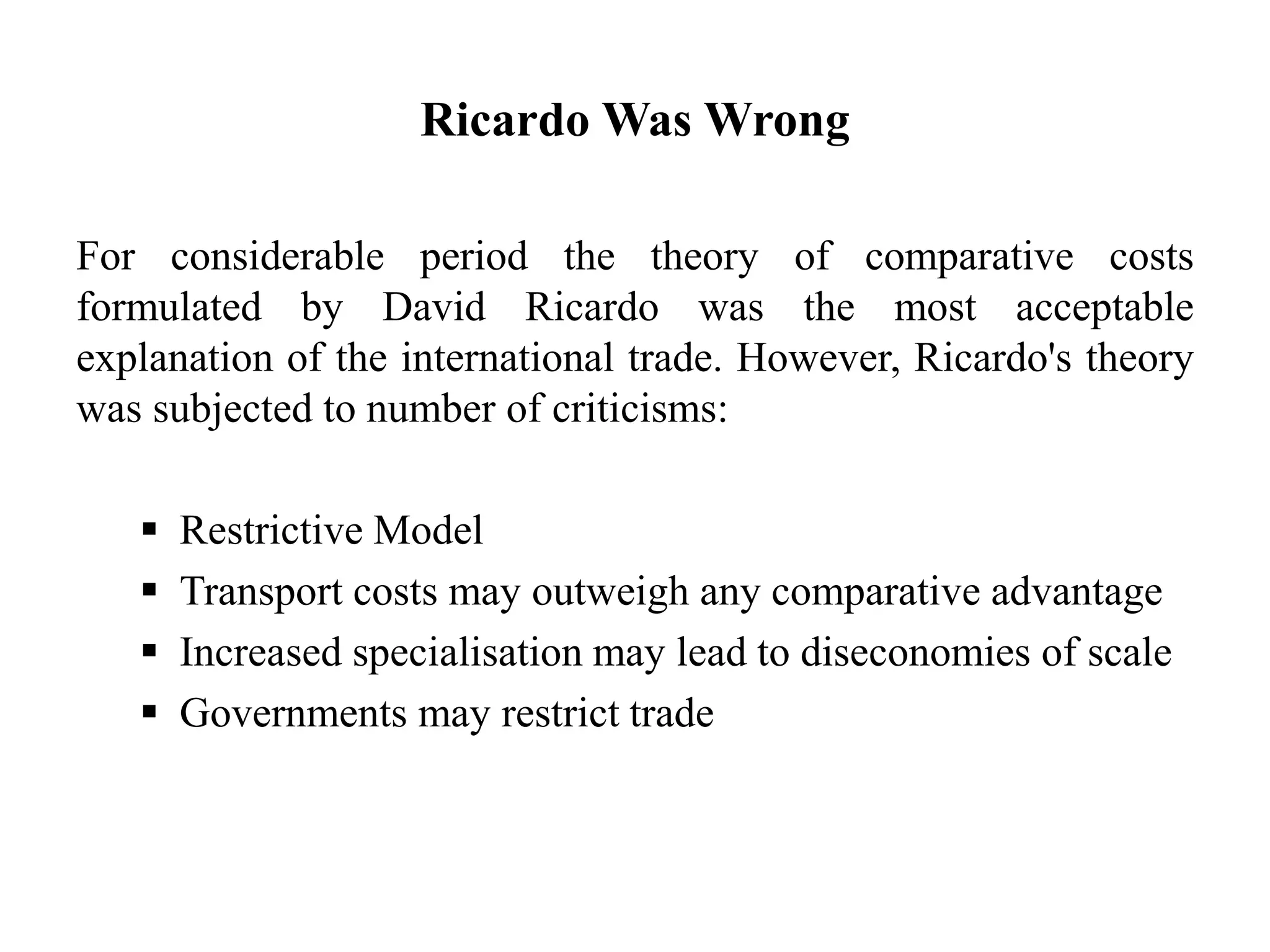

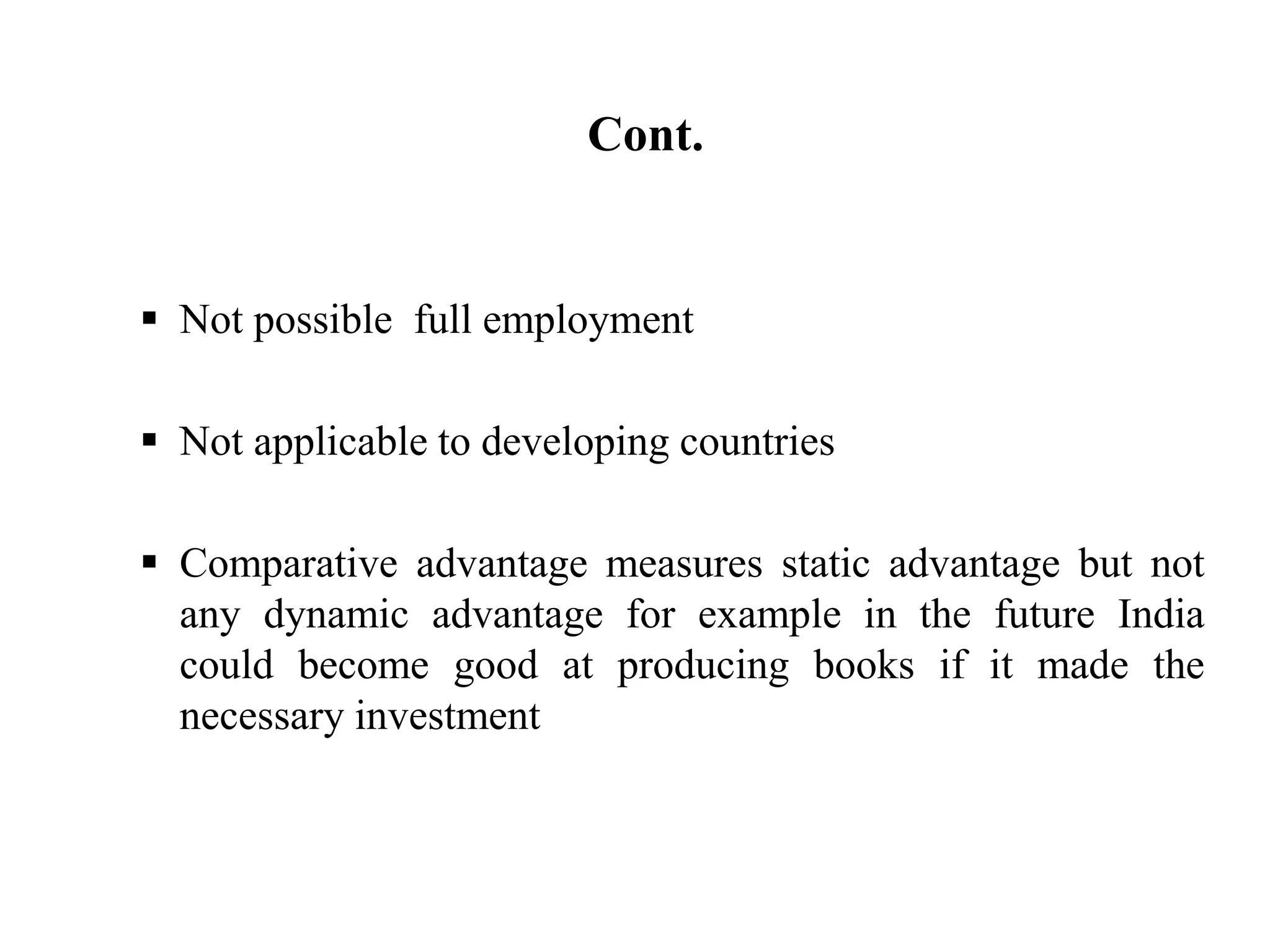

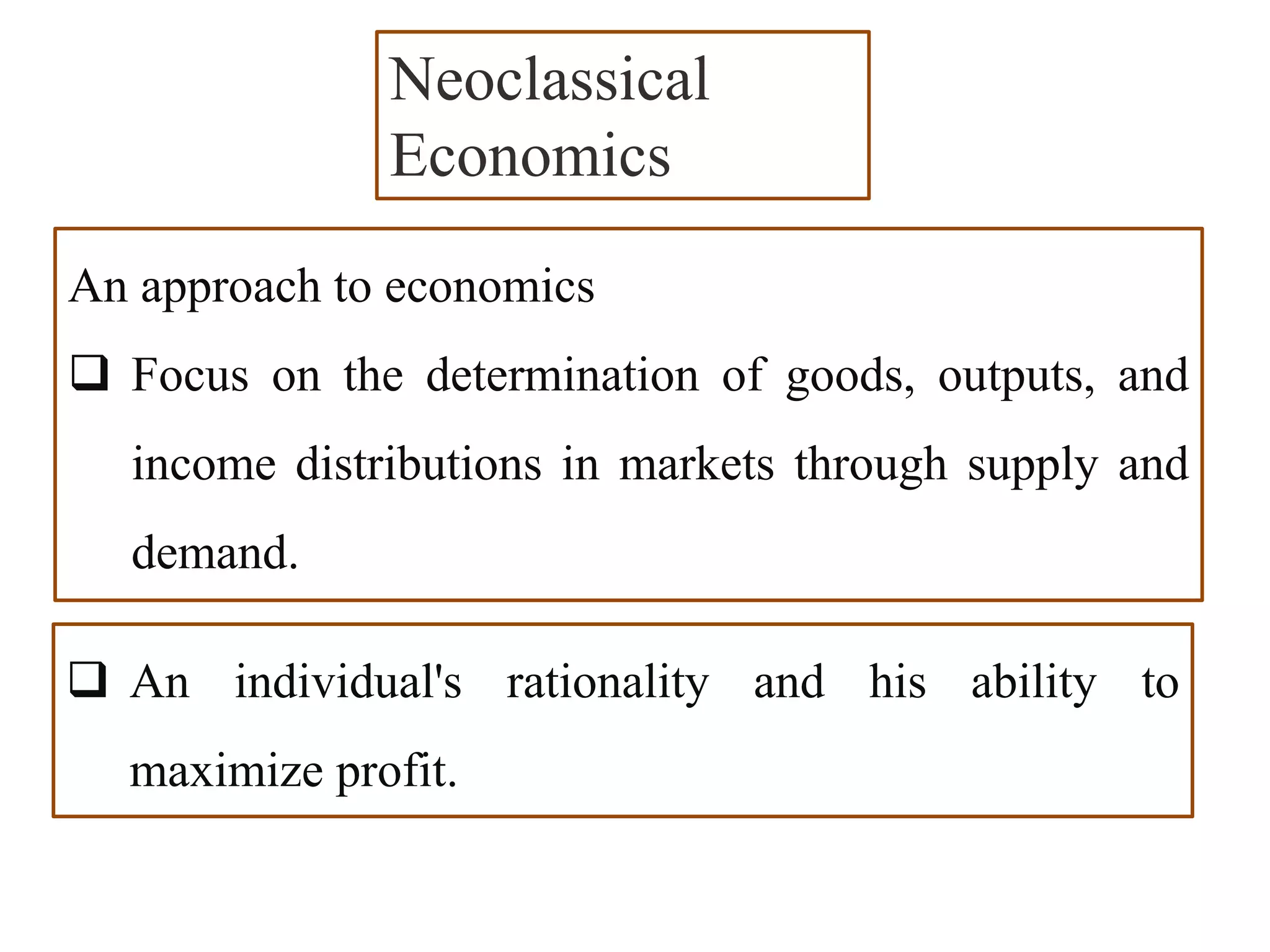

Classical and Neoclassical Economics developed out of the Enlightenment period in Europe. Classical economists like Adam Smith, David Ricardo, and Thomas Malthus analyzed economies based on theories like the labor theory of value, comparative advantage, and populations growth. They viewed economies as self-regulating systems driven by individuals pursuing self-interest. Neoclassical economics built on these foundations with assumptions of rational behavior, market equilibrium from supply and demand, and utility maximization. Both approaches remain influential but face criticisms like oversimplifying human behavior and the real-world complexity of economies.